Over the last few weeks, I released my Grab Holdings deep dive series. As always, to make this research as accessible as possible, I’ve woven all four parts of the series into this single, unified resource, making it easier for you to “ctrl + search” for specific elements of the research. I hope my paying subscribers will find it useful. Also, keep in mind that in the Substack App, you should be able to access an audio version of the analysis, so you can conveniently listen to it on the go.

Imagine two Harvard Business School students, sitting together, brainstorming ideas that would go on to reshape the landscape of Southeast Asia’s transportation, food delivery, and financial services.

In 2012, Grab was born from a simple, but ambitious business plan aimed at tackling one of the most unreliable and unsafe taxi systems in the world – Malaysia’s. Fast forward to today, and Grab has evolved from that small idea into effectively the “operating system” for daily life in (most of) Southeast Asia.

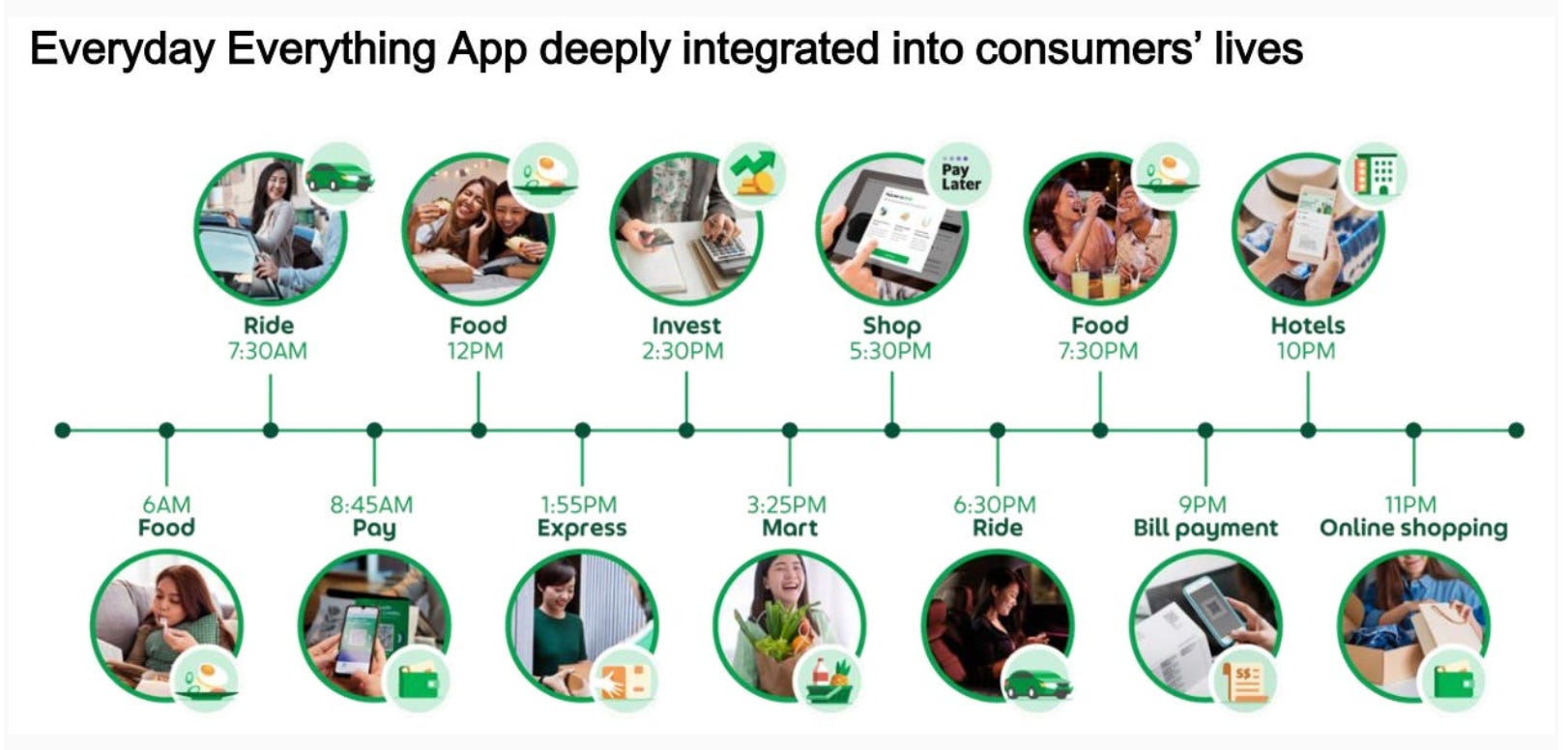

And Grab is not just another app. In Southeast Asia, Grab is more than a name – it’s become a verb for many. People say, “It’s raining; let’s just Grab to the mall instead of walking” or “I’m too tired to cook, should we Grab some Thai food?” without thinking twice. And it doesn’t stop there – Grab has mastered the art of creating habits, seamlessly integrating itself into the daily lives of millions of people who now rely on it for everything from getting from point A to point B to paying bills to online shopping.

Grab’s story is also a survival narrative that most tech companies would envy. In 2018, Grab managed to outmaneuver the global giant Uber in its home region and, eventually, when Uber basically gave up, acquired Uber’s Southeast Asian operations in a unique deal. That was a pivotal moment in Grab’s history, solidifying Grab’s dominance and ensuring that Uber’s exit from Southeast Asia would make Grab the undisputed leader in ride-hailing and delivery services.

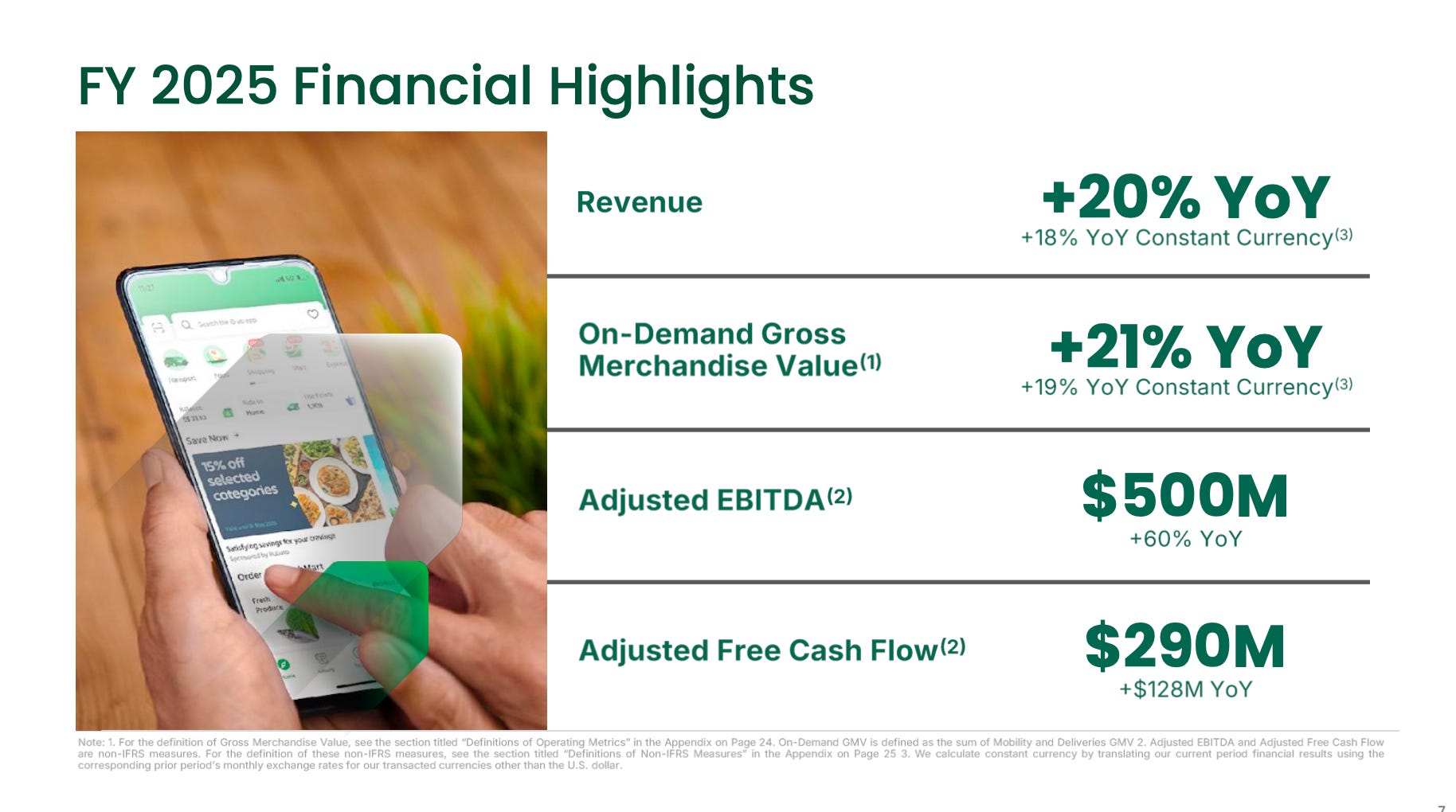

Fast forward to 2025, and Grab hit a major milestone: profitability. After years of burning through capital in pursuit of growth, Grab reached its first full year of net profit in 2025 – $200 million in the black. This marks a significant inflection point, where the company is transforming from a “growth-at-all-costs” startup-like-business into a more disciplined, profitable growth powerhouse with a clear path to long-term value creation.

But here’s the thing: Grab’s story is far from over. In fact, despite its massive scale already – Grab is a multi-billion-dollar company today –, the company is still just scratching the surface. Grab’s Monthly Transacting Users (MTUs) currently represent just 6% to 7% of the Southeast Asian population. That means there’s a huge growth runway ahead – roughly 94% of the market is still untapped.

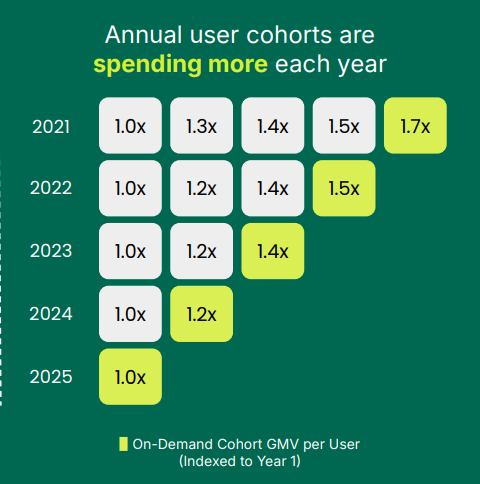

What’s even more exciting is Grab’s ecosystem flywheel. About two-thirds of Grab’s users engage with two or more services, and for those using three or more services, the one-year retention rate is an impressive 88%. When customers stay, they not only use more services, but they spend more, too. This is a growth driver that keeps feeding itself.

And then there’s Grab’s cutting-edge use of AI-driven efficiency. By utilizing proprietary AI models, Grab has been able to double its revenue from 2022 to 2024, all while keeping headcount flat. Over 90% of mobility rides are now dispatched using AI, showcasing just how much the company has automated its operations.

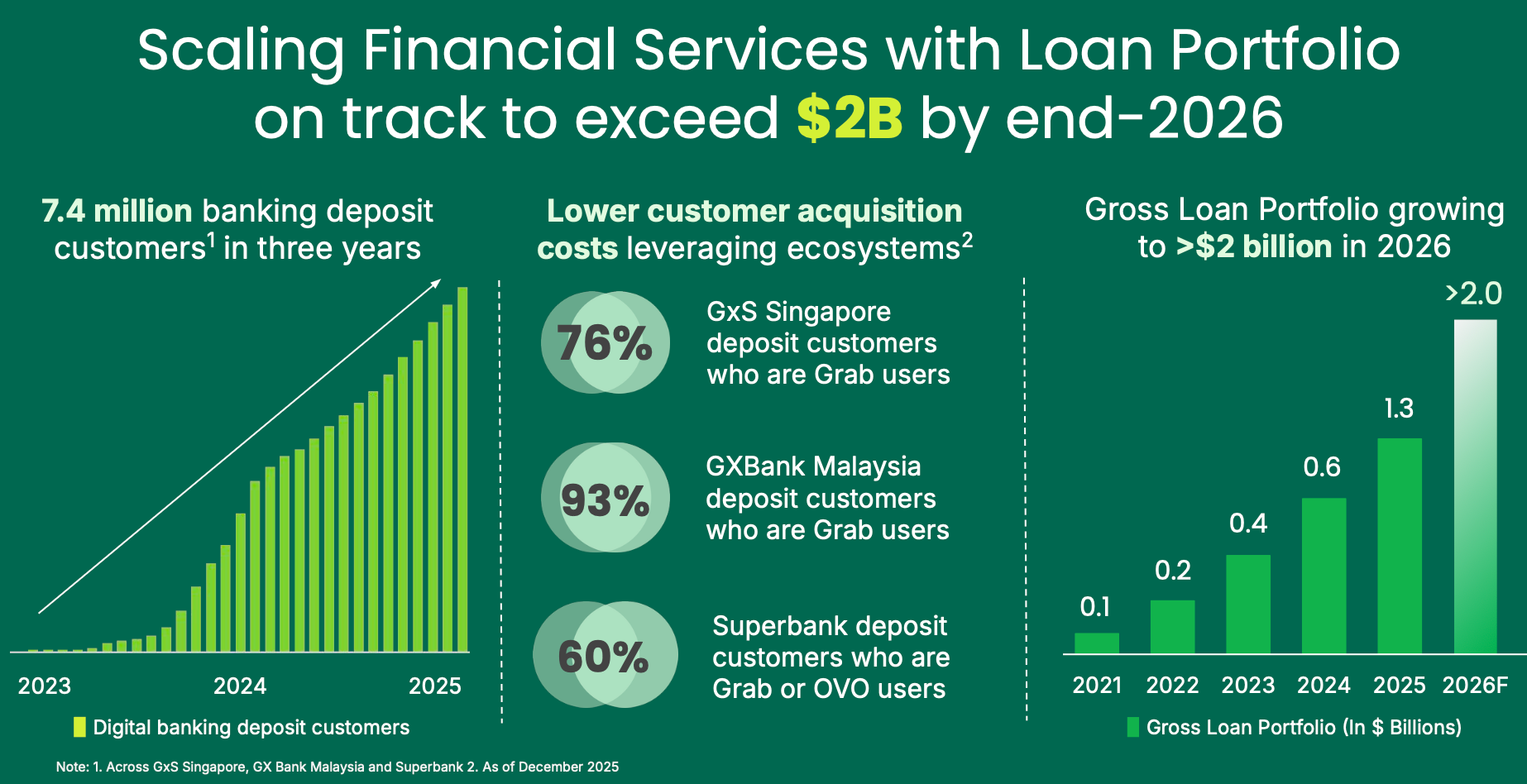

On the financial side, Grab has successfully expanded into digital banking. In just three years, Grab amassed 7.4 million deposit customers across its three digital banks, and its loan portfolio crossed the $1 billion mark in 2025 and is expected to exceed $2 billion by 2026 year-end.

And as if all of this wasn’t enough, Grab is setting its sights on global expansion. In early 2026, it completed the $600 million acquisition of foodpanda Taiwan, signaling the company’s intention to push beyond Southeast Asia and tap into new, high-value markets. This marks the first major step in Grab’s journey toward becoming a truly global player.

Of course, this is just the tip of the iceberg. Grab is positioning itself for the future with ambitious plans around autonomous vehicles (AVs) and scaling its financial services. The company is constantly innovating, finding new ways to integrate its services and make the lives of its users easier and more connected.

But what does this mean for investors? Can Grab sustain its growth? What challenges lie ahead? And most importantly, what kind of valuation can you expect as this story unfolds?

As you can tell, Grab is a fascinating business to dive into. So let’s do exactly that and dive deeper into Grab’s history, business model, management team, moat stack, its future, and the growth drivers that will continue to propel this Southeast Asian juggernaut forward.

Are you excited yet? Let’s dive into the first part (11,500 words) of this deep dive.

Disclaimer: I own Grab shares. The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

High-Level Thesis: “Bam Bam Bam Bam Bam”-90 Second-Hypothesis

As always, in the style of legendary investors like Bill Miller and Peter Lynch, I’m attempting to give you the quick 90-second rundown on Grab Holdings (GRAB) – what’s the investment hypothesis (which we are then going to test throughout this deep dive?

Right now, the stock trades around $3.6, a significant pullback from its 2021 debut. While that might sound concerning, the real story lies in the business transformation that’s been happening under the hood (i.e. not reflected in the share price).

Here are the five reasons why I think Grab is an interesting opportunity:

Via the link below, you get access to a rare 20% discount on the annual plan (limited to the first 5 who take it). The 20% discount is then locked in forever, meaning it applies to all future payments as well.

This is where it gets interesting.

Become a paying subscriber to read the rest of this post and get access to all of my other research, including valuation spreadsheets, deep dives (e.g. well-known mid- and large caps such as LVMH, Duolingo, Meta, Edenred as well as more hidden gems such as Tiger Brokers, Digital Ocean, Ashtead Technologies, InPost, Timee, and MANY more), and powerful investing frameworks.

As a member, you get:

Complete Access: Every deep dive in our library (65+ and counting).

The WhatsApp Community: Real-time discussion and networking with like-minded investors.

Digital Investing Conferences: 3-4 times a year, we also hold digital conferences where members present and share stock ideas, and discuss broader themes, and we’d love for you to join in!

Incredible Value: Full access to all of this for less than $1/day.

PS: Using the app on iOS? Apple doesn’t allow in-app subscriptions without a big fee. To keep things fair and pay a lower subscription price, I recommend just heading to the site in your browser (desktop or mobile) to subscribe.