The Paradox of Investment Skill: Why Exceptional Thinkers Fail in Crowded Games

Tables, Rakes, and Time: Why Your Investing Skill Is Worthless Without an External Edge

I find myself returning to a core philosophy of the markets lately, and I decided to write about it, largely because I want to permanently pound this concept into my own brain. Over the past few days, I have been hashing out the nuances of market dynamics with Tiho Brkan, and his perspective on this matter is entirely spot-on. We kept coming back to a foundational distinction that most market participants completely distort or overlook: the difference between internal skill and an external edge.

"First answer the question, 'What's your edge?" - Seth Klarman

The Poker Room Paradox: Why Raw Talent Fails at the Wrong Table

To understand this clearly, I often look back to my late teens and early twenties, a period of my life during which I spent a good amount of hours each week playing poker online.

I believe, in poker, the demarcation between skill and edge is brutally transparent – and easier to grasp than in investing, I believe – because it can be quantified with mathematical precision, and if you play at multiple tables simultaneously, sample sizes are large (in contrast to the handful of bets you place in investing).

You measure your performance in big blinds won per one hundred hands played. If you possess superior technical proficiency, your long-term expected value rises.

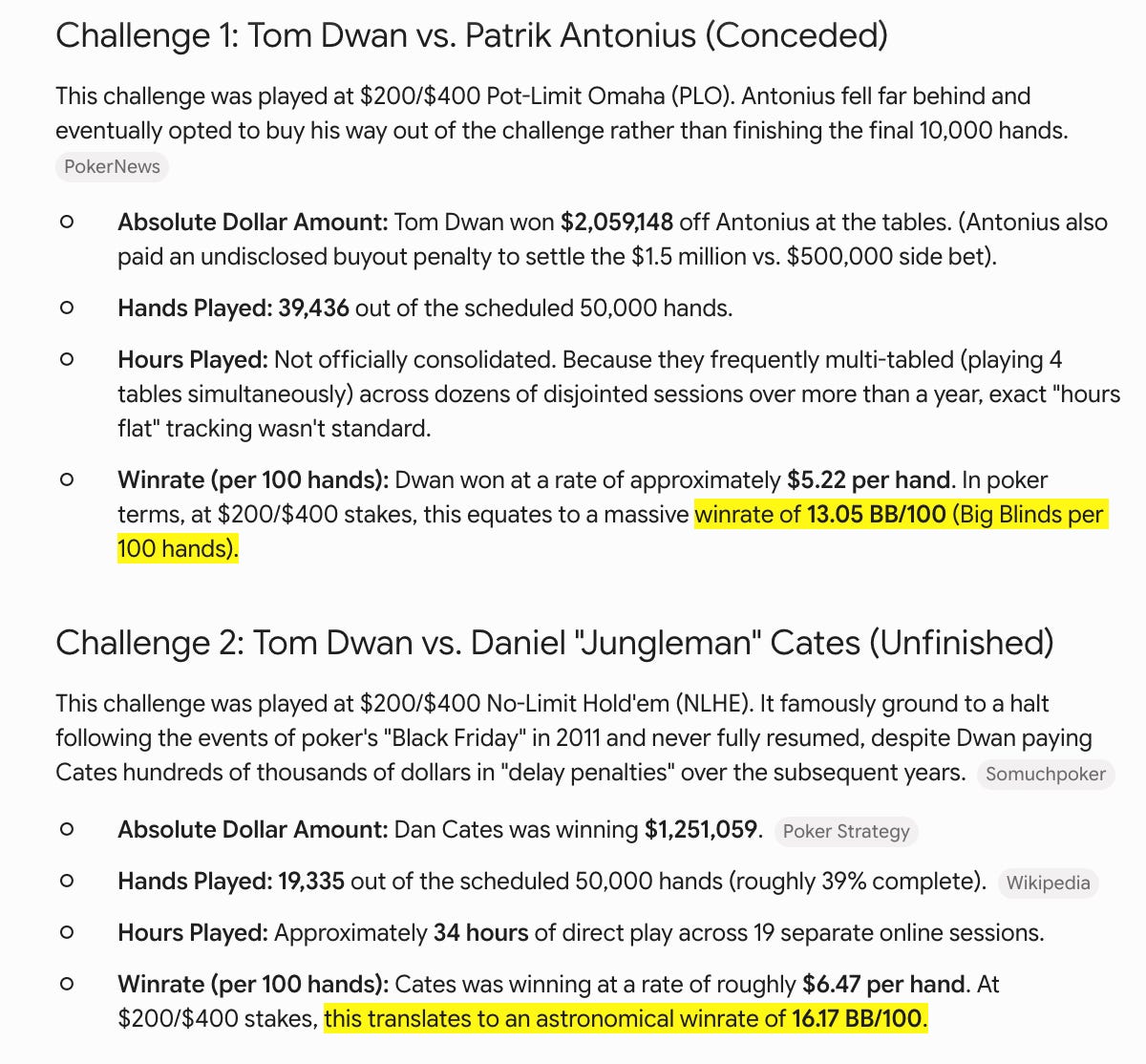

Consider the "durrrr" Challenge, for instance, which was a legendary high-stakes online poker wager issued in 2009 by Tom "durrrr" Dwan, who offered to play anyone in the world (except Phil Ivey) heads-up for 50,000 hands at $200/$400 stakes, backing his confidence with a massive 3-to-1 side bet where he risked $1.5 million against an opponent's $500,000. It became a defining spectacle of poker history that ultimately ended in incomplete drama: Finnish pro Patrik Antonius conceded the first match in 2010 after falling over $2 million behind, while the second match against Daniel "Jungleman" Cates – who was crushing Dwan for $1.25 million – was abruptly halted by the 2011 "Black Friday" shutdown of US online poker and never formally finished.

I’ve attached the final results and the respective win rates (measured in BB/100 hands) below. For context, in modern heads-up poker, a win rate over 5 BB/100 is considered a significant edge. Both of these challenges saw incredibly high win rates, suggesting that while at the beginning the challenge, both players thought they had an edge on the other, in reality, only one of them had (of course, in a heads up setup; it’s more complex at a six-seat table).

In poker, table selection matters.

You could be the tenth-best Texas Hold’em player on the planet, but if you sit at a table with the nine players who are better than you, you are the sucker.

Throw in the casino rake – the structural cut taken by the platform or house – and a hyper-competitive table will easily turn a world-class player into a break-even grinder.

You simply cannot out-skill a terrible environment.

This exact dynamic governs the global stock market. Think of it through the lens of a classic fishing analogy which Charlie Munger frequently referenced: some bodies of water are teeming with fish, meaning you do not even need fantastic talent to walk away with a heavy catch. Other waters are so heavily fished and depleted that no matter how legendary of an angler you are, you are going to struggle to catch anything at all.

When you can locate an attractive setup (which in itself may be a skill) – a market pocket overflowing with fish – you can exploit that external inefficiency comfortably.

Conversely, when competition is fierce and the “paradox of skill” kicks in, the edge vanishes, the game becomes dictated primarily by luck, and even the elite practitioners begin to flounder.

As Michael Mauboussin famously observed, all the investing skill in the world means absolutely nothing if you cannot find an attractive opportunity to exploit or an easy game to play.

“The key is this idea called the paradox of skill. As people become better at an activity, the difference between the best and the average and the best and the worst becomes much narrower. As people become more skillful, luck becomes more important. That’s precisely what happens in the world of investing. […] That said, over longer periods, skill has a much better chance of shining through.”

– Michael Mauboussin

This brings us to a critical, baseline definition. You possess skills; you do not possess an edge. An edge is an entirely external development, a situational setup or a behavioral inefficiency that appears in the market landscape for you to exploit. It is an event.

But it may also disappear! Think of a broader market panic for instance, where the wisdom of the crowd turns into the madness of the crowd.

Hence, it is not necessarily a repeatable part of the investment process. You can spot “edge-favoring” setups and lean into them, but they may be temporary.

Security selection skill, on the other hand, is an internal attribute. It is comprised of technical sub-skills like parsing complex financial statements, understanding corporate accounting, assessing competitive dynamics or management integrity, modeling cash flows, and analyzing chosen competitive strategies or incentives embedded in compensation packages. Mastering these disciplines makes you a highly competent analyst.

But while these “sub-skills” are essential, they represent internal capability rather than a market edge, which only manifests when a structural breakdown creates a deep mispricing.

Unless you are a political insider with an uninterrupted, asymmetrical flow of corporate data – a rare, controversial exception that someone like Nancy Pelosi or the Trump family might enjoy – you cannot personally own an edge. It belongs strictly to the environment.

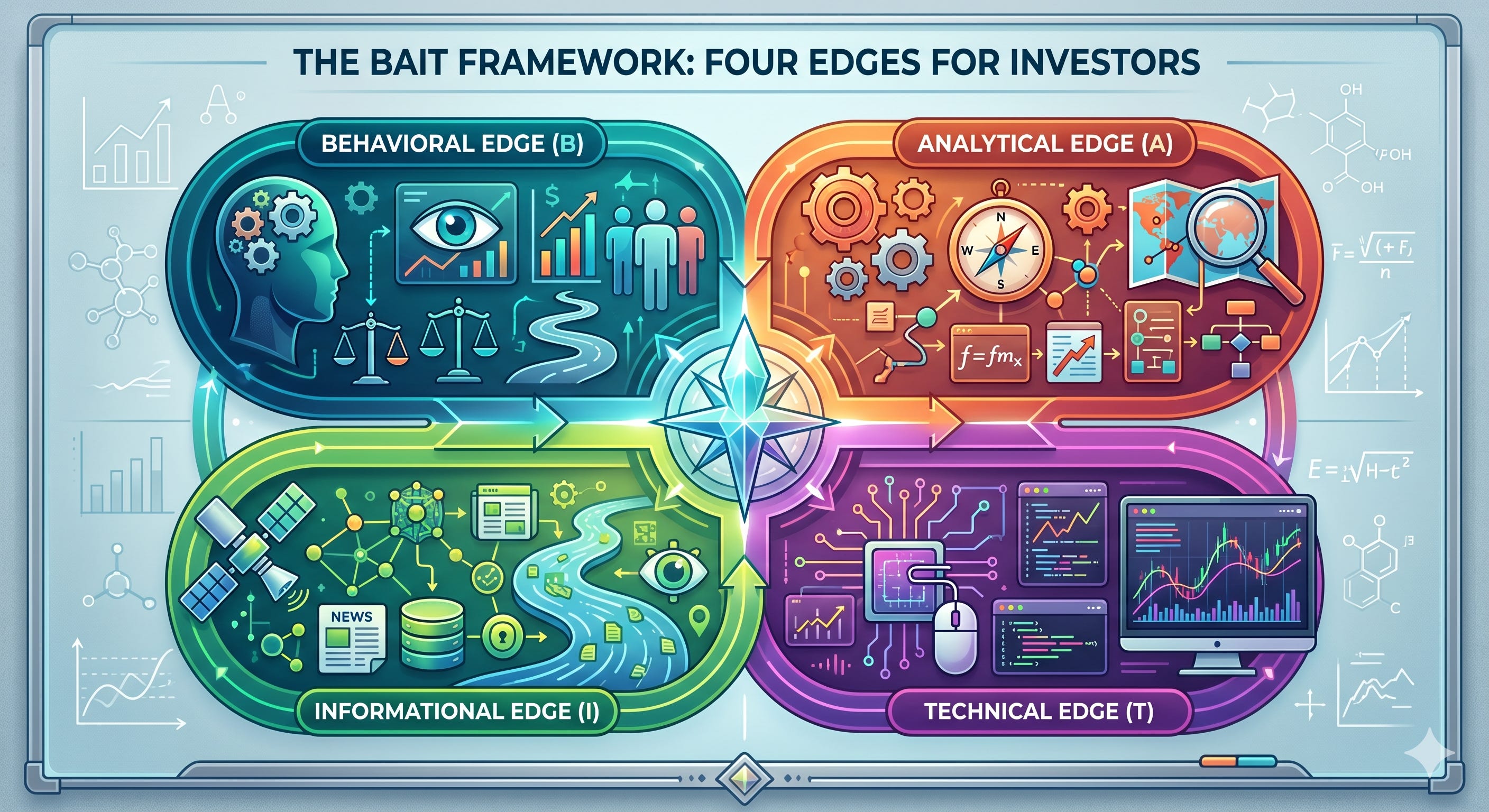

The BAIT Framework & How it Defines Your Counterparty’s Mistakes

To truly exploit an edge, you must transition from broad philosophy to a rigorous taxonomy. If you want to actively look for setups that may present an edge, you have to isolate exactly how these setups manifest in the wild.

This brings us directly to the BAIT framework, a mental model built on the reality that markets are frequently choked with …

behavioral (B),

analytical (A),

informational (I), and

technical (T)

… inefficiencies.

“Broadly, Bill Miller argued that there are three competitive advantages in investing: informational (I know a meaningful fact nobody else does); analytical (I have cut up the public information to arrive at a superior conclusion) and psychological (that is to say, behavioural). Sustainable competitive advantages are usually a product of analytical and or psychological factors.” - Nick Sleep

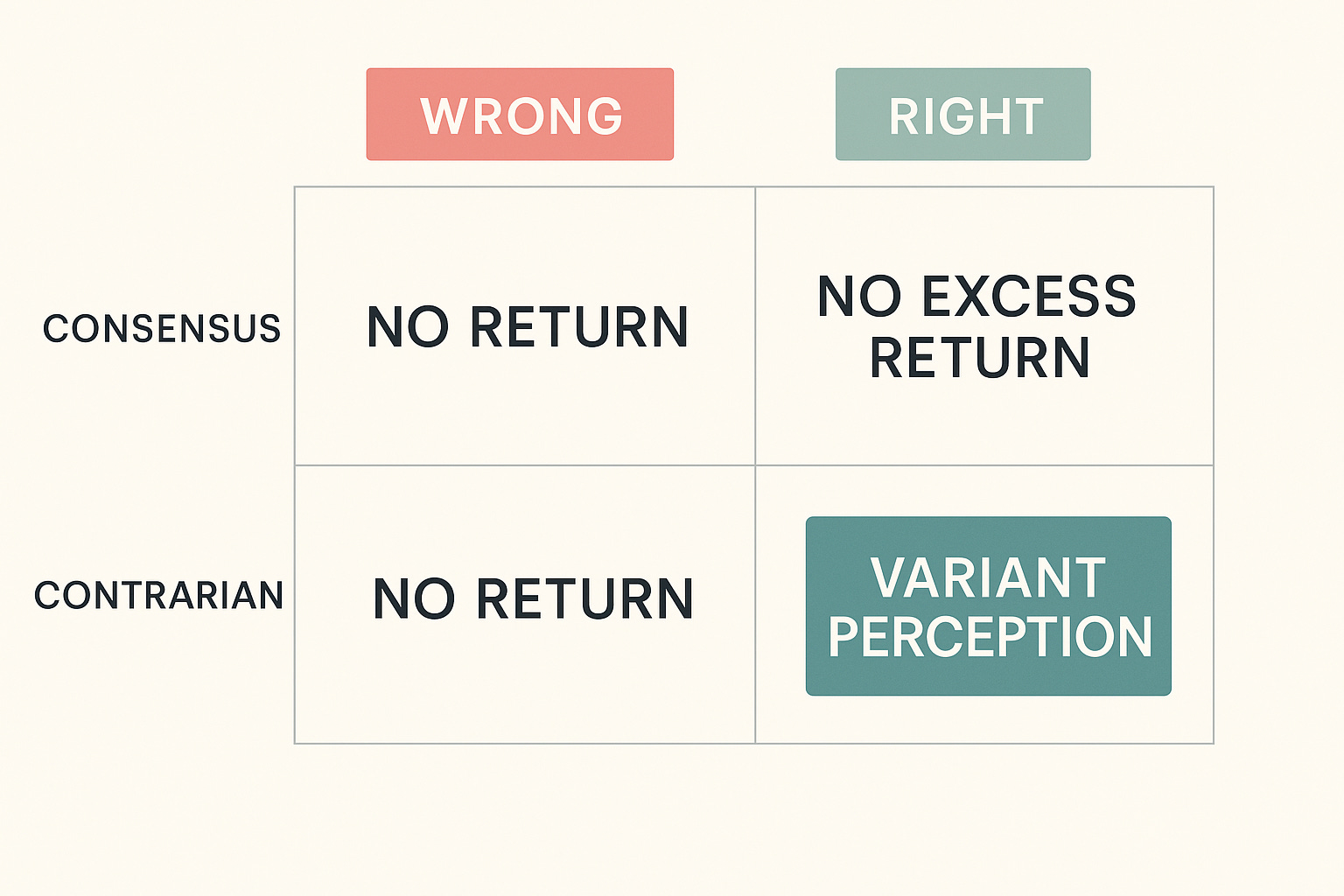

Before we explain each edge in more detail, let me share some general observations: An edge only exists when you can confidently identify who is on the other side of your trade, while proving with sound theory or empirical evidence why they are wrong and you are right.

If you cannot articulate the counterparty’s specific error, you are the mark at the table (we’re back to the poker analogy).

In the vocabulary of modern finance, a market inefficiency can be expressed in several distinct ways depending on your level of mathematical rigor. It represents a (positive) expected value that beats the return generated by the broader market. If the market generates a 9% IRR over the next five years, your edge should be measurable by you achieving a higher 5-year IRR. Buffett, the greatest investor of all time, CAGR-ed at roughly 20% over his lifetime (many decades) fwiw. Highly impressive.

But again, the calculation of an “edge” works beautifully in games of defined risks and outcomes, games where you can quickly accumulate large sample sizes, though it becomes significantly cloudier in games of true economic uncertainty and games where you bet infrequently (think of the handful of bets an investor places in a calendar year vs. the 100,000+ of hands a poker player plays in the same time frame) where calculation errors creep in and luck becomes another dominant force.

Culturally, the fancy way to label this phenomenon is a variant perception – a well-grounded view that stands completely apart from the consensus.

Practically, however, an inefficiency is just the gap between current market expectations and structural fundamentals. You could measure this delta using traditional discounted cash flow modeling and reverse DCF analysis to isolate exactly what the market is pricing into an asset today.

There is a critical secondary considerations here that most amateur investors ignore: position sizing. Size matters. In fact, you should never place a bet without a clear edge, regardless of how highly you rate your own internal skill. This is really important to understand, and if anything, this should be your key takeaway from reading this piece.

“Without an edge, one should not bet. Ever. Regardless of skill.“ - Tiho Brkan

Your bet sizing must be dictated exclusively by the magnitude of the external edge you are exploiting. The larger the edge, the larger your capital allocation can be; in theory, up to a mathematically optimal limit. Push past that threshold, and over-betting will inevitably lead to financial ruin.

"Playing poker in the Army and as a young lawyer honed my business skills .. What you have to learn is to fold early when the odds are against you, or if you have a big edge, back it heavily because you don't get a big edge often." - Charlie Munger

And to tie this discussion back to poker again: this is the exact blueprint used in modern poker. In a game that is now effectively solved, a mathematically optimal bet size does in fact exist for every scenario. However, applying this in practice requires a nuance that amateur investors often miss: you cannot simply deploy a single, predictable size all the time. To keep opponents from exploiting, elite players must balance their strategy by thinking in bet-size ranges. You scale your allocation based on the strength of your edge, while remaining mathematically unpredictable to the rest of the table.

Back to investing … I’d argue that in today’s environment, locating these setups, setups that offer you to lean into and exploit an edge is brutally difficult. Wait for the fat pitches.

“We’re always looking for something where we think we have an insight which gives us a big statistical advantage. And sometimes it comes from psychology, but often it comes from something else. And we only find a few, maybe one or two a year.” - Charlie Munger

So what do the four edges mentioned above actually refer to?

“Knowing when you have an edge is very difficult, but in my experience it is the critical factor that allows us to stand out in the ultra-competitive world of institutional money management.” - Brian Bares

Behavioral Edge

I view the behavioral edge as a direct exploitation of psychological breakdowns in the market landscape. When investors are gripped by collective panic or blind euphoria, they stop acting as cold calculators and begin reacting to raw emotion. Fear reigns supreme. This herd mentality creates an external setup where asset prices dislocate wildly from their actual worth, creating an attractive playground for rational capital. My role here is to let my intensive training in sentiment take over while the crowd makes expensive, emotional mistakes. You cannot force these opportunities. They appear situationally when market participants abandon their senses, hand-delivering a structural mispricing that you can calmly capitalize on if you possess the internal discipline to remain completely rational while others implode.

“Both poker and investing are games of incomplete information. You have a certain set of facts and you are looking for situations where you have an edge, whether the edge is psychological or statistical.” - David Einhorn

Analytical Edge

An analytical edge manifests when you look at the exact same public data as your competitors but arrive at a vastly superior conclusion. This is the art of variant perception, where you articulate a well-grounded view that stands completely apart from the consensus. The consensus is wrong. I actively execute this edge by calculating the stark delta between current market expectations and underlying business fundamentals, utilizing tools like a reverse discounted cash flow analysis to decode what the market is pricing in. It requires deep cognitive skill. You are essentially identifying a massive pricing breakdown because the crowd is misinterpreting a company’s long-term trajectory, allowing you to capture a setup where your unique interpretation of the data aligns with reality while the market remains blind.

“Investors operate with limited funds and limited intelligence; they do not need to know everything. As long as they understand something better than others, they have an edge.” - George Soros

And as Howard Marks very clearly articulates in the quote below, more data or more manpower does not equal better results. Raw scale is a commodity. Anyone with enough capital can hire 160 analysts, buy expensive data terminals, or run massive computing clusters. If everyone has access to the same raw numbers (lack of informational edge) and processes them using standard methodologies (lack of analytical edge), they will arrive at the exact same conclusion. That’s why some fund managers can also ask for multi-million dollar paychecks. They possess unique abilities that allow them to arrive at variant perceptions that turn out to be correct.

"I was recently on a panel that was asked what gave our firms their edge. One panellist responded “we have 160 analysts around the world”. To me, that response demonstrated a total lack of insight. Unless those 160 analysts are more astute than the average investor, they’ll contribute nothing. Certainly another 160 wouldn’t double the managers ability to add value (if they could everyone would be an analyst).” - Howard Marks

Many people argue that finding an analytical edge has become incredibly hard and that this edge may entirely disappear soon.

"There are a lot of trends going on now that make the business very tough. You've had a lot of smart people come into it, making it much harder to find opportunities. You need to determine what your real competitive advantage is." - John Phelan

PS: Funnily, I also came across this quote from Ray Dalio on the website of MastersInvest, and I’m wondering whether Marks was actually referring to Dalio?

“If you’re going to come to the poker table, you’re going to have to beat me. … We have 1500 people who work at Bridgewater. We spend hundreds of millions of dollars on research and so on, we’ve been doing this for 37 years.” - Ray Dalio

PSS: Don’t forget to constantly update your (analytical) view as new information flows in.

Informational Edge

The informational edge is centered entirely on possessing an asymmetric flow of data before anyone else can access it. In an era dominated by instant digital communication, this setup is exceptionally rare for the average investor and can typically only be exploited if you maintain a constant, structural line of insider communication. Data is king. I do not operate in this arena. It is the playground of corporate insiders or political figures – like Nancy Pelosi or the gentlemen referred to in the article below – who leverage unique relationships to feed on actionable corporate data before it ever hits a public screen. While it offers a definitive advantage, it relies on an external pipeline of non-public knowledge rather than superior cognitive processing, making it a high-stakes setup that remains entirely out of reach for most unconstrained market participants who play strictly by the rules.

Technical Edge

A technical edge materializes when structural mechanics force market participants to liquidate assets for reasons completely divorced from intrinsic business value. This is an entirely situational setup driven by rigid institutional mandates, legal rules, fund liquidations, or urgent corporate financing needs.

Think of a massive corporate spin-off – like when Pfizer spun out Zoetis in 2013 – where certain funds receive shares of a newly independent entity but are legally barred from holding stocks without a long listing history or a specific market cap floor. The fund managers are legally forced to dump the stock automatically, ignoring price and long-term fundamentals altogether. This predictable, mechanical selling creates a beautiful breakdown in pricing, allowing unconstrained investors with sufficient patience to step in and capture institutional bargains at a massive discount.

Joel Greenblatt discussed these kinds of setups extensively in his book titled “You Can Be a Stock Market Genius: Uncover the Secret Hiding Places of Stock Market Profits.“

This is a concept Michael Mauboussin integrated into the literature a few years back, and it is a dynamic you can see play out across different asset classes. In real estate, for instance, a forced sale is an involuntary transaction where a property is sold to satisfy debts or resolve legal disputes. Driven by legal orders rather than economic choice, these sales (think of foreclosures or partition actions) often result in selling prices below market value.

Why “Time” May Be the Only Durable Arbitrage Left

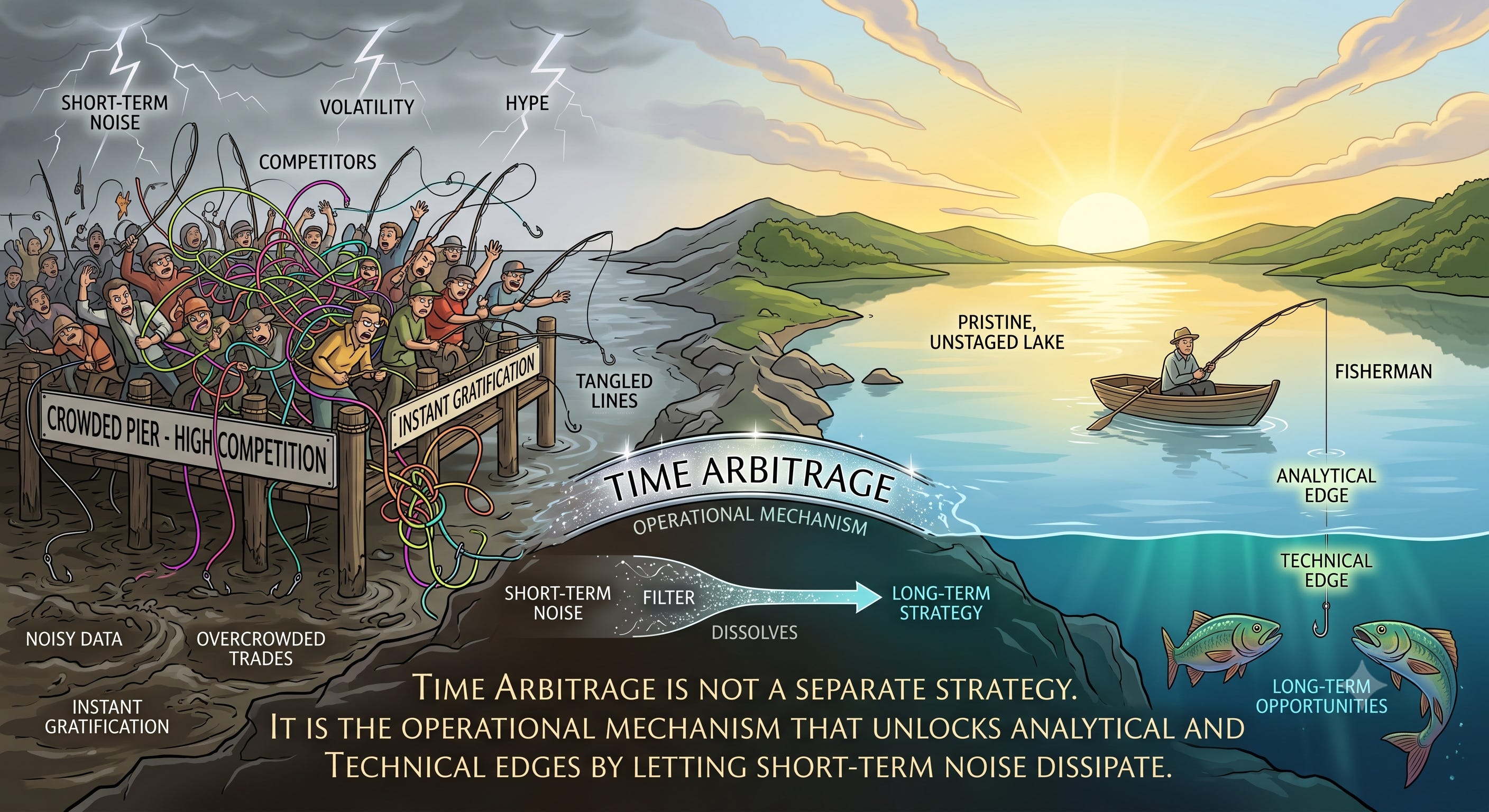

Time arbitrage represents the ultimate external setup. The modern financial ecosystem is systematically, structurally incapable of playing a long game. The short-term arena is a bloodbath of hyper-concentrated talent. Just like that crowded poker table where world-class players trade blows over minuscule advantages, Wall Street pours trillions of dollars and infinite intellectual capital into predicting the next quarter’s earnings or the next Federal Reserve announcement. The participants are extraordinarily skilled.

But when you purposefully extend your investment time horizon, you choose to step away from that hyper-competitive table entirely.

William Browne summarized this reality cleanly: the longer you can extend your time horizon, the less competitive the game becomes.

"The longer you can extend your time horizon, the less competitive the game becomes." – William Browne

This systemic inefficiency persists not because professional investors lack brilliance, but because they lack structural freedom (a technical setup). The entire institutional asset management apparatus is tightly shackled to twelve-month evaluation cycles, tracking errors, and quarterly benchmarks. If a portfolio manager underperforms for two consecutive quarters, clients pull capital, fees dry up, and careers end. Consequently, high portfolio turnover becomes a career survival mechanism rather than an alpha-generation strategy.

“Given the competitiveness of the investment business, we believe it is important in every investment to have an edge, an advantage over the herd. This edge could be a willingness to take a long-term perspective in a short-term-orientated market, a tolerance of complexity when others crave simplicity, or the absence of constraints which either impede the ability of others to act or force them to act in uneconomic ways.” - Seth Klarman

While institutional constraints provide the technical backdrop for this phenomenon, I am convinced that a severe analytical blind spot plays an equally devastating role here. The mathematical reality is that very few investors truly comprehend the non-linear nature of sustained compounding at high, double-digit rates. Our minds are naturally optimized for linear progression – which makes the exponential trajectory of an exceptional business compounding over a decade feel completely counterintuitive. It requires a rare level of cognitive imagination to map out the long-term future trajectories of high-quality, young companies that possess the runway to compound at these speeds. Because the typical analyst spreadsheet truncates abruptly at year three or five, or maaaaybe at year ten, the market systematically fails to price the massive terminal value of these compounding machines. You see peers obsessing over next quarter's margin compression while remaining completely blind to the structural macro-tailwind and resulting trajectory of the business model. This collective lack of imagination ensures that the long end of the equity curve remains mispriced, leaving it wide open for those who can look past the immediate horizon.

Horizon Kinetics explored this market-wide disinterest in long-dated returns, noting that the institutional market systematically and heavily discounts outcomes that lie three to five years into the future. Nick Sleep observed this identical structural flaw during his tenure at the Nomad Investment Partnership, noting that the ever-shortening timeframes adopted by institutional investors mean that longer-term opportunities are typically foregone. Wall Street has willingly abandoned the long end of the curve.

To formalize how this structural vacuum relates to our core success formula, we can look at Richard Grinold’s Fundamental Law of Active Management, …

… which posits that investment success is a product of internal skill multiplied by opportunity.

Success = Skill (+ Luck) x Edge (BAIT)

As an aside, I liked the way the paper begins as it provides some good food for thought on the concept of skill:

“Suppose you could start a new investment management firm. How would you do it? Imagine that your choices even include determining your own skills not so much the level of skill, but that you can choose the “what,” as in “skill at what.” You could be an aggressive stock picker, a growth stock manager, a value-oriented manager, a rotating or cyclical manager, a quantitative manager, an economic sector manager, an index fund manager, or an ex-tended/enhanced index fund manager, to mention just a few possibilities. Which style would you choose?

This paper tries to give some guidance to help you make those decisions. With a little reading between the lines, you can see how these insights might apply to your own investment management operations and allow you to exploit your own particular insights into the market.“ - the first few lines of the paper

If the short-term market is completely flooded with exceptional analytical skill, the net alpha generated there inevitably compresses to zero. The paradox of skill reigns supreme.

If the long-term horizon is completely starved of competition, even a moderate level of technical proficiency paired with a long duration can achieve outsized results.

Time arbitrage is not a separate strategy. It is the operational mechanism that unlocks analytical and technical edges by letting short-term noise dissipate. Think of it as a fisherman finding a pristine, completely unfished lake while your competitors are all tangled up in each other’s lines at a crowded pier.

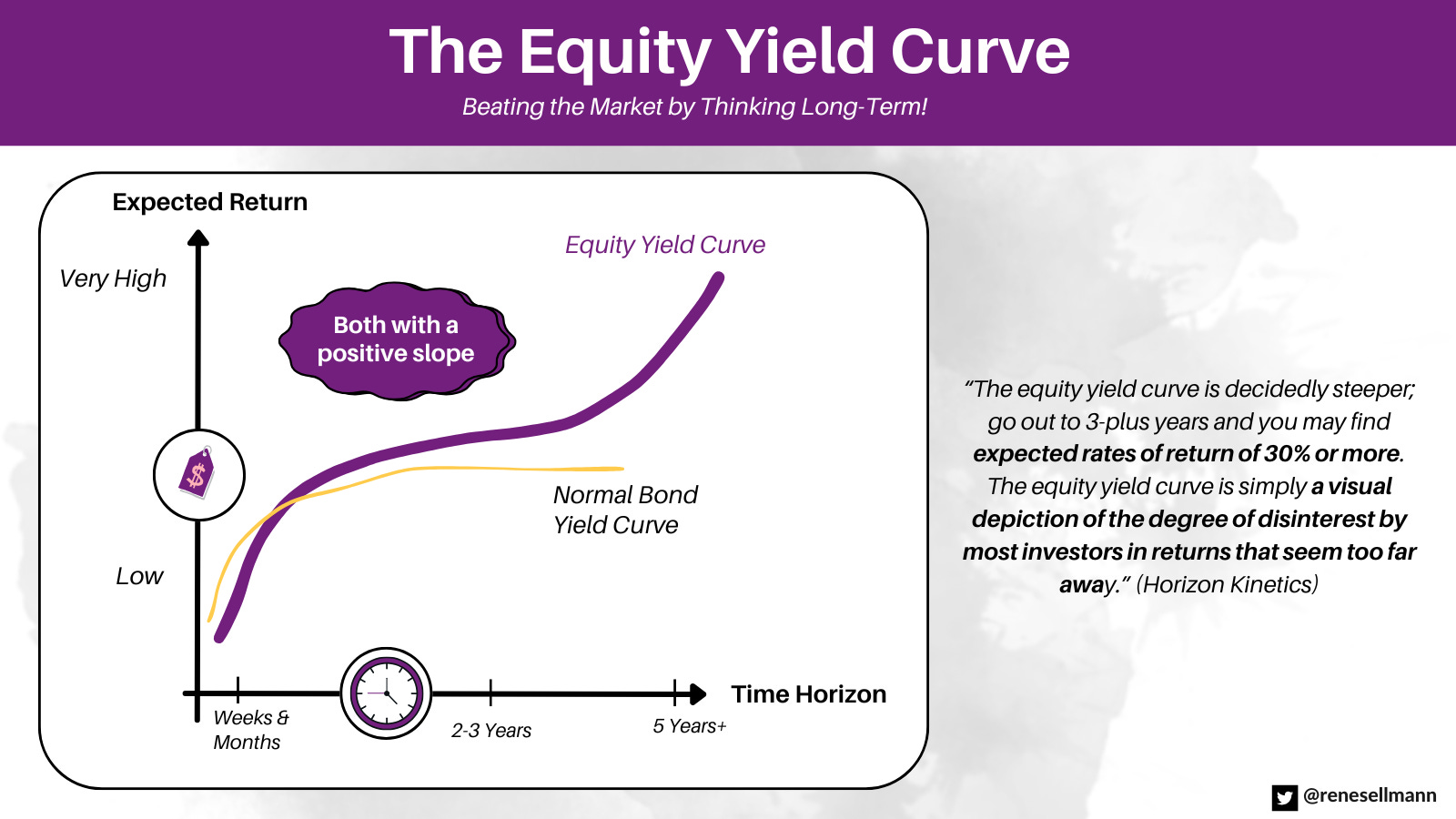

This dynamic creates a highly predictable topography of return across time. At the front end – spanning weeks and months – the market operates with immense efficiency because high-frequency algorithms, hedge funds, and quant strategies dominate the space. Visibility is clear, and the competition is cutthroat. As you push out to the one-to-three-year mark, catalysts begin to emerge, and sentiment starts to mean-revert. The true structural pricing breakdown happens at the deep end, past the five-year mark. Here, long-term compounding and structural business fundamentals dictate the ultimate outcome, yet almost no one is playing the game. The visual above conceptualizes this as an S-curve, where expected rates of return can skyrocket simply because institutional investors refuse to assume long-term time risk.

Moreover, you must realize that time arbitrage is never free. It carries a brutal psychological toll. John Huber articulated this cost perfectly, writing that the price of gaining this specific edge is the volatility that could occur in the near term. You have to be completely willing to accept the possibility that your stock will go down A LOT before it goes up – even though you should attempt to do everything in your power to time your entry well, of course.

Yet, you will not always be able to get your timing right, and this is precisely why the edge remains so remarkably durable. Wall Street analysts often cannot experience stomach-churning drawdowns. They cannot handle the career risk. They cannot look their clients in the eye and defend a position that is down 30% over a twelve-month stretch, even if the ten-year compounding thesis is ironclad. Their structural constraints prevent them from paying the price of admission.

Ultimately, time arbitrage bridges the entire chasm between internal skill and external edge. Your internal skills – your patience, your emotional discipline, your mastery of reverse DCF modeling, etc., etc., – are the tools you use to survive the journey. The structural short-termism of the institutional market is the external setup that hand-delivers the opportunity occasionally.

In an investing ecosystem that is moving faster every single day, trying to out-trade or out-analyze your competitors on a quarterly horizon is a fool’s errand. You are simply choosing to sit at the hardest poker table in the room.

The only way to win consistently is to change the parameters of the game entirely. Extend your gaze. Embrace the near-term volatility. In a world completely obsessed with the immediate present, a long time horizon is not just a patient virtue. It is potentially the last remaining structural edge.

Final Thoughts

Applying this framework to the current market environment requires immense discipline. Right now, the broader market is giddy, euphoric, and blindingly greedy. When everyone is chasing the exact same momentum, true behavioral edges in terms of buying opportunities vanish completely – even though they may very well present a behavioral opportunity to exploit when it comes to liquidating positions.

Remember that you cannot manufacture an external setup out of thin air, regardless of your proficiency. If no one told you that a geopolitical crisis was about to disrupt energy markets, you could not make money trading oil stocks.

Recommended reading: