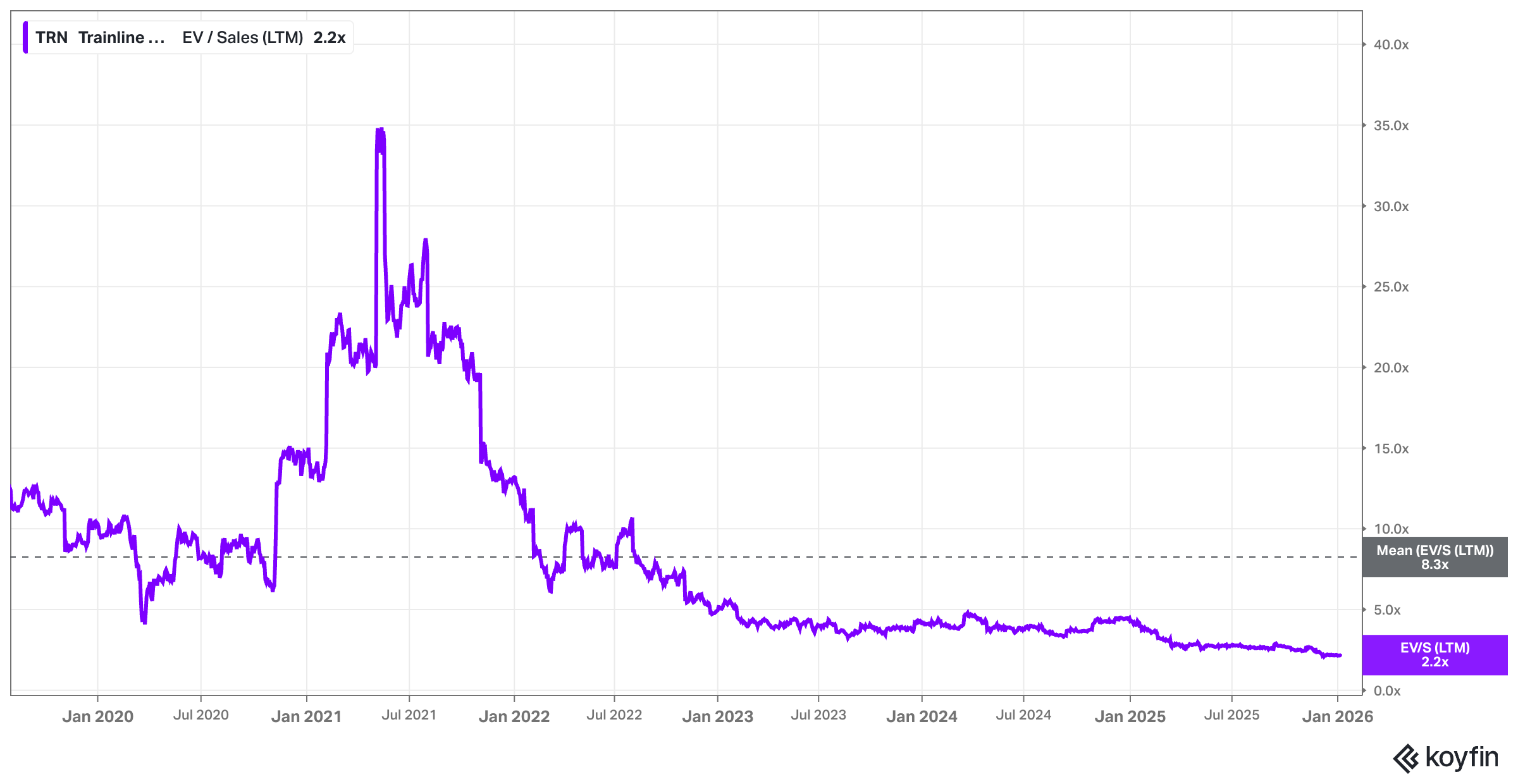

In the first days of 2026, while most investors were still dusting off their watchlists and refreshing market charts, I stumbled across a new idea that stopped me in my tracks – and made me stop everything else I was working on at the time. It was another UK business. The valuation looked almost too attractive to ignore: an asset-light compounder generating 80%+ gross margins, free-cash-flow margins above 25%, and strong and improving reinvestment returns on incremental capital (ROIIC). It has compounded its topline at a 5-year revenue CAGR of 16%, and most importantly, in my Koyfin dashboard it appeared as a 14% FCF yield opportunity (19% according to my H1 annualized “owner earnings” adjustments; as to be discussed in part 5 of the analysis) – the EV/Sales multiple collapsed from around 35x at the peak in 2021 to just 2x right now.

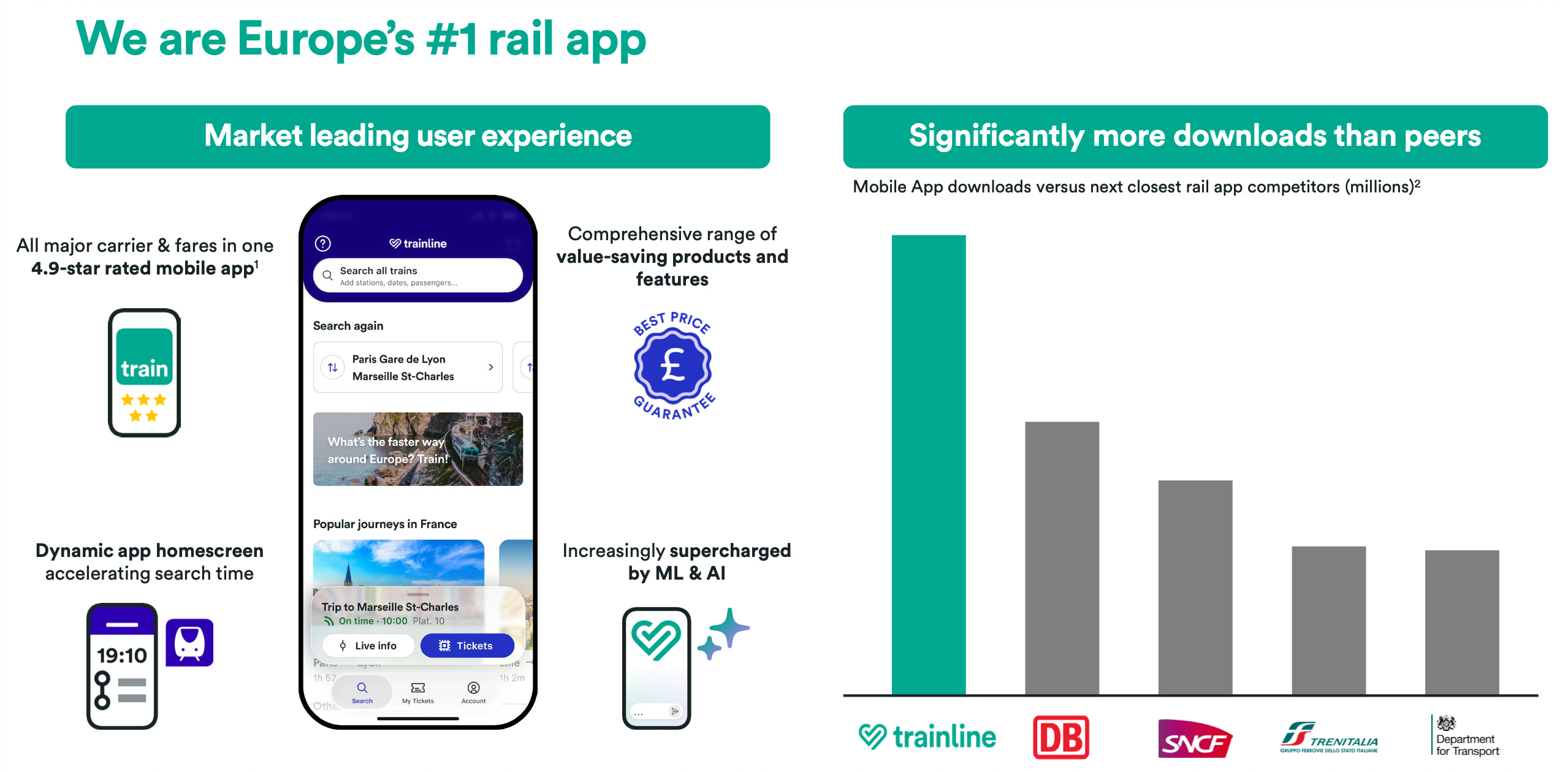

The stock I’m talking about is British digital rail and coach technology platform Trainline, Europe’s most downloaded rail app (“in a market estimated to be worth around €55 billion“).

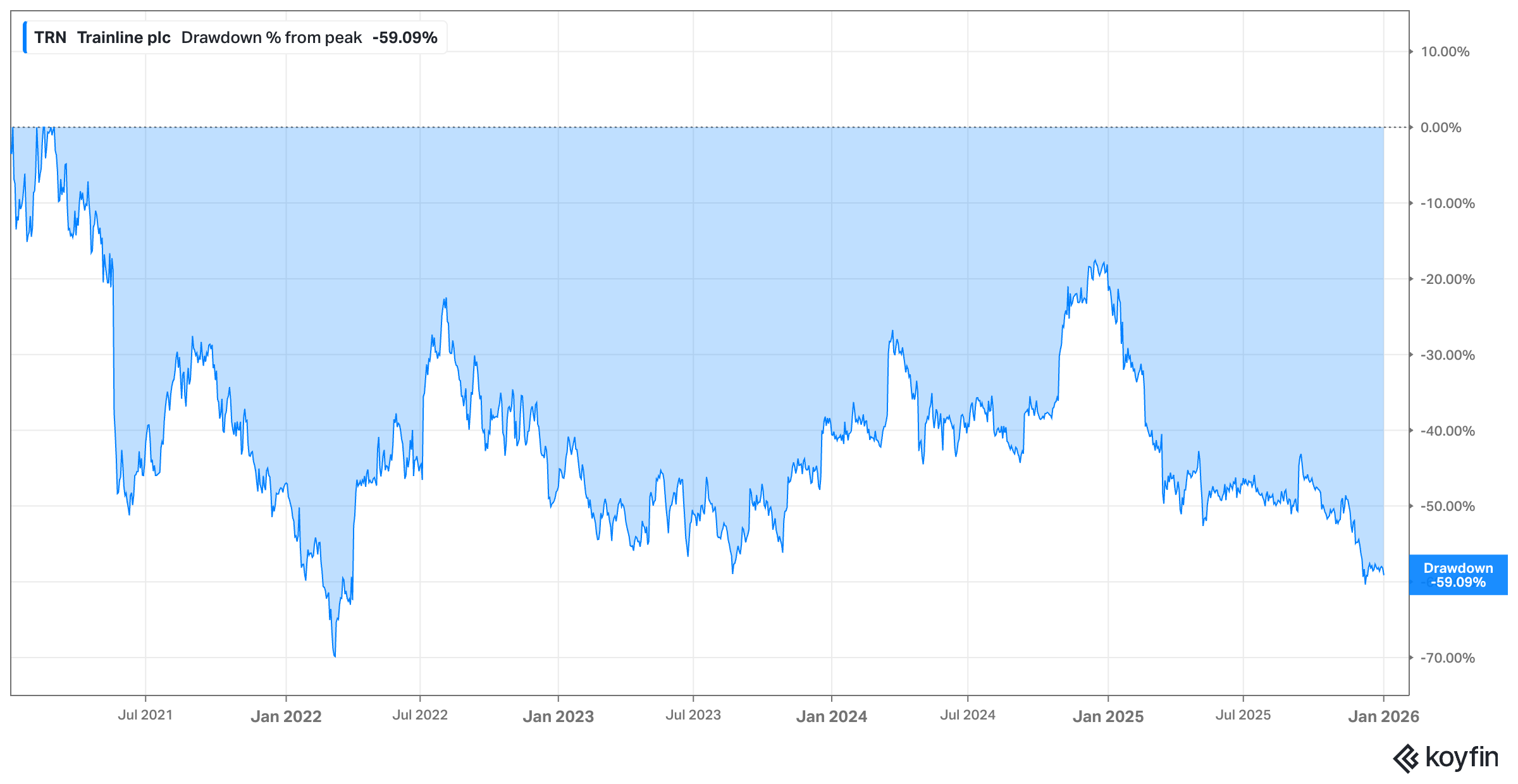

And arguably, few companies illustrate the tension between structural disruption and secular digitization tailwinds quite like this business. On one side, you have a pan-European travel marketplace with 27 million active users, 270+ operator integrations, and gross margins north of 80%. On the other, a UK rail system in political overhaul, creeping contactless ticketing that bypasses apps entirely, mobility behemoth Uber entering the space three years ago, and a Google search funnel that has already shown it can shift traffic dynamics with a UI update. Put differently, the numbers suggests this is a “high-quality compounder.” The narrative and current sentiment, however, tells you there’s serious “middleman & disruption risk.” And in 2025, the market made it clear which version it feared most: the stock price roughly halved – down 60% from a prior peak – as regulatory uncertainty took centre stage.

Trainline’s de-rating isn’t the result of collapsing demand or evaporating margins. It’s the result of five structural debates that question whether this business model can still capture value when the rails go digital, centralized, or AI-navigated. These debates have created one of the most asymmetric setups in UK travel-tech: a business that has already demonstrated post-pandemic profitability, but hasn’t yet demonstrated immunity to disruption – especially in a core market being redesigned by public policy and influenced by external platforms. And while the market prices uncertainty quickly, marketplaces like Trainline only earn back credibility slowly, through evidence, great economics, and durable customer habits.

To understand why this stock polarizes opinion so aggressively, you need to understand what Trainline is and what it isn’t. We’ll discuss this in great detail in this analysis, but from a high-level POV: It doesn’t run trains. It doesn’t own coaches. It doesn’t set ticket prices. It doesn’t hold inventory. What it does own is the transaction layer, the operator connectivity graph, and the user interface that simplifies a highly fragmented industry. It’s a typical aggregator business. Trainline captures a small slice of a huge rail ticketing and journey ecosystem – a category estimated to be worth tens of billions in Europe (€55 billion according to a C&C analysis) and still structurally shifting online.

This is not a stock for people who want easy answers. This is a stock for people who want nuanced answers to the right set of questions. And arguably, those questions are the five debates outlines below that will ultimately determine whether Trainline is mispriced, misunderstood, or merely early in a sentiment recovery cycle:

Can a UK government platform unseat an independent aggregator?

How far can contactless ticketing spread before app-based retail becomes optional, not default?

Are pan-European corridor wins enough to prove scalable continental relevance?

Is integration-depth friction strong enough to defend a moat when AI assistants can shortcut search?

Can margins expand further while commissions compress, or do take-rates ultimately reset downward?

My goal in the full post below is not to pick a side emotionally, but to stress-test each question carefully. It seems like there is a massive disconnect – between the share price and the financials the company actually delivered – and this is exactly why Trainline has become one of the most interesting travel-tech stocks in Europe.

Here are the topics I’ll explore in this comprehensive 21,000-word analysis:

The 90-second “Bam Bam Bam Bam Bam” pitch – how the stock can be pitched in under two minutes, and what makes it intriguing right now.

What the business actually is, beyond the simplification of being a ticketing app (segment analysis, geographical mix, product, customers, etc.)

How carrier integrations shaped Trainline’s expansion and market positioning (in the past and today)

The economics of being a travel intermediary that doesn’t own trains, tracks, or coaches & why the model shows negative working capital dynamics

How the UK and Europe differ in adoption maturity, monetization, and app entrenchment

Comprehensive competitive advantage analysis – Competitive pressures, moat stack, supplier leverage, and whether the moat is narrowing or expanding in different geographies

Management background, compensation, ownership, capital allocation behaviour through crisis, and capital return discipline

What the balance sheet reveals about settlement timing, capital intensity, and impairment sensitivity

Maybe most importantly, a nuanced discussion of risks & the five key debates outlined above.

My own valuation work – key variables and assumptions & the long-term growth levers that drive long-term value

My “owner earnings” estimates which are based on a couple of adjustments, producing a higher effective yield than the one showing up in investment terminals

Detailed segment modelling

A multi-stage TSR model (downloadable so you can make your own adjustments)

Where this business sits in its life cycle, and why optionality in adjacencies exists

Disclaimer: The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

High-Level Thesis – The “Bam Bam Bam Bam Bam” 90-Second Pitch

The full analysis starts here:

The rest of this post covers the topics outlined above. If you’re serious about sharpening your investing edge, the full post (and all my previous premium content, including valuation spreadsheets, deep dives (e.g. well-known mid- and large caps such as LVMH, Duolingo, Meta, Edenred as well as more hidden gems such as Tiger Brokers, Digital Ocean, Ashtead Technologies, InPost, Timee, and MANY more) and powerful investing frameworks. is just a click away. Upgrade your subscription, support my work, and keep learning.

Annual members also get access to my private WhatsApp groups – daily discussions with like-minded investors, analysis feedback, and direct access to me.

PS: Using the app on iOS? Apple doesn’t allow in-app subscriptions without a big fee. To keep things fair and pay a lower subscription price, I recommend just heading to the site in your browser (desktop or mobile) to subscribe.