A while ago, I came across a tweet that made me pause. The user asked: “What are some good businesses that have gone sideways for a few years? Thinking MSCI, EXPO, OTCM… what else?” Among the replies was one from Dennis Hong – a name many value investors will recognize from his appearances on Tilman’s podcast and Rob Vinall’s annual gathering. His list included: LVMH, Mettler-Toledo, Kone, SGS, Intertek Group, Veeva Systems.

LVMH? That caught my attention, because it is high up on my watchlist too.LVMH – the world’s largest luxury conglomerate – has gone precisely nowhere for more than five years. Since January 2020, the stock has basically flatlined.

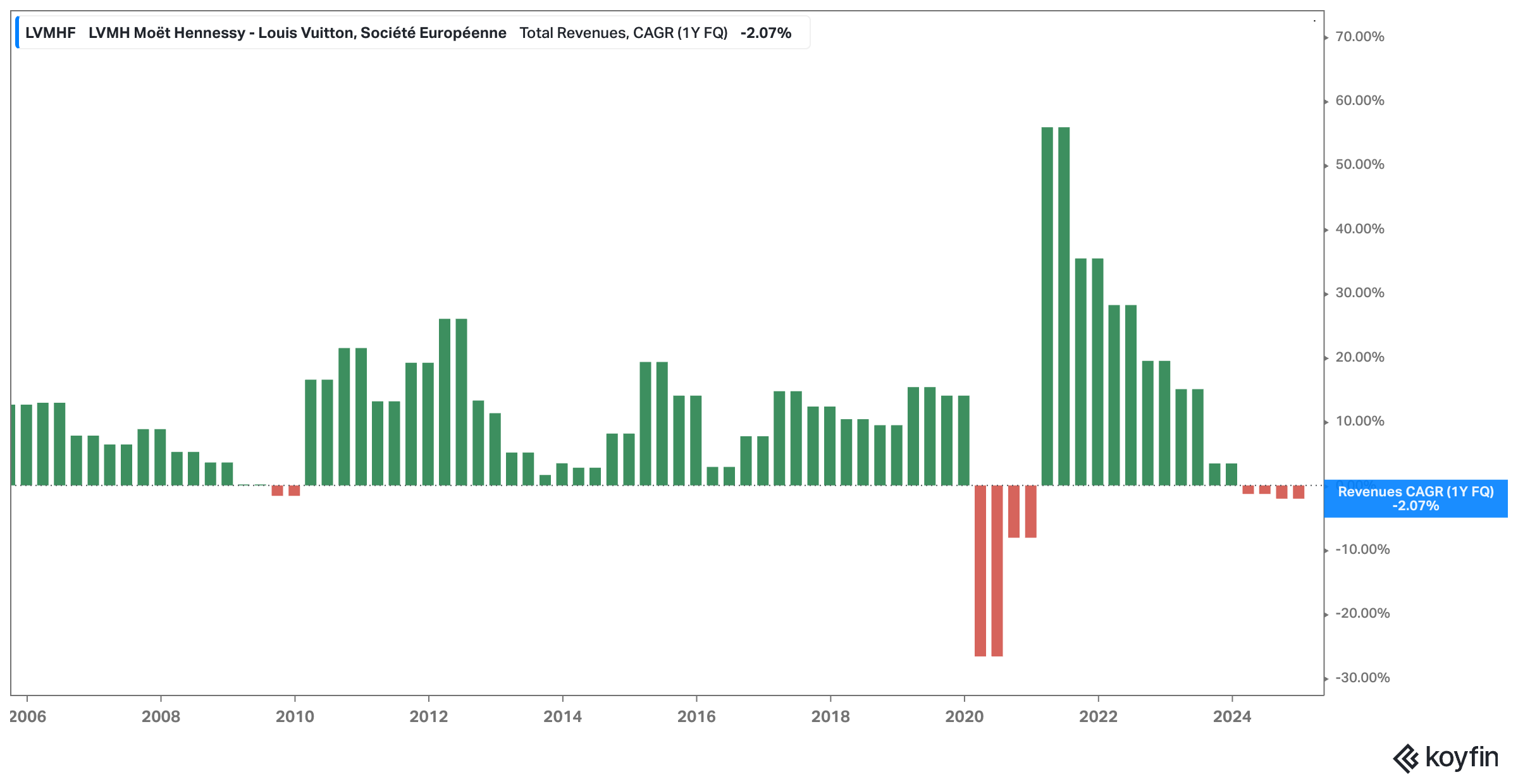

It’s been 5.5 years of watching the S&P climb steadily higher (up >90% since early 2020) while LVMH, one of the most prestigious brand empires on the planet, treaded water.

That alone could test any long-term investor’s conviction. But add to that the fact that the stock was down roughly 46% (until just a few days ago) from its April 2023 peak, and what you get is LVMH’s worst drawdown since the global financial crisis, when it dropped more than 60%.

So yes, the tweet was timely. But it got even more interesting when someone replied to Dennis:

“I’m not sure if $LVMH is a good business. Individual sub components may be, but the collection as a whole is pretty unwieldy. Wouldn’t be a buyer, they need to majorly rethink this entity.”

That comment pushed me to chime in. I wrote:

“When people start calling $LVMH an average business, we're getting close to this being an opportunity. I get the point, it's not $RACE or $RMS, but LVMH is clearly an above-average business. I'll probably own it soon.”

And that’s the thing. I meant it.

The best time to sell a stock is usually when the headlines are glowing, the earnings beats are stacking up, and everyone’s onboard. But the best time to buy? That’s typically when the air gets thick with pessimism. When the stock is in freefall, the narrative turns sour, and everyone suddenly rediscovers their inner skeptic. That’s when you need to start looking closely again. Not always to buy immediately, but to understand what’s real and what’s just recency bias dressed up as insight.

That’s exactly where we are with the luxury sector. A nasty mix of fading Chinese demand, an overstretched post-COVID consumer, and geopolitical noise (including tariffs and trade war tensions) has taken the wind out of the sails.

According to Bain & Company, the sector has shed 50 million customers in just two years (from 400 million in 2022 to 350 million in 2024). Fifty million.

In fact, luxury might be one of the most unloved corners of the market right now. It's right up there with alcoholic beverages in terms of investor sentiment. And let’s be honest: when a sector goes from being the belle of the ball to barely getting invited, that’s often when things get interesting again.

So that’s what I’ve been doing—taking a closer look at LVMH. And in this post, I’m going to walk you through what I’ve found so far.

Yes, a lot of the bullish case is fairly well-known. But I’ll also dig into some of the bearish talking points that are starting to circulate more loudly: things like the group’s structural complexity, the cyclical nature of growth, and the risk of China exposure. I’ll also cover the succession question, acquisition dynamics, concentration risk, and even why Berkshire might have passed on this type of business entirely. Along the way, I’ll highlight which concerns I take seriously, which ones I think are overblown, and where I still have open questions.

“While maintaining its 'hold' recommendation on Moncler, Jefferies has lowered its target price from €57 to €49, following a 'high single-digit reduction in its estimates for the Italian luxury winter clothing company. 'Estimates for the second quarter are looking cautious, even as investors debate how the increased pressure on demand in the sector will play out across brands," the broker said. – Source: CercleFinance.com

This isn’t a one-dimensional pitch piece. It’s the product of an ongoing research process, and I want to bring you into it. Because sometimes, the most interesting opportunities aren’t the ones where everything’s perfect – they’re the ones where the cracks in the narrative start revealing a deeper kind of strength.

Here’s a bullet-point overview of topics covered in this piece (10,000 words in total):

Why I started looking at LVMH again now

A condensed “bam bam bam” version of the bull case: If I had to summarize the thesis in five bullets, this is it.

An excerpt from an investment letter I wrote in April: I’ll share the rationale I laid out when I made my first purchase for my parents’ account, covering the business model, margin profile, management incentives, and my valuation framework at the time.

How “luxury” LVMH really is, and why segment-level margins can be misleading: We’ll look at what LVMH’s profitability really tells us – and why looking at individual business group margins in isolation misses the bigger picture. I’ll show long-term trends, cross-brand dynamics, and why operating leverage still matters here.

Why desirability – not just exclusivity – is the tightrope LVMH must walk

How the recent boom (and bust) exposed the cyclical nature of luxury

Why downturns are when Arnault gets aggressive – and why that’s good for shareholders: I’ll dig into LVMH’s acquisition playbook, from Tiffany to Moncler to potential rumors around Richemont.

Three underappreciated risks: No thesis is complete without looking at what could go wrong.

I’ll explain why LVMH’s diversified structure helps mitigate brand-specific blowups.

What it means that a famous quality investor has started building a position

The philosophical tension behind why Berkshire may never buy a stock like this: Drawing on thoughts from Guy Spier and Charlie Munger, I’ll close by reflecting on the idea that luxury businesses profit by triggering envy.

Before we dive back in, a quick note…

Want to compound your knowledge – and your wealth? Compound with René is for investors who think in decades, not headlines. If you’ve found value here, subscribing is the best way to stay in the loop, sharpen your thinking, avoid costly mistakes, and build long-term success – and to show that this kind of long-term, no-hype investing content is valuable.

Thank you for your support!

Disclaimer: I own a few LVMH shares. The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

Part 1: Bam Bam Bam Bam Bam – Why LVMH?

Before we dive deeper into the weeds, let me first zoom out and frame the core thesis. When I think about LVMH right now – where the stock is trading, how investors are talking about it, what the headlines are focused on – I honestly don’t see a broken business. I see a world-class company going through a classic short-term downturn and a resulting sentiment reset.

Luxury as a sector has fallen out of favor, and LVMH, despite its dominance, hasn’t been spared. But if you strip away the noise and focus on the fundamentals, the long-term case remains compelling, despite four consecutive quarters of negative revenue growth – which only happened once before in the last twenty years of LVMH’s history as a public company!

Here’s the high-level view – the five reasons why I believe LVMH deserves serious attention from long-term investors right now:

BAM 1 – Global Champion of Timeless Brands: Owning LVMH means owning stakes in the most iconic names across fashion, cosmetics, jewelry, and spirits – brands that define status across cultures and generations. Louis Vuitton, Dior, Tiffany, Hennessy – these names aren't going away.

BAM 2 – Durable Moats and High Margins: LVMH’s intangible assets are off the charts. Deep brand equity, cultural relevance, and artisan heritage fuel serious pricing power – reflected in industry-leading gross margins and consistently decent returns on capital.

BAM 3 – Founder-Led with Skin in the Game: Bernard Arnault still runs the show – and he owns nearly half the company. The Arnault family eats its own cooking and has spent decades building this empire. When the guy buying more shares is also the CEO, that matters.

BAM 4 – Resilient Financials, Optionality for Offense: The balance sheet is strong, cash flow is steady, and capital allocation has historically been disciplined. When the cycle turns down, LVMH doesn’t flinch – it hunts – and the current downturn may actually provide opportunities for acquisitions at attractive prices.

BAM 5 – Attractive Valuation in Disguise: At ~13-14x steady-state EBIT (my estimate), LVMH is trading like a boring industrial. But this is a compounding machine (albeit slowly in the high single digits) with pricing power, brand depth, and a track record of solid FCF growth. The setup looks compelling – especially with sentiment so low.

The full story starts here:

Investing is the one domain where better thinking compounds. If this intro gave you new insights, the full piece goes even deeper. A paid subscription is an investment in your decision-making process – and your returns.