Below you find my July reading (and listening) list: a handful of recent finds that offer valuable context on market trends and the frameworks driving them.

Subscribe below to not miss these kinds of posts in the future.

Articles:

REQ Capital 2026 Half Year Investment Report (especially interesting to those into serial acquirers)

Yale Review: The dangerous unknowns at the heart of LLMs by Melanie Mitchell

“We humans, like most other biological intelligences, are active seekers of information, not passive predictors of next tokens.“

“There are (at least) two problems with such predictions. The first is that they are based on AI performance on benchmarks, which, as we’ve seen, has a poor record of predicting success in the real world. The second is that AI is tested on “tasks,” such as classifying medical images, writing computer code according to given specifications, or generating ad copy for real estate listings. But human jobs are not simply collections of independent fixed tasks; most jobs require the jobholder to understand how different tasks relate to one another, to adapt to change on the fly, and, more generally, to be flexible based on the open-ended nature of the real world.“

Community member Ruki shared the above article in response to my blog piece on the potential return of the analytical edge (“The Analytical Edge Was Dead. AI Might Be Bringing It Back.“)

“There have been market structure changes […] which are resulting in stocks trading differently to how they have historically. More specifically, a shrinking portion of the market is pricing stocks based on long-term fundamentals. The rise of multi-manager firms (a.k.a. pods), retail investors, systemic investment strategies, and passive flows has changed the way that some parts of the stock market trade, and our belief is that we won’t see a return to the way markets previously used to function.“

“The Artificial Intelligence (AI) trade continued apace in the quarter, both through continued fulsome valuations for anything associated with AI and the accompanying buildout on the one hand, and ongoing concerns of AI disruption across various industries on the other. One example in our portfolio is Colliers International, which has seen close to a 50% share price decline after hitting an all-time high last fall. Since we believe the AI concerns relating to Colliers are misplaced, we have increased our position such that it is now a top five weighting.“

“There is of course a lot of negativity on the sector, as investors fear it will be disrupted by AI, leaving terminal value in doubt. Most investors have put software into the “too hard” pile, and some are actively short (most of our software holdings have double-digit short interest as a percentage of float). Amidst widespread selling, we think nuance is being missed. Some software will be disrupted by AI; others will be largely fine and continue as is (defensive thesis); and some will be big beneficiaries (offensive thesis).“

“SaaS is an amazing business model, which makes us reluctant to give up on the category entirely without deeper analysis.“

Discl: I still own Up Fintech

Podcasts & Videos:

A new Pat Dorsey interview! “The Nuances of Investing in Moats” – Capital Allocators with Ted Seides

And here’s another one from March on the Morningstar network —> Pat Dorsey: Economic Moats and More

Chris Mayer on the Excess Return podcast

“On this episode of the 100 Year Thinkers, Chris Mayer and Matt Zeigler discuss long-term investing, 100-baggers, AI stocks, SpaceX valuation, founder-led companies, and why the best investments often come with brutal drawdowns. We also cover his new book The Investor’s Odyssey, the danger of letting labels like AI do too much work, how to think about TAM and capital allocation, and why patience may be the biggest edge for investors trying to own great businesses for decades.“

Value After Hours Vacation Edition (discussing Terry Smith’s letter among other things):

Other:

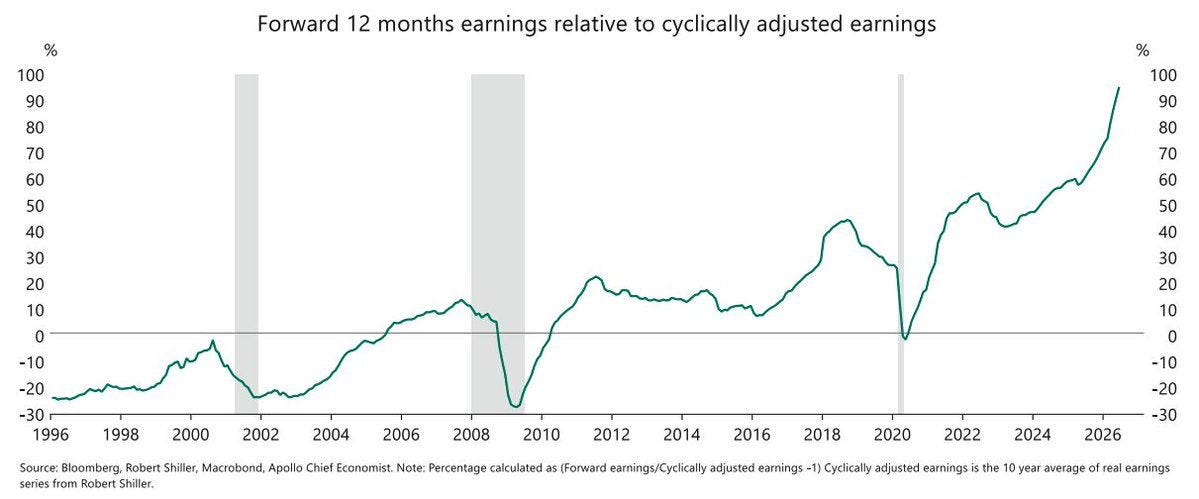

I did my first live stream yesterday and discussed this mind-blowing chart from Robert Shiller on it: