You can read this article entirely for free. If you find value in this research, consider becoming a Premium Member to unlock our full archive and join our growing circle of investors (I highly recommend checking out “The Library” to see what’s inside; you can find it right on the homepage).

Why join the community, you may ask? Our library is fast approaching 70 comprehensive deep dives, providing institutional-level research on some of the world’s most fascinating businesses. Most recently, we’ve dissected companies like Grab Holdings ($GRAB), Fair Isaac ($FICO), and Topicus.com ($TOI).

Compound with René is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

As a member, you get:

Complete Access: Every deep dive in our library (65+ and counting).

The WhatsApp Community: Real-time discussion and networking with like-minded investors.

Incredible Value: Full access to all of this for less than $1/day.

If you want to see the level of research we provide before committing, the following deep dives are free to read:

InPost ($INPST)

Monday.com ($MNDY)

DigitalOcean ($DOCN)

Novo Nordisk ($NVO)

It is finally official. After months of signaling its intentions to expand into the Asia-Pacific region, Robinhood has secured in–principle approval (IPA) from the Monetary Authority of Singapore (MAS) to offer brokerage services.

The news, which broke on April 23, immediately sent ripples through the market, and I noticed that Tiger Brokers’ stock felt the weight of this development almost instantly (ending that day down 6-7%).

For an investor in UP Fintech, who follows the Asian fintech space closely, this wasn’t exactly a surprise, but it certainly represents a fundamental shift in the landscape. I have watched Robinhood carefully navigate the US and European markets, and their arrival in Singapore marks a significant escalation in the war for the retail investor’s wallet in this part of the world.

The immediate reaction from the market was telling. As highlighted, Tiger Brokers was down significantly following the announcement, which is not exactly surprising given the negative momentum of the stock this year.

However, in contrast to prior 1-day -6-10% stock price moves (there have been many recently), I think this was the first time in a while that we saw “major news” that actually required a serious pause for reflection for those invested in brokerage businesses with Asia exposure. While some might dismiss this as mere noise, I believe the arrival of a player with Robinhood’s capital and brand recognition has in fact fundamental significance for the incumbents. This is a company that effectively pioneered commission–free trading in the West and forced some legacy giants to change their entire business models. Now, they are setting up their regional headquarters in the Lion City.

The in–principle approval itself is quite comprehensive. It covers the trading of securities, exchange–traded derivatives, custody services, product financing, and collective investment funds. This is not a limited trial or a niche product launch – it is a full–stack brokerage play. Patrick Chan, who heads Robinhood’s Asia operations, noted that Singapore’s regulatory environment and high digital adoption make it the ideal hub.

I agree. But while the market panicked, I found myself asking whether the threat to existing players is truly as existential as the stock price movements suggest.

From my perspective, the net impact is likely a slight net negative in the short term due to the sheer intensity of the competition. Robinhood isn’t just bringing an app; they are bringing a massive balance sheet and a subsidiary, Bitstamp Asia, which already holds a Major Payment Institution license. This means they are ready to offer a unified ecosystem of traditional securities and digital assets right out of the gate.

Get 3 FREE GIFTS when you subscribe: 📈 Valuation Spreadsheet 📚 eBook: Investing Visualizations 💡 eBook: 250 Thought-Provoking Quotes - Join 4,000+ subscribers.

However, as I will outline below, I am not losing sleep over this development. I have found that in the world of Asian brokerages, the market often overestimates the speed of disruption while underestimating the stickiness of existing platforms.

I want to dig deeper into why I think the “Robinhood threat” might be more nuanced than the headlines imply.

Disclaimer: I own UP Fintech shares. The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

Why Stickiness and Segmentation Matter

The market’s immediate reaction to the Robinhood news was a classic example of “shoot first, ask questions later” – investors were pricing in a zero–sum war for the Singaporean retail market. But if we pull back the curtain, the competitive threat looks far less existential. The reality is that the digital brokerage space in Asia is not a monolith, and Robinhood is entering a market that has already been carved up by a few very sophisticated incumbents who have spent years moving up the value chain.

One of the most significant reasons I am not concerned about a mass exodus from Tiger or Futu is the strong switching cost embedded in most brokerage business models. Let me just share what I wrote in my deep dive on the industry last year:

“When you open a brokerage account, you’re signing up for a long-term relationship. You link your bank accounts, set up recurring deposits, maybe transfer a pension plan, learn the interface, customize your dashboard, and store your trading history.

All of this creates switching friction. It’s not impossible to leave, but it’s a bit of a hassle.

And humans don’t like hassle.

Most people will endure a slightly worse user interface, a marginally lower interest rate, or a tiny increase in fees if it means they can avoid the administrative nightmare of moving everything elsewhere. It’s the same with bank accounts, and the reluctance to switch is arguably strong in the brokerage business. Transferring assets between brokers can trigger taxable events, delays, or even data loss.

There’s also a trust element: once you’ve entrusted your life savings to a platform, the psychological barrier to switching is higher than most investors admit.

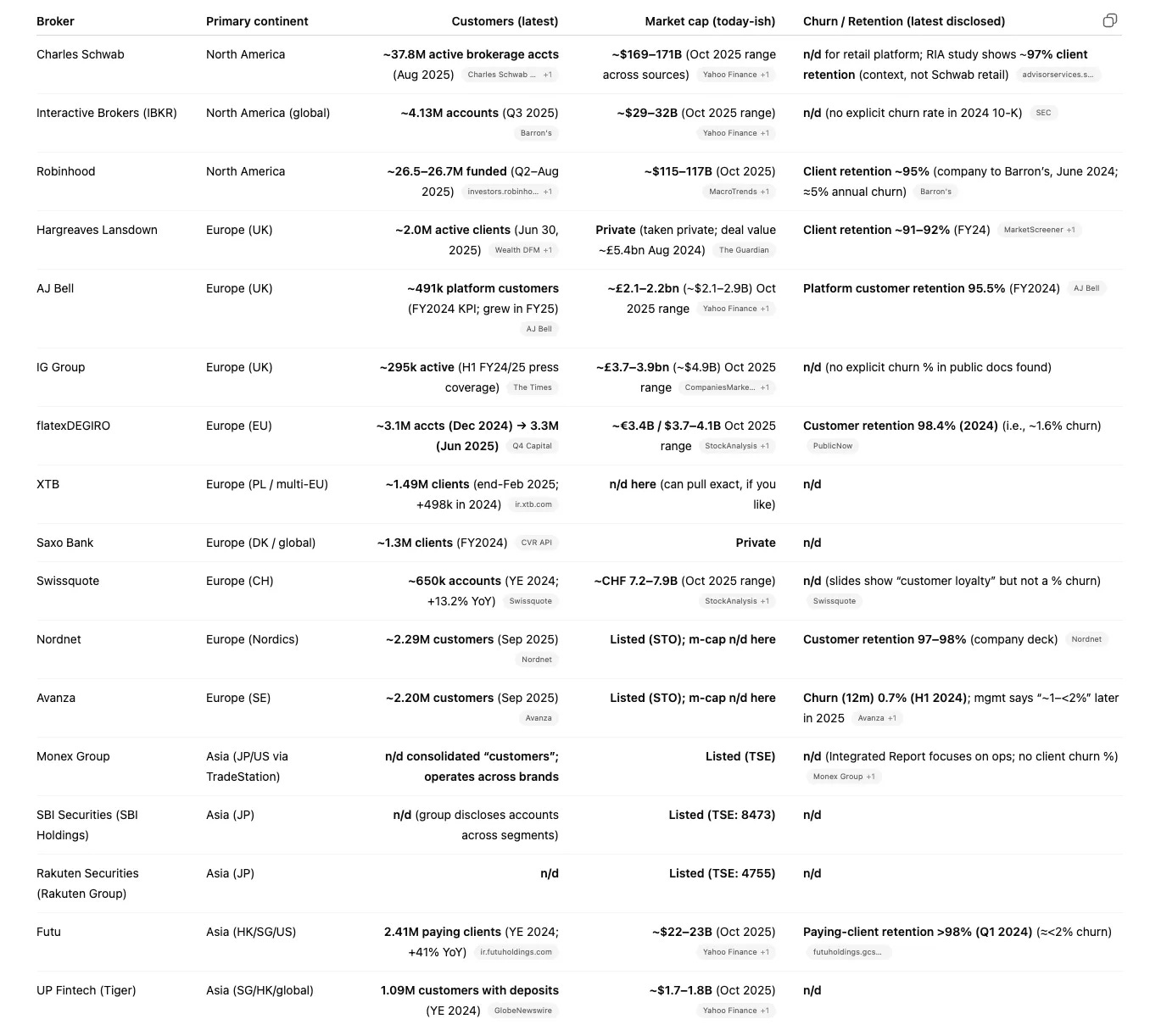

That’s why customer retention in brokerage is off the charts. Nordic brokers like Avanza and Nordnet report retention rates above 97–98%. In the UK, platforms like Hargreaves Lansdown or AJ Bell are typically in the 91–95% range. Even discount platforms like flatexDEGIRO or Futu report similar figures. Annual churn of 2–9% might sound trivial, but in business-model and business economics terms, it’s transformative. It means that for every hundred clients acquired, over ninety are still around a year later – and most of them will still be there five or ten years from now, if not longer.

Here’s an overview of some well-known brokerage businesses and their corresponding churn/retention rates:

Moreover, another reason for not being overly concerned is the stark difference in the actual profile of the users. If you look at Robinhood’s most recent full–year results for 2025, their average assets under custody (AUC) per funded customer sit at approximately $12,000. While that is a record high for them, it pales in comparison to what we see with the Asian leaders. Tiger Brokers has been quite vocal about its focus on higher quality users – depending on the regions, users with account balances of >$40,000.

This is a massive discrepancy. It tells me that while Robinhood is still fundamentally a platform for the mass–market Gen Z retail trader, Tiger and Futu’s Moomoo have successfully “graduated” their user base into the higher–quality, affluent segment.

When I talk to seasoned investors in Singapore, they aren’t looking for just a slick interface; they want deep technical tools, comprehensive wealth management options, and reliable access to Hong Kong and China markets.

I believe that you aren’t going to convince a client with a $70,000 portfolio to switch to a platform designed for $300 trades just because the brand is famous.

The Friction of Success and the Stickiness of Ecosystems

Beyond the AUM numbers, we have to talk about the sheer friction of switching brokers one more time. In the brokerage world, the business model is incredibly sticky. It isn’t like switching from Grab to Gojek; there are real costs and administrative hurdles involved. Moving a portfolio often incurs “share transfer” fees that can range from $20 to $100 per counter. While a new entrant might offer to subsidize these costs, the “tax” on your time and the psychological effort of setting up a new account, re–doing KYC, and learning a new UI is a powerful deterrent.

Furthermore, Tiger and Futu have built deep ecosystems that go far beyond simple stock trading. Their revenue streams are much more diversified today compared to just a few years ago.

For instance, Tiger has been aggressively expanding its ESOP (Employee Stock Ownership Plan) management business and its high–quality “Tiger Vault” for cash management. These are products that entrench a user. If your company’s stock options are managed by Tiger, or if you have your entire emergency fund parked in their wealth management suite, the likelihood of you leaving for a new app is remarkably low.

I suspect that Robinhood will find the Singaporean market far more “picked over” than the US market was in 2013. In the West, they were competing against clunky, expensive legacy brokers. In Singapore, they are competing against 2nd–generation digital natives who are already faster, cheaper, and more feature–rich than anything Robinhood has faced as competition elsewhere early on.

The market may have panicked, but I see two different tiers of players hunting two different types of prey.

The Rising Tide Hypothesis – Could Robinhood Be an Unintentional Ally?

I want to pivot to a theory that some might call a bit of a moonshot – and I do too –, though I find it somewhat plausible the more I look at the history of fintech. There is a possibility that Robinhood’s entry into Singapore will not just take market share, but will actually expand the total addressable market in a way that fundamentally benefits both Robinhood and its competitors. I call this the “Graduation Effect.” In the United States, Robinhood didn’t just steal customers from Charles Schwab or Fidelity – it minted millions of new investors who had previously felt priced out or intimidated by the complexity of the stock market.

If we look at the Singaporean market, digital adoption is already near saturation at over 95%. However, there is still a significant gap between “having an app” and “active investing.” Robinhood is a master at top–of–funnel acquisition. Their interface is designed to lower the psychological barrier to entry, making a first trade feel as simple as sending a text message. By bringing their brand of “democratized” finance to Asia, they are likely to attract a cohort of younger, first–time investors who might have found other brokers’ solutions a bit overwhelming.

But here is where it gets interesting for the incumbents. As an investor matures, their needs change. A casual trader who starts with $500 on Robinhood today will, in three years, likely be looking for more sophisticated instruments – things like advanced options strategies, detailed technical analysis tools, and perhaps the ability to trade across more diverse global markets like Hong Kong or mainland China via Stock Connect. If Tiger and Futu continue to aim for higher-quality users, those are technical capabilities they’ll need to continue developing – even though the current tools are by no means comparable to a platform like IBKR (just to be clear).

However, both have spent years refining a platform that caters to the “prosumer” investor. In this light, Robinhood might act as the primary school of investing, while Tiger serves as the university (and IBKR would be considered your PhD thesis). If Robinhood successfully brings 100,000 new retail participants into the Singaporean ecosystem, a significant percentage of those users will eventually “graduate” to a more robust platform once they outgrow Robinhood’s simplified UX.

The Crypto Synergy and the Quest for the Super App

At the same time, we also cannot ignore the Bitstamp angle. Robinhood’s subsidiary, Bitstamp Asia, already holds a Major Payment Institution license from the MAS. This gives them a massive head start in creating a unified “Super App” experience that bridges the gap between traditional equities and digital assets. In a market like Singapore – which has a very high appetite for crypto but a strict regulatory environment – this could be a major draw for the younger demographic.

However, I have noticed that when a platform tries to be everything to everyone, it often loses the specialized edge that seasoned investors crave. Tiger has been very intentional about its pivot toward high–quality users and asset management. By focusing on “K+ users” and sophisticated wealth management solutions, Tiger is positioning itself as a premium alternative. I believe the market is large enough for both a mass–market “entryway” like Robinhood and a specialized “wealth hub” like Tiger. Instead of a zero–sum game where one must die for the other to live, I suspect we are entering an era of market stratification. Robinhood could dominate the “volume” end of the market, while the incumbents will continue to dominate the “value” end.

The wild hypothesis here is that Robinhood might actually be doing the expensive work of customer education for its rivals. Every dollar Robinhood spends on marketing “investing for all” in Singapore is a dollar that helps normalize stock market participation for the masses. In the long run, those educated investors become the prime targets for Tiger’s more advanced, higher–margin services. It is a bold play, but I’ve seen this pattern repeat across multiple industries: the disruptor expands the market, and the specialist captures the mature demand.

The Valuation Gap and the Final Verdict

When I look at the hard numbers, the disconnect between market sentiment and fundamental reality becomes even more pronounced. Investing is ultimately a game of expectations, and for the current incumbents in the Asian brokerage space, those expectations have been beaten down to a level that I find genuinely remarkable. To justify its current valuation, a business like Tiger Brokers doesn’t need to conquer the world; it doesn’t even need to grow at all, and if it maintains even a modest level of growth, I believe the stock should do very well from here.

To learn more about my latest thoughts in this regard, check out this piece:

In sum, I believe the market is making a classic mistake by treating Robinhood’s entry as a “zero–sum” event. Investors see a large, well–capitalized player entering and assume they will cannibalize the entire pie. But as I’ve noted, the “pie” in Singapore and broader Asia is not only growing, it is also splitting into distinct segments. Robinhood’s focus on the mass market and lower–AUM users means they are essentially fighting for a different pool of capital than Tiger, which more recently has successfully positioned itself as a hub for more affluent, higher–quality users. If Tiger doesn’t even need to growth from these prices, and they are currently at a very solid rate, then Robinhood doesn’t just need to be successful for the thesis to not work out from current levels – they would need to actively destroy Tiger’s existing ecosystem to break the investment thesis.

Given the stickiness of these platforms, I find that scenario highly unlikely.

Disclaimer: I own UP Fintech shares. The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

Compound with René is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.