When I think about e-commerce and fintech in Latin America, one name keeps surfacing: Mercado Libre. Founded in 1999, it’s far more than just an online marketplace. Over the last two and a half decades, it has evolved into a fully integrated, infrastructure-heavy commerce ecosystem around logistics, fulfillment, payments, etc. – an indispensable hub where consumers and merchants converge.

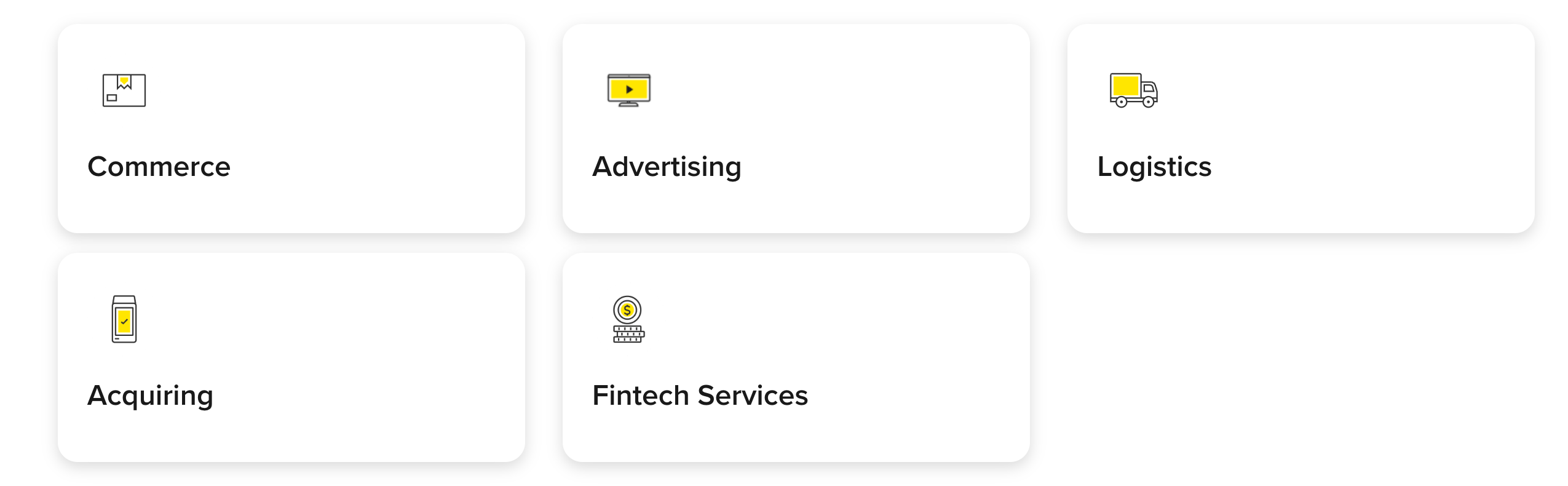

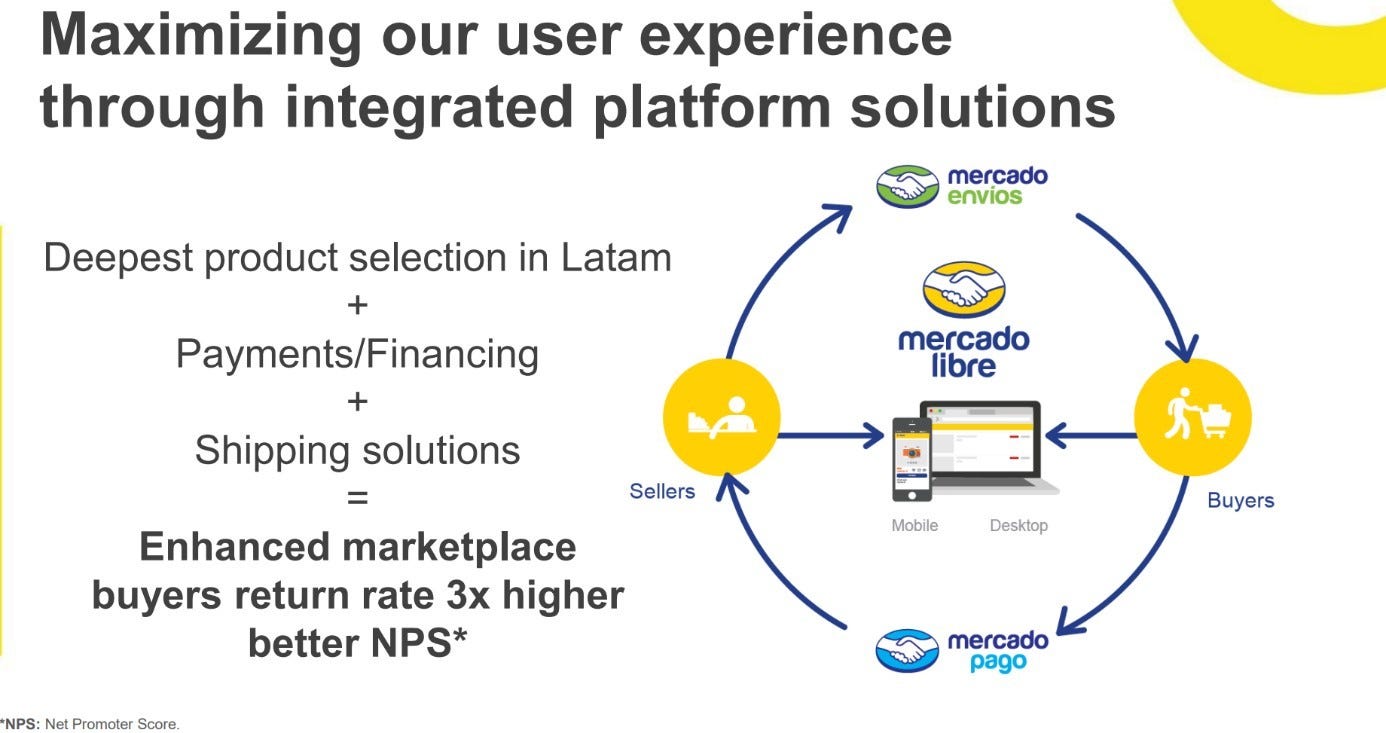

Sure, Mercado Libre is also facilitating transactions, but on top of this, it has built, and still is in the process of building, an entire digital economy through its synergistic pillars: the marketplace itself, the fintech platform Mercado Pago, the logistics network Mercado Envios, and the advertising arm Mercado Ads.

Together, these elements create a self-reinforcing flywheel that few companies in emerging markets can rival.

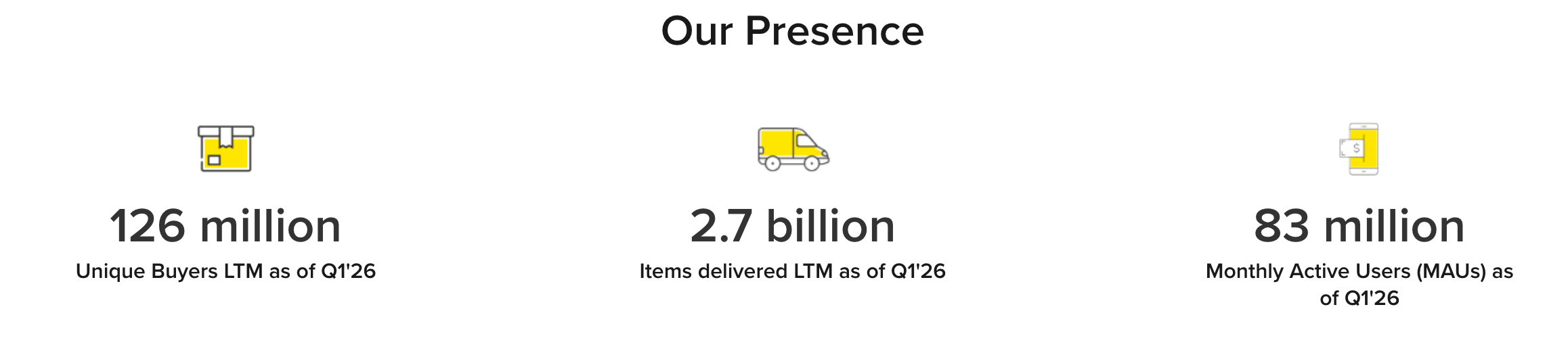

What fascinates me most is the sheer runway for growth. E-commerce penetration in Latin America still lags the US, UK, and China by roughly half, while a vast swath of the population remains underbanked or unbanked. Mercado Libre has positioned itself to capture both markets. Its fintech arm, Mercado Pago, leverages proprietary data and machine learning to extend credit to underserved populations – replacing the need for traditional collateral and turning users’ digital footprints into financial access. Meanwhile, the logistics network now reaches over 94% of the population in key markets, enabling deliveries that brick-and-mortar retailers struggle to match.

Moreover, Mercado Libre’s management doesn’t chase short-term profits. Their “time arbitrage” strategy is clear: invest boldly now to cement long-term dominance. The mantra “The best is yet to come” isn’t marketing fluff – it’s a strategic declaration.

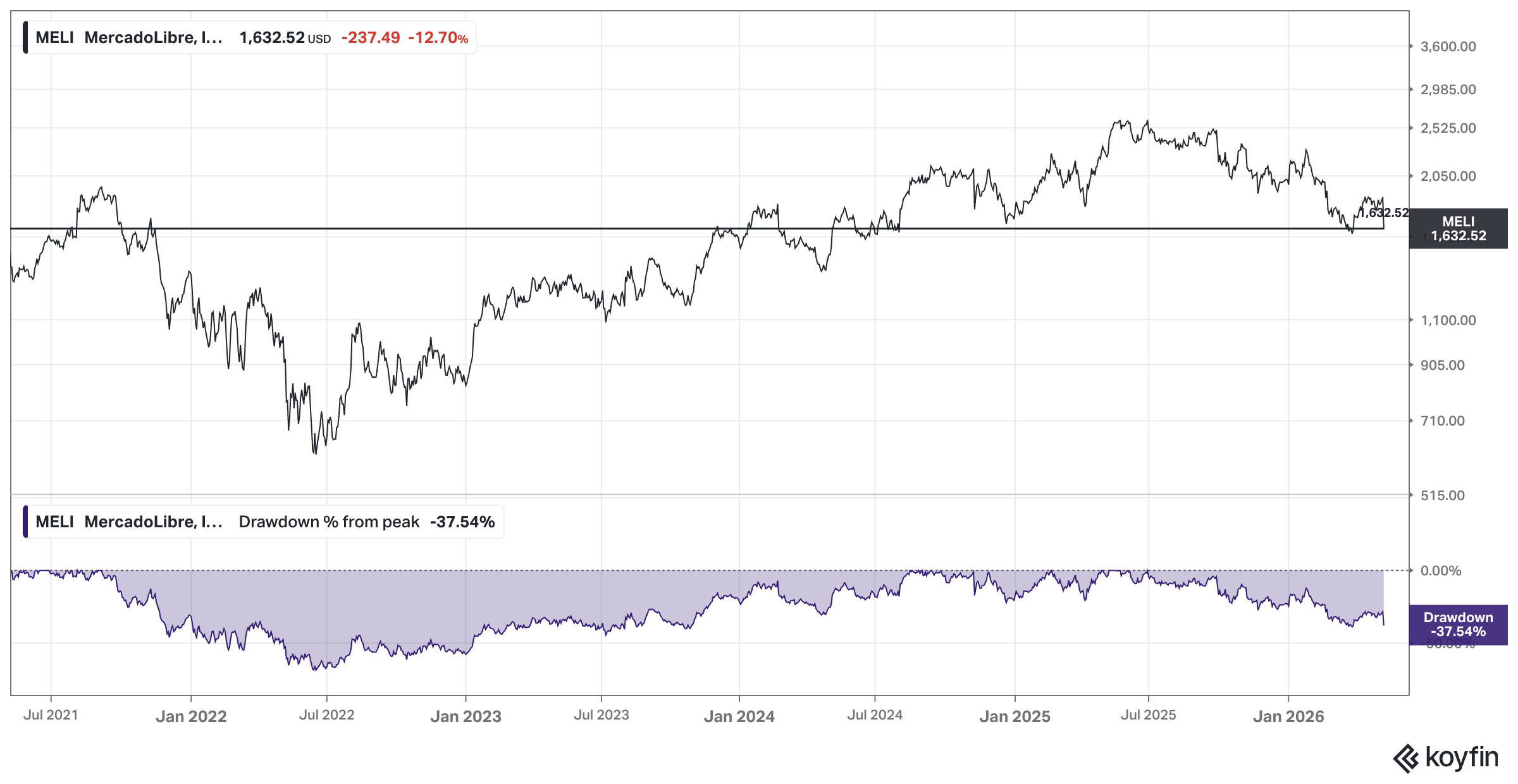

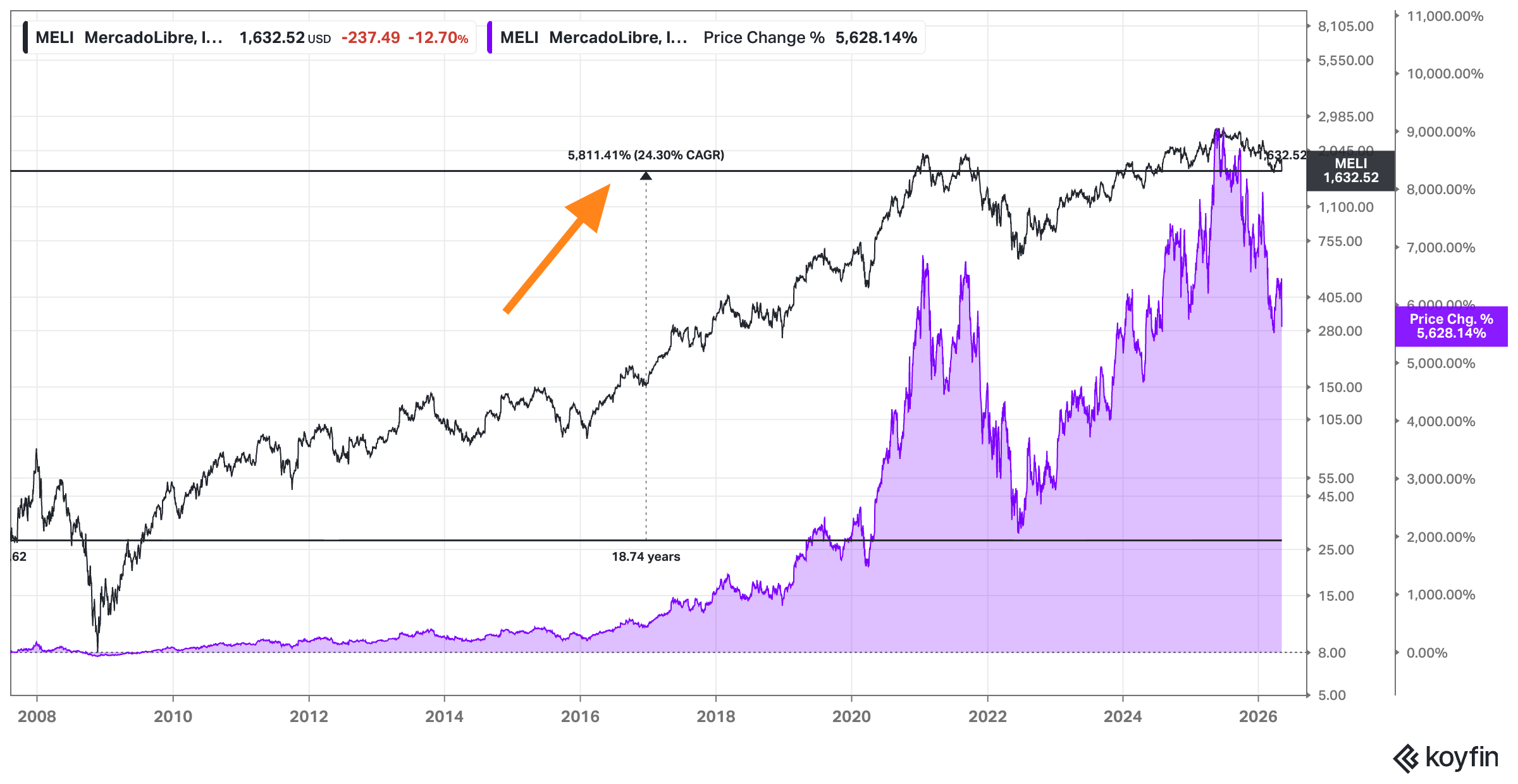

This approach has allowed MELI to compound value at an extraordinary pace. Even with the current 37% drawdown and a stock that has essentially gone sideways over the past five years, …

… it’s remarkable to remember that over nearly twenty years, Mercado Libre has delivered an average annual return north of 24%, far outpacing global indices.

Yet dominance has its challenges. Chinese entrants like Temu and Shein are pressing into Brazil and Mexico with aggressive pricing and logistics models. Singapore-based Sea Limited's Shopee is also actively competing with Mercado Libre in Brazil. Furthermore, regulatory scrutiny is intensifying in key markets, particularly around anti-competitive practices and data governance. The platform, too, faces reputational pressure from counterfeit products and disputes over seller accountability.

Still, Mercado Libre’s network effects, data-driven lending, and logistical moat give it a resiliency few competitors can match, even in the face of Latin America’s macroeconomic volatility.

Did I catch your interest yet? This was only the start, as this post is a deep dive into Mercado Libre – not just as a stock, but as a business, a strategy, and a regional powerhouse. I’ll explore how it built its moat, how management thinks about growth, the risks it faces, and ultimately, whether the stock still deserves a place in a long-term portfolio.

Disclaimer: I own Meli shares. The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

High-Level Thesis: “Bam Bam Bam Bam Bam”-90 Second-Hypothesis

As always, let’s return to Bill Miller, who has long emphasized that portfolio managers have ultra-short attention spans. He recalls how Peter Lynch would literally set an egg timer for 90 seconds during stock pitches – forcing the analyst to get to the point fast. As Miller put it: “The best thing to say is, ‘I want to talk to you about [stock]. It is at $X. Here are the five reasons why I think it is worth $Y.’”

Following that philosophy, I want to give you the quick Mercado Libre hypothesis. Admittedly, this one is longer, and I’m playing around with different formats here. I went with a similar format in my Nintendo write-up, where I try to condense down the core thesis to the most important pillars (I ended up putting together eight “BAMs” in this write-up; but one could certainly add more), and then couple this with a very thorough business model overview, thoughts valuation, plus other relevant findings.

Mercado Libre (Ticker: MELI) is trading around $1,556 as I type this, down another 4-5% after the 10% decline post Q1 results, as highlighted, even as net revenue growth reaccelerates to 49% (its fastest growth in four years). I believe it might be an interesting buy for the following five reasons:

Bam 1 – Ecosystem Control: It controls Latin America’s leading integrated commerce and fintech ecosystem, creating a self-reinforcing flywheel where marketplace traffic feeds payments, and payments feed deposits and proprietary credit data, and traffic feeds its advertising business, and the generated profits are reinvested into its infrastructure and logitiscs.

“Mercado Libre’s logistics network is one of our strongest competitive advantages. We deliver a world-class experience for buyers, driving greater traffic, conversion, and sales for sellers, along with higher NPS and improved cost efficiency. We continue to innovate and offer multiple delivery options, such as Next Day Delivery, Meli Delivery Day, and Meli Places“ - Company website

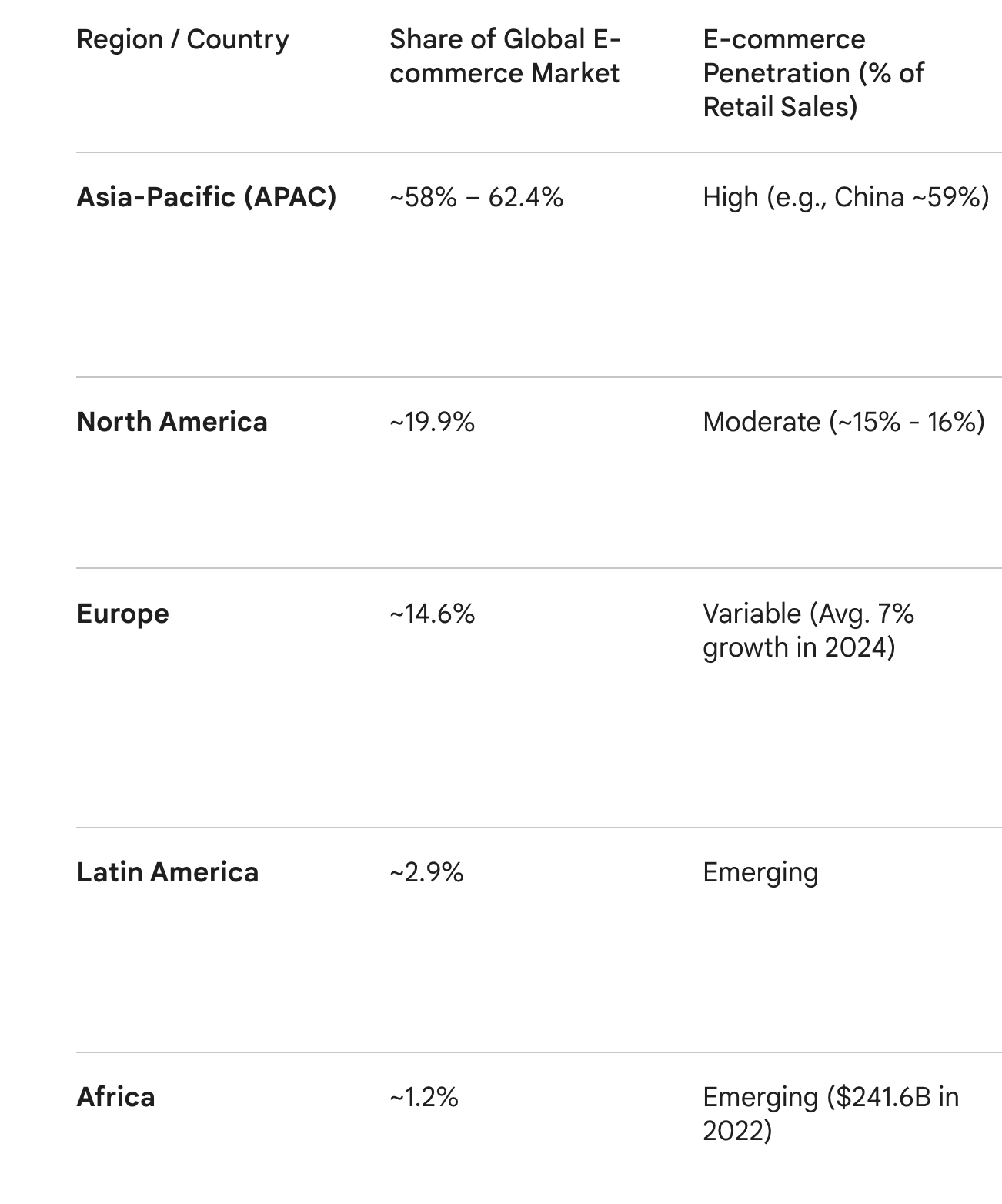

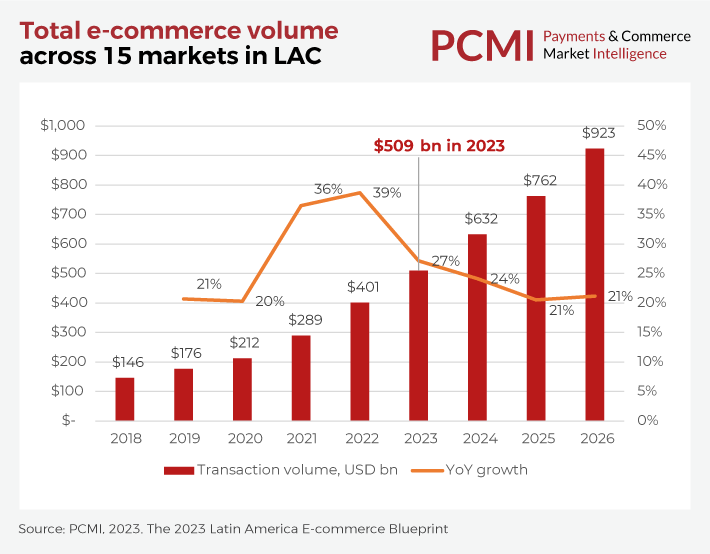

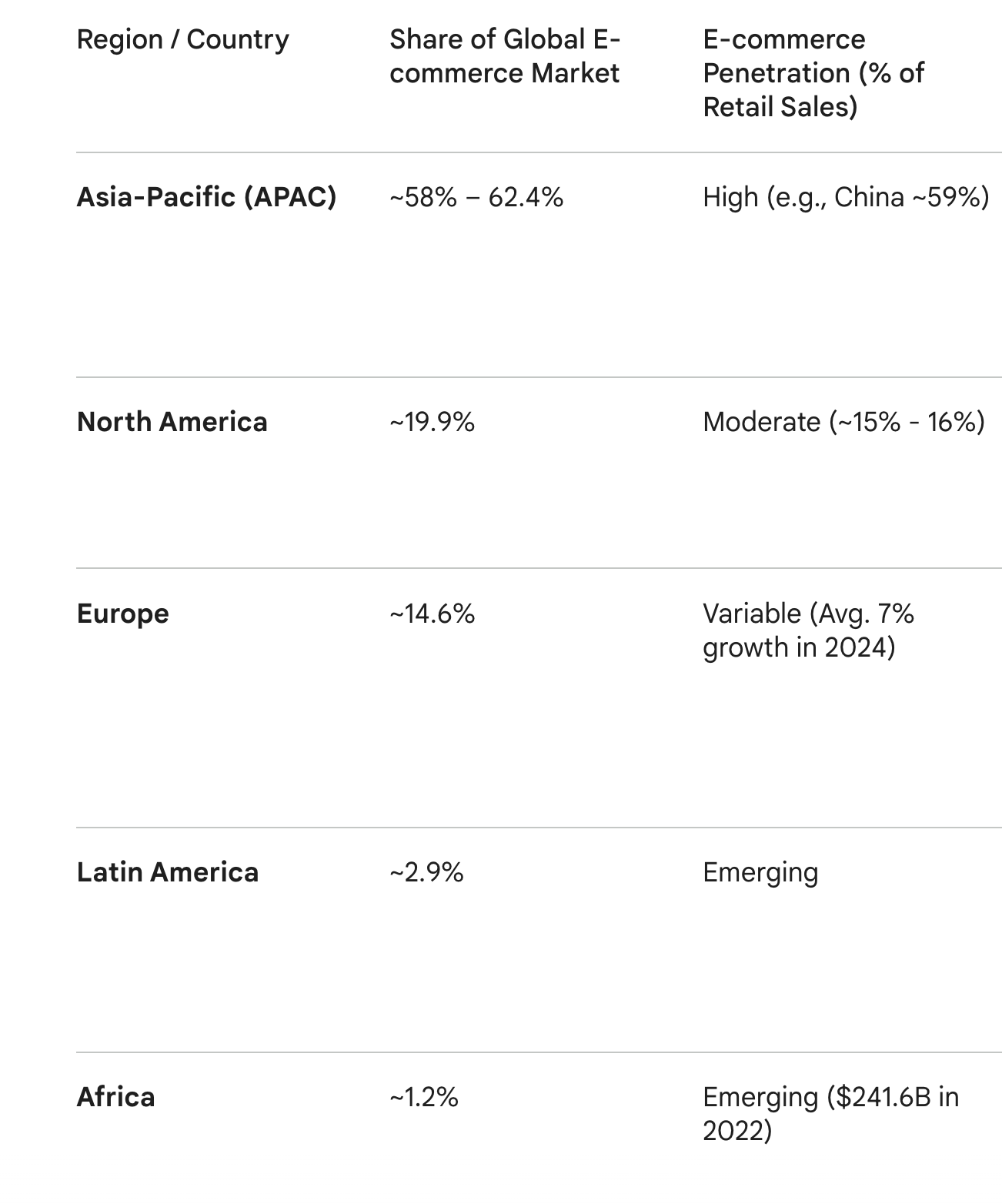

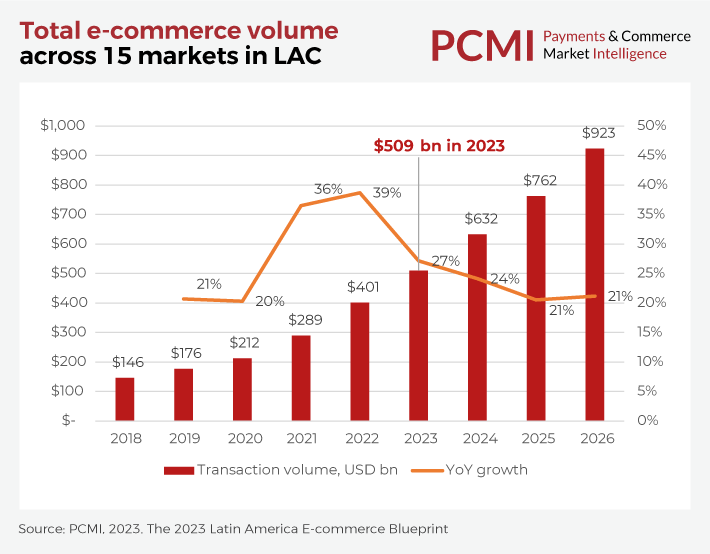

Bam 2 – Riding the Secular Growth Runway: One of the most compelling reasons to consider Mercado Libre is the sheer size of the opportunity in Latin America. While e-commerce is a global trend, the region remains roughly half as penetrated as more mature markets like the U.S., UK, or China.

Regional e-commerce penetration sits in the mid-teens as a share of total retail, compared with roughly 15-25% in the U.S. (depending on which analysis you look at) and over 35% in some Asian countries. Management believes the market could more than double – in fact, LatAm e-commerce has been the fastest growing market recently – as the region catches up, meaning the growth runway is enormous.

The habit of online shopping itself is still in its infancy. The average American makes 41 online purchases per year; in Latin America, that number is just seven.

“We have a once-in-a-generation opportunity to transform how hundreds of millions of Latin Americans shop, pay and access financial services. In commerce, the region is at an early stage of a shift that markets like the US are much further along. The average American makes 41 online purchases per year whereas the average Latin American makes just 7. Our own buyers average 11 – ahead of the region, but still a fraction of what we expect over time as online shopping becomes a habit for many more people.“ - Q1 Letter