Deep Dive: LVMH ($MC) – Is the Luxury King Losing Its Crown?

Stagnation in Paris: Time to Reassess the LVMH Thesis?

You can read the majority of this article entirely for free. If you find value in this research, consider becoming a Premium Member to unlock our full archive and join our growing circle of investors (I highly recommend checking out “The Libary” to see what’s inside; you can find it right on the homepage).

Why join the community you may ask? Our library is fast approaching 70 comprehensive deep dives, providing institutional-level research on some of the world’s most fascinating businesses. Most recently, we’ve dissected companies like Grab Holdings ($GRAB), Fair Isaac ($FICO), and Topicus.com ($TOI).

As a member, you get:

Complete Access: Every deep dive in our library (65+ and counting).

The WhatsApp Community: Real-time discussion and networking with like-minded investors.

Incredible Value: Full access to all of this for less than $1/day.

If you want to see the level of research we provide before committing, the following deep dives are free to read:

InPost ($INPST)

Monday.com ($MNDY)

DigitalOcean ($DOCN)

Novo Nordisk ($NVO)

Computer Modelling Group ($CMG.TO)

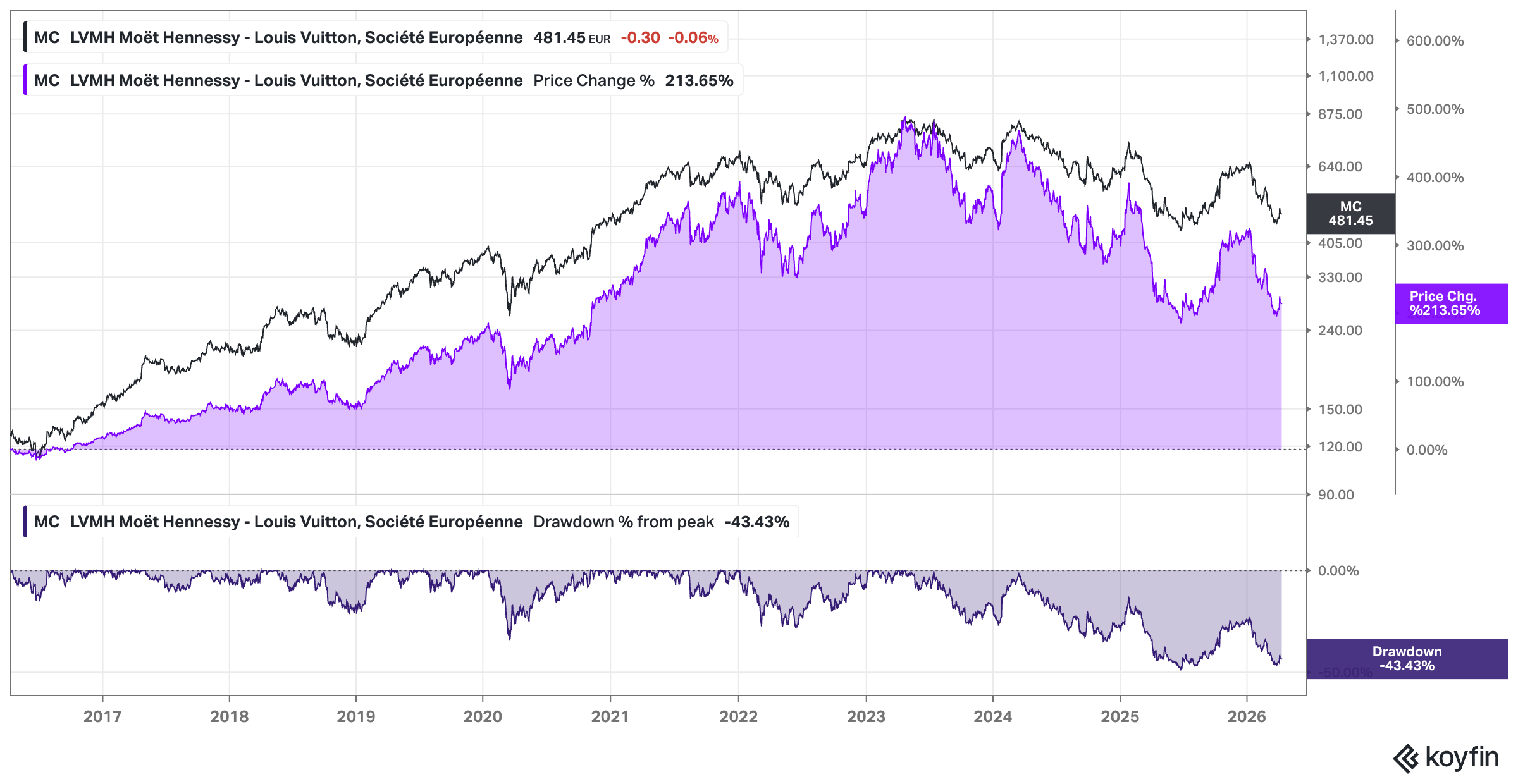

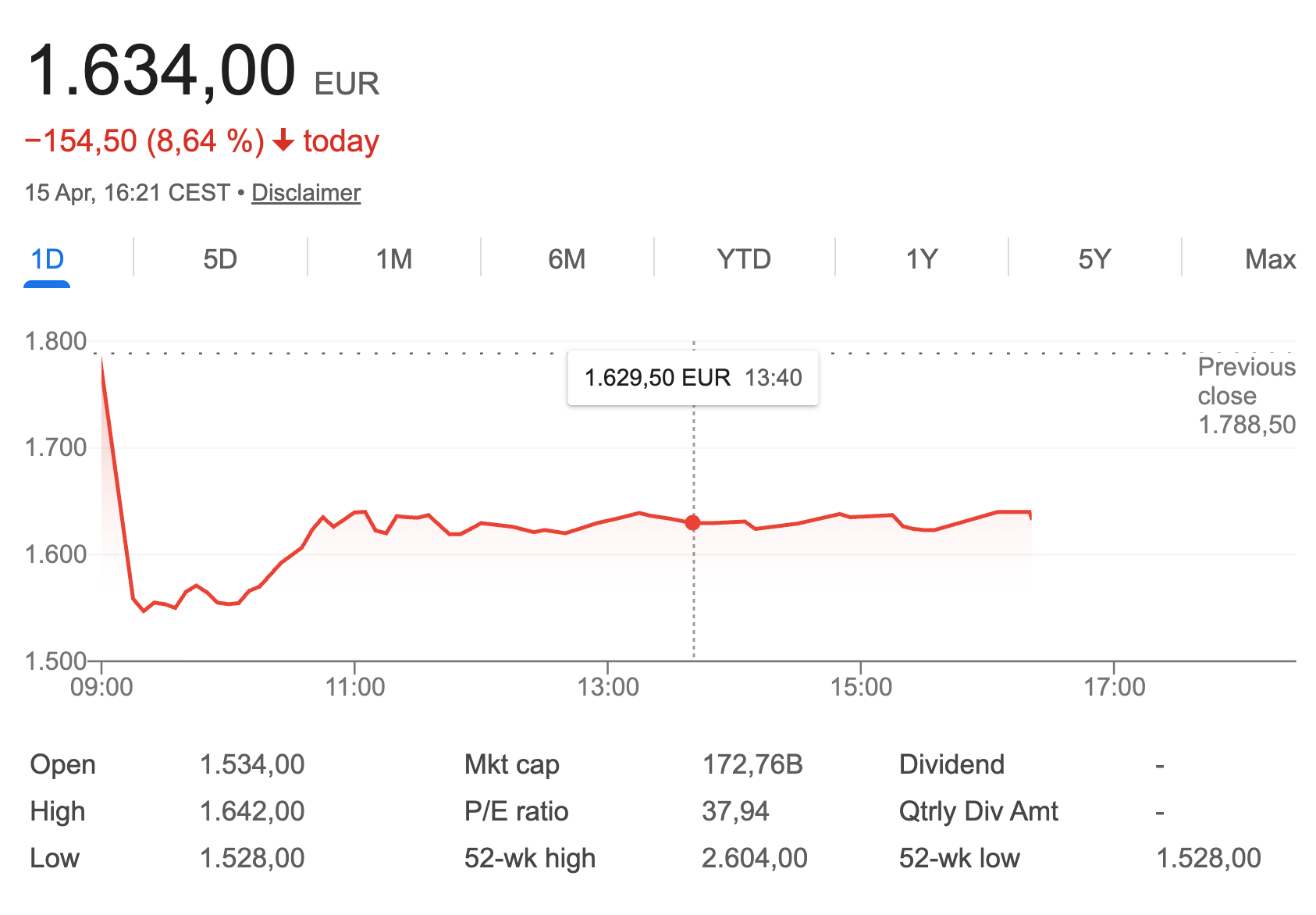

The recent performance of LVMH stock has been a sobering experience for many investors. As you can see from the current price action, the shares have been trending downward for quite some time now and are now hovering near the €480 mark.

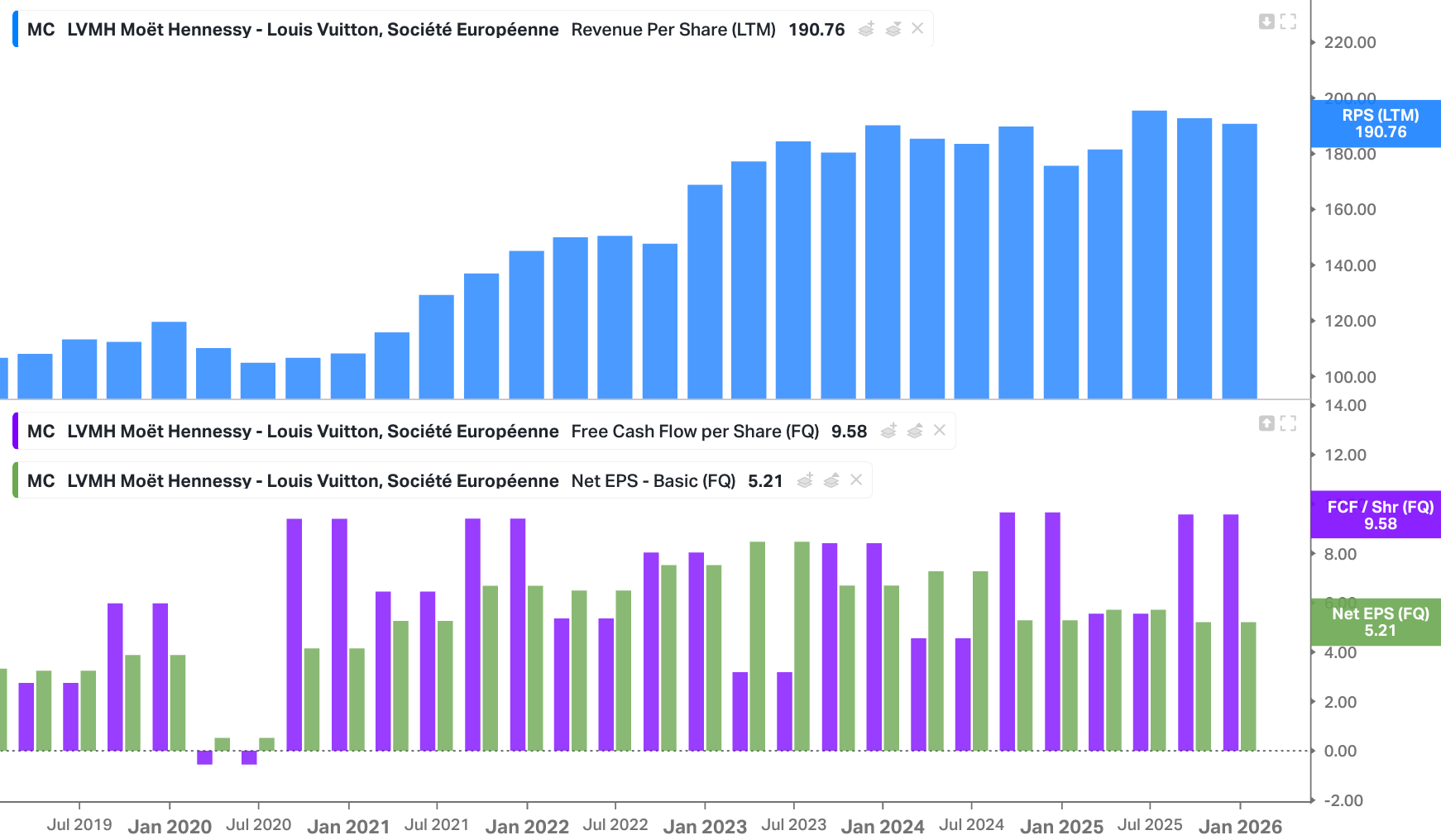

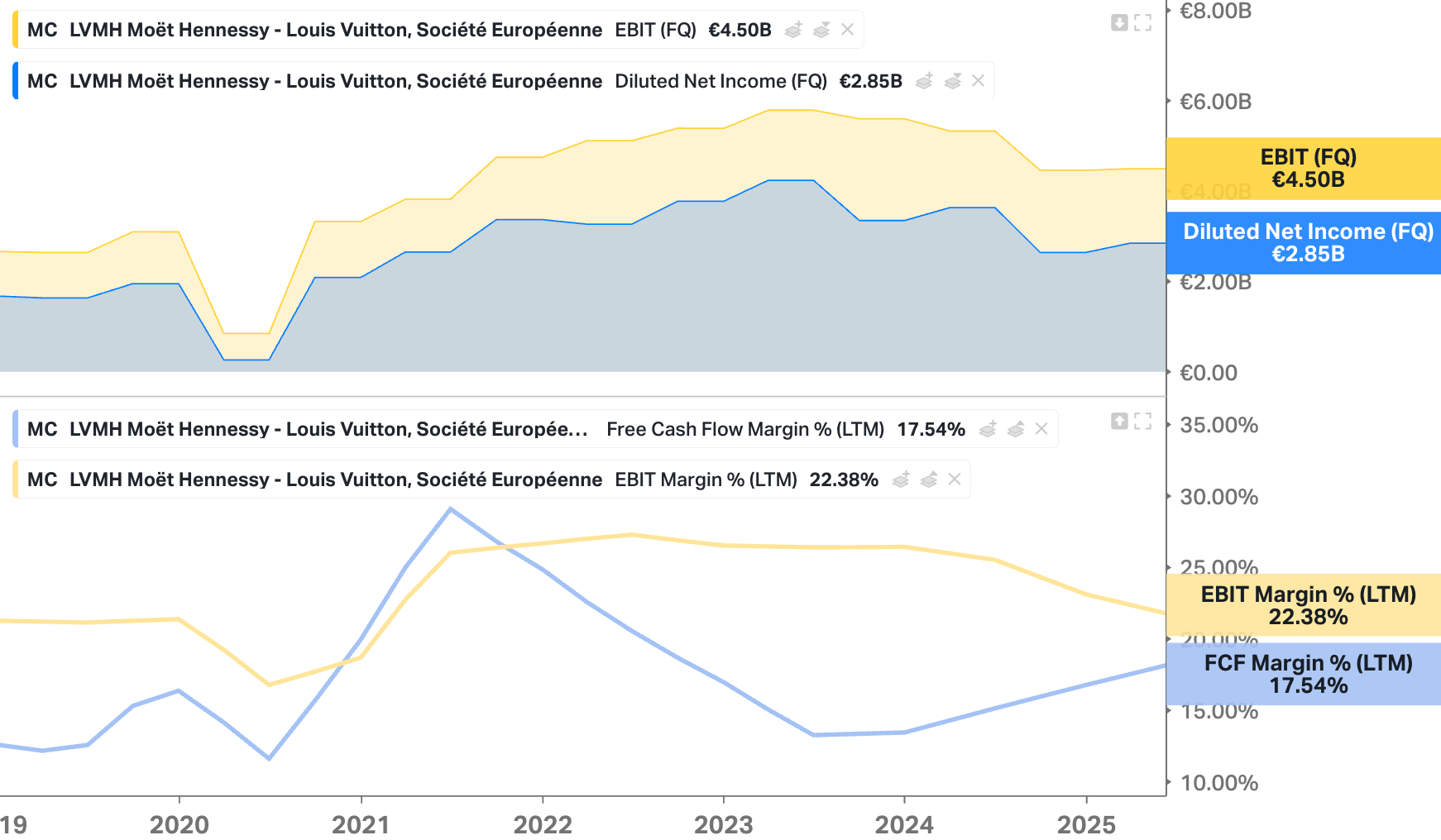

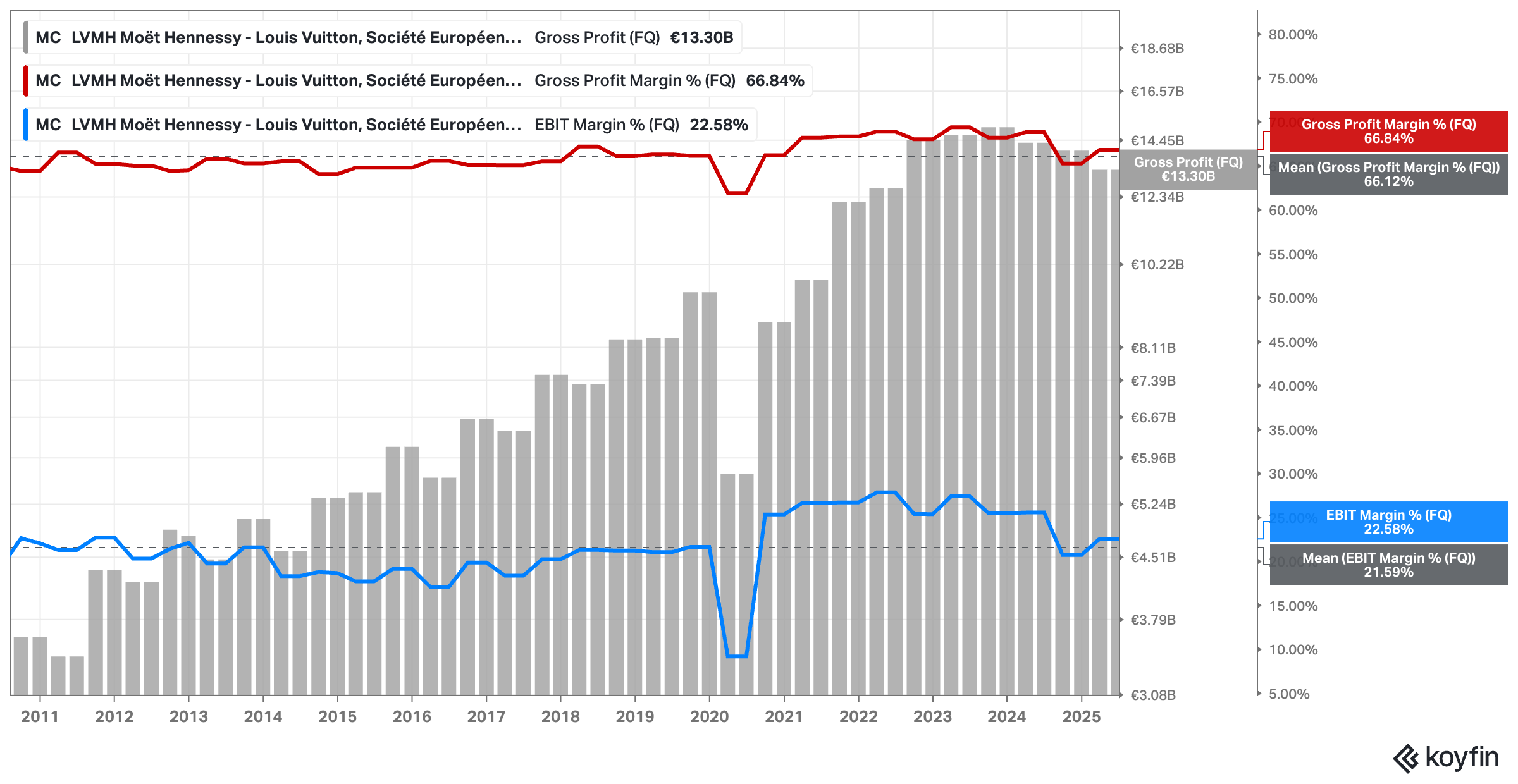

Clearly, this is not just a temporary market fluctuation (depending on how you define "temporary,” of course). Arguably, the share price performance is a reflection of a fundamental trend that has been developing for several – and I mean SEVERAL – quarters now. If you look at the company’s recent financial dashboard, the picture is clear. Both the topline, cash flow, and net profits (all represented on a per share basis) have effectively reached a (temporary?) plateau.

Net income and operating profit have, in fact, been declining.

There has been very little meaningful movement in these key metrics for some time. The post-pandemic surge is over. We are now in a period of grinding stagnation.

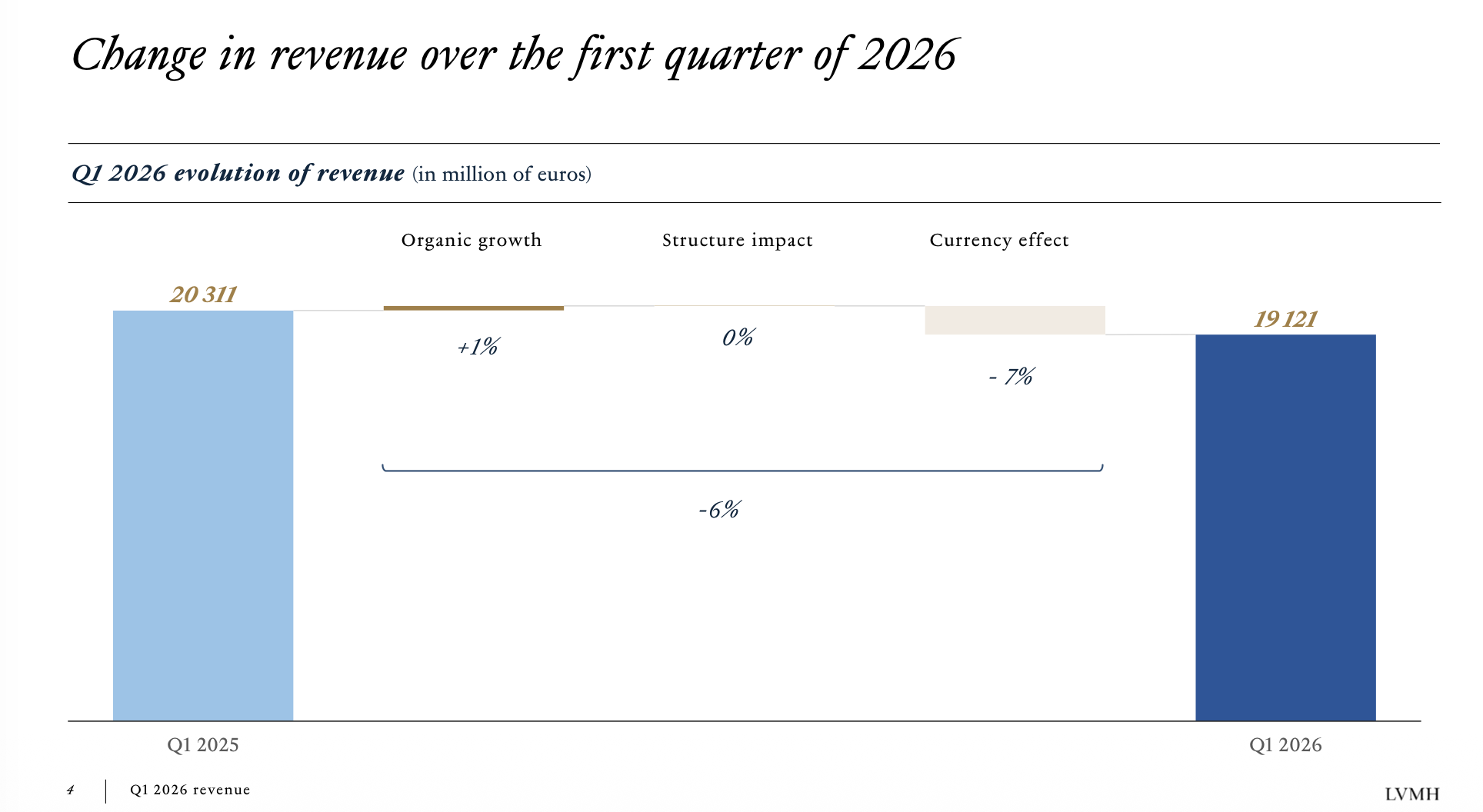

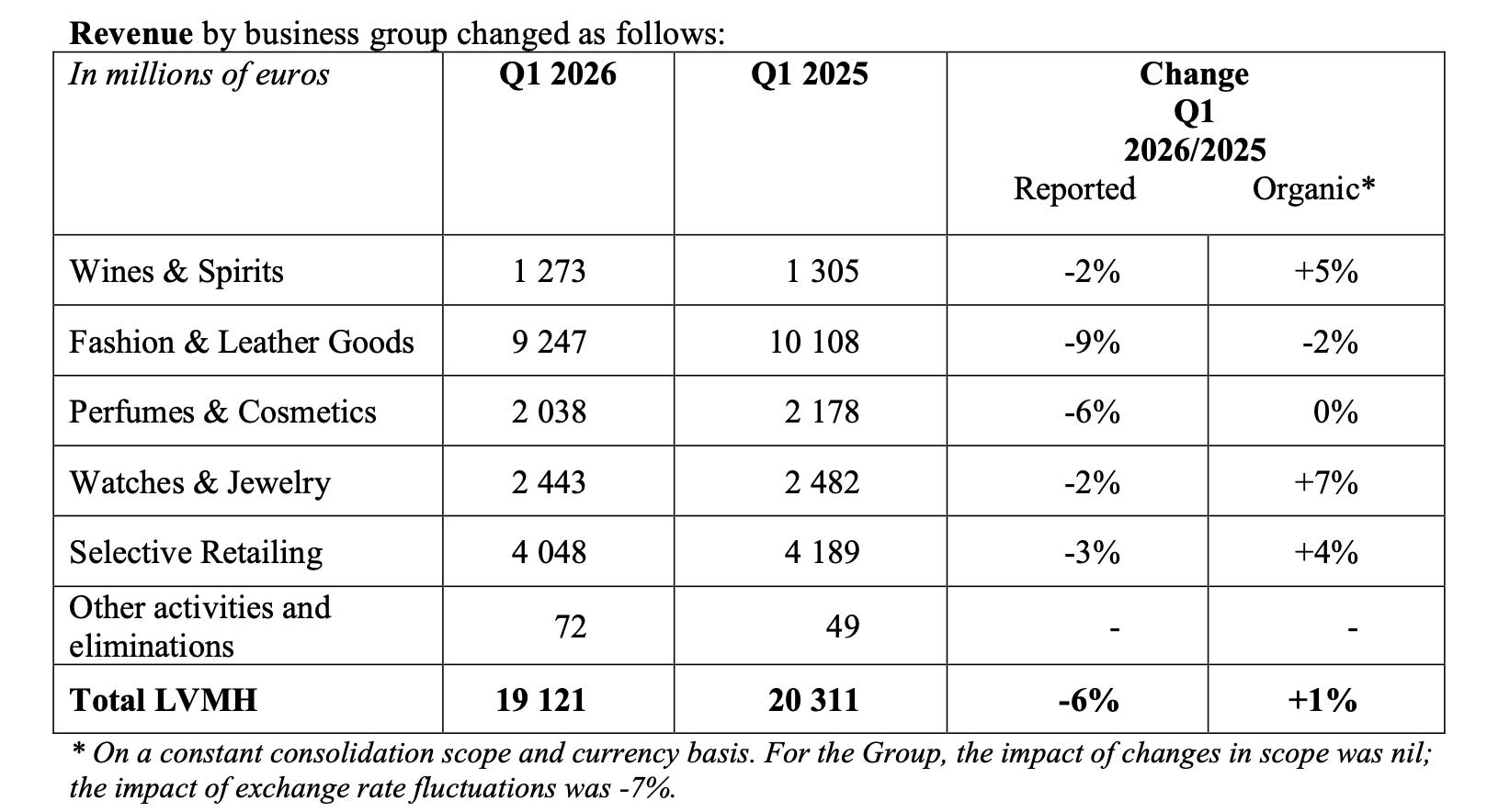

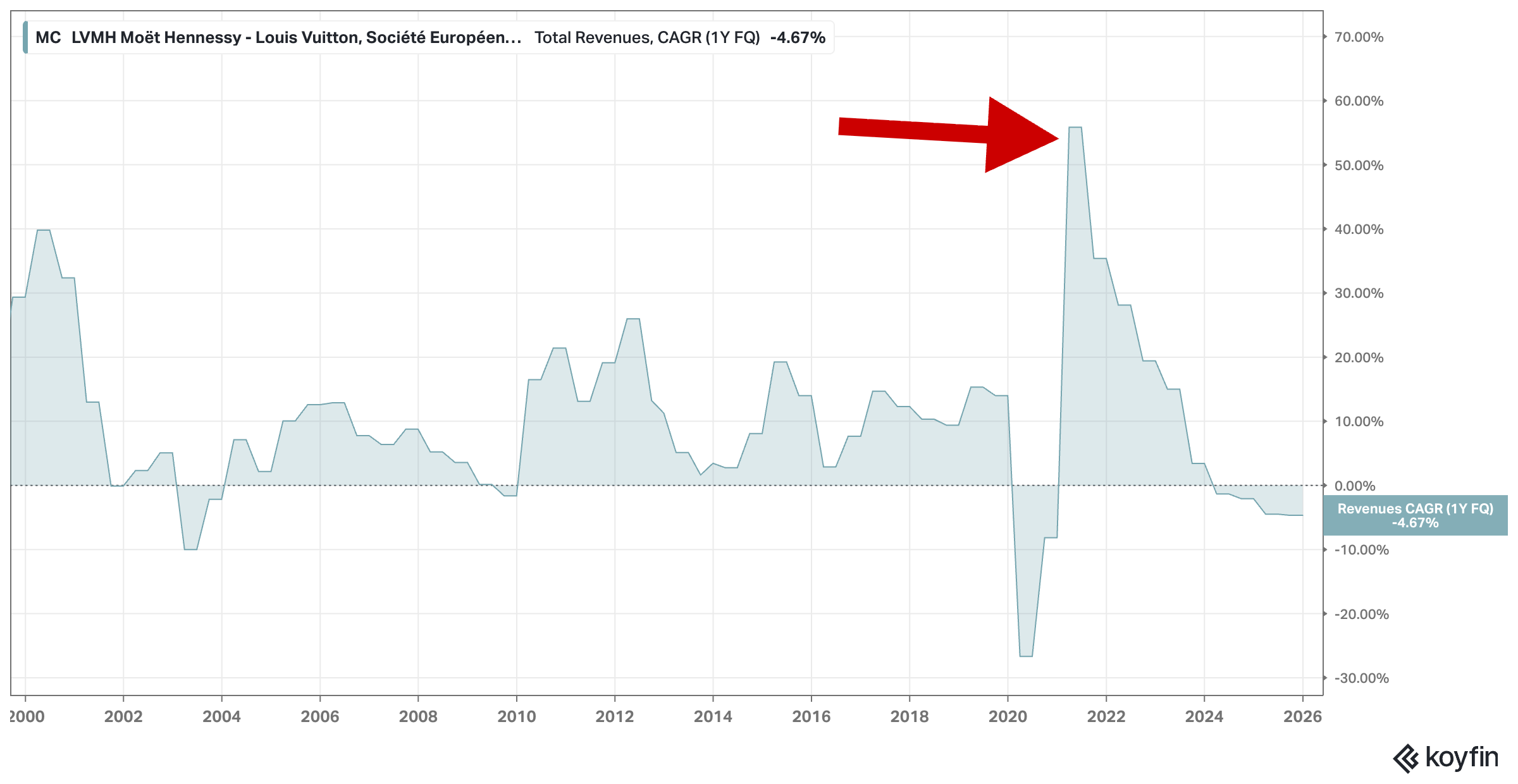

The Q1 2026 revenue results were another clear disappointment. Revenue came in at €19.1 billion. This represents an organic growth rate of just 1% (-6% reported). For a company that market participants previously valued for its consistent double-digit growth, this is a stark change in reality.

External factors have certainly played a role in this quarter’s underwhelming print. Management noted that the conflict in the Middle East created a headwind that shaved roughly 1% off the organic growth figure in March alone.

However, the problems appear to be more than just geopolitical. The Fashion & Leather Goods segment – the core of the entire group –, for instance, saw an organic decline of 2% (-9% reported). This suggests a softening in demand for the primary brands that drive the company’s valuation.

In my previous piece from July last year, I discussed the long-term moats of the business. I still believe those brands have value. But the current data shows that even the strongest names are not immune to a broader slowdown. The fundamental business performance is simply not moving forward.

In this post, I want to unpack what this means for the future of the stock. I will start by placing these results in context by comparing them to the latest updates from Hermès and Kering. It is important to see if LVMH is an outlier or if the entire luxury sector is facing a structural shift.

I will then dig into the specifics of the Q1 earnings and share my takeaways from the earnings call; what are the executives saying? We will also examine the bull case provided by Francois Rochon of Giverny Capital who purchased the stock last year. I want to weigh his optimism against the growing list of concerns regarding management’s recent creative and strategic decisions. Furthermore, I will address a question that is becoming more common among seasoned investors: Has management forgotten how to run the business? And what could this mean for the future? Finally, I raise the question of what the implications of investors fleeing the US could be on LVMH as currency headwinds prove to be more permanent than many may anticipate.

As you can see, there is a lot to cover. Let’s get into the details.

Disclaimer: I own LVMH shares in the portfolio I run for my partens. The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

Quick Q1 High-Level Overview

LVMH recorded revenue of €19.1 billion for the first quarter of 2026. On the surface, the headline figure of 1% organic growth might appear resilient in a volatile climate.

I find this narrative a bit too convenient. When you peel back the layers, the core engine of the group – Fashion & Leather Goods – actually saw an organic decline of 2%.

This is a significant yellow flag for a division that has historically been the bedrock of the company’s valuation. It is the first time in recent memory that we are seeing a sustained period where the brand heat of Louis Vuitton and Dior isn’t translating into growth (excluding the 2020 COVID quarters).

Management was quick to point out that the result was heavily weighed down by the conflict in the Middle East. That specific geopolitical drag shaved roughly 1% off the total organic growth in March. Without it, we would be looking at a 2% print.

“LVMH maintained its powerful innovative momentum and showed good resilience in a geopolitical and economic environment that remained disrupted, amplified by the conflict in the Middle East.” – PR

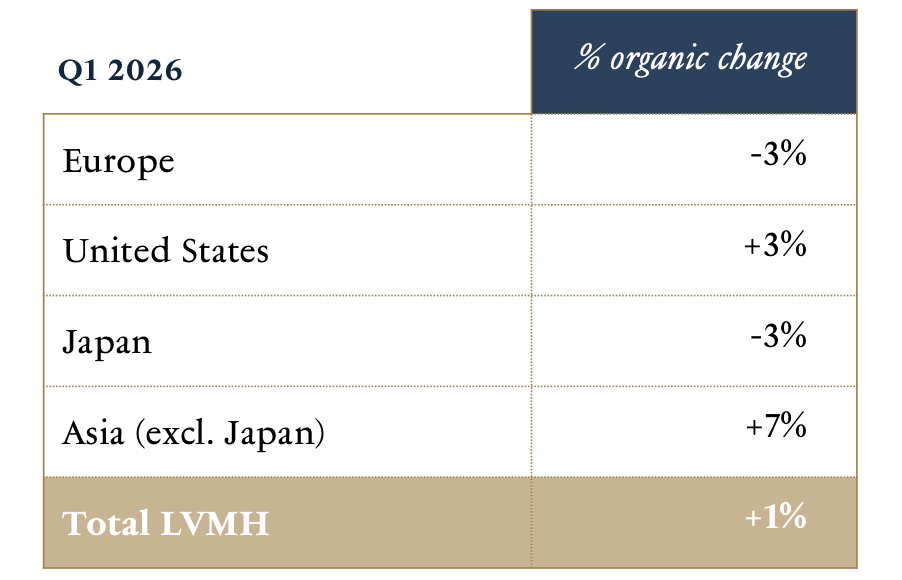

The geographic data tells a story of shifting dependencies. Asia excluding Japan remains a bright spot with 7% organic growth – the best quarterly performance really since the end of 2023 –, while the United States showed a decent start to the year at 3% (both geographies signaling a reacceleration QoQ).

“[…] it’s the best quarter since 2023. And it’s good because it’s broad-based. One thing to -- maybe to notice is that also Sephora is flat this quarter on the Asia cluster and especially China, which was one of the geographical areas that we were fixing for Sephora. So it’s good to see that it’s rebounding.“ - Earnings Call

However, the picture in Europe and Japan is much more somber, with both regions posting a 3% organic decline.

The culprit here is a significant drop in tourist spending. This highlights a structural vulnerability. If the wealthy globetrotter stays home or spends elsewhere, the European flagship stores suffer. While the top line is struggling, the currency situation made the reported numbers look even worse. A strong euro created a massive 7% headwind, dragging the reported revenue down by 6% year–over–year. This is a purely accounting–driven impact, but it adds to the general sense of a company under pressure.

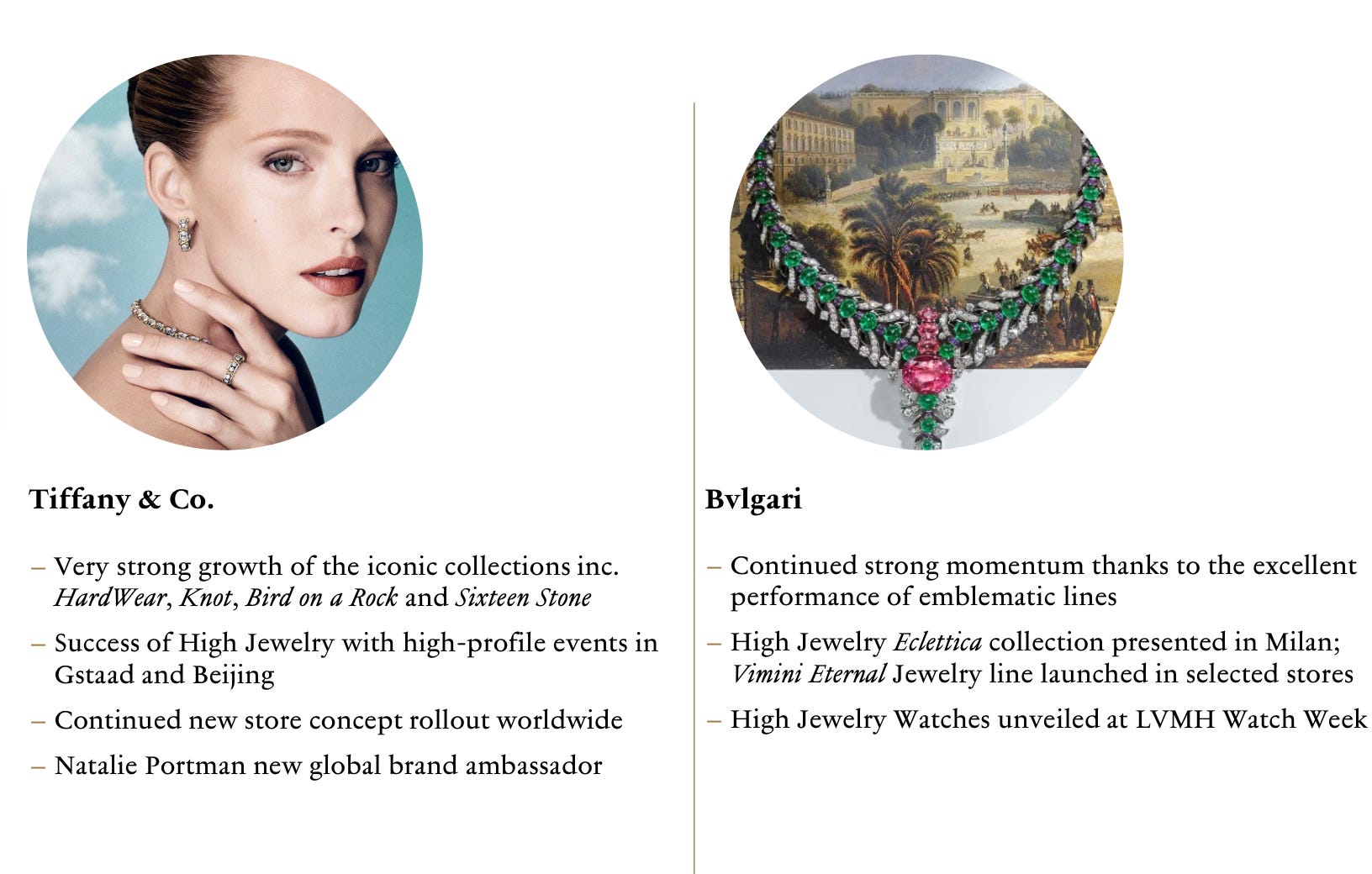

There were some pockets of strength that deserve mention. Watches & Jewelry grew by 7% organically, driven by what I see as a successful transition at Tiffany and continued momentum for Bulgari.

“The Maison [Tiffany] continued to successfully renovate its store network and strengthen its iconic product lines, with HardWear in particular posting very strong growth. Highlights of the quarter for Tiffany included the launch of a marketing campaign featuring its new global brand ambassador, Natalie Portman, and its latest high jewelry collections being showcased in Gstaad and Beijing.

Bvlgari achieved strong growth and unveiled Eclettica, a new artistic vision of high jewelry and prestige watches. The iconic Serpenti and Tubogas lines performed very well. Chaumet was boosted by the expansion of its Bee de Chaumet collection.”

Selective Retailing, which includes Sephora, also managed 4% growth. These “defensive” segments are currently doing the heavy lifting while the main house is undergoing a period of creative and regional transition.

The contrast between these segments and the core fashion business is stark. It suggests that while the brand equity of the jewelry houses remains intact, the “lifestyle” and high–fashion components are facing a much tougher sell. You have to wonder if the aspirational consumer is finally reaching a breaking point. The numbers suggest that for now, the answer is yes.

Insights From the Earnings Call

I spent a significant amount of time parsing the most recent earnings call, but I’ll be honest: there was no single “aha” moment that fundamentally altered the long–term outlook. The discussion largely revolved around the kind of granular, technical questions that analysts love to use for fine–tuning their quarterly models. While understanding the exact timing of inventory shipments or the perception of social media campaigns is useful for a hedge fund trader, it doesn’t move the needle for a structural thesis. Example?

Real investing requires a different kind of lens. You have to ignore the noise of the quarter and look at the horizon.

Generally, the tone of the Q1 2026 earnings call was one of cautious defense. CFO Cecile Cabanis repeatedly leaned on the word “resilience” to describe a set of numbers that, in any other cycle, would be considered anemic.

“On the EU, actually, the Europeans are resisting and quite resilient, because the European clientele is only slightly negative. But you still have the impact on the touristic clientele because of your currencies. And you might have some disruption also, it’s very difficult to address, on some specific tourism because of the conflict. [...]

On the question on tourist and clients, the best performing local clientele have been American and Chinese on Fashion & Leather Goods. The Japanese is still a bit down. And the Europeans are quite resilient, but slightly negative -- flattish, slightly negative.”

One specific exchange worth highlighting, however, was the way management quantified the fallout from the Middle East. We finally got a clear look at the scale of the impact, which doesn’t fully show up in the quarter yet. During the Q&A, an analyst asked for more specifics on the month of March, and the response was illuminating. Management noted:

Question: “So first of all, coming back to the impact of the Middle East, I think you said down double digit, but is it possible to be a bit more specific on the month of March? Was it down 30, 50? And also, are you seeing a bit of an improvement early in the quarter? And also if minus 1% is the impact from 1 month, do you think that minus 3% would be the impact on the full quarter?“

Answer: “Middle East, maybe I’ll put it simple so that you can have an easy idea of the impact. If you take the group, it’s overall 6% of the mix. I’ve said earlier, there are plus and minuses depending on the division. When the conflict started in the month of March, there was a shortfall and a deterioration of demand between 30% and 70%, depending on the malls, depending on the businesses. So overall, if you take a 50% deterioration, then you can have the overall impact, which would be indeed 3 points in March and 1 point on the quarter. I think the outcome, it’s anybody’s -- probably anybody’s guess. What we have not seen yet is repatriation. And what we know is that the wealth has not evaporated. So there will be a time where we’ll see that coming probably elsewhere and mitigate the impact should the conflict continue.“

Moreover, I found the narrative particularly telling when the discussion shifted to the 1% organic growth figure. Management was quick to isolate the geopolitical noise, stating that “the conflict had a negative impact of around 1% on organic growth for the quarter.” By their math, the underlying business is running at a 2% clip. While I understand the need to strip out one–off events, you have to wonder if this is becoming a convenient shield for a broader slowdown. There is a clear divide between what I see as short–term volatility and more structural, long–term challenges. The short–term pain is obvious: a massive 7% currency headwind and the sudden disruption in Middle Eastern tourist flows. However, the commentary on the United States and China suggests something more permanent is shifting. Cabanis admitted that demand for Wines & Spirits, for instance, in the U.S. “is still soft and that we don’t see moving a lot.” What if this isn’t a temporary dip but rather LVMH reaching a saturation point? As we will discuss below, I generally consider the alcoholic beverages segment to be the more permanent “problem child.”

The Q&A segment also revealed an interesting divergence in how the group views its various “engines.” While the Fashion & Leather Goods division – the crown jewel – is currently contracting, management is pivoting the conversation toward “hard luxury” and selective retailing. They noted that for brands like Tiffany and Bulgari, “the overall response to the icon, the craftsmanship, the high jewelry are very strong.” This might suggest that the ultra–high–net–worth individual is still showing up for €50,000 necklaces, even if the “HENRY” (High Earner, Not Rich Yet) consumer has stopped buying €3,000 handbags (this thesis can only partly be confirmed when looking at Hermès’ results further below, though).

The Broader Black Hole of Luxury Consumption? Looking at LVMH’s Peers

LVMH is not an island. To understand the current stagnation, you have to look at the broader wreckage across the sector. I’d argue that for around three years (mainly during the 2021–2023 period), the luxury industry benefited from a massive pull–forward of demand – a pull-forward demand cycle. We are now witnessing the formation of a consumption “black hole.” This is the natural hangover that follows a period where “aspirational” buying became almost a mania – or a way to cope with Covid and its aftermath? Even the most resilient players – yes, I’m looking at you Hermès – are now showing signs of fatigue.

It seems like this is a sector–wide reset. The tide is (temporarily) going out.

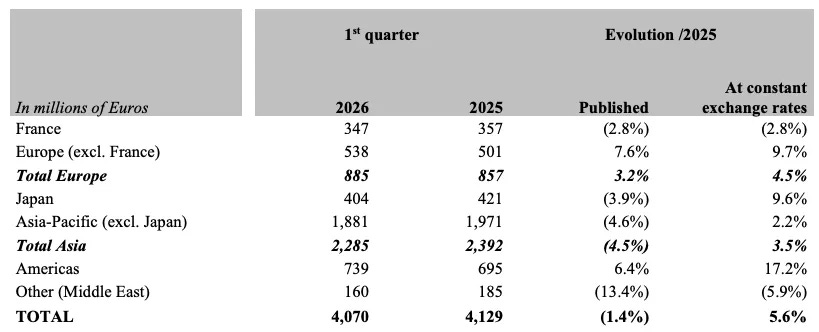

Today’s results from Hermès provided the most shocking evidence of this shift. For years, Hermès has been treated as the ultimate safe haven, a stock supposedly immune to the laws of economic gravity. That illusion shattered this morning. The shares are cratering, down 9% in a single session (-13% at one point).

This is a rare, almost unprecedented move for a company that hasn’t seen a one–day drop of this magnitude in two decades, excluding the literal onset of a global pandemic. While organic growth was 6% (yet negative on a reported basis) – a number most peers would envy in the current environment – it wasn’t enough to hide the cracks. France saw a 3% decline, and the Middle East fell by 6%. The myth of “absolute pricing power” regardless of any macro backdrop is finally being tested. When even the UHNWI Birkin bag crowd starts to hesitate, you know the environment has turned challenging.

The disruption in the Middle East and the escalating conflict in Iran have created a double–sided trap. First, there is the direct loss of regional sales. Second, and perhaps more importantly, is the impact on global tourist flows. High–end travel is the lifeblood of luxury. If flights are more expensive or routes are canceled, the “concession” stores and airport boutiques – which represent a massive chunk of high–margin revenue – simply stop breathing. Management confirmed that their owned stores grew at 7%, but their concession sales dropped by an identical 7%. This tells me that the local, loyal client is still there, but the traveling luxury nomad has disappeared.

It is a structural headwind that LVMH, with its massive global footprint, is feeling just as acutely.

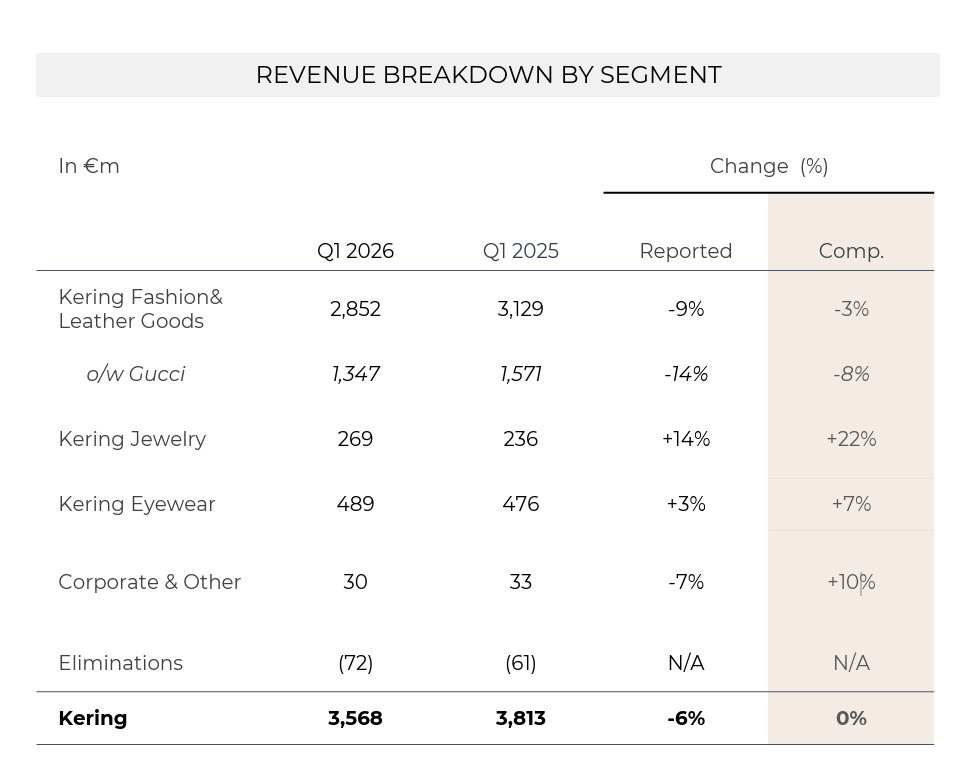

Kering, the industry’s perpetual laggard, also reported yesterday. You could describe the quarter as a period of “stabilization.” There is a massive divergence here though. Jewelry grew by 22%, proving that “hard luxury” is still a preferred store of value for the wealthy.

Meanwhile, fashion was down 3%. Gucci, the heart of the Kering investment case, is still stuck in a mid–turnaround purgatory (sales “down 14% on a reported basis and 8% on a comparable basis year on year“). While Balenciaga showed some signs of life, the overall fashion segment outside of Gucci looks remarkably similar to the flat performance we are seeing at LVMH. The “Gucci stabilization” is taking far longer than Kering bulls anticipated. It shows that once a brand loses its heat in this climate, rekindling it is an expensive and slow process.

“Outlook: In a still uncertain geopolitical and macroeconomic environment, the Group places a strong emphasis on agility and flawless execution, equipping each House with sharper, more sustainable brand strategies and the operational support required to accelerate progress. As Kering progresses through 2026, its objective remains to return to growth and improve margins.“

Looking at the results of these two peers, arguably, what we are seeing is a collective “pause” from the global consumer. The luxury powerhouses are paying the price for the excess of the COVID and post-COVID period. The industry pulled so much demand from the future that there is simply nothing left to harvest in the short term.

The question for investors is who can survive this black hole without diluting their brand or destroying their margins? And when can you reasonably expect a recovery and a return to higher growth (if any growth at all).

Right now, none of the big three look particularly comfortable.

Francois Rochon’s Longer-Term & High–Conviction View

I recently spent some time reviewing Francois Rochon’s discussion on “The Investor’s Podcast” with host Clay Finck (linked below). Rochon is a fund manager I’ve long admired for his ability to filter out the cacophony of the daily ticker and focus on the fundamental trajectory of a business. His perspective on LVMH is particularly valuable right now because it stands in such stark contrast to the prevailing gloom in the market.

He was refreshingly honest about his own position, noting that he bought into the company last year and has yet to see a positive return.

“Well, I’m not that good in timing because I bought it last year and so far has not yielded good results“

But for an investor of his caliber, the immediate price action is almost irrelevant. He is focused on the earning power five years from now. His central argument is that the current slowdown is not a sign of structural decay. Instead, just like I do, he views it as a necessary cooling period after the feverish growth of the pandemic era. He sees this as a return to normal rather than a collapse.

“I think probably the years 21, 22, 23 were very very strong but at some point you know consumers needed a little pause in their purchasing and it’s very hard to predict but I think part of the slowdown is just a return to normal so probably the first years 2021 22 was a little too strong relative to let’s say historical norms. So there’s part of that. Also you know inflation makes those products pretty expensive and it’s been a tougher period for consumer in general.”

This normalization thesis is a powerful counter–narrative to the panic selling we’ve seen recently. It suggests that the double–digit growth some investors grew accustomed to was actually the outlier.

Rochon remains unshaken because he believes the brand equity is intact. To him, the only thing that matters is whether the name Louis Vuitton still signifies unparalleled quality to the global elite. He argues that as long as the brand resonance hasn’t faded, the financial results will eventually catch up. It is a long game. The quarterly fluctuations of 2026 are merely footnotes in a much larger story of brand durability.

“I think the key factor is that you want the brand to be as strong as it ever been. That’s what you want. So perhaps people are a little wary of purchasing Louis Vuitton bags, but what you really want is the brand, the name still resonate to clients as quality, something you want to own because it’s of quality and also it’s been there for 150 years and I think that’s the key thing. If the brand is as strong as it was five years ago, eventually the sales will reflect that. […]

But the rest of the business I believe is more cyclical. So I think at some point earnings will rebound and I think probably from here earnings could increase 60 or 70% in the next 5 years. So let’s say a 10-11% growth rate and you’ve got a two percent dividend. So the two together I think … we should be able to attain our objective of finding a 13% grower including the dividend.”

The second pillar of Rochon’s thesis involves China. While many investors are running for the exits due to geopolitical tensions and the “common prosperity” movement, Rochon remains a dedicated optimist. He views China through a lens of decades, not years. His belief is rooted in the simple math of GDP per capita growth. He expects the Chinese middle and upper classes to continue expanding at a rate that will eventually surpass the Western world in terms of luxury consumption. To Rochon, the current political climate and the trend of “luxury shame” is a temporary headwind. He is betting on the triumph of human aspiration and the universal desire for status.

“As they get richer at a faster rate than North American, I think they’ll want to acquire LVMH products, luxury products. Could also be Hermès bags or Prada bags. But in general, I think the demand for luxury goods in China will increase. There will be ups and downs. Perhaps there will be some periods like you described that the government doesn’t really sponsor showing up your wealth but that’s temporary at some point we’ll be back to normal and as the country improves and continues to improve the GDP per capita it’s going to be a stronger economy and they’ll purchase more luxury goods and I think it’s going to be a good market for perhaps not in one year or two years, five year, 10 years, 15 years, and they’re building a business for the next decade.”

I think many investors also overlook the “hidden” engines within LVMH because they are so focused on the headline leather goods numbers. Keep in mind that LVMH is home to 75 distinguished Maisons rooted in six different sectors and hence, is arguably the most resilient of all the luxury stocks you can purchase on public markets (and yes, more resilient than Hermès, one could argue!).

Rochon’s enthusiasm for Sephora is a perfect example of this. He views it as a “fantastic business” and a “very very strong retailer.” While it only represents about 10% of the group’s total revenue, it is growing at a rapid clip. He even noted that Sephora is now a significant competitive threat in the U.S. market, putting visible pressure on the margins of companies like Ulta Beauty.

“Sephora I think is a fantastic business. And I think people when they talk about LVMH, they don’t talk that much about Sephora, but it’s probably just 10% of revenues, but I think it’s growing pretty fast and it’s a very very strong retailer. We’ve been following also Ulta Beauty, which is a very very well-managed company, but you know there there have been some pressure on margins because in the IM they got more competition from Sephora in the United States.”

One of the most intriguing details Rochon highlighted during the interview – and something I haven’t seen discussed much elsewhere – is the specific tax headwind LVMH is facing in France. He noted that a “temporary increase in the tax rate” has been quietly eating into the reported earnings per share. The corporate tax rate for entities earning over €1 billion jumped from 28% to 33%. This is a five–percentage–point drag that has nothing to do with brand heat or consumer demand. It is purely a matter of fiscal policy. Rochon remains hopeful that this is a temporary measure, and if the rate reverts to 28%, it would serve as an immediate and mechanical catalyst for earnings growth.

What I also found compelling about Rochon’s stance is his focus on the Arnault family’s stewardship. While I have my own concerns about the current creative direction and the headwinds facing the aspirational consumer, Rochon’s thesis provides a necessary anchor. It forces you to look past the immediate carnage and ask if the soul of the business is still healthy. For him, the answer is a resounding yes. It’s a bold bet on the persistence of luxury.

Has Arnault Lost the Midas Touch?

I recently encountered a comment in my investor community that stuck with me. A member asked whether the Arnault family might have forgotten how to run their business properly in recent years?

I’ve given this some thought – and while it’s easy to blame the captain when the ship hits choppy waters (remember how many investors called for Google CEO Pichai to step down during the tough quarters?), the reality is usually far more nuanced.

When a stock is underperforming and the chart looks like a mountain range in descent, our brains often default to System 1 thinking. Price starts affecting the narrative surrounding a stock. Humans’ intuitive, impulsive side of their psychology starts taking over; the part that seeks simple narratives. We see a drawdown and assume management has lost its edge. It is far harder to admit that the forces at play might be entirely outside of their control.

But let’s start by considering what the Arnault family could’ve done better in recent years. If we look at the case against the Arnault family, there are certainly some valid criticisms to be made regarding recent creative and strategic choices.