Earnings Review: Monday.com ($MNDY)

Big 37% Selloff – When Strong Results Meet Harsh Market Reality

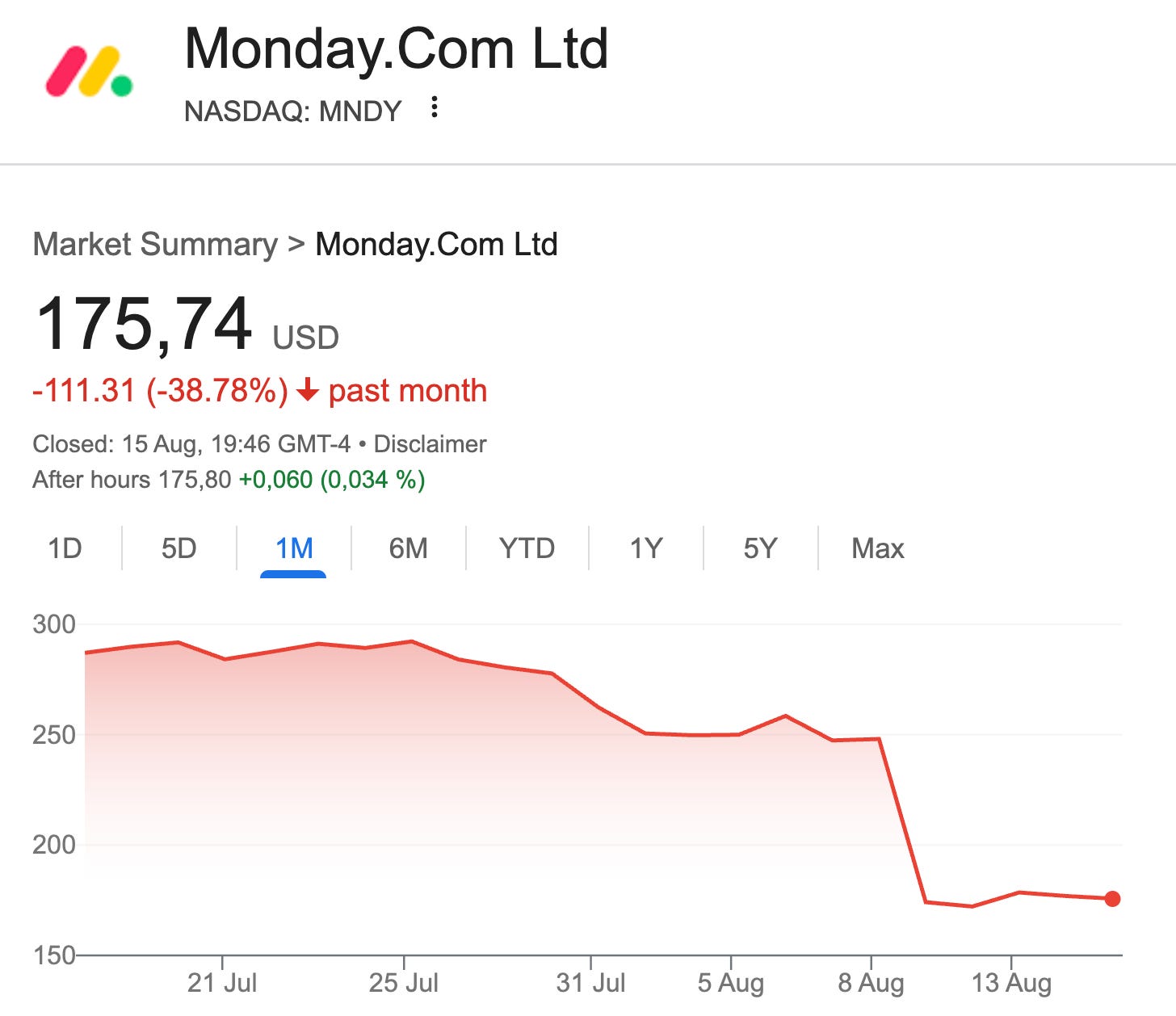

It’s not often you see a company deliver exactly what investors had been asking for – strong growth, expanding profitability, healthy cash flow – and then watch its stock price collapse by nearly a third in a single day and 38% over the last four weeks.

But that’s precisely what happened with Monday.com ($MNDY) after releasing its Q2 2025 results.

The contradiction is striking. On the surface, the quarter looked like another step forward in Monday’s journey from scrappy Israel-based SaaS upstart to durable platform business. Dig a little deeper, though, and you begin to see the web of factors – shifting sentiment in software, AI disruption fears, cautious guidance, and perhaps simple market mechanics – that help explain why investors hit the sell button so aggressively.

That gap between business performance and stock reaction is where things get interesting. Is this an early sign that something in the story is breaking? Or is it simply a case of sentiment washing out, setting up a more attractive entry point for long-term investors willing to stomach volatility?

I don’t think the answer is straightforward. But mapping the terrain is essential if you’re going to make sense of what Monday is today versus what it might become tomorrow.

Here’s how I’ll break it down:

Quick Results Recap – Monday’s latest earnings in plain English.

Operational Check-In – How the company is performing beneath the headline numbers.

What’s (Likely) Driving This Selloff – Why the stock collapsed despite strong fundamentals

Updated Valuation – A fresh look at Monday’s valuation after the 38% decline

Conclusion – Where I stand now

For me, the real value of revisiting Monday now isn’t just about deciding whether the stock is a buy, sell, or hold. It’s about sharpening my understanding of how quality businesses can still trade like battleground stocks, why multiples compress even when numbers improve, and what “margin of safety” actually means in a sector that swings between euphoria and despair.

Before we dive back in, a quick note…

If you’re reading this as a free subscriber and finding value in this kind of deep, idea-by-idea analysis, consider upgrading to the full version. I write these posts for long-term thinkers who want more than earnings call recaps and press-release summaries. If that’s you, I’d love to have you on board.

Read my Monday.com deep dive here (no paywall):

Monday.com: A Quiet Powerhouse in a Crowded SaaS World

When Monday.com went public in 2021, many investors dismissed it as just another project management tool competing with the likes of Asana, Smartsheet, and Trello. In a sector flooded with flashy SaaS IPOs, it was easy to overlook a company that presented itself not with bold visions of "changing the world," but with a rather modest mission: making work…

Disclaimer: The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

Monday’s Q2 Results: What the Quarter Really Tells Us

Whenever a stock moves as violently as Monday.com’s has, the first instinct should be to check whether the underlying business results justify the shift.

In this case, the numbers and commentary from the second quarter tell a story that looks very different from the share price chart. Growth remains strong, cash generation is solid, and management is leaning even harder into product expansion – especially through AI.

To make sense of it all, I’ll first walk through the quarter’s results, then turn to what management had to say about strategy, before finally zooming in on the company’s AI push and what it means for the investment case.

The Quarter in Numbers: Momentum and Mixed Signals

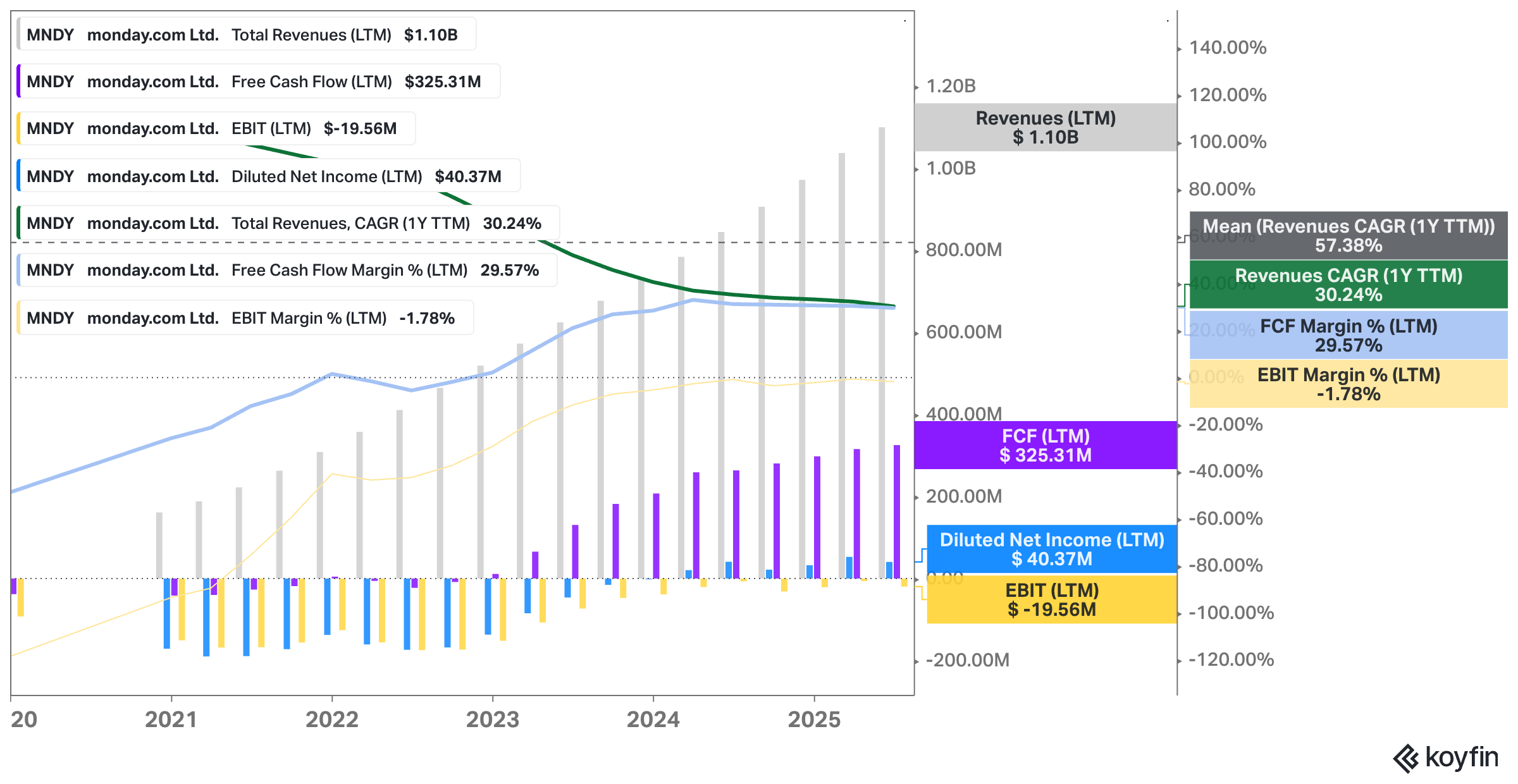

Monday.com’s second quarter of 2025 showed once again that this is a company still very much in growth mode. Revenue came in at $299 million in Q2, up 27% year-over-year – a figure that’s impressive in its own right, especially against a tough macro backdrop where many software peers are struggling to maintain double-digit growth.

But what’s striking isn’t just the topline growth, but the quality of it. Expansion within the enterprise segment continues to accelerate, with record additions of customers spending more than $100,000 annually. That figure now stands at 1,472, a 46% increase from last year. On top of that, the company’s mid-market and larger customers remain highly engaged, as reflected in a 117% net dollar retention rate in the $100k+ cohort. Highly impressive!

Profitability tells a more nuanced story. On a GAAP basis, the company posted an $11.6 million operating loss. This sounds concerning at first glance, but the headline is more a reflection of continued investment in R&D and go-to-market efforts. Stripping out stock-based compensation and other adjustments, non-GAAP operating income rises to $45 million, a 15% margin. Free cash flow remained robust: $64 million of adjusted FCF for the quarter, translating to a 21% margin.

Speaking of the balance sheet, Monday.com’s liquidity position is formidable. The company ended the quarter with nearly $1.6 billion in cash and equivalents, giving it both a safety net and the firepower to keep investing aggressively into product development and growth initiatives without raising external capital. This is particularly relevant given the competitive dynamics in software and the capital intensity of building new AI-driven features.

Operationally, there were several milestones worth noting beyond the raw numbers. Monday CRM, a product launched only three years ago, has already surpassed $100 million in annual recurring revenue – a remarkable ramp that signals strong cross-sell potential and the ability of Monday.com to move beyond its flagship Work Management product. Again: HIGHLY impressive!

The company also announced three new AI-powered capabilities – monday magic, monday vibe, and monday sidekick – which I’ll dig into more in a subpart below. Combined, these moves underscore the company’s push from being a workflow tool toward becoming a broader execution platform.

With over 61,000 paying customers using the platform across teams of ten or more, the expansion opportunity remains vast, but execution here is critical.

Finally, guidance for the next quarter calls for $311–313 million in revenue, representing 24–25% growth, and non-GAAP operating income of $34–36 million. For the full year, management expects $1.22 billion in revenue and roughly $320 million in adjusted free cash flow, a 26–27% margin. That guidance paints the picture of a company balancing growth and profitability, albeit with a clear willingness to sacrifice near-term GAAP margins in order to invest in AI and product breadth.

The full story starts here:

The rest of this post covers the content outlined in the table of contents above. If you’re serious about learning more about Monday.com and about sharpening your investing edge, the full post (and all my previous premium content, including valuation spreadsheets, deep dives (e.g. LVMH, Edenred, Digital Ocean, or Ashtead Technologies), and powerful investing frameworks) is just a click away. Upgrade your subscription, support my work, and keep learning.

PS: Using the app on iOS? Apple doesn’t allow in-app subscriptions without a big fee. To keep things fair and pay a lower subscription price, I recommend just heading to the site in your browser (desktop or mobile) to subscribe.