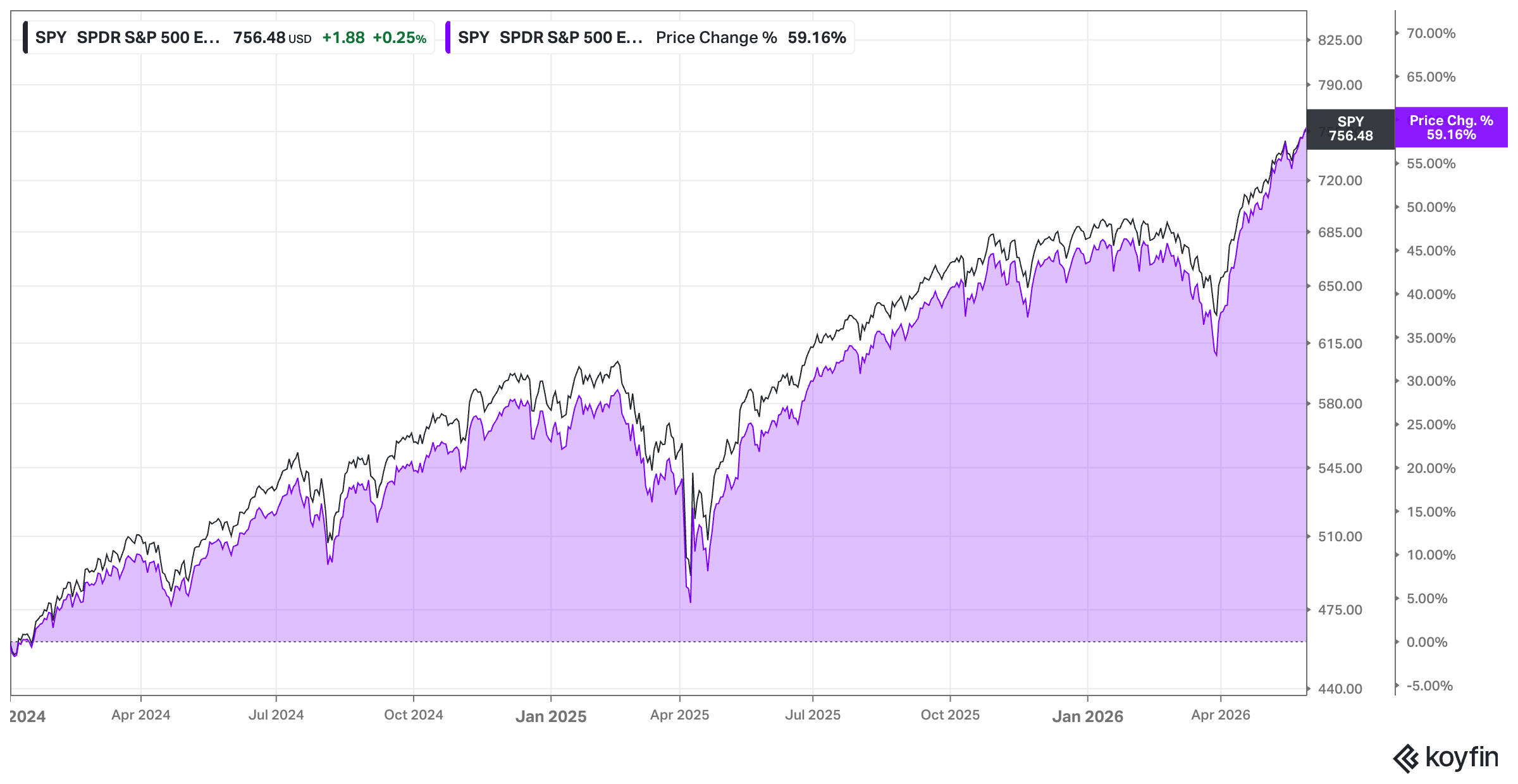

Look at the surface numbers, and the stock market seems absolutely bulletproof. The S&P 500 closed out 2024 up roughly 25%, carried that momentum through another positive year in 2025 (roughly +18%), and is already sitting on an 11% gain year-to-date in 2026.

If you solely track the price developments and financial media headlines, it feels like the party will never end. We’re still dancing.

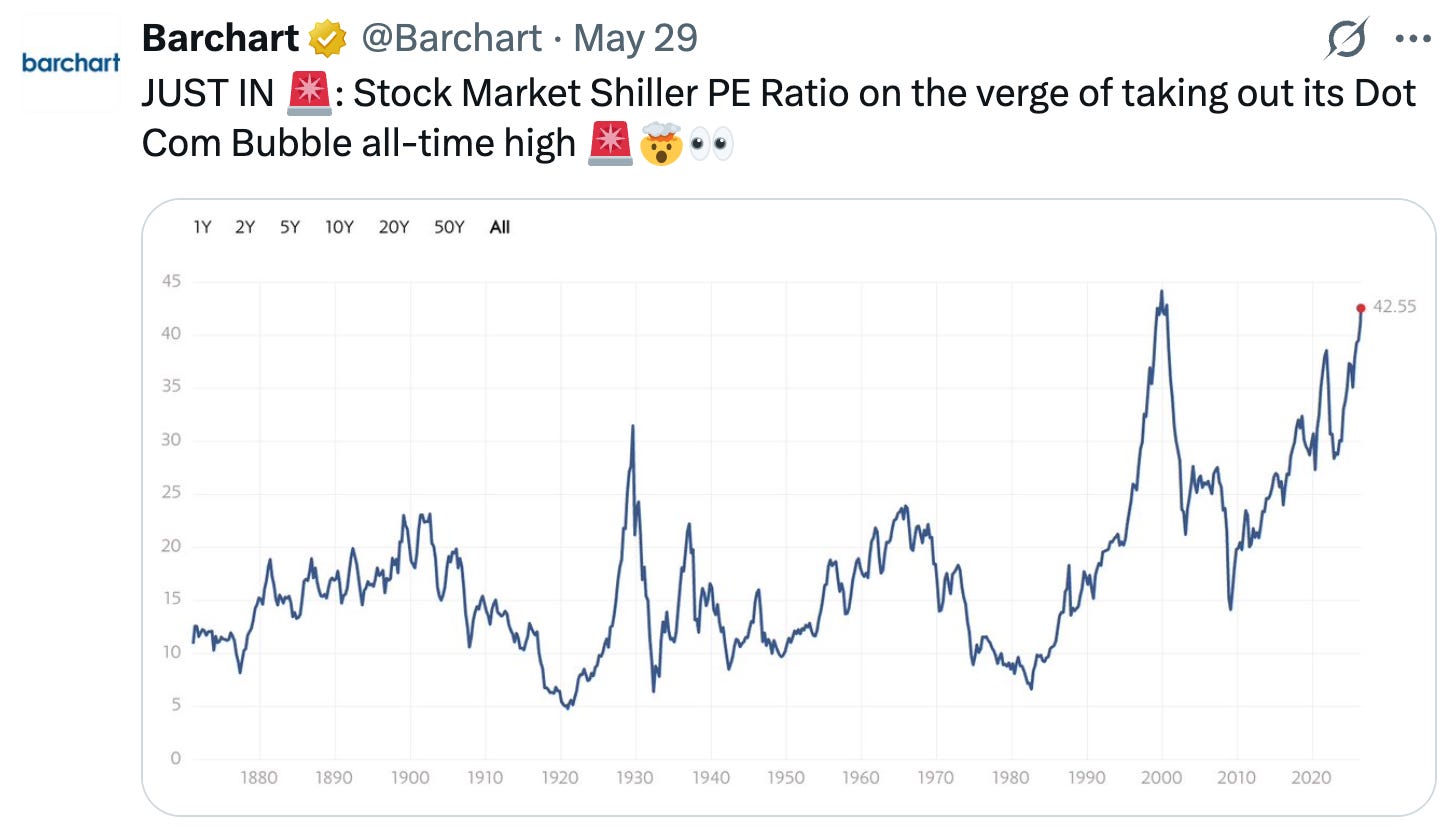

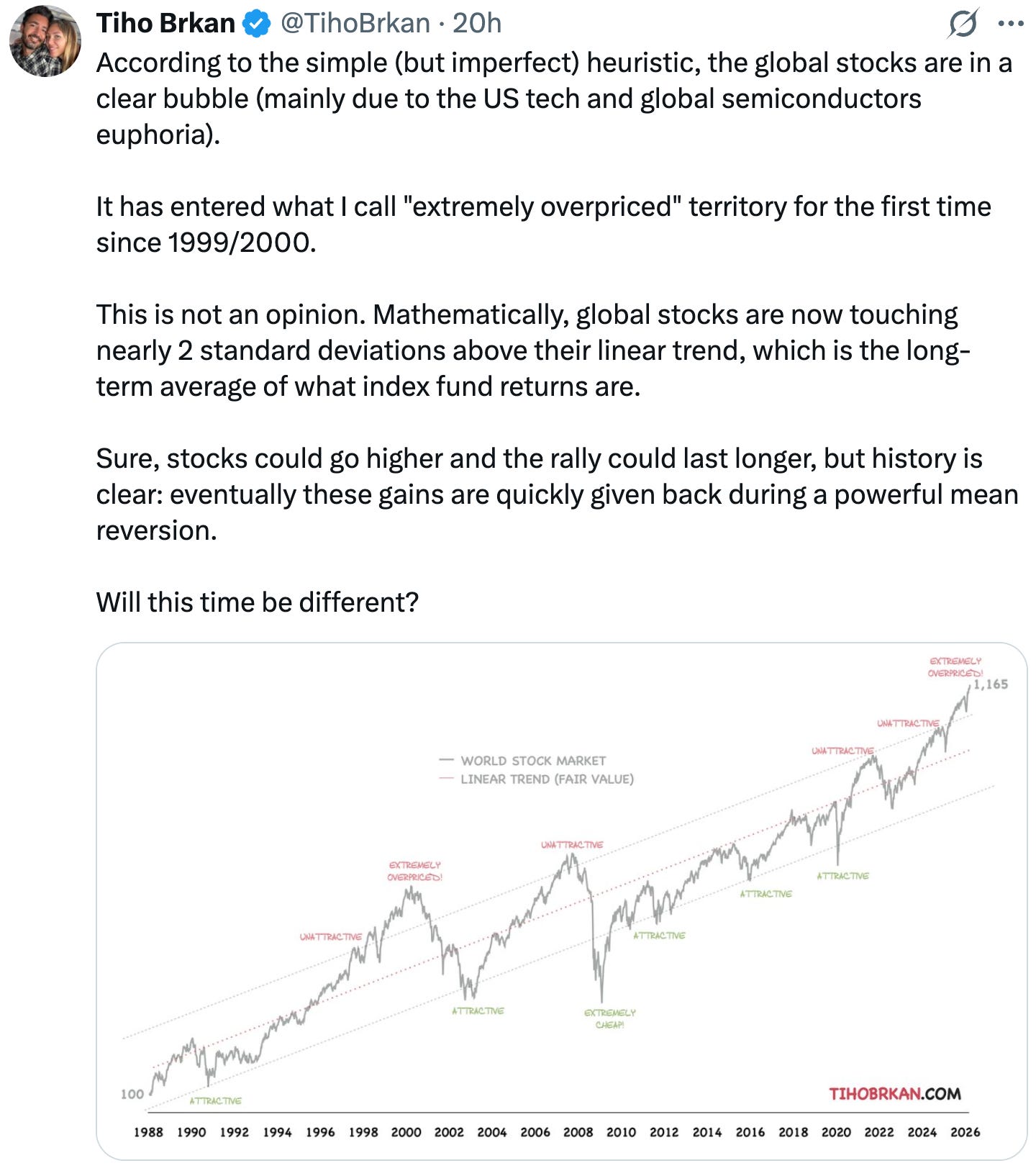

But if you look under the hood, things are starting to look incredibly frothy in my view. Traditional valuation metrics – like the Shiller PE ratio or the Buffett Indicator – are already screaming that equities are historically expensive.

The problem? Valuations are notoriously terrible market timers. Markets can stay irrational and expensive a lot longer than most investors can stay patient. Stock market indicators are by no means crystal balls. You cannot use these indicators to predict what is going to happen in a year or two from now.

Let me repeat: They are NOT stock market timing tools!

This is backed up by this research by YCharts that shows that “of |the] seven leading indicators studied, none have consistently predicted major market declines dating back to 1950. Even the most consistent indicators provided a warning signal for only about half of major declines. “ A major decline in this study was defined as a decline of 10% or greater from the S&P 500’s most recent all-time high

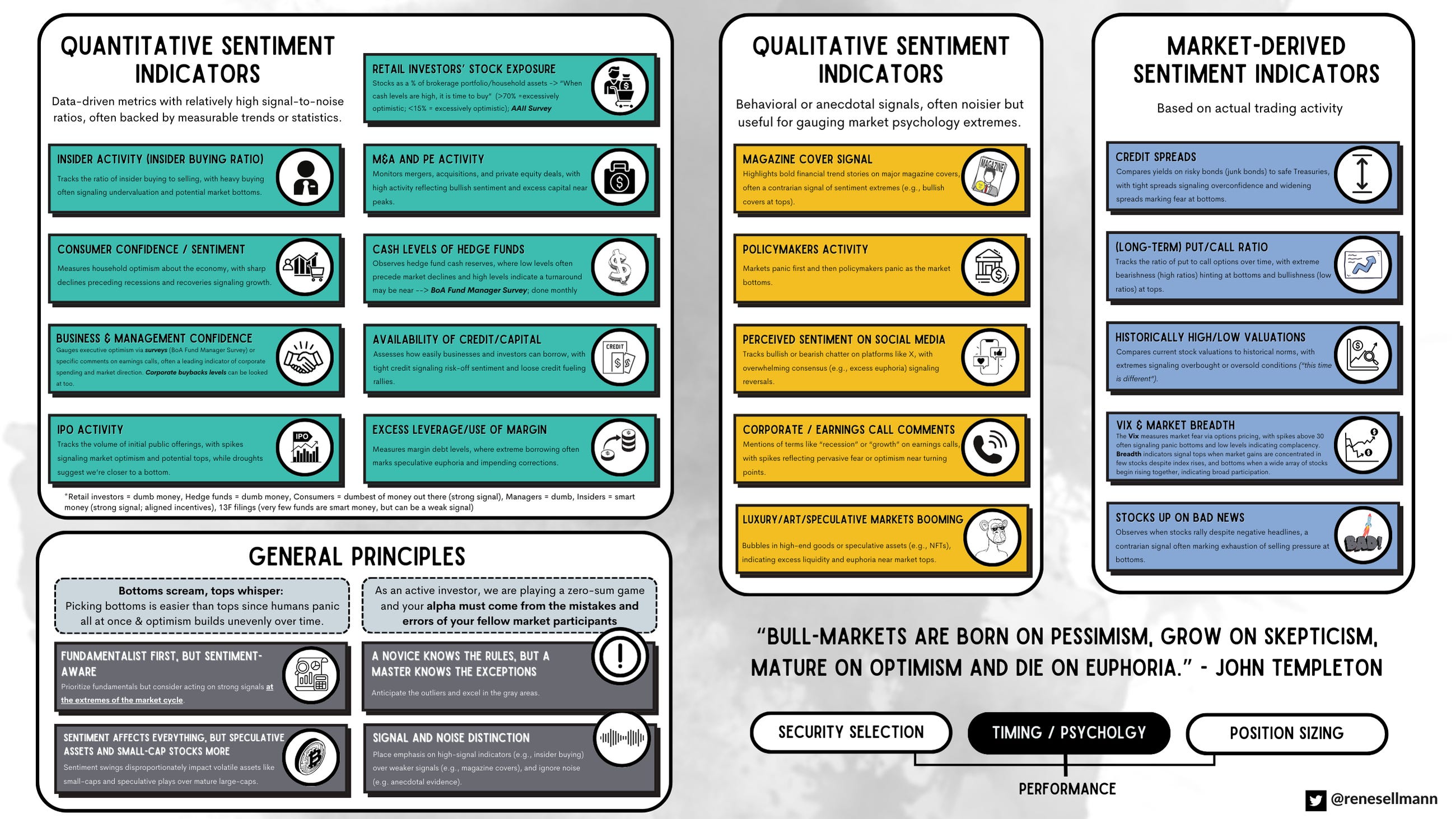

So to spot a true cyclical turn, we have to look past standard metrics and focus on alternative, structural, and behavioral signals. I will once again insert my “Market Sentiment Cheat Sheet” below:

In this post, we are going to break down six unorthodox signs that I’m seeing that I believe are pointing to us being in a late-stage bull market.

And maybe more importantly, towards the end of the post, we’ll explore the investor’s paradox in this market regime: why an overextended index can coincide with an attractive environment for disciplined, fundamental stock pickers.

Disclaimer: The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

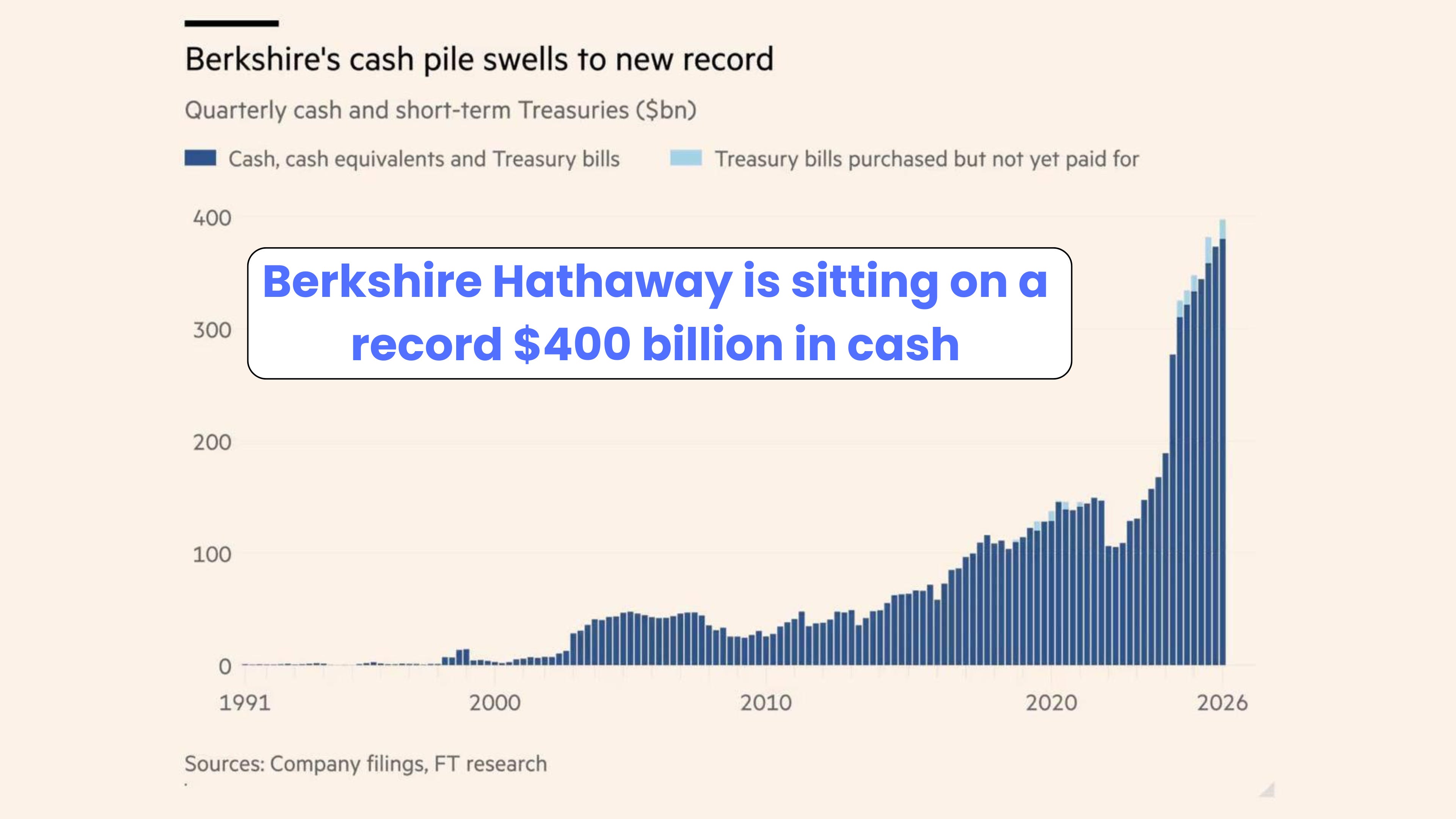

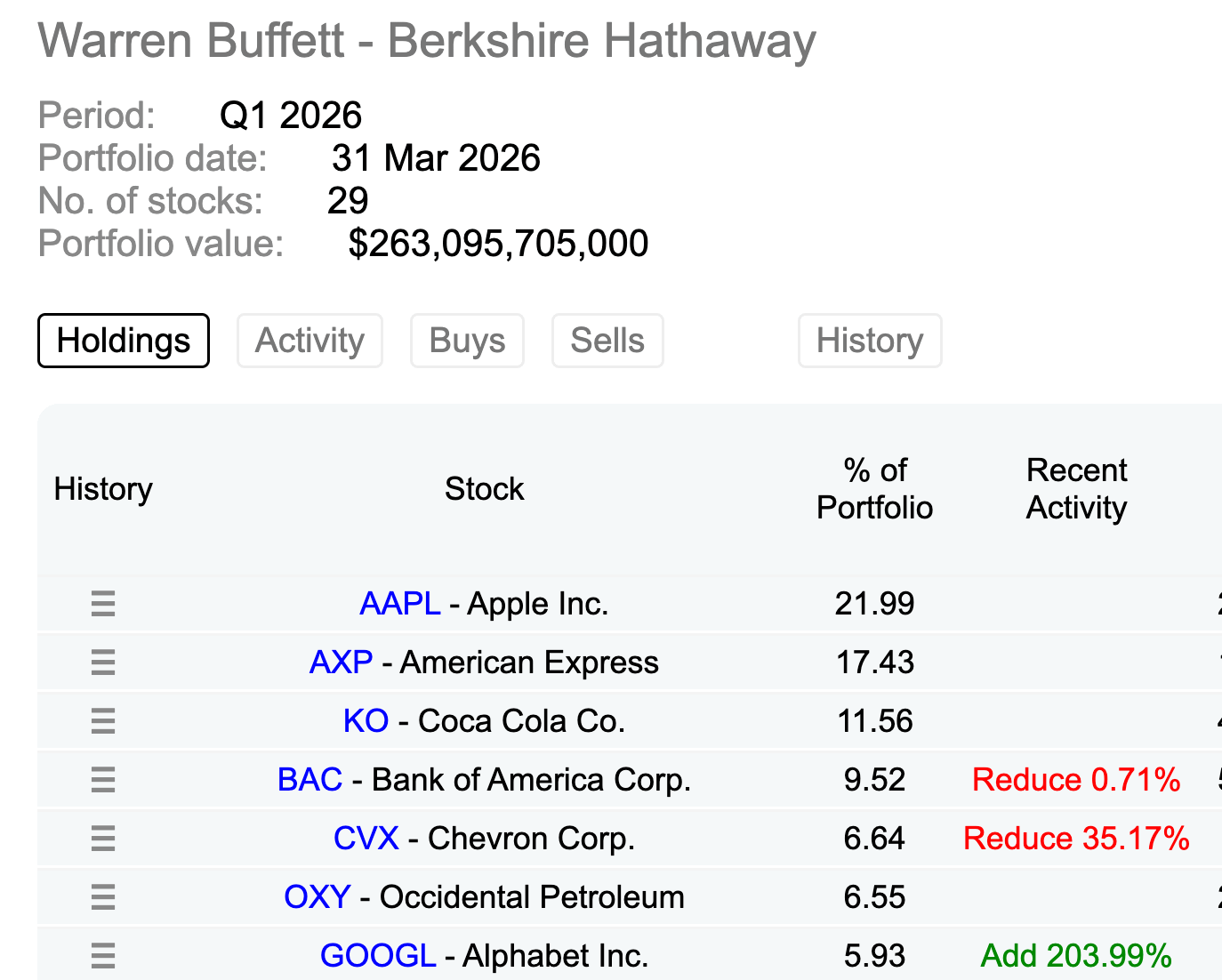

1. The $400 Billion Cash Mountain

The ultimate gauge of market value isn’t a spreadsheet; it’s what the smartest capital allocators in the world do with their money. Right now, Berkshire Hathaway is sitting on an absolutely astonishing cash hoard of around $400 billion as of their latest filings.

Whether you view Warren Buffett (and now CEO Greg Abel) as proficient market timers or simply disciplined buyers, the conclusion is exactly the same: they cannot find anywhere to put this capital to work at reasonable prices.

Aside from a highly surprising, significantly increased stake in Alphabet (Google), …

… and the Monday-announced acquisition of Taylor Morrison for $72.5/share (or an $8.5B enterprise value (premium of roughly 24%)), Berkshire has been hoarding cash, letting their pile climb to vertical, historic records.

When the largest corporate war chest in history refuses to buy because the math no longer makes sense, retail investors should take note. If Berkshire will have a hard time deploying that much capital even during a market crash – Buffett is certainly secretly rooting for a prolonged crash, possibly a lost decade (not another COVID-like flash crash) –, it’s a glaring sign that the broader market has run far ahead of fundamental reality.

2. The Illusion of Market Breadth

When an index hits consecutive records, you naturally want to see a broad army of companies marching upward together.

Right now, that isn’t happening.

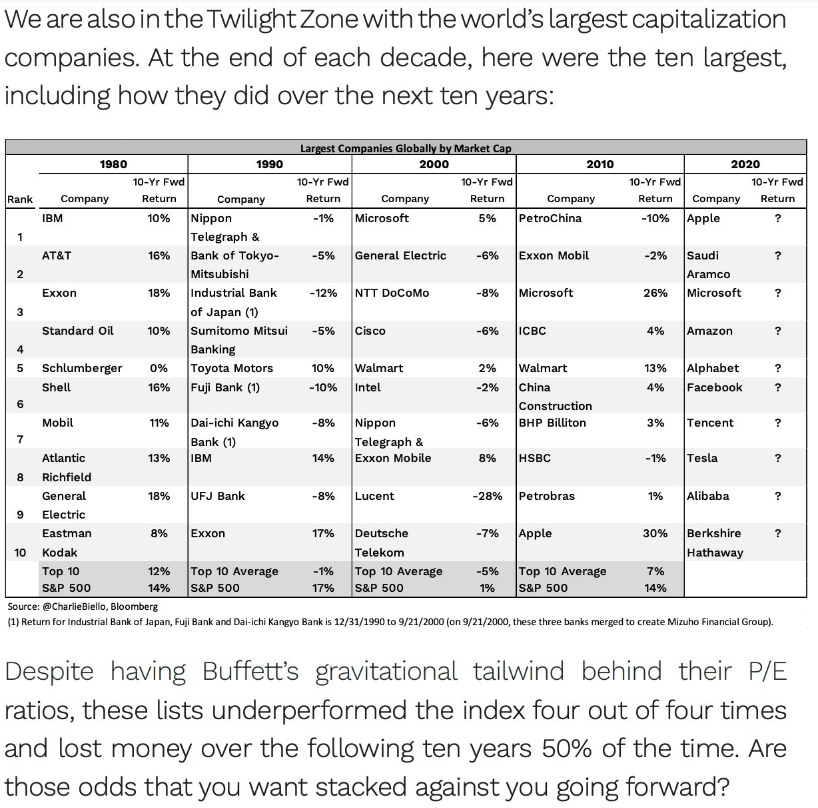

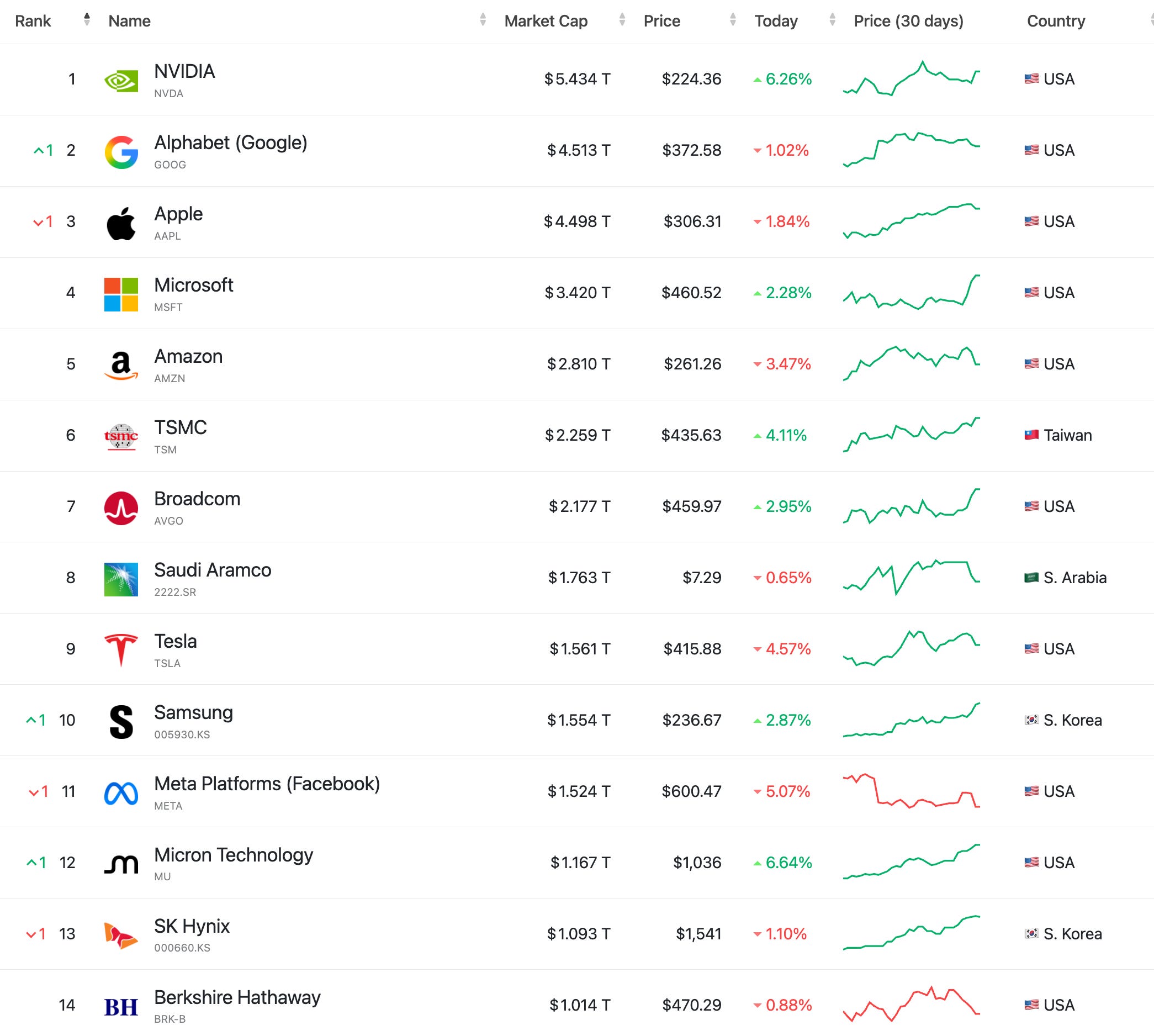

Instead, we have an elite group of mega-cap tech generals pulling up a heavily dragging baseline. A lot has been written about the historic levels of concentration we are witnessing in the S&P right now. The track record of the “top 10” club is generally rather poor. Massive concentration – I believe we’re close to the top ten names of the S&P representing 40% or more right now – will only magnify the impact of this base rate, I believe.

Back to my point: This is what market insiders call poor market breadth or high return dispersion. Poor market breadth occurs when a stock index (like the S&P 500) rises, but only a small handful of heavy-hitting stocks are driving the gains while the majority of the market is stagnant or declining.

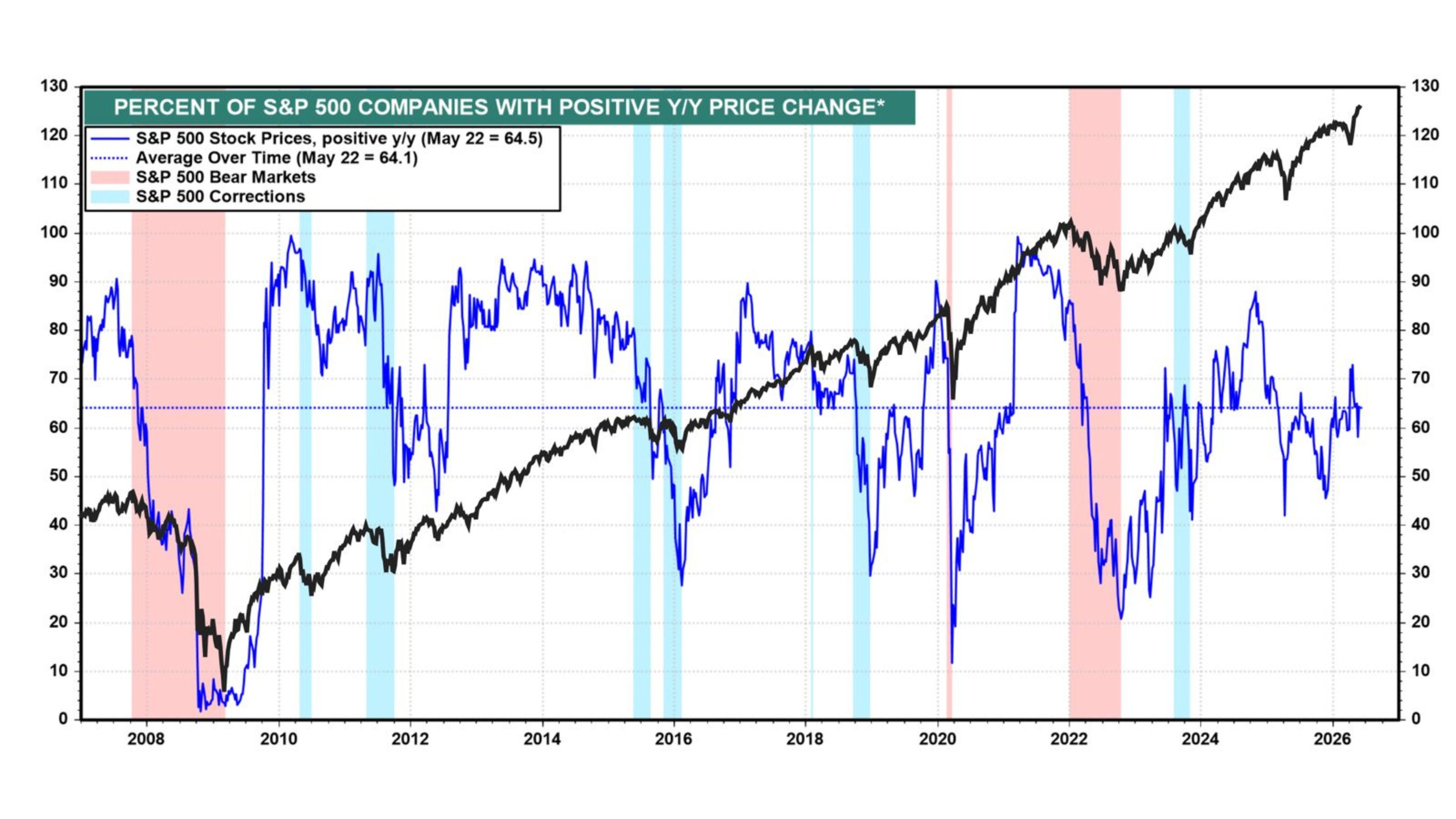

Let’s look at the exact breakdown from the S&P 500 data: As of May 64.5% of S&P constituents posted a positive return over the last year. Hovering right at the long-term historical average of 64.1%. Despite a massive rally, over a third of the index is flat or losing money.

The index itself is up 27.6% YoY.

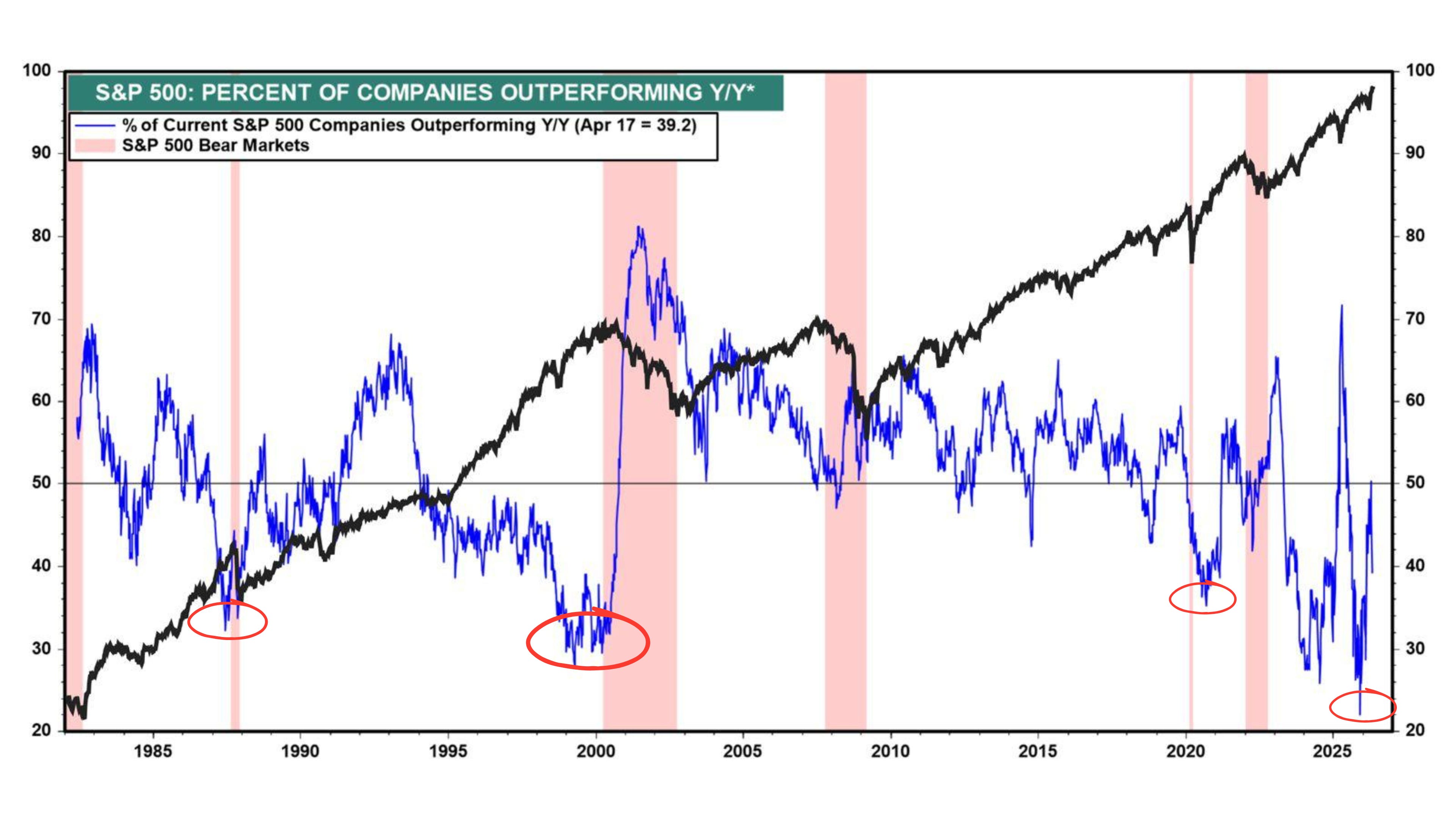

The more significant signal, however, can be found in the chart below (which is a bit dated to be fair!). As of last year, only 39% of S&P members outperformed the index in terms of YoY performance. Strikingly low. Only about 39% of companies were actually beating the index itself back then, meaning the index’s returns are heavily skewed by a few heavyweights.

Given the increasing concentration in the largest index constituents and the “AI winners,” I would not be surprised if the data today doesn’t look all too dissimilar! (feel free to share more up-to-date data in the comments below!)

This extreme lack of participation is a classic late-cycle indicator. Historically, often when the percentage of outperforming companies dropped into this sub-40% territory, a major market correction followed close behind – most notably ahead of the 1987 crash, the 2000 dot-com peak, the 2020 drop, and the 2025 tariff conundrum.

And if you think about it, this makes sense, right? When a tiny handful of stocks carry the weight of the entire financial system, the index becomes incredibly fragile. If these winners at some point stop “winning,” the index has a problem.

However, this environment completely changes the game for stock pickers. It becomes increasingly harder to outperform the market. As legendary Michael Mauboussin explains in one of his papers:

“Security selection skill is entirely dependent on market dispersion, which is the range of returns across a group of stocks. If all stocks in the S&P 500 return roughly the same amount in a given year, picking the ‘best’ stock yields very little excess return, blunting your skill. High dispersion is an absolute prerequisite for security selection skill to shine.”

3. Global AI Mania

This hyper-concentration isn’t just an American phenomenon. The AI infrastructure boom has officially gone global, turning major international indices into concentrated vehicles moving with the volatility of micro-cap assets.

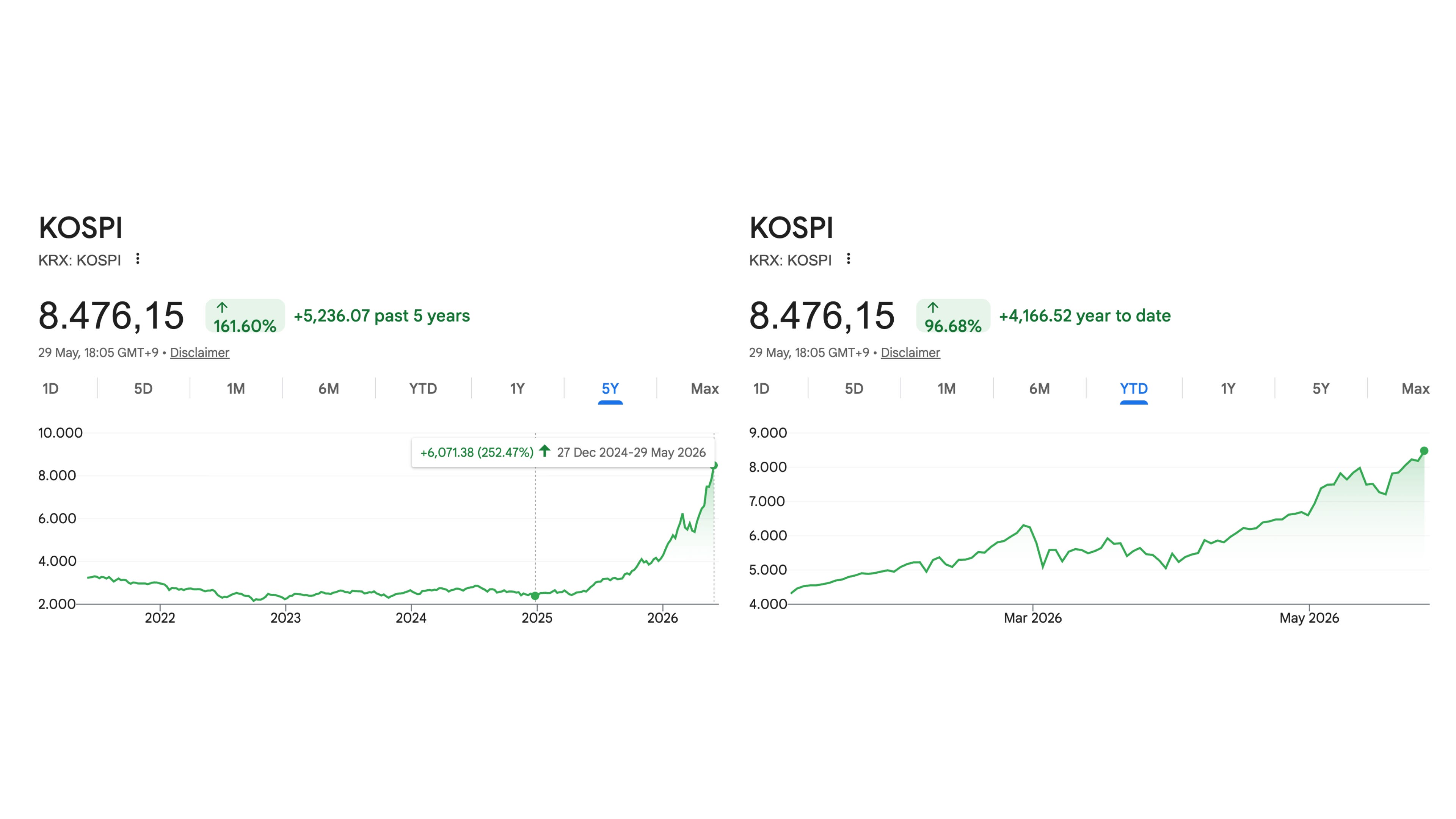

Look no further than South Korea’s KOSPI index. The index has staged a breathtaking rally, skyrocketing 96.7% year-to-date and climbing 252% from late 2024/early 2025.

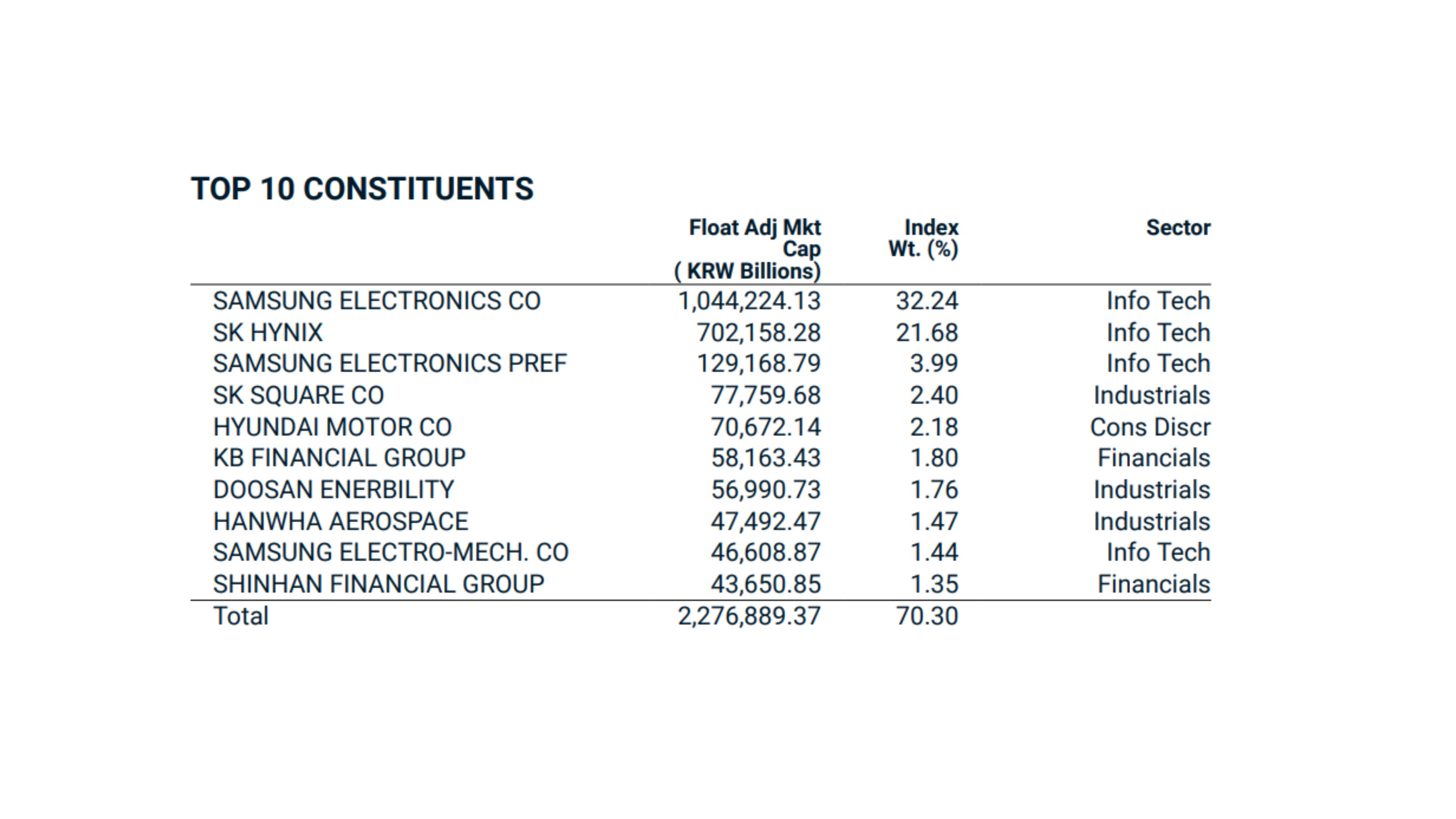

Why is an entire national index moving like an early-stage cryptocurrency? The answer lies in its extreme structural weightings. I couldn’t find the actual weight of the KOSPI index, but here are the weightings of the MSCI Korea index:

More than 57% of the entire index is tied up in the fortunes of just two top semiconductor players.

Are you looking for a passive investing vehicle? Look somewhere else!

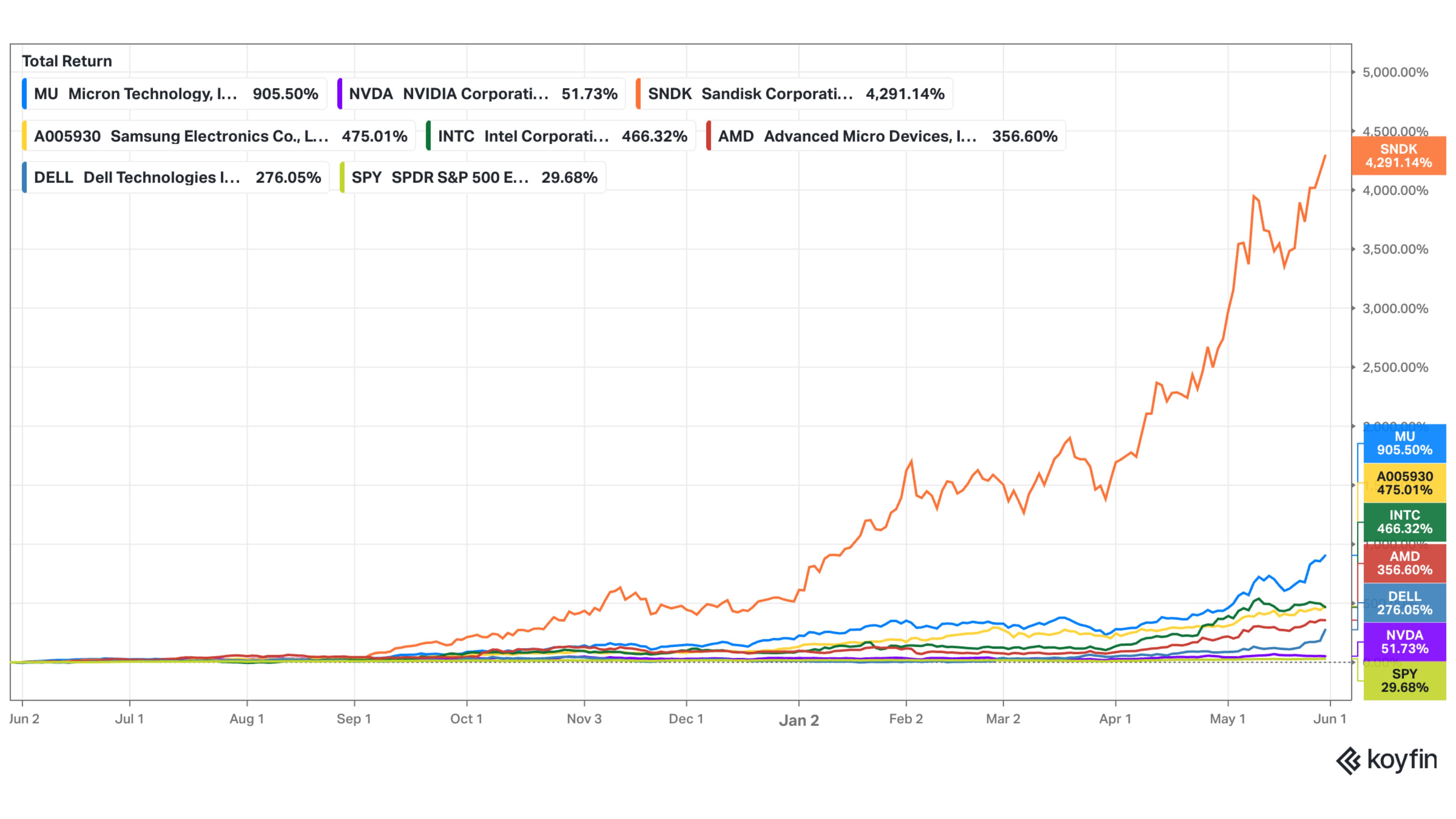

When you look at the underlying stock returns of some of the biggest and most popular “AI stocks” over the past year, the numbers appear anything by sustainable to me. While the SPY (S&P 500 ETF) put up a strong 29.68% return, look at what the AI hardware and memory supply chains did:

NVIDIA (NVDA): +51.73%

Dell Technologies (DELL): +276.05%

Advanced Micro Devices (AMD): +356.60%

Intel (INTC): +466.32%

Samsung Electronics (A005930): +475.01%

Micron Technology (MU): +905.50%

SanDisk (SNDK): A mind-numbing +4,291.14%!

These aren’t speculative penny stocks being pumped in internet forums; these are massive, multi-billion-dollar corporations experiencing vertical, parabolic price expansions.

When mega-cap hardware manufacturers trade like speculative lottery tickets, you are looking at classic, textbook market froth.

4. The Luxury Car Bonus Cycle

Speculative bubbles eventually leak out of brokerage accounts and manifest in the real world. When wealth is generated at a historic pace, consumer behavior shifts rapidly – and we are seeing exactly that happen right now.

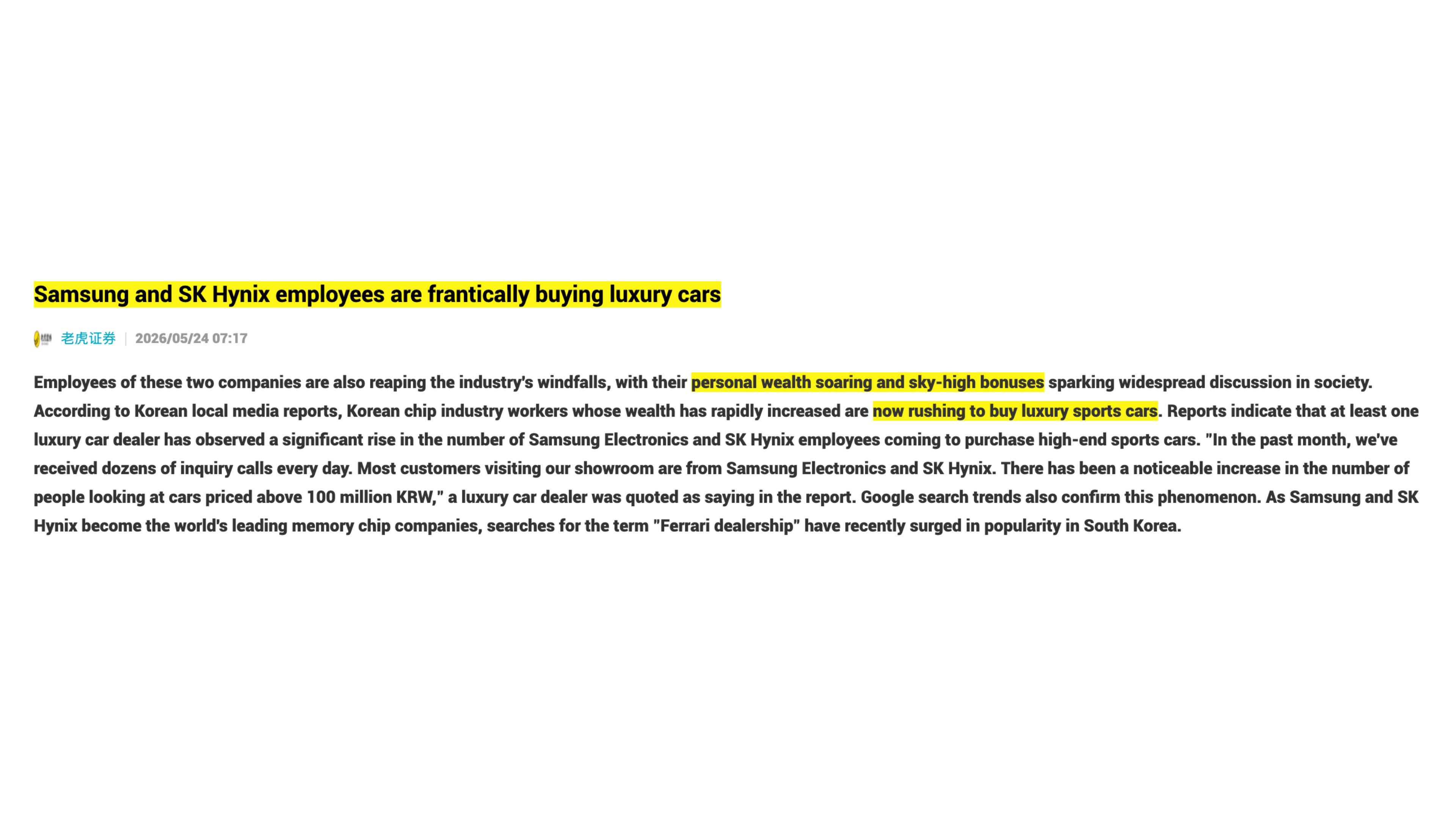

In late May 2026, financial media and local reports highlighted an unprecedented phenomenon in South Korea: luxury car dealerships are experiencing a frantic rush of buyers.

The individuals driving this demand aren’t traditional high-net-worth real estate tycoons or seasoned executives; they are rank-and-file chip industry workers from Samsung Electronics and SK Hynix.

Thanks to the global AI chip boom, these employees have been reaping massive industry windfalls, with sky-high corporate performance bonuses scaling into the hundreds of thousands of dollars. According to dealership showrooms, the wealth effect has been instantaneous:

Dealerships have reported receiving dozens of inquiry calls every single day.

The vast majority of showroom foot traffic looking at high-end sports cars priced well above 100 million KRW consists of Samsung and SK Hynix workers.

Google search trends confirm the retail mania, showing a massive regional popularity spike in South Korea for the phrase “Ferrari dealership”.

When middle-management tech employees turn into immediate luxury sports car buyers en masse, this strikes me as another soft sign that we’re in the middle of late-cycle euphoria.

5. CEOs as Cultural Pop Stars

Think about how corporate executives are treated near market bottoms versus market tops. At the depths of a bear market, CEOs are often vilified, hauled before regulatory committees, or blamed for economic downturns. But at the absolute peak of a bubble, some select executives transform into mainstream cultural icons.

NVIDIA’s Jensen Huang has officially achieved full-blown pop-star status. We see a similar phenomenon with Anthropic's Dario Amodei, whose profile has skyrocketed into billionaire, tech-titan status as his company's valuation pushes toward the twelve-figure mark. Even Alphabet’s Sundar Pichai has pulled off a stunning narrative reversal – evolving from an executive facing investor calls for his ouster just a year ago to a celebrated pioneer leading Google's triumphant, multi-billion-user 'agentic AI' era.

Don’t get me wrong: Jensen Huang strikes me as an exceptionally brilliant, humble, and likable leader. But the way the broader public and social media now obsess over his lifestyle (I’m not going to insert the image of him giving a fan a special signature here …) is highly unusual for the leader of a B2B hardware company.

Just take a look at what went viral on platforms like X in late May 2026:

Mainstream food bloggers tracking him down like a Hollywood celebrity as he casually grabbed pepper buns at a night market in Taipei with his wife.

Videos flooding financial timelines showing him dancing on stage during an all-employee celebration event in Taiwan.

When the general public begins tracking a semiconductor executive’s street-food choices and viral dance moves with the same intensity usually reserved for pop musicians, retail euphoria has peaked. It’s yet another psychological signal that a sector is running on pure, unadulterated adoration rather than sober fundamental analysis.

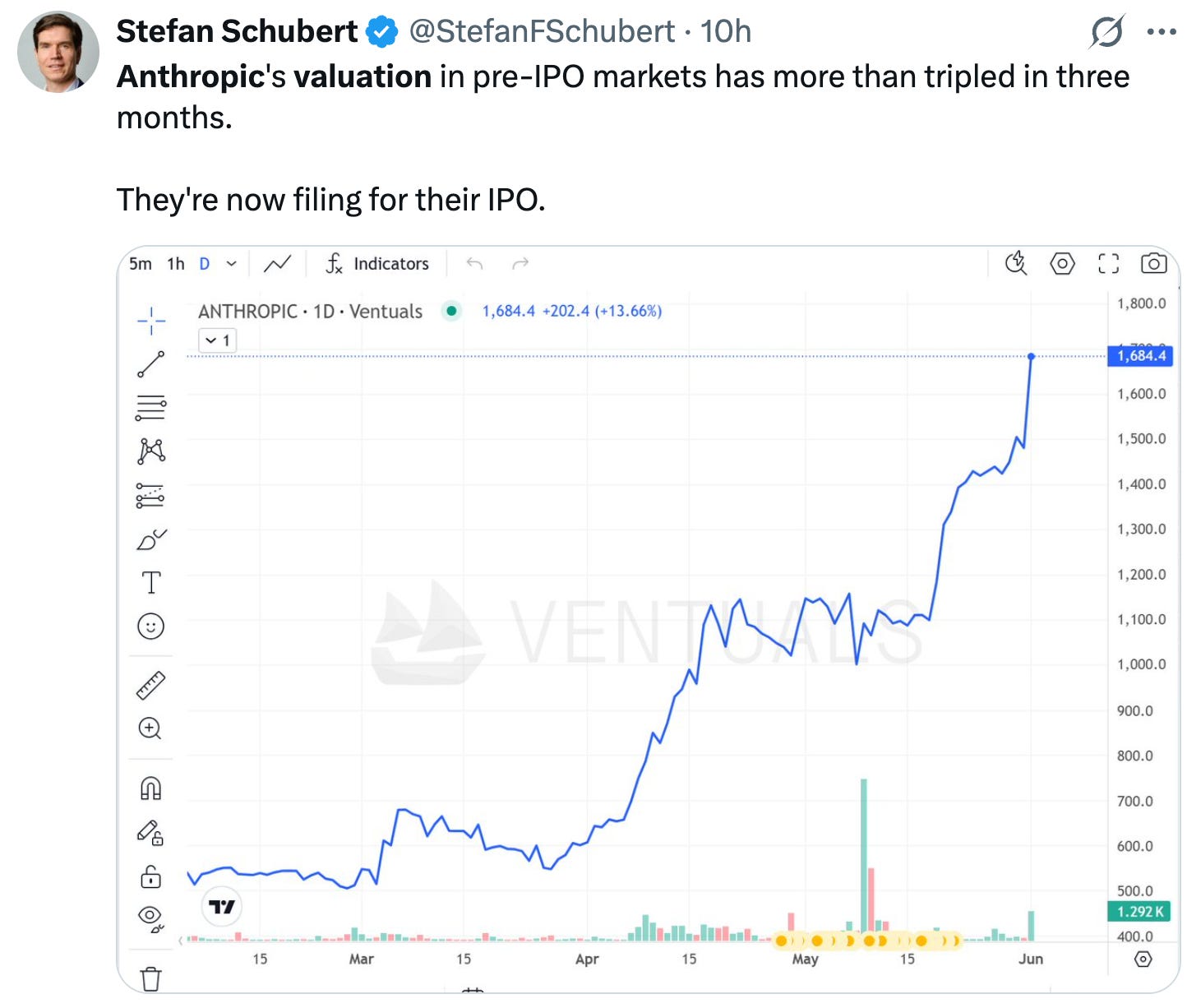

6. The Trillion-Dollar IPO Rush

The final structural signal of a market peak we will discuss in this piece is the sudden, aggressive rush toward the Initial Public Offering (IPO) market. When market conditions are average, companies list systematically. But when a bubble reaches its maximum thickness, late-stage private companies scramble to go public all at once.

Why? Because insiders, founders, and venture capitalists understand market cycles better than anyone else.

They see the massive premium the public market is currently paying for tech, and they want to capture that peak liquidity before the window slams shut.

Right now, we are witnessing what financial media is calling “The $3 Trillion Reckoning.”

Three of the most highly valued private giants in the world are simultaneously charging toward the public markets:

OpenAI

SpaceX

Anthropic

What makes this absolutely unprecedented is the scale: all three companies are aiming to go public at valuations hovering close to $1 trillion each.

For perspective, there are only a small handful of trillion-dollar public companies in existence today, and these three are aiming to join that elite club all at once. This is not something you are seeing in a normal market environment.

When you see high-profile founders rushing these massive capital raises to market as fast as humanly possible, it’s a major sign the party may come to and end soon.

It’s an implicit admission that they believe raising capital at a trillion-dollar valuation might be a flat impossibility two or three years from now if the macroeconomic environment shifts and the AI bubble deflates.

The Paradox & Avoiding the “Blast Zone”

All of these signs point to a highly counterintuitive conclusion. If you look at the S&P 500 as a whole, its valuation is stretched so thin that the statistical base rates for 10-year compounded annual returns from these price levels look deeply disappointing.

This macro anxiety was perfectly captured by value investor Matthew Fine on a May 2026 episode of the Value Investing with Legends podcast:

“I’m a simple creature and I’m worried about the elephant in the room. And US equities are such a dominant force in global capital markets today, and the statistical base rates of what somebody should expect from valuations like these are very, very poor. And I’m fearful that there will be a lot of disappointment.

And I personally grapple with how to create distance from the blast zone because [we are] largely a long-only fund, and there will be collateral damage and there are correlations across all equity markets. And I think about how to avoid the fallout from a significant decline in US equity markets.”

So, how exactly do you “create distance from the blast zone” if you aren’t managing a portfolio as massive as Berkshire Hathaway’s and don’t want to sit entirely on a mountain of cash?

You look at exactly where the institutional money isn’t flowing right now.

Because index funds, ETFs, and momentum-driven institutional capital are blindly forcing trillions of dollars into anything loosely associated with AI, they are actively starving the rest of the global market of liquidity.

Arguably, and it sounds almost insane to say this in the current environment, this structural shift has created a paradise – and I’m the first one to admit that “paradise” may be a slight exaggeration, but you get the point – for disciplined, active stock pickers.

While the S&P 500 mega-caps may be approaching a rigid valuation ceiling, beautiful, high-quality, free-cash-flow-generating businesses outside the US and across select emerging markets are trading at rather cheap and compressed valuations, often at record-low multiples.

Pockets of exceptional value are hiding in plain sight. Pockets like e-commerce powerhouse Coupang Holdings, or regional giants like Mercado Libre or Grab Holdings, both of which we recently covered in a deep dive on this blog (check out the Library), are, I believe, worth your attention.

Deep Dive: Mercado Libre ($MELI)

When I think about e-commerce and fintech in Latin America, one name keeps surfacing: Mercado Libre. Founded in 1999, it’s far more than just an online marketplace. Over the last two and a half decades, it has evolved into a fully integrated, infrastructure-heavy commerce ecosystem around logistics, fulfillment, payments, etc. – an indispensable hub where consumers and merchants converge.

Deep Dive: Grab Holdings Ltd ($GRAB) – Master Piece

Over the last few weeks, I released my Grab Holdings deep dive series. As always, to make this research as accessible as possible, I’ve woven all four parts of the series into this single, unified resource, making it easier for you to “ctrl + search” for specific elements of the research. I hope my paying subscribers will find it useful. Also, keep in mind that in the Substack App, you should be able to access an audio version of the analysis, so you can conveniently listen to it on the go.

In 2026, payment companies are as unloved as they have been in a decade.

To sum up, I don’t know whether this market cycle turns in two months or two years. But the playbook for intelligent investing remains completely unchanged. Standing aside – potentially raising cash – while the crowd frantically chases trillion-dollar IPOs and semiconductor hype requires serious emotional discipline, but it is exactly how you avoid the eventual fallout. Keep your eyes locked onto true business fundamentals, protect your downside, and remember that the absolute best time to accumulate world-class businesses may be when the rest of the market is too distracted by the retail euphoria to notice them.

What are your thoughts? Are you seeing other unorthodox signs that the market is topping out, or do you think this AI-driven momentum still has room to run? Drop your thoughts and data points in the comments below!

Join the Community & Cut Through the Noise

If you want to move past the retail euphoria and start uncovering high-conviction, fundamental investment ideas, don’t navigate this late-stage bull market alone.

When you join our blog community today, you’ll instantly unlock 3 FREE GIFTS to sharpen your strategy.

For those looking to take their strategy to the next level, our Annual Subscribers receive exclusive access to our private WhatsApp Community, direct networking with serious investors, and a ticket to our digital investing conference, “The Idea Factory” in July.

PS: You might enjoy Dirtcheapstocks’ recent piece on the same subject as well:

PSS: You may also enjoy this Barron’s piece (paywalled) —> “If It Walks Like a Bubble and Quacks Like a Bubble, Then It’s Probably a Bubble”

Disclaimer: The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

Great post, René! You make excellent points on market concentration, and the lagging nature of metrics like the Shiller P/E. It's hard to ignore the luxury car rush, the CEOs as pop stars and the sheer scale of the trillion-dollar IPOs looming on the horizon.

However, the critical counterweight here is that actual earnings growth and forward expectations entirely justify these valuations (in contrast to the dot.com bubble) .... provided, of course, that those expectations turn out to be correct.

Take Nvidia as the poster child for this rally. Based on current analyst consensus estimates, its forward P/E for 2030 sits at roughly 10. If those predictions materialize, that valuation isn't bubbly at all; it's actually cheap. The market is simply pricing in a massive, continued expansion of the denominator. As long as the companies actually deliver on the earnings, the math holds up.

Time will tell, if those predictions will hold. Fingers crossed.

My take on the valuation issue. Solving the Metzian Dilemma.

https://substack.com/home/post/p-198878429