You can read a good chunk of this article entirely for free. If you find value in this research, consider becoming a Premium Member for less than $1/day to unlock our full archive and join our growing circle of investors (I highly recommend checking out “The Library” to see what’s inside; you can find it right on the homepage).

Why join the community, you may ask? Our library is fast approaching 70 comprehensive deep dives, providing institutional-level research on some of the world’s most fascinating businesses. Most recently, we’ve dissected companies like Grab Holdings ($GRAB), Fair Isaac ($FICO), and Topicus.com ($TOI).

As a member, you get:

Complete Access: Every deep dive in our library (65+ and counting).

More Content: Company updates; powerful valuation spreadsheets, frameworks, and processes; regular portfolio updates (insights into my investing decisions); market commentary: etc.

The WhatsApp Community: Real-time discussion and networking with like-minded investors.

Digital Investing Conferences: 3-4 times a year, we also hold digital conferences where members present and share stock ideas, and discuss broader themes, and we’d love for you to join in!

Incredible Value: Full access to all of this for less than $1/day.

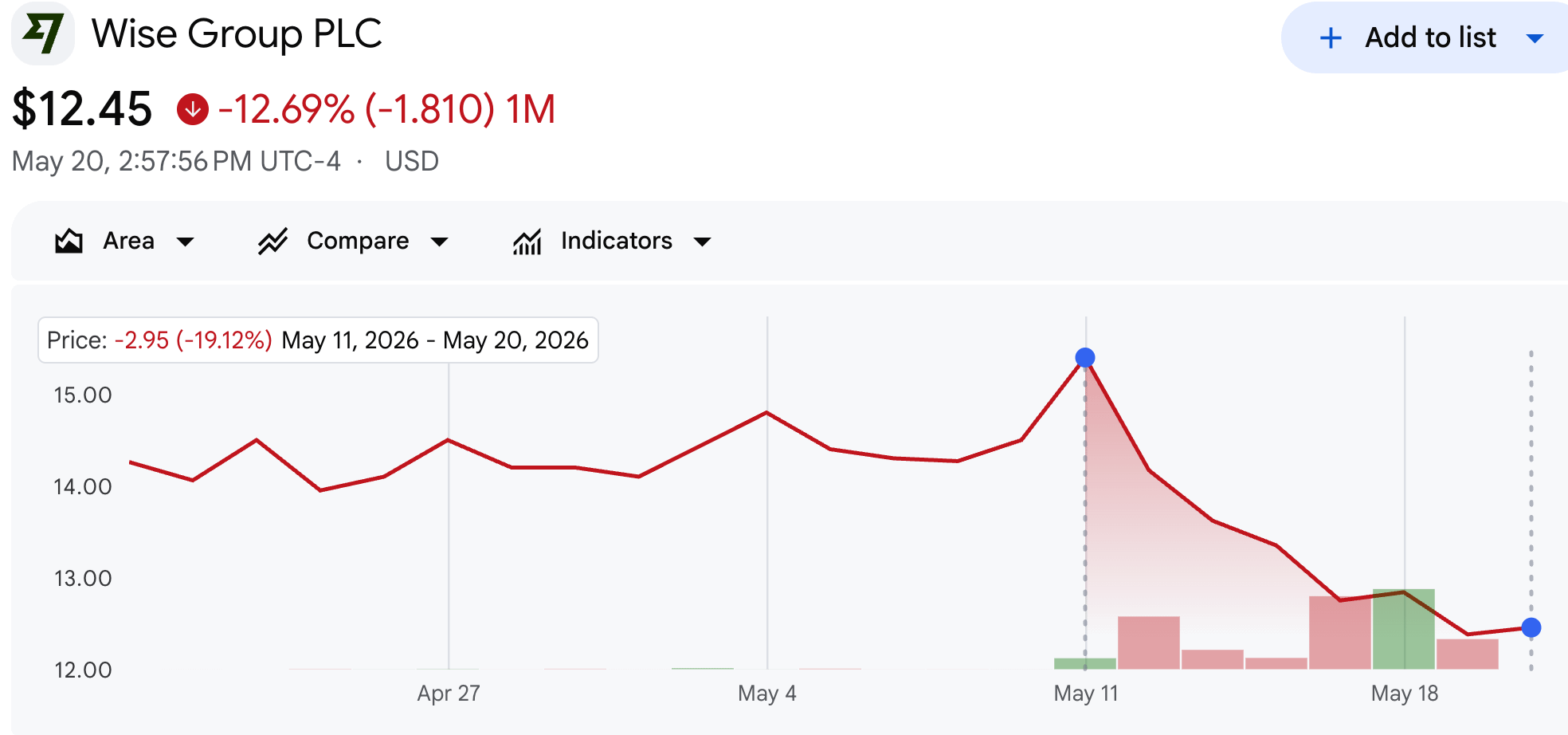

When Wise executed its highly anticipated dual listing on the Nasdaq, the financial media focused almost entirely on the superficial mechanics of the ticker tape. The opening price hit the screens, algorithmic trading systems adjusted to the new liquidity pools, and during the first few trading days, the share price immediately came under some structural selling pressure.

Short-term traders quickly pointed to the downward price action as proof that the payment sector is doomed and that Wise won’t be the exception spared by the market’s forces, but for those investors who ignore day-to-day market noise, the more insightful story was unfolding elsewhere. While the tape was flashing green (at first Wise’s stock shot up 7%) and red (before later declining for a couple of consecutive days), management was hosting a special call for analysts and owners.

It turned out to be the single most illuminating corporate presentation Wise has delivered, maybe in second place behind the landmark 2025 Owners Day – a high-substance, 120-minute masterclass packed with raw operational data and profound strategic disclosures.

Listening to a call like that requires a completely different analytical filter. If you only look at headline narratives or commentary driven by share price developments, it is easy to move right past the immense fundamental transformations occurring inside this business and the massive opportunity ahead.

“We believe our US listing will help us accelerate our mission, helping to bring more of Wise to everyone in the US, as customers and as owners.” - Company press release

“But in the context of the enormous size of this market, we’re really only starting to scratch the surface. We moved less than 5% of the money moved by people and less than 1% moved in the small business market. So this means that overall, we’re less than 1% of this enormous $43 trillion market of cross-currency transactions. And it also means that there’s a huge opportunity ahead of us. We’ve gone from 0, 15 years ago to now moving $0.25 trillion, but we are building this network and the apps to move trillions.“ - Special call transcript

The presentation was dense with subtle nuances, regulatory engineering details, and competitive dynamics that you can only truly appreciate if you have been tracking Wise’s global infrastructure build for years. And that’s what I’ve been doing ever since the company went public on the LSE in 2021. And the stock hasn’t moved anywhere since fwiw:

It is precisely this gap between superficial commentary and deep, operational reality that makes Wise arguably one of the most misunderstood, high-quality future compounder stocks in the entire global market right now.

To cut through the market skepticism and map out exactly where this business is heading over the next decade, I have broken down the 10 most critical insights from that special call that every long-term investor needs to internalize.

So let’s get right to it!

Disclaimer: I own Wise shares. The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

Insight #1 - More on the Stablecoin Disruption Risk

As described above, in my view, Wise remains one of the most deeply misunderstood high-quality companies in the global market today. Observers frequently look at the superficial layers of the business – treating it as just another sleek consumer remittance application that will bring take rates to levels where Wise will disrupt its own profit generation capabilities – while completely overlooking the monolithic, proprietary infrastructure humming beneath the surface.

"But if Wise keeps lowering prices, won't they run out of profit?"

Lately, especially in 2025, a new narrative has taken hold among skeptics looking to derail the investment thesis, and that is the supposed disruption risk posed by stablecoins. We have dissected this specific threat on the blog before, and I previously sat down to map out the mechanics of global liquidity in a comprehensive podcast episode with Mike from Money Flow Research. I’ll link all these pieces below:

The core argument from the bear camp is that blockchain architecture will render intermediaries obsolete by allowing value to transfer instantly across borders for fractions of a cent.

This narrative sounds convincing on paper, but it fundamentally misunderstands how global money movement actually functions. During Wise’s Nasdaq listing presentation, CTO Harsh Sinha directly confronted this crypto-native thesis, offering an analytical reality check that every serious investor needs to internalize.

Moving digital tokens between two crypto wallets is incredibly simple, yes, but the actual bottleneck of global commerce is not the token transfer itself. It is the friction of the real-world perimeter.

The true complexity of an international transaction is concentrated entirely in the on-ramp and off-ramp mechanics. People and businesses do not live, trade, or pay taxes in dollar-pegged digital tokens unless they happen to operate in a tiny, insular web3 sandbox.

As Harsh pointed out during the special call, “people and businesses want to use money in their local form.” They need to pay their local taxes in the United Kingdom or Brazil, settle domestic property transactions, and pay for university tuition.

“The real complexity arises when you actually have to on-ramp off-ramp these table cards to different currencies.”

This means that a stablecoin-based cross-border transaction is rarely a straight line. Instead, it typically requires a complex multi-leg execution sequence, often called a stablecoin sandwich. A user must convert their local fiat currency into a stablecoin, move the stablecoin across a blockchain network, and then convert that stablecoin back into the destination fiat currency via a local exchange or liquidity provider. Each leg of that sequence triggers financial crime screening protocols, compliance tracking, and foreign exchange conversion spreads. When you tally up the total structural friction, the economic argument for crypto rails completely falls apart. Harsh quantified this disparity clearly, noting that “most players in this space using the stablecoin route or stablecoin sandwich would charge anywhere between 100 to 200 basis points or more.”

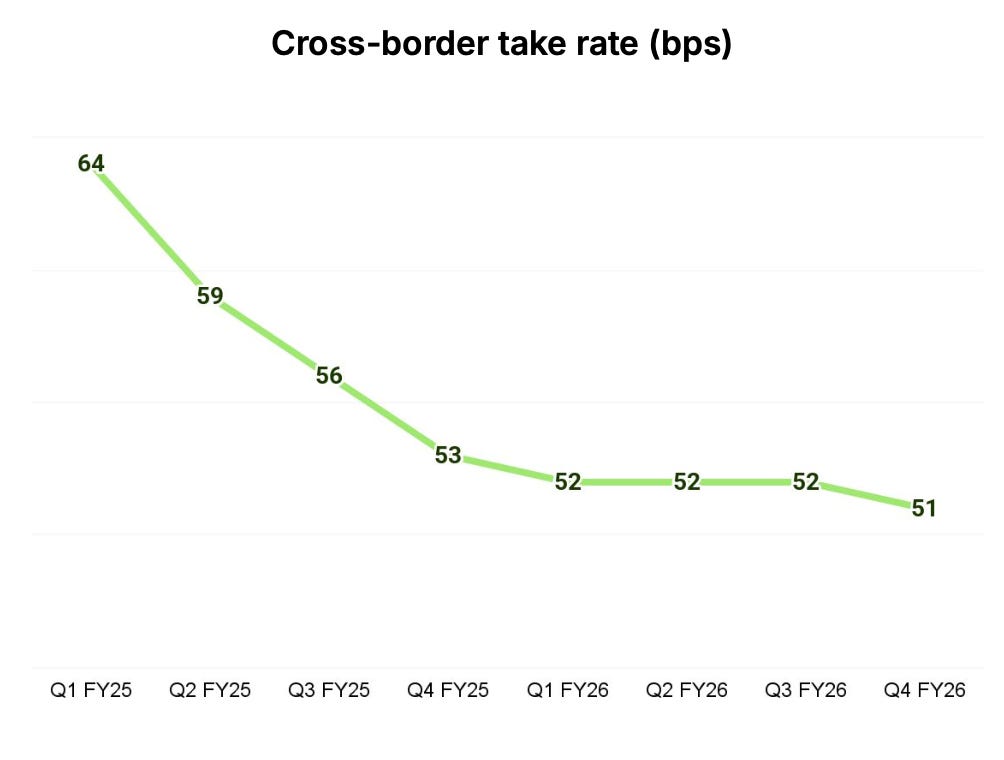

Compare that to Wise’s infrastructure, which charges a global average of just 52 basis points, and can drop below 20 basis points for large-volume corridors like Swiss Franc to British Pound transfers.

“… if you were to use stablecoins for doing cross-border payments, we’ve learned that the infrastructure we’ve built is by connecting local payment systems and direct connections that we’ve built, is is delivering a better price and speed than current stablecoin solutions can provide in this space. As we covered before, we charge 52 basis points on average.

And this is actually the global average. In some jurisdictions, if you were to move Swiss francs like CHF 1 million to GBP, we could get it as low as 20 basis points or even lower.”

The reason Wise can routinely outperform blockchain liquidity models is that it connects directly into domestic clearing systems. These massive local payment rails already process trillions of dollars in daily domestic volume, making them highly optimized and remarkably cheap.

Wise simply rides these massive local engines directly, bypassing the expensive intermediary spreads that plague crypto on-ramps.

The secondary argument for stablecoins is their utility as a capital flight hedge in inflationary environments. If you live in an economy where the local currency is rapidly losing purchasing power, holding a dollar-pegged digital asset is a rational defensive maneuver. Harsh acknowledged this macroeconomic reality, highlighting that “the Brazilian real has lost 15% against the USD in the last year,” which naturally drives local demand for foreign-denominated hedges.

Yet, the assumption that stablecoins are the only or best tool for this job is incorrect.

For the vast majority of non-crypto native users, a regulated multi-currency account is a vastly superior proposition. The Wise Account allows users to instantly hold 40 different fiat currencies at the click of a button, swap between them at the real mid-market exchange rate, and actively yield interest on those stable fiat balances without navigating the custody risks, smart contract vulnerabilities, or regulatory gray areas of decentralized finance. The company has already proven its ability to expand this framework into adjacent asset classes, having seamlessly integrated equities and money market funds into the core user interface over the past few years.

If stablecoins eventually achieve regulatory clarity and emerge as an efficient, compliant medium of exchange that users actively demand, Wise will simply add them to the platform as another standard asset class.

“But that said, that is the story today. We will continue to invest and see how this space evolves and as it evolves and if it does solve the problems for cross-commodity was for our customers in some regions, so maybe globally to make it cheaper and faster, we would, of course, use this technology. And the key thing here I want you to take away as the infrastructure we've built is extendable so that it'd be easy to add this.”

The primary takeaway for long-term owners is that Wise is completely agnostic to the underlying technology rail. Their proprietary software layer is entirely extendable. If public blockchain ledgers ever manage to outcompete domestic central bank rails on cost, compliance engineering, and raw speed, Wise will simply plug its global treasury engine directly into those networks.

Until then, their fifteen-year lead in regulatory licensing, domestic payment system access, and global compliance architecture remains an unmatched competitive moat. I am left with the exact same conviction that Harsh shared at the close of his presentation: “looking forward 10 years from now... I see most roads in cross-border payments leading to the Wise Infrastructure.”

Insight #2 - Wise’s 15-Year Headstart?

When evaluating the global payments landscape, investors routinely crown Visa and Mastercard as the ultimate, untouchable monopolies.

It is an accurate assessment, of course. Two fantastic and incredibly “moaty” businesses. Their entrenched network effects are virtually impossible to dislodge.

Yet, I believe Wise is quietly emerging as another incredibly structurally advantaged, unassailable business in the payments sector – a sector not necessarily known for deep, impenetrable moats (with a few exceptions) – outside of those two card giants.

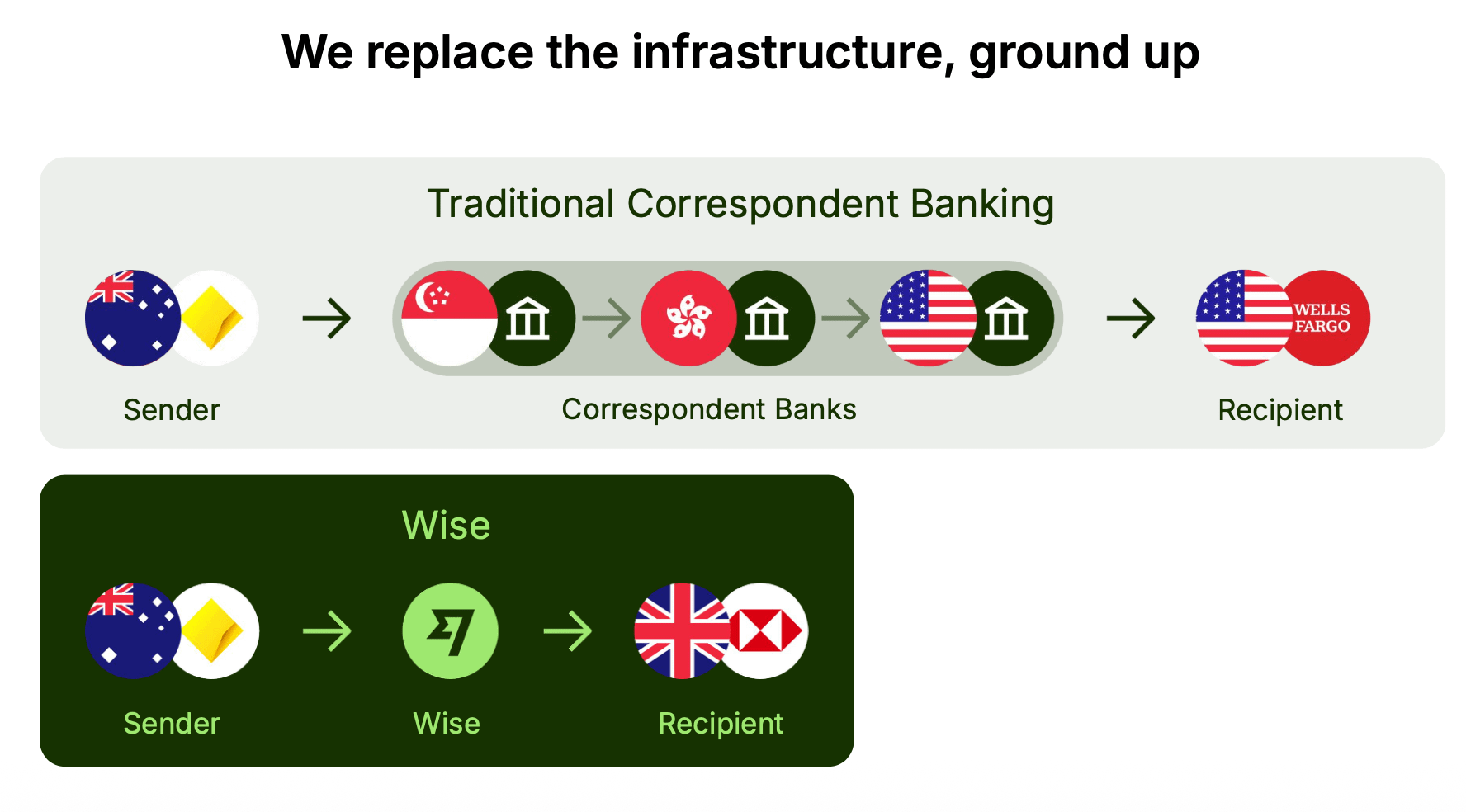

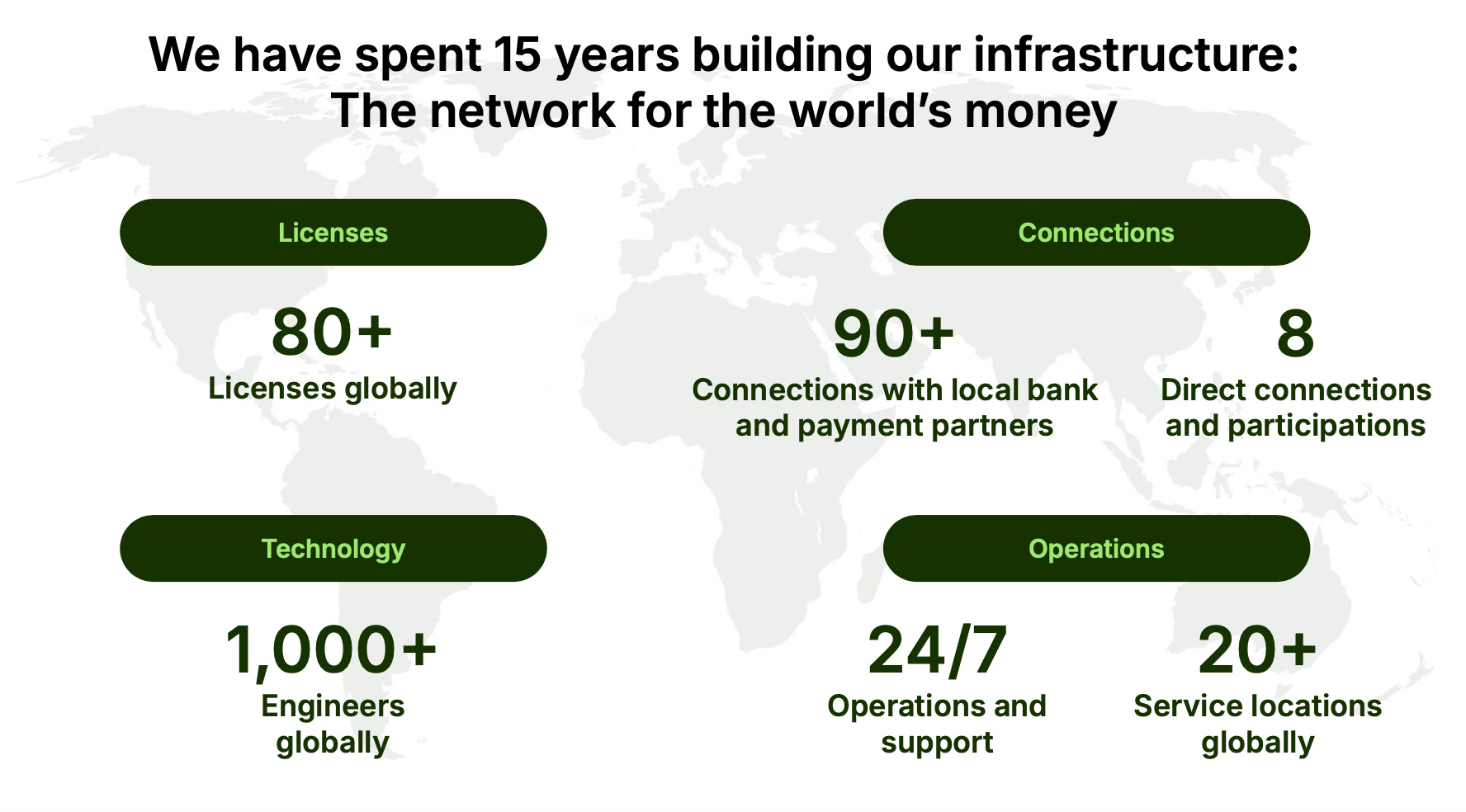

The source of Wise’s competitive advantage lies in the difficult-to-replicate process of bypassing the traditional correspondent banking system entirely. I think most investors glancing at Wise misunderstand this part.

During the Nasdaq presentation Q&A, David Scharf from Citizens Capital Markets pressed management on this exact topic, asking about the backlog of other remittance providers trying to replicate Wise’s feat of becoming a non-bank member of local domestic payment networks like ACH in the US, BACS in the UK, or Zengin in Japan.

“Wanted to follow up on the competition question. I mean at a high level, it seems like at the end of the day, the biggest differentiation for Wise as you bypass correspondent banks and became a nonbank member of individual payment networks. Can you speak specifically to first, just what are some of the hurdles and challenges for a nonbank to get accepted to a local payment network like ACH, BACS, [ Zengin ] And then secondly, since these payment networks by admitting you have sort of set the precedent for admitting a non-bank, are you aware of any kind of backlog of other remittance providers sort of seeking to ultimately embark on the same kind of integration.“

Founder and CEO Kristo Kaarmann’s response revealed the immense structural headstart Wise has and that younger FinTech upstarts AND legacy providers face. He noted that while Wise has been trailblazing through its first eight direct integrations, “in order to build up this network, it’s kind of not worthwhile doing just 2. You kind of need to invest behind doing the 30 or the 40 or the 50.”

This reality completely changes how we think about competition. Gaining direct access to a central bank clearing system as a non-bank financial institution is a regulatory and technical nightmare. It requires YEARS of intense local lobbying, securing bespoke financial licenses, maintaining pristine compliance frameworks, and embedding custom physical and digital infrastructure directly into domestic clearing houses. Doing this in a single country takes years of focused effort. To build a globally competitive cross-border network, a competitor cannot just succeed in Japan or the UK – they have to repeat this agonizing process dozens of times across the globe.

And importantly, as Kristo bluntly observed, “none has seriously started yet. So it’s hard for me to comment how far behind they will be. But it’s an enormous investment of time, efforts and the kind of expertise that you need to build up.” If no one “has seriously started yet,” Wise, which was founded in London in January 2011, has a 15-year headstart!

Insight #3 - On the SES Playbook

This fifteen-year operational lead is further reinforced by an exceptional economic model and corporate DNA known as the scale economies shared (SES) framework.

In a standard business model, growing transaction volumes should yield fatter profit margins as operating leverage dynamics are harvested that are promptly pocketed by executives and shareholders.

But that’s a rather vulnerable, and arguably short-sighted model to run a payments business as PayPal has learned the hard way. For years, PayPal’s branded checkout button commanded premium take rates – historically hovering around 2.9% plus $0.30 per transaction. This yielded strong margins because merchants paid a premium for PayPal’s trusted brand and built-in buyer base. However, aggressive unbranded competitors like Adyen and Stripe disrupted this dynamic. Instead of relying on a consumer-facing button, these processors embed directly into a merchant’s white-label checkout, driving massive volume by undercutting PayPal on price. Unbranded processing operates on razor-thin margins, often charging large enterprise merchants take rates well below 2%, and sometimes just basis points above interchange fees. To defend its market share, PayPal had to aggressively push its own unbranded solution, Braintree. But this strategic pivot forces a brutal trade-off: trading its high-margin branded volume for low-margin unbranded volume, effectively neutralizing the very operating leverage that executives and shareholders once took for granted.

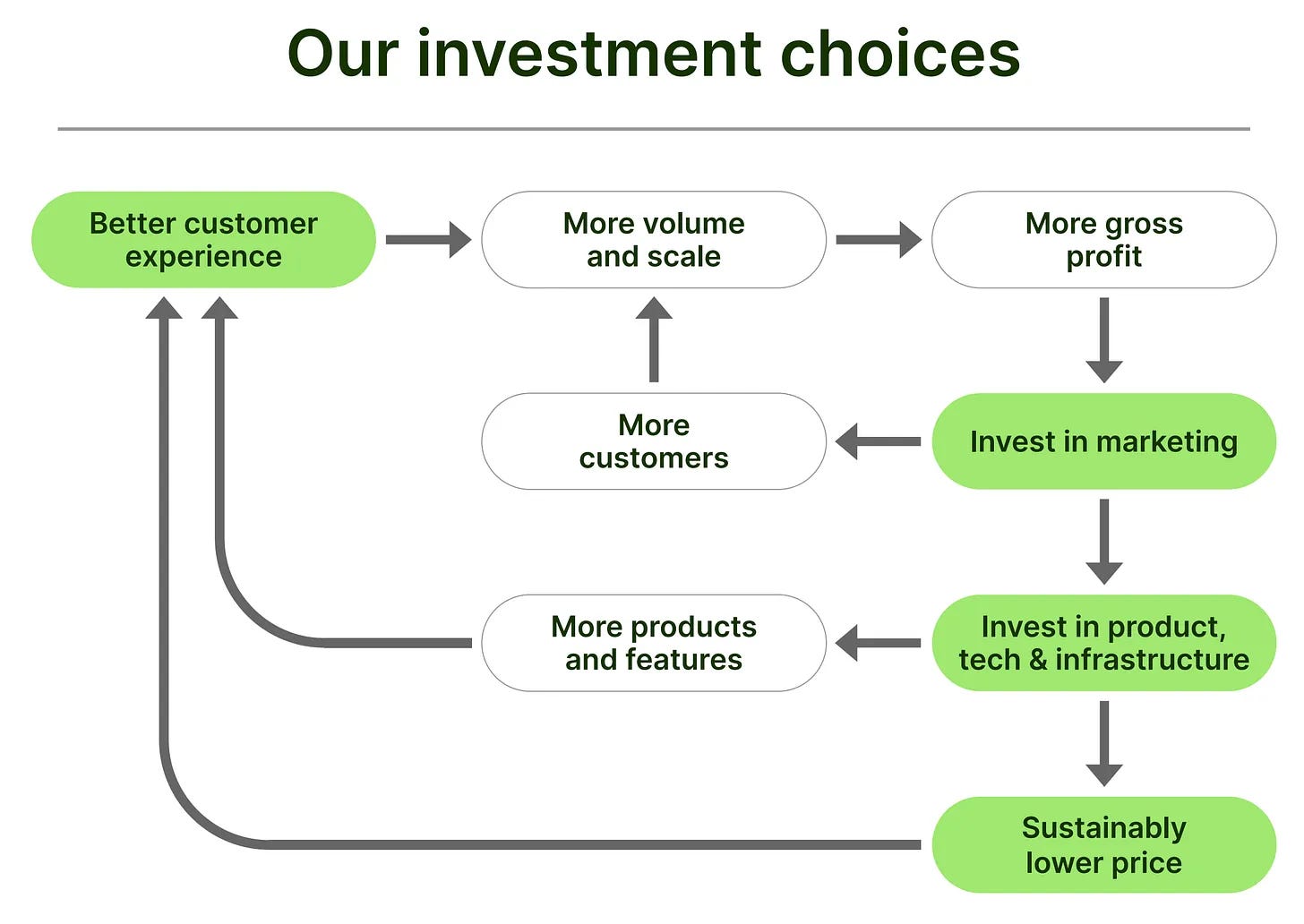

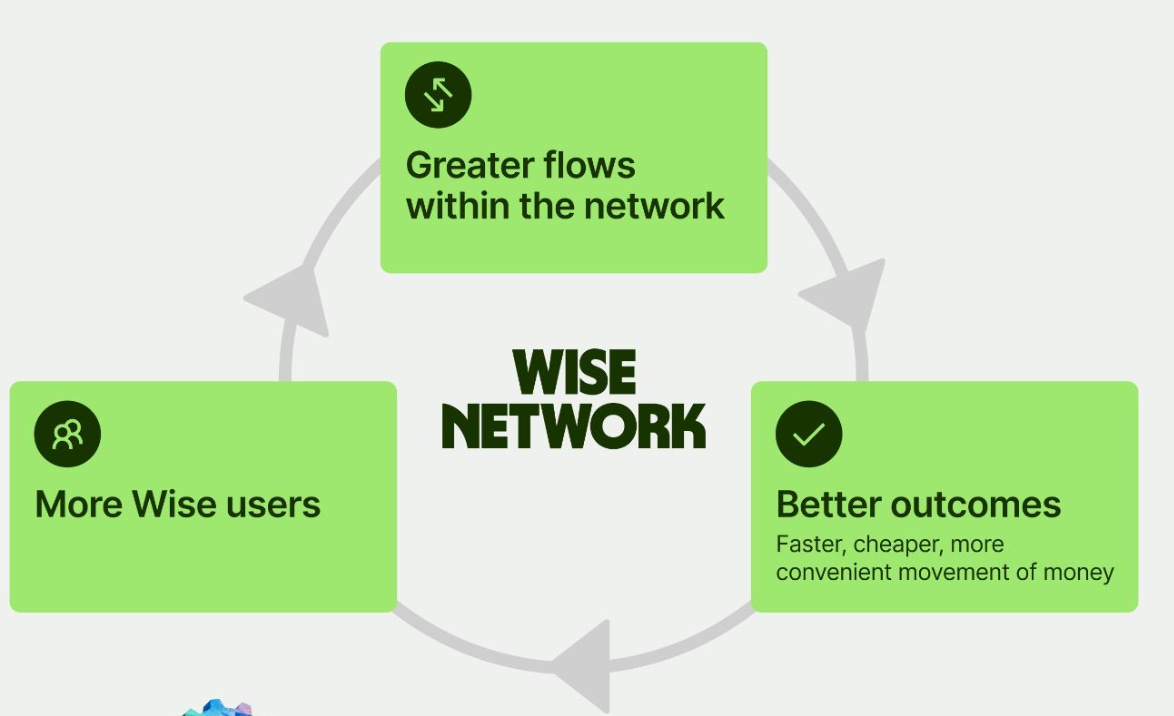

And here comes Wise! Because Wise flips this script entirely.

They treat their massive infrastructure as a utility, systematically returning the cost savings achieved through higher volumes directly back to the customer in the form of lower fees and faster speeds.

This creates an agonizing dilemma for any potential rival trying to catch up. If a well-capitalized competitor decides to spend the next decade and hundreds of millions of dollars building direct integrations into global payment systems, they will eventually emerge into the light only to realize that Wise has already used its massive scale to cut global average prices down to 52 basis points or lower. The competitor, lacking Wise’s multi-billion dollar volume and the underlying infrastructure, regulatory licenses, etc., etc., to subsidize their fixed operational overhead, would have to price their transactions at a devastating loss just to match Wise on day one. Wise has effectively commercialized its cost structure into an aggressive defensive weapon, starving out potential rivals before they can even achieve the scale and the infrastructure buildout required to compete.

When you blend this scale economies shared flywheel with the sheer operational friction of global regulatory licensing, it becomes incredibly difficult to envision any traditional competitor ever catching up.

The structural moat is simply too wide. Barring a radical, black-swan technological regime shift – such as the stablecoin disruption risk we already debunked – Wise’s position at the center of global cross-border rails looks increasingly bulletproof.

Insight #4 - Measuring the Scale Economies Shared Playbook: Nick Sleep’s Formula

To truly appreciate the strength of this operational framework, we might look past vague corporate buzzwords and actually measure the financial footprint of Wise’s economic engine.

Most of my readers are likely familiar with Nick Sleep, who famously generated a 921% return over 13 years at Nomad Investment Partnership by mastering a counter-intuitive concept: the aforementioned idea of scale economies being shared.

To quantify this dynamic, Sleep invented the robustness ratio, a metric designed to calculate exactly how much economic value a company passes back to its customers relative to the residual profit it retains for its own shareholders.

When Sleep ran these calculations on Costco, he discovered the wholesale retailer operated at a ratio of roughly 5:1. For every single dollar Costco kept in profit, it left five dollars in savings inside the consumer’s wallet compared to standard supermarket prices.

Costco is, in fact, considered the gold standard of scale economies shared.

Yet, Wise is weaponizing this exact formula today at an even higher clip, a reality made clearly measurable by the fresh financial disclosures from their recent Nasdaq listing.

When I first ran these calculations on Wise two years ago using their fiscal year 2023 disclosures, the results were staggering. Back then, the network saved its cross-border users £1.5 billion while retaining just £114 million in net income, yielding a jaw-dropping robustness ratio of 13.2. It was a textbook manifestation of a management team aggressively prioritizing multi-decade customer goodwill and terminal market share over short-term earnings optimization.

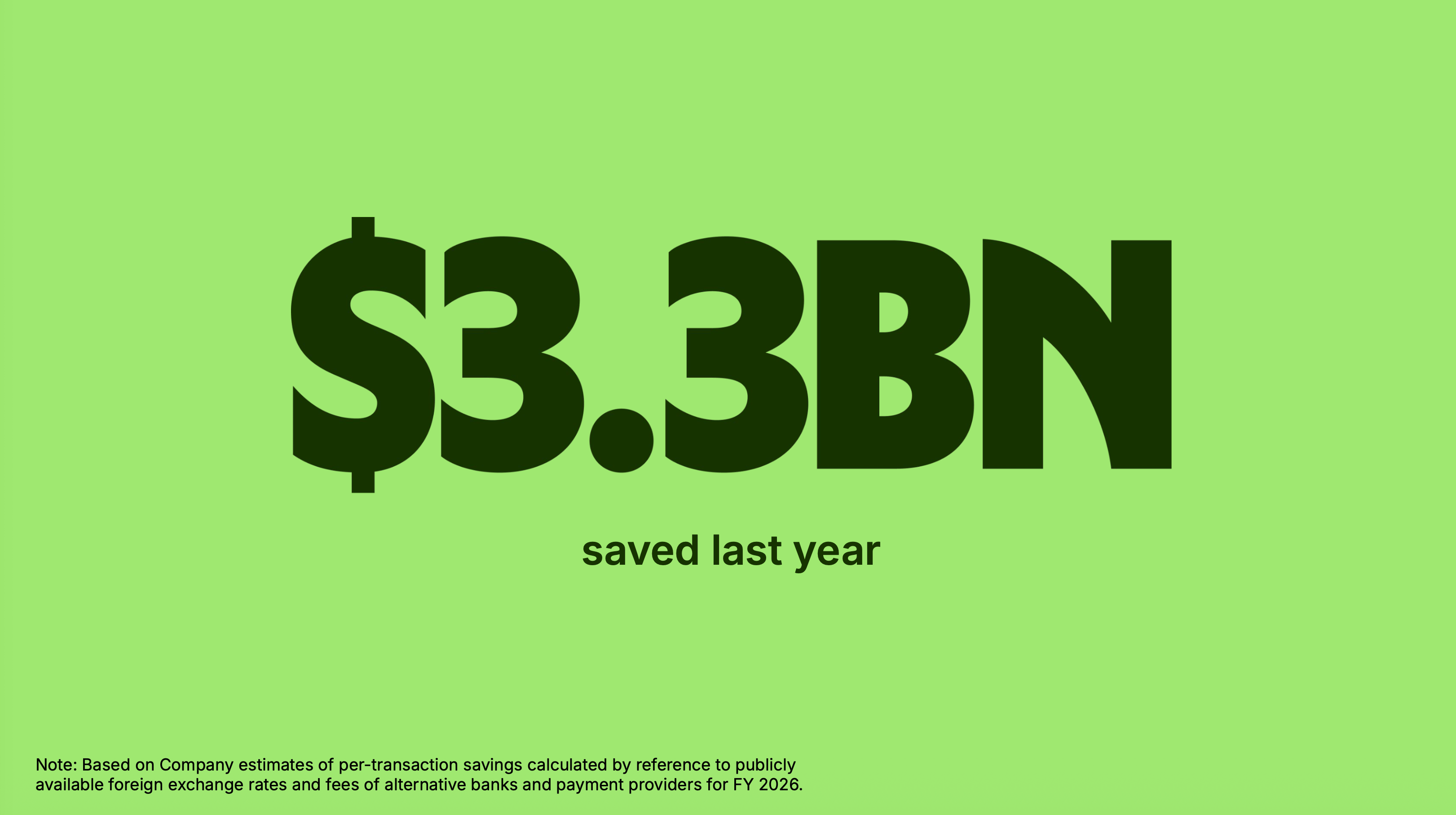

Updating the math with the preliminary fiscal year 2026 data allows us to see how that structural defensive perimeter is tracking. According to the listing presentation, Wise generated $3.3 billion in direct customer savings compared to traditional market alternatives.

Meanwhile, the business pulled in $2.5 billion in preliminary total net revenue. If we apply a net income margin of roughly 18% based on their first-half financial profile, Wise generated an estimated $450 million in full-year net profit for its equity owners.

Placing those updated metrics into the formula – dividing the $3.3 billion in quantified customer savings by the estimated $450 million in total shareholder profit – leaves Wise with a current aggregate robustness ratio of 7.33.

On a superficial level, an analyst might glance at this shift from 13.2 down to 7.33 and assume the company’s customer centricity is beginning to erode. That conclusion would be entirely incorrect, as it overlooks a massive structural evolution in the revenue mix.

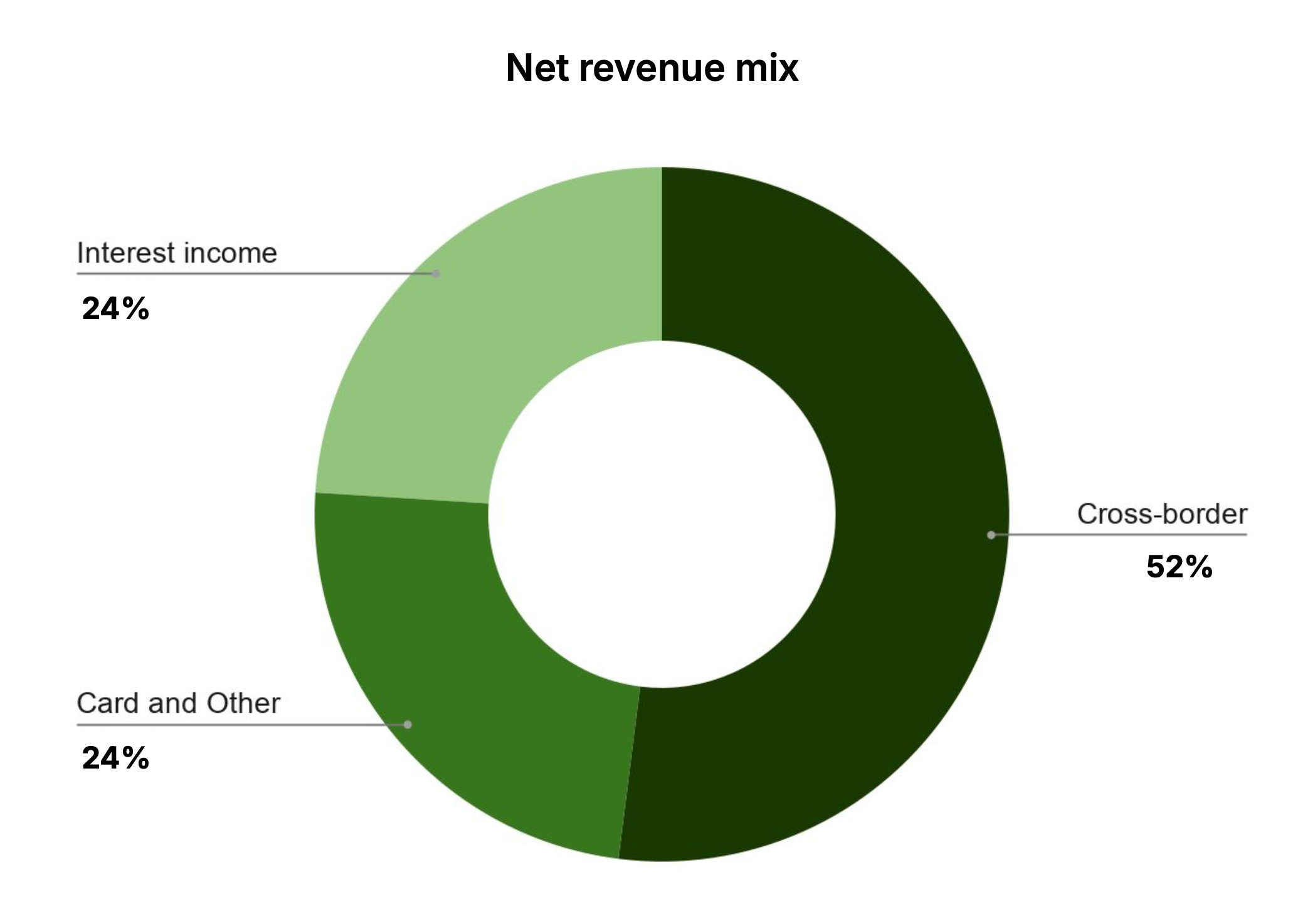

Back in the 2023 fiscal year, cross-border payments was the undisputed primary engine of the firm (around 70% of total revenue). Fast forward to today, and core cross-border transaction fees have stepped down to comprise just 52% of the total revenue mix. The remaining 48% is now driven by the rapid scaling of adjacent ecosystem products, specifically international card services and net interest income from customer balances.

This product diversification means that looking at the aggregate company-wide net income distorts the true underlying efficiency of the payment rails. The $3.3 billion in customer savings highlighted by management refers specifically to the efficiencies achieved on the cross-border transaction side of the house. If we isolate that specific segment, assuming a standard 18% profit margin on cross-border operations and halving the retained net income to align with its 52% revenue contribution, the true transaction-level robustness ratio remains comfortably in the exact same double-digit territory as before.

Even if you choose to take the more conservative, consolidated company-wide ratio of 7.33, the underlying economic reality remains an absolute powerhouse. It demonstrates that for every single dollar Wise keeps in net profit across its entire global enterprise, it actively leaves more than seven dollars (or up to $14) in its users’ pockets.

The best part is just ahead — unlock the full post to continue (insights #5-10).

Investing is the one domain where better thinking compounds. If this intro gave you new insights, the full piece goes even deeper. A paid subscription is an investment in your decision-making process – and your returns.

PS: Using the app on iOS? Apple doesn’t allow in-app subscriptions without a big fee. To keep things fair and pay a lower subscription price, I recommend just heading to the site in your browser (desktop or mobile) to subscribe.