The Analytical Edge Was Dead. AI Might Be Bringing It Back.

Buffett's Vanished Edge, and the Strange Way AI May Return It

You can read this article entirely for free. If you find value in this research, consider becoming a Premium Member for less than $1/day to unlock our full archive and join our growing circle of investors (I highly recommend checking out “The Library” to see what’s inside; you can find it right on the homepage).

Why join the community, you may ask? Our library is fast approaching 70 comprehensive deep dives, providing institutional-level research on some of the world’s most fascinating businesses. Most recently, we’ve dissected companies like Mercado Libre ($MELI), Grab Holdings ($GRAB), Fair Isaac ($FICO), and Topicus.com ($TOI).

As a member, you get:

Complete Access: Every deep dive in our library (65+ and counting).

More Content: Company updates; powerful valuation spreadsheets, frameworks, and processes; regular portfolio updates (insights into my investing decisions); market commentary; etc.

The WhatsApp Community: Real-time discussion and networking with like-minded investors.

Digital Investing Conferences: About three times a year, we also hold digital conferences where members present and share stock ideas, and discuss broader themes, and we’d love for you to join in!

Incredible Value: Full access to all of this for less than $1/day.

If you want to see the level of research we provide before committing, the following deep dives are, for instance, free to read (access them via The Library):

InPost ($INPST) - generated an IRR of >400% as an acquisition offer emerged 2-3 months post-write-up

DigitalOcean ($DOCN) - up 5x in less than a year post write-up release

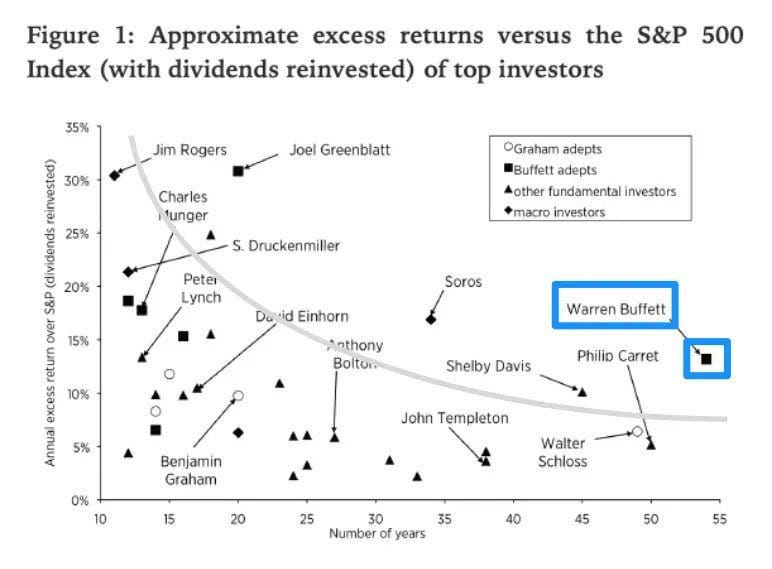

Warren Buffett compounded capital at roughly 20% a year for more than six decades.

Sit with that number for a moment, because almost nothing in the history of markets rivals it. Buffett is an absolute outlier in the chart below.

Part of the explanation is temperament, part is structure, part is the simple arithmetic of a very long runway.

Buffett’s edge was real!

But a meaningful slice of it, especially in the early partnership years, came from something we’d now call an analytical edge. He read the Moody’s manuals nobody else bothered to open. He found the net-nets, the obscure insurance floats, the mispriced stubs that were sitting in plain sight because the work of finding them was tedious, and the audience for that work was small.

"[Warren] expends a lot of energy checking out details and ferreting out nuggets of information, way beyond the balance sheet. He would go back and look at the company's history in depth for decades. He used to pay people to attend shareholder meetings and ask questions for him. He checked out the personal lives of people who ran companies he invested in. He wanted to know about their financial status, their personal habits, what motivated them. He behaves like an investigative journalist. All this stuff about flipping through Moody's Manual's picking stocks, it was a screen for him, but he didn't stop there." Alice Schroeder

That world is gone.

You know this already. Investing has been democratized. Every 10-K is a click away. Every transcript is transcribed, indexed, and searchable within minutes of the call ending. Calls are available in podcast-like apps. Screeners that would have been science fiction in 1965 are free inside your brokerage account. The manuals Buffett had to physically hunt down now arrive pre-digested. Investors share their processes freely online.

And so the intuition almost everyone holds, seasoned investors included, is that the analytical edge has been arbitraged down to something close to zero. The skill ceiling rose so high, and access became so universal, that being smart and diligent stopped being enough. Everyone is smart now. Everyone is diligent.

Then AI arrived, and the intuition hardened into something like certainty.

If the internet flattened the information advantage, generative models look poised to flatten the analytical one. A tool that can read a 300-page filing in seconds, build a discounted cash flow model on request, and summarize the bear case before you’ve finished your coffee would seem to be the final erasure of any thinking advantage a human might once have held. The machine does in ten seconds what took a diligent analyst a week.

Where’s your edge now?

Anne Lundgaard Hansen and Seung Jung Leea thus propose that widespread AI adoption may lead to more efficient markets as bubbles driven by human behavior become less likely.

I want to propose the opposite.

Not as a settled conclusion, because I haven’t arrived at one, but as a hypothesis I think is badly underdiscussed.

The widespread, homogenizing adoption of AI in analysis may not bury the analytical edge. It may be digging it back up. It may not lower volatility, but increase it. It may not lead to less herding, but more crowded trades.

“… when teams simultaneously consult homogeneous AI systems, they unknowingly undergo a process we term Invisible Groupthink. Invisible Groupthink is an AI-mediated conformity that operates without the social pressure or directive leadership that classical groupthink requires, and which is therefore structurally invisible to the organizational safeguards designed to prevent it.“ - Invisible Groupthink: AI Homogenization, Epistemic Diversity, and Organizational Decision Resilience

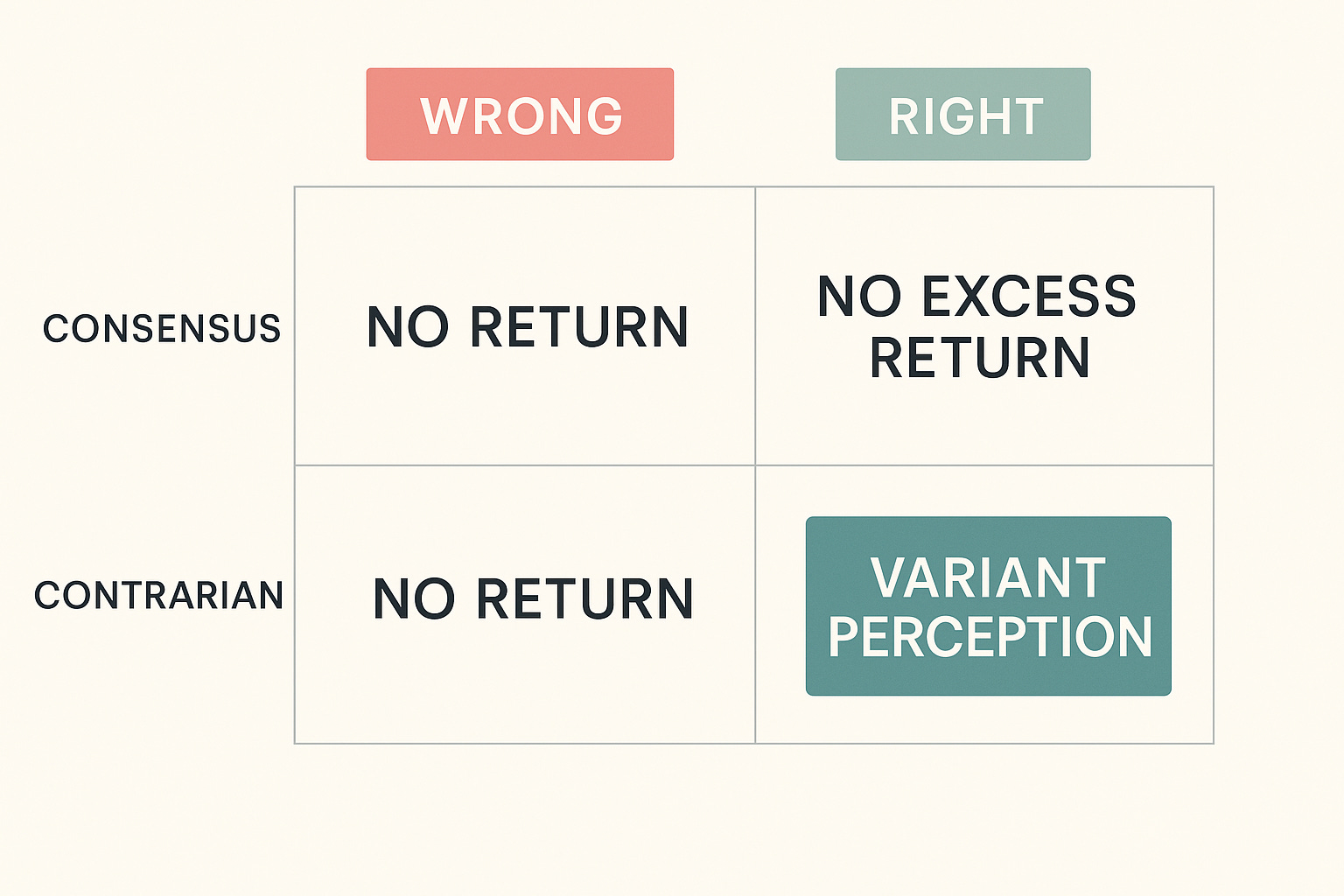

A quick word on what an edge actually is …

I’ve written at length in a recent post about the distinction between skill and edge, so I won’t rebuild that whole argument here. You can read that piece here:

The short version, for anyone who hasn’t read it: you possess skills, but you do not possess an edge. An edge is external. It’s a situational setup, a behavioral inefficiency, or a structural quirk in the market landscape that appears for you to exploit. It’s an event, not a trait. And the uncomfortable corollary is that you cannot out-skill a bad environment. All the analytical horsepower in the world does nothing if there’s no inefficiency for it to act on.

That framing is highly relevant here, because I believe whether AI makes you more skilled isn’t even a question. Obviously, it does. It makes everyone better.

The question is whether AI creates or destroys the external conditions under which skill converts into excess return.

It helps to be precise about the kinds of edges available. Bill Miller framed it cleanly, and Nick Sleep later paraphrased him well: there are broadly three competitive advantages in investing.

Informational, where you know a meaningful fact nobody else does.

Analytical, where you take the same public information everyone has and cut it up to reach a superior conclusion.

And psychological, or behavioral, where you are able to think and act rationally when others cannot.

Sleep added the observation that sustainable advantages tend to come from the analytical and psychological buckets, because pure informational edges are fragile and, in regulated markets, often illegal. There’s a fourth edge worth naming, the technical or structural one (I’ll again point you to the write-up linked above).

The informational edge, for the ordinary investor, is mostly dead. Regulation and the internet saw to that. Which leaves the analytical and the behavioral as the only edges a fundamental investor can realistically build a career on.

And the analytical one is precisely the edge everyone now assumes AI has finished off.

The edge that eroded before anyone typed a prompt

To understand what AI might do, it’s worth being honest about what already happened without it. The analytical edge didn’t wait for large language models to start decaying. It had been thinning for decades.

Think about the sequence. Decimalization narrowed spreads. Regulation FD, back in 2000, killed the selective-disclosure game where a favored analyst got the nod on the quarter before everyone else. EDGAR put every filing online for free. Then came the screeners, the aggregators, the transcript services, the research terminals, and eventually a generation of investors raised on all of it who think of a fully-built reverse DCF as table stakes.

The barrier to competent analysis fell and fell.

Here’s the thing that gets missed, though. When a skill becomes universal, it stops being an edge, but it doesn’t stop being necessary. You still have to do the work. You just no longer get paid for doing it, because so does everyone else.

“Financial firms are contending with the most significant overhaul of technology capabilities in a generation. AI-driven digital transformation is reshaping job roles and investment processes, prompting professionals to reconsider the boundaries between human and machine cognition, while firms work to upgrade their technology stacks and human capital to remain competitive. Amid this shift, firms and professionals must reevaluate the skills needed for success.“ - CFA Institute in “AI in Finance: Changing Workflows, Growing Demand for Human Judgment“

So by the time AI showed up, the patient was already pale. Most thoughtful investors had made a quiet peace with the idea that their durable edge, if they had one at all, was behavioral. Time arbitrage for instance. The willingness to be patient when the institutional world structurally cannot be, to hold through drawdowns that force a fund with quarterly redemptions to sell. To step in the ring when everyone is panicking.

If universal access to information compressed the informational edge, and universal access to analytical tooling compressed the analytical edge, then generative AI looks like the same movie with the resolution turned up. The tool doesn’t just hand you the filing. It reads the filing, cross-references it against eight years of prior filings, flags the change in revenue-recognition language, drafts the model, writes the bear thesis, and stress-tests your bull one.

What took a skilled analyst a focused week now takes an afternoon, and the analyst on the other side of your trade has the same afternoon.

The empirical trend supports the worry. There’s a growing body of research, and a growing chorus on Wall Street, warning that as more investors lean on similar models they converge on the same conclusions. From hedge funds to wealth managers, the industry has embraced AI in search of an edge, and researchers are now asking what happens when everyone turns to similar models to find one: buying the same stocks, reacting to the same headlines, and making the same mistakes. Several recent studies suggest widespread adoption could shorten the lifespan of profitable trading signals as investors converge on the same opportunities. If a signal that once took years to arbitrage away now gets crowded out in months, the shelf life of any analytical insight collapses. You did brilliant work, the model agreed with your brilliant work, and so did every other model, and the opportunity was gone before you could size into it.

That’s the steelman. Faster synthesis, universal tooling, accelerating alpha decay, everyone converging on the same answer at the same time. If you stop the story there, the analytical edge isn’t just dead. AI held the pillow over its face.

But notice the word doing all the work in that paragraph. Converge.

Convergence is not the problem. Convergence is the opening.

Here’s what we were assuming so far: when everyone’s analysis converges, it converges on the truth. That the machine consensus is correct, and being correct alongside everyone else simply means the reward gets competed away.

If that were true, the analytical edge really would be finished, because there’d be nothing left to be right about that the crowd hadn’t already priced.

But that’s not what the research on these models actually shows. It shows convergence, yes. It does not show convergence on truth. It shows convergence on the mean.

This distinction is everything, so let me ground it. When researchers measure the creative and analytical output of large language models, they find something consistent and, for our purposes, remarkable. The models don’t just each produce somewhat generic output. They produce similar generic output to one another.

One study by Emily Wenger and Yoed Kenett administered standard divergent-thinking tests to twenty-two different models from distinct model families alongside a group of human participants, and the models produced dramatically less diverse output than the humans, with effect sizes that in social-science terms are enormous.

“We find that LLM responses mirror other LLM responses far more than humans do other humans, even after controlling for key confounding variables.“

The gap didn’t close when researchers switched models. It’s structural.

Different systems, trained on overlapping data with similar objectives, land on overlapping answers. You cannot escape it by using a different provider, because the homogenization isn’t a quirk of one model. It’s a property of the category.

Why does this happen? Two reasons, both baked in. The models are trained to predict the most probable next token, which, by construction, pulls them toward the statistical center of their training data rather than out to the strange, correct, non-obvious tails where real analytical insight tends to be found. The contrarian, non-consensus view. The variant perception.

“Researchers are now asking what happens when more investors turn to similar AI models to find one: buying the same stocks, reacting to the same headlines, and sometimes making the same mistakes. […] AI may make investors faster and more informed while also making their trades more crowded, their systems easier to fool and their risk-taking harder to control.“ - The Straits Times

And the alignment process that makes them pleasant to use, the reinforcement from human feedback, systematically compresses the variance of what they’ll say.

The output gets smoother, more agreeable, more standardized. It regresses toward consensus by design.

There’s even research showing the effect intensifies when a model has access to your prior conversations and profile, tuning its answers toward what it infers you already believe. The tool is engineered to tell you a well-structured version of what everyone already thinks, and to do it more persuasively the longer it works with you.

Now put that back into a market. If a large and growing share of participants outsources the analytical layer to systems that regress toward the same mean and flatter the user’s existing priors, then the market’s collective analysis doesn’t necessarily get sharper.

It just gets narrower.

The dispersion of views that makes markets efficient in the first place starts to collapse into a monoculture. And a monoculture is not an efficient market. A monoculture is a market that has agreed to stop looking in the same places at the same time.

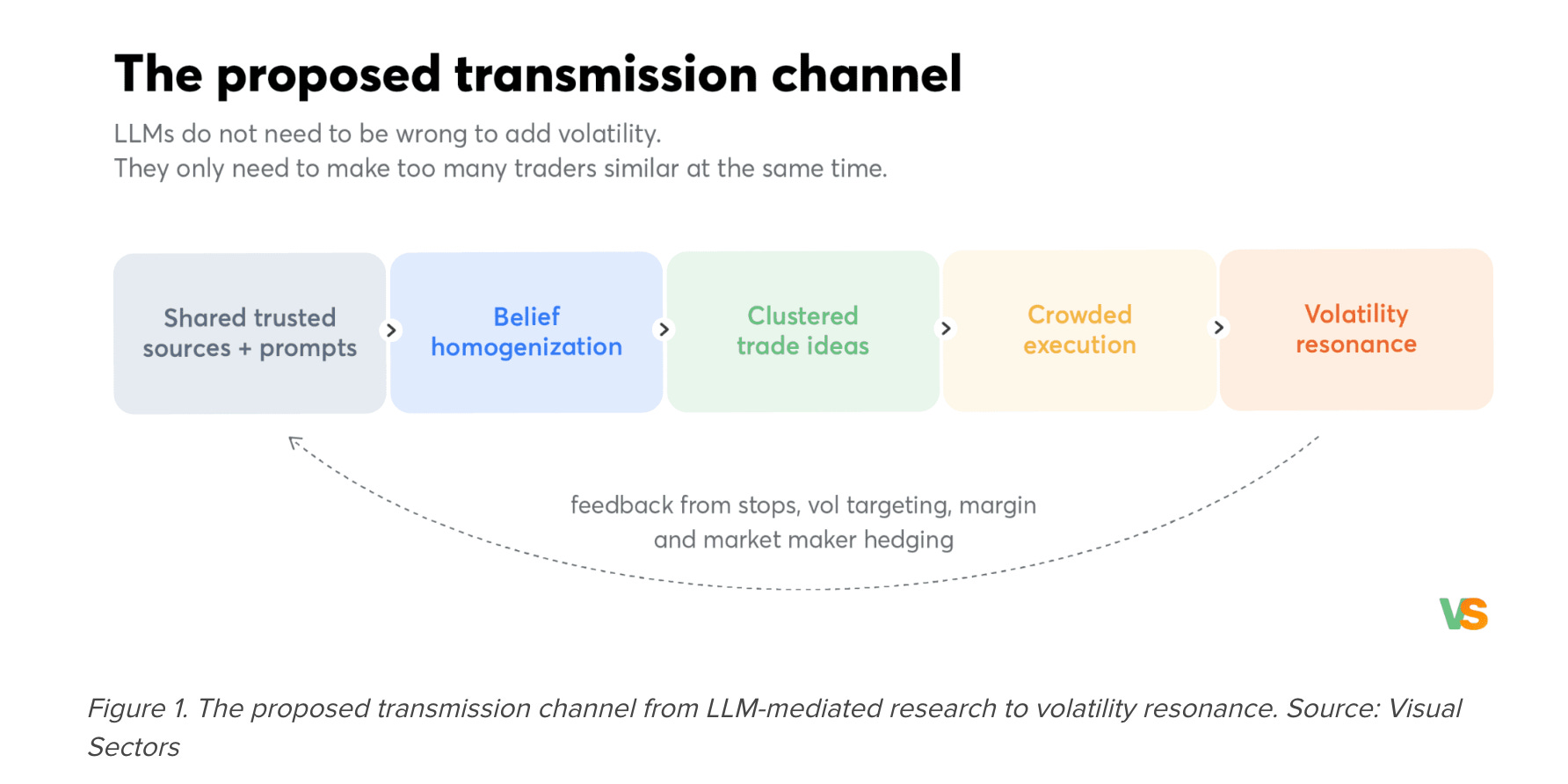

Interactive Brokers visualized the impact of “belief homogenization” beautifully in the illustration below:

Maybe that’s what’s already driving the multi-trillion momentum trades?

So that agreement may create inefficiency? That’s at least a hypothesis to wrestle with I believe. And IBKR does too, and they propose that widespread LLM adoption may also increase volatility, which stock pickers should love:

“A more important risk question is whether they can make a large number of investors interpret the same information in the same way, at the same time. LLMs may become market-relevant not because they create perfect forecasts, but because they compress diverse research processes into similar narratives, rankings, watchlists and execution plans.“ - Can LLM-Based Trading Systems Increase Market Volatility?

That may be the edge, sitting right where the crowd stopped looking.

I’m not alone in reading it this way, which I’ll admit, surprised me when I went looking. The CFA Institute, not exactly a contrarian fringe outlet, published an analysis titled “The Perils of Declining Judgment in the Age of AI“ arguing that as AI-generated research proliferates, consensus forms faster, and that algorithmic systems tend to reinforce dominant paradigms and raise the risk of intellectual stagnation.

“Artificial intelligence (AI) now introduces a paradox. While machines significantly expand our capacity to process information, excessive reliance on automated cognition may erode the epistemic foundations that enabled civilizational progress. […]

Humans are passively consuming AI-generated outputs rather than actively engaging with data. The consequences have become evident in a decline in critical thinking and decision-making skills, or cognitive laziness (Cheng, 2025; Chatterji, 2025; and others). Left unchecked, reliance on automation risks compromising the quality of investment decisions. The question is not whether machines will become more powerful, but whether human decision-making will remain grounded in evidence.“

Their conclusion is almost word for word the hypothesis I’m circling: widespread AI adoption elevates the value of independent judgment and process diversity precisely by making both increasingly scarce.

“Widespread adoption of generative AI in investment management risks diminishing critical thinking, eroding human expertise, reducing innovation, and concentrating decision-making power in AI models, potentially leading to systemic vulnerabilities, poor adaptability, and ethical concerns.“

When the marginal cost of generating consensus analysis falls to nearly zero, the thing that becomes valuable is the analysis that consensus can’t produce. Scarcity moved. It used to be scarce to do the analysis at all. Now it’s scarce to do analysis that departs from the machine.

So the analytical edge doesn’t return in its old form. You don’t win anymore by being the diligent one who read the filing, because the model read the filing too, and so did everyone else’s model.

You win, if you win, by being the one who reads the filing and then thinks something the model structurally cannot think.

The judgment that sits in the tails. The non-conforming question. The read on a management team, a regime shift, or a second-order consequence that doesn’t sit anywhere in the training distribution because it hasn’t happened yet.

So what does a reclaimed edge actually look like?

Suppose I’m right. Suppose the machine consensus is narrow, confident, and increasingly universal, and suppose that narrowness reopens a door that had been closing for thirty years. What do you actually do with that?

The first thing to understand is what the edge is not. It is not out-computing the machine. You will lose that race, badly, and so will everyone else. The model reads faster, models faster, and never gets tired. If your process is to do by hand what the AI does automatically, you don’t have an edge, you have a slower version of the commodity.

The reclaimed analytical edge can be found downstream of the machine’s output. It begins where the consensus ends.

Practically, that means using the tool to find the consensus rather than to form your own view. Ask the model for the bull case, the bear case, the standard framing, the obvious risks. Not because you’ll adopt them. Because now you know, with real precision, what everyone else who queried a similar model is looking at.

That’s the map of crowded ground. Your job is to work out where the map is wrong. Where does the training distribution fail? Usually in the places the data can’t reach: a genuine regime change with no historical analog, a management team whose behavior you can only judge by having sat across from them, a second-order consequence that hasn’t happened yet and so exists in no corpus.

The model regresses to the mean of what has been written. Your edge is the well-founded view about what hasn’t.

This is roughly the “AI plus human” paradigm the CFA Institute has been circling, though I’d put it more sharply than they do.

“As we’ve noted elsewhere, we believe the future will be defined by the complementary cognitive capabilities of humans and machines, characterized by the “AI + HI” paradigm and the continued importance of professional competence.” - Rhodri Preece in AI in Finance: Changing Workflows, Growing Demand for Human Judgment”

The benefits of AI don’t accrue to individuals, they accrue to processes, which is precisely why the individual edge has to come from somewhere the process can’t reach. When earnings-call analysis and filing review get automated, the repeatable, auditable parts of the job become table stakes. What’s left, the scarce thing, is judgment. Human judgment. The willingness to hold a differentiated view and be wrong in public for a while before you’re right for instance.

Which brings me to the part I find least comfortable, and the reason I’m holding this as a hypothesis rather than a thesis. A reclaimed analytical edge is brutally hard to hold. It was hard when it belonged to Buffett reading manuals, and it’s harder now, because holding a view the machine disagrees with means holding a view almost everyone disagrees with, generated confidently, phrased persuasively, and repeated everywhere you look.

The homogenization that creates the opportunity also creates enormous pressure to abandon it.

When every screen, every note, every colleague’s model says the same thing, the contrarian has a particularly tough time.

And a good deal of the time, the contrarian may in fact be wrong, because being different is not the same as being right. That distinction is the whole game, and AI does nothing to make it easier.

So the analytical edge and the behavioral edge may be collapsing into a single thing. The analytical work identifies where the consensus is mechanically narrow. The behavioral discipline is what lets you stand there once you’ve found it.

You need both. You always did.

What’s changed is that the machine may now manufacture the consensus faster and more uniformly than any prior technology, which sharpens the opportunity and, in the same motion, sharpens the discomfort of taking it.

I’ll leave you where I started, which is without a firm conclusion. Maybe AI finishes off the analytical edge for good, and everything I’ve laid out is a rationalization for staying in a game that’s already over.

Or maybe the great homogenizing wave washes out the middle, floods the market with confident, average, identical analysis, and quietly restores a premium to the one thing it cannot produce: An independent mind, willing to look where the machine won’t, and to stay there.

I’d love to hear what you think.