Buy Good Companies, Don't Overpay, Do EVERYTHING ...

Terry Smith spent fifteen years telling us to do nothing. His latest letter does the opposite.

“I think people who study the psychology of investment will tell you that, you know, you can't have an end to certain types of market until the last hope is given up. I mean, I presume after that the entire UBS funds were switched into something which tracked the the Nasdaq index, bought all those things. And oh dear, there we are.“ - Terry Smith at this year’s Fundsmith AGM

Let me say something up front, before I say anything critical. I’ve learned an enormous amount from Terry Smith over the years. His quality-first principles, laid out in plain language that any investor could absorb, shaped how I think about businesses.

The rational temperament, the refusal to be dragged around by the crowd, the insistence that you focus on what a company actually does rather than what its share price did last week – that’s been an inspiration to me and to a whole generation of retail investors who found a way into serious investing partly through his letters and the recorded AGMs that were then uploaded on YouTube.

Earlier this year, when the pile-on over his underperformance was at its loudest, I was one of the people defending him. I watched this year’s AGM and came away thinking his reasoning was still clear, still rational, still willing to question the lazy conclusions you reach when you let herd instinct do your thinking for you.

Then I read the July letter yesterday evening. And I was, frankly, in shock.

Because it reads like a man throwing that rational thinking overboard.

A note on the spirit of this

One more thing before I get into it. I try to follow Buffett’s principle: praise by name, criticise by category.

I’m not going to manage that here. This post names names, and the name is Terry Smith. And in some weird way I feel bad about it, and will hit the release button regardless.

So let me be clear about the spirit in which it’s written. I mean it with the best of intentions – as food for thought, and if anyone at Fundsmith happens to read it, so much the better.

There’s also a simple reality that comes with the territory. When you manage billions – with a B – of other people’s money, you accept a degree of public scrutiny of your decisions. It comes with the chair.

There’s a line from the former German Chancellor Helmut Kohl I was thinking of in this regard. Faced with sharp press criticism, mockery, and political hostility over the course of his time in office, he expressed a version of the same idea again and again. Anyone who reaches for the highest office in a democracy has no business complaining afterwards about the harsh headwinds. You take the job, you take the weather.

My German readers can watch a clip in which he states exactly this here:

To this day the line gets thrown back at his successors (as in the clip above) whenever they grumble about the tone of the media.

And I think it applies, in its own way, to anyone managing billions of other people’s capital, too. Nobody forced the job on you.

Full Tilt

In poker there’s a concept called tilt. I played a lot of online poker in my younger days – my favourite platform, fittingly, was called Full Tilt.

Tilt is what happens when a good player stops playing his game. He takes a bad beat, or a run of them, and the frustration takes over. He starts chasing. He plays hands he’d normally fold. He abandons the discipline that made him a winning player in the first place, precisely because it stopped working for a stretch, and he convinces himself that the answer is to do more, do it faster, and force a result.

The tragic thing about tilt is that it feels like decisiveness from the inside. It looks like activity. It’s actually the absence of the thing that made you good.

I think Terry Smith might have just gone full tilt.

His whole credo, the thing printed on the tin, was three lines. Buy good companies. Don’t overpay. Do nothing. He shared this credo in his latest letter again.

And yet, as outlined in the letter, now he is doing an awful lot.

I count twelve buys and thirteen exits in a single half-year.

In his own words: “our portfolio turnover hit a high of 51% in the first half of this year.”

For a manager whose full-year 2025 turnover was 12.7%, that is … quite something.

It is the buy-and-hold monk at the poker table suddenly playing every hand at the table.

I tweeted yesterday that if someone had shown me the paragraphs laying out all these transactions back in April, I genuinely could not have told you whether it was an April Fool’s joke. And I mean genuinely.

Twenty-five major portfolio decisions in roughly six months? AppLovin, Uber, Netflix, TSMC, GE Vernova, Mastercard, Yum!, TJX, on the buy side. Novo Nordisk, Unilever, LVMH, Nike, Zoetis, Coloplast, Intuit, on the way out. This is anything but the Terry Smith we thought we knew.

So here’s the question I keep turning over. What stage of the market cycle is it when a die-hard quality investor – someone who has practised this exact discipline for decades – reinvents himself as a momentum trader?

“We will take more account of momentum — both fundamental and share price — in our investment decisions.“

I’ve always been a bit of a skeptic on the prices he paid, and I’ll come back to that. But the man’s identity was patience. This was his edge. When that breaks, it tells you something. Usually not about the companies. About the pressure. It’s on.

He sees the problem clearly. That’s what makes this so strange.

The frustrating part is that Smith’s diagnosis of the market is largely right, and beautifully argued. The letter’s first half is vintage Terry.

He lays out how a market now dominated by passive flows and the AI capex boom has become a momentum machine, one that no longer prices businesses on “profitability, returns on capital and growth – in other words the factors we focus on.”

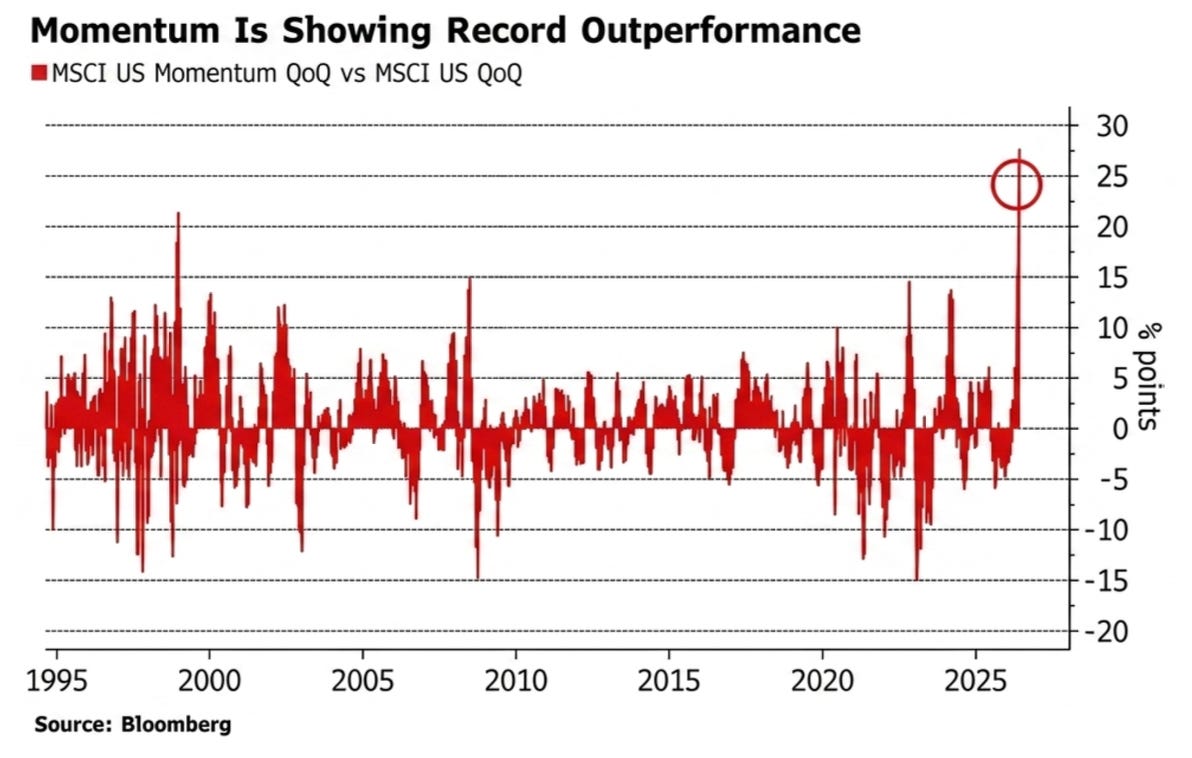

He leans on Simon Evan-Cook’s excellent “Victory for Passive!” piece. He quotes David Booth, of all people, admitting that “index funds are really trading desks.” He points out that active managers, though still 40% of assets, are down to something like 10% of actual trading volume, so the marginal price is set almost entirely by the flow machine. He shows the Bloomberg momentum chart sitting at a thirty-year high, more stretched than late 1999.

Momentum Is Showing Record Outperformance – “It is at a 30 year high and more extreme than in late 1999 just before the Dotcom bubble burst. As active fund performance continues to worsen, more people abandon it, producing a pernicious feedback loop.”

I agree with almost all of this. In fact, the most valuable thing I’ve published on this blog in recent months, I believe, isn’t any single deep dive. It’s my three-part perception-change framework, which is about exactly this: how to you improve your timing skills in a perception-driven market?

I’d encourage Smith to read it. If he messages me, I’ll gift him a lifetime subscription, no charge, of course. Again, I write all of this with good intentions. He seems to be an avid Substack reader as he even references a blog post he read on this platform early in the letter.

Playing a Different Game: When Fundamentals Aren’t Enough Anymore! (Part 1)

This will be a 3-part series. If you don’t want to miss the follow-up pieces, make sure to subscribe to the blog.

But here’s the thing that stops me cold. Having diagnosed a momentum bubble, having said in plain type that he has “no insight into how or when this passive-led momentum market will end, other than to say badly” – he then responds by leaning into momentum?

He tells us he will “take more account of momentum – both fundamental and share price – in our investment decisions.”

You’ve just described a casino where the roulette wheel is rigged and the last table of value players is being carried out on stretchers. And your conclusion is to pull up a chair and start betting on red because red’s been hot?

That’s the tilt. He sees the trap with total clarity and walks into it anyway, because standing still has become unbearable.

Learning from Druckenmiller

There’s a story every investor should have tattooed somewhere. In early 2000, Stanley Druckenmiller, one of the greatest to ever do it, walked into George Soros’s office and said he was selling all the tech stocks. This is crazy at 104 times earnings, he said. This is nuts.

He had it exactly right. And then he had to sit there and watch two young gunslingers inside the same firm make 3% a day, their little account up 50% on the year while Quantum sat flat. It drove him mad.

In his own telling: “So like around March I could feel it coming. I just – I had to play. I couldn’t help myself. And three times during the same week I pick up a phone, don’t do it. Don’t do it. Anyway, I pick up the phone finally. I think I missed the top by an hour. I bought $6 billion worth of tech stocks and in six weeks I had left Soros and I had lost $3 billion in that one play.”

Then the part that should stop any investor cold. Asked what he learned: “I didn’t learn anything. I already knew that I wasn’t supposed to do that. I was just an emotional basket case and couldn’t help myself.”

Read that and then read Smith’s letter again. Druckenmiller didn’t lose three billion because he misjudged the businesses.

He lost it because he couldn’t bear being cold while everyone around him was hot.

The diagnosis was right and the discipline broke anyway, precisely at the moment of maximum envy, precisely at the top.

That’s the same machinery I see running in this letter. Smith has the correct read on the bubble in the very same pages where he decides to start chasing it. He’s chasing. Full stop. I think that’s what’s really happening here. And that’s rarely a good long-term strategy.

And here’s the lesson Druckenmiller has spent the years since preaching, the one that matters most for Smith right now: when you’re not hot, you take a break.

You reduce size, you step back, you wait for a pitch you can actually hit. What you do not do is tear up the entire strategy, the entire identity you’ve built as an investor, because a cold streak has become psychologically intolerable.

Cold streaks are not a signal to become a different person. They’re a signal to protect the person you already are until the conditions turn back in your favour. That’s also your fiduciary duty, managing other people’s capital.

The consistency problem

Set the philosophy aside for a moment and just look at the trades against one another. They don’t hang together.

Where’s the consistency in his reasoning?

Take stock-based compensation. Smith flags SBC as a mark against Intuit, and it’s a fair criticism.

“Intuit – Although we only recently repurchased Intuit we were sensitive to the way in which they have reacted to the poor Mailchimp acquisition as this is why we sold the shares in the first place. The fact that they have now taken to giving results ex Mailchimp both shows how bad the acquisition was but also worries us about a continuing state of denial.

Sage – We switched our position from Intuit into Sage, the other main operator in accounting software. Sage has much less reliance on share based compensation, a lower rating and does not have Intuit’s record of injurious acquisitions. ROIC: 18%, FCF yield: 6.0%.“

Yet in the same letter he’s buying Veeva Systems, a company famous for exactly that.

I’ve written about Veeva myself – it’s a genuinely excellent business, arguably cheap here, and it fits his quality profile well.

5 Quality Names Ready to Turn?

Identifying a high–quality business is only half the battle in this market. The other half – the part that keeps most investors up at night – is the entry price.

I’m not knocking the buy. I’m knocking the logic that dings one name for a trait while waving it through on another in the same breath.

Then there’s the tape itself. Does Uber have momentum? Take a look at the chart yourself. Where?

Hold that same thought against Novo Nordisk on the sell side. Novo has been through a historic drawdown. Truly historic.

If anything, it’s a name in the early stages of building a base, possibly building momentum, precisely the kind of setup a momentum convert should be interested in.

Selling it after a historic collapse – “parlayed a market leading position in the biggest drug discovery in decades into an investment disaster” – while buying into cleaner, more expensive stories where the good news may already be in the price, is the opposite of what the new doctrine implies.

It’s selling low on the ugly one and buying high on the pretty one. That’s not momentum discipline. That’s just discomfort management.

And the whipsaw on his own recent convictions is the part that genuinely startled me.

At the February AGM – five months ago – Smith told shareholders, in as many words, that he was rotating into EssilorLuxottica, Wolters Kluwer and Zoetis as the businesses that would “survive and prosper better” when the reckoning comes.

Five months later, all three are on the sell list. What the …

He praised Wolters Kluwer’s CEO at length, bought it, and has already sold it. He framed Zoetis as a survivor and is now dumping it near multi-year lows, after the stock was more than halved on the Librela scare and the Q1 miss – a beaten-down quality name at the exact kind of valuation his old playbook was built to exploit.

This isn’t a change of mind over a cycle. It’s a change of mind over a quarter or two. Conviction isn’t supposed to have a shelf life measured in months.

What is Smith’s edge, really?

Here’s the question I’d want Smith to ask himself: What is his edge?

Not his philosophy, not his brand, his actual edge – the thing he spots and leans into to exploit it.

And where does his skillset shine? Where is he better than the person on the other side of the trade?

Because you only make money in markets by being right about something the price doesn’t yet reflect, and you can only reliably do that where you have a genuine advantage.

I’ve never believed Smith’s core competence was timing or trading. I doubt he and his team are skilled momentum traders, and I mean that as an observation rather than an insult. Why would they be?

Momentum is a craft, too. The people who do it well have done it for years, built systems around it, developed a feel for flows and reflexivity and the moment a trend exhausts itself.

A team trained for decades in patient, fundamental, business-quality analysis is not going to walk onto that field and outplay specialists who live there.

Decade-long value-trained investors do not out-trade career momentum traders. That’s not how skill transfer works. You don’t get to be world-class at the discipline you spent thirty years explicitly not practising.

What I always believed Smith’s edge actually was: analytical rigour in identifying above-average businesses, paired with the behavioural temperament to sit on them and do very little. Or the patience to sit on the sidelines and wait. Wait for the conditions that present bargain opportunities.

That combination is rare and valuable. It’s genuinely hard to find great companies, and it’s even harder to hold them through noise without fiddling. That was the advantage he had.

Buying and selling twenty-six names at once is the precise opposite of that temperament. It’s abandoning the one (temperamental) edge he had to go compete in an arena where he has none.

If the game has changed such that his skillset no longer gives him an edge, the answer isn’t to acquire a new skillset overnight that takes others a career to build. The answer is to be honest about what you’re good at and accept that there will be stretches – possibly long, painful ones – where the market doesn’t reward it. That’s not failure. That’s the cost of having a style at all. And “quality” is simply not in vogue right now.

Recommended reading:

The Paradox of Investment Skill: Why Exceptional Thinkers Fail in Crowded Games

I find myself returning to a core philosophy of the markets lately, and I decided to write about it, largely because I want to permanently pound this concept into my own brain. Over the past few days, I have been hashing out the nuances of market dynamics with Tiho Brkan, and his perspective on this matter is entirely spot-on. We kept coming back to a f…

The timing blind spot, and the irony in these sales

There are three ways to express skill in investing:

And I’ll say something now that I’ve believed for years, through the good times as well:

I always admired Smith’s security selection.

I have always been skeptical of his timing.

He frequently bought companies at prices I would never have paid – 20-times-plus normalized earnings, and often a good deal more.

For most of the post-GFC era that didn’t matter, and I think it’s worth being honest that a lot of the Fundsmith record was riding a wave. Quality was the factor of the 2010s.

The compounders he owned went from reasonably cheap in the early part of the decade, to expensive, to genuinely absurdly rich.

A stock you could have bought on a 7-10% free cash flow yield re-rated to 4-5%, and Smith kept buying. Then it re-rated to a 2% yield.

And that – the 2% yield, the top of the multiple expansion – was the moment to show timing skill and trim. That’s when discipline on price would have earned its keep.

He didn’t.

And here’s the bitter irony of the current letter. Some of the very names he’s now selling are back down to the kind of 7-10% yields that, on his own quality framework, ought to make them buys, not sells.

He held them up the entire way, watched them de-rate, and is now letting them go at the bottom of the valuation range. Bought richly, sold cheaply. That is the single most expensive pattern in this business (buy high, sell low), and it’s the shadow side of never having had timing as part of the toolkit.

Momentum-adjacent selling of your cheapest, most beaten-up names is not a refinement of the strategy. It’s the timing weakness finally showing up on the sell side, having already shown up on the buy side a decade ago.

The real reason: it’s the structure, not the market

So why now? I don’t think this is really about a considered evolution of philosophy. I think Smith is feeling the pressure, and the pressure is structural.

He runs an open-ended fund. That single fact governs everything.

When investors redeem, he has to sell to meet it, whether or not it’s a good time to sell. He said it himself, and to his credit he said it plainly: a buy-and-hold approach “can only work if you are not subject to flows, and we are.”

He even reached for the old line about the market staying irrational longer than you can stay solvent – “Sticking to our current approach may well fall foul of the adage that the market can remain illogical longer than we can remain in business.”

Read that again, because it’s the whole letter in one sentence. He is not describing an investment thesis. He is describing a business risk to Fundsmith LLP.

If this market environment persists for another few years – and momentum bubbles can persist for an uncomfortably long time – and the fund keeps underperforming, redemptions accelerate even further, assets bleed, and at some point the vehicle itself is in jeopardy.

Note his own tell: Buffett could catch falling knives during the salad-oil crisis because he did it inside a closed structure he controlled. Smith flags exactly this distinction, that Buffett “executed this strategy in a closed fund which he controlled not an open-ended fund.”

He knows precisely what’s constraining him. The tilt isn’t coming from the charts. It’s coming from the redemption queue.

And this, I believe, is the single biggest advantage the individual investor has over Terry Smith. You don’t have flows. Nobody can redeem you. You will never be a forced seller at the bottom because somebody else panicked. When the market is at its most irrational and the opportunities are richest, the open-ended manager is often selling into it to fund withdrawals, while you can simply sit. Permanent capital is the retail investor’s structural edge, and most people don’t even realise they’re holding it. Smith’s letter is, inadvertently, the clearest argument for it I’ve read in a while.

He told us this himself, at the AGM

The thing is, Smith understands all of this better than almost anyone. He essentially narrated the whole trap out loud at this year’s AGM, telling the story of Tony Dye. It’s worth quoting at length, because it’s remarkable in hindsight:

“I was head of research at UBS before I managed to famously get myself fired. And when I was there, a gentleman who ran UBS Phillips & Drew Fund Management was a guy called Tony Dye. And Tony was a guy who was very vociferous about the fact that he thought the dot-com boom was a sham and that was going to burst and cause catastrophe. Stuck with the old line stocks … And he used to have lunch with me from time to time … and say to me, ‘Terry, do you think I’m mad?’ And I said, ‘No, you’re not mad, Tony, but your timing is quite likely going to be your undoing.’”

Dye was right about the bubble. He was fired on 1 March 2000 for sticking to his discipline while it hurt. That date, as Smith notes with a showman’s timing, “is the same day marked on the Nasdaq chart.” The top. The manager who saw it most clearly was removed the very day he was vindicated, because the pain had lasted just long enough to break his backers’ patience. “You can’t have an end to certain types of market until the last hope is given up.”

Then Smith went further and put up the Cambridge Associates and Research Affiliates data on when investors fire managers, and delivered the punchline himself:

“The time to fire a fund manager is when he’s doing very well … the guys who were doing 7.2% under-performed the guys who were under-performing. And so it is on 1 year and so it is on 3 years. And look, the time to fire us, were you going to do so, was about 2021.”

He knows the game. He knows that capitulation marks the bottom, that the manager who abandons his discipline at the moment of maximum pain is usually selling the low, that being right too early is indistinguishable from being wrong right up until it isn’t. He told the whole room, months ago, that the time to fire a manager is when he’s performing, and the time to back him is through the drawdown.

And now here he is. Terry Smith is capitulating. I never thought I’d write these lines.

Tony Dye, at the lunch table, deciding that this time he’d better start buying the Nasdaq after all.

Where this leaves us

I want to be careful not to overclaim. Smith may be right that the environment has changed in a durable way, and he may navigate the new one better than I expect. The buys, taken individually, aren’t crazy – several are excellent businesses, and a few, like Veeva, I’d happily own – at the right price.

Quality investing has had a genuinely brutal five years, and it is easy to critique from the cheap seats, with no billions and no redemption queue and no shareholders emailing at midnight. I hold the permanent capital he’d love to have. That’s not nothing, and it colours how easy this is for me to say. I’m not the “man in the arena” here. Smith is.

But the pattern is the pattern. A manager whose edge was patience has stopped being patient. A manager who diagnosed a momentum bubble has decided to chase momentum. A manager who told us the time to fire someone is when they abandon their discipline has abandoned his. And he’s doing it, on his own admission, because he runs a vehicle that can’t afford to wait as long as the strategy might require.

The old mantra was three lines, and the third line was the hardest and the most valuable: DO NOTHING.

It was hard precisely because doing nothing, in a screaming market, feels like negligence. That third line was the edge.

Turning it into DO EVERYTHING doesn’t fix the problem. It just converts a quality investor with a temporary performance issue into a momentum trader with a permanent skill deficit.

I hope I’m wrong. I’ve been wrong about him before, in his favour. But if you asked me what this letter is, I wouldn’t call it an evolution. I’d call it tilt. Full tilt. And the one thing every poker player learns, usually the expensive way, is that you can’t win it back in a single session by playing more hands. You win it back by getting up, clearing your head, and going back to the game you actually know how to beat.

Do nothing was never the weakness. It was the whole point.

Feel free to share your thoughts in the comments below.