Deep Dive: Buying the Network for Peanuts – Additional Thoughts on Tiger Brokers

From CAC to Churn and Lifetime Value: A Valuation Exercise

I have been long Tiger Brokers for a few months now. If you have followed my work, you know I have covered this company extensively in several previous deep dives, which I will link below:

2026-01: Investing in China When the Rules Are Changing: Opportunity, Illusion, and Tail Risk

Robinhood’s Entry into Singapore: Assessing the Competitive Threat to Tiger Brokers and Futu

Despite all the noise surrounding anything China-related, and despite the underwhelming share price performance, I still believe it is one of the most inefficiently priced stocks in all of Asia right now.

Most investors see a volatile fintech play. The “Robinhood of Asia,” which completely misrepresents the business we are looking at.

I see something else entirely. A brief discussion in our community this morning sparked a new perspective for me, which I wanted to write about.

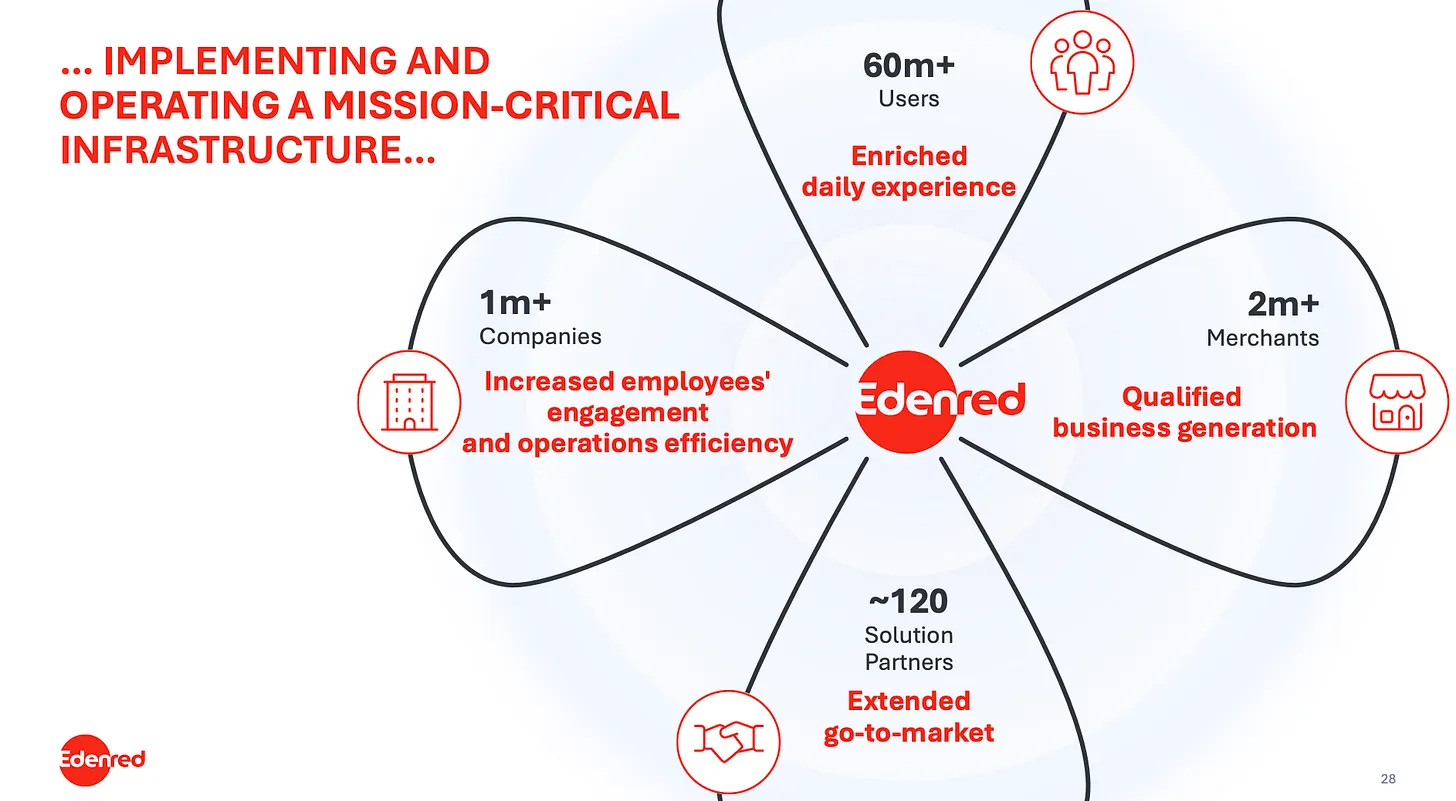

Tiger being a prime takeover target at a roughly $1B market cap has crossed my mind before. But today, for some reason, I was immediately reminded of a valuation framework I applied to Edenred recently (in the article linked below; that buy worked out quite well from those levels so far).

Portfolio Update: Four Recent Transactions

Active stock picking often involves the recalibration of capital toward the highest-conviction ideas available.

In that analysis, I argued the market was completely ignoring the replacement cost of the underlying network (merchants, users, corporate clients).

It turns out that when you apply that same logic to Tiger, the math becomes similarly impossible to ignore.

This is not a traditional discounted cash flow exercise. It is a look at what the business is actually worth to a strategic buyer today. It’s another lens to illustrate the massive mispricing in Tiger’s stock.

If a massive financial institution wanted to replicate Tiger’s footprint in Singapore or Hong Kong, they couldn’t just snap their fingers. They would have to spend a lot of money (and I’ll share my best estimate in this analysis). They would have to fight for every single user.

This replacement cost lens provides a massive, invisible floor for the stock that the current market price seems to completely disregard. I also looked at churn and valued the Up Fintech funded account base on an LTV basis. This was fun. I hope you enjoy the analysis.

Disclaimer: I own a lot of UP Fintech stock (relative to the rest of my portfolio). The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

If you’re unsure about what you get, here’s an overview of some of the companies we covered in a little over a year: