Thinking in Bets: What Poker and Horse Racing Teach Us About Markets

Three Worlds, One Core Idea!

Most people wouldn’t naturally group stock market investing, poker, and horse betting into the same category. One has billion-dollar companies and earnings calls, another is played in smoke-filled card rooms (or sleek online interfaces), and the third involves animals, turf, and betting slips.

But peel back the surface layers, and you’ll find that all three domains are deeply connected by one powerful thread: they’re probabilistic disciplines.

What does that mean? It means that success in any of them doesn’t come from always being right, but from consistently making high-quality decisions in the face of uncertainty, incomplete information, and randomness. The outcomes are noisy.

Skill plays a role, yes—but so does luck. And while luck may dominate the short term, process-driven thinking and sound probabilistic reasoning win out over time.

This is a mindset shift that many investors – especially newer ones – struggle to make. We’re wired to crave certainty, to seek patterns, to believe that good outcomes come from good decisions and bad outcomes from bad ones. But in probabilistic environments, that just isn’t how it works.

You can make a perfect decision and still lose money.

You can make a terrible call and get lucky. And the reverse.

That’s why I find it so valuable to study other domains where this probabilistic nature is front and center, especially poker and horse betting. Both force participants to constantly weigh odds, assess ranges, understand risk and reward, and – crucially – manage variance.

And if you can train your brain to think probabilistically in those arenas, you’ll be far better prepared to navigate the messy, complex world of investing.

In this post, I want to explore what poker, horse betting, and investing have in common, and just as importantly, where they diverge.

I’ll look at how luck, skill, and competition intersect, why sample size matters more than we think, how process over outcome is the only sane way to think long-term, and why investing is perhaps less like poker than many believe, and more like betting on horses; at least if you’re doing it thoughtfully.

This is a deep dive, so we’re going to explore:

Why variance can obscure even the best decisions

How luck vs. skill plays out differently in each field

Why competition changes the landscape over time

How poker’s concept of +EV decisions maps to investing

Why risk and uncertainty aren’t the same and why it matters

And finally, why horse betting may offer the richest analogy for investors

Whether you're just getting started in investing or you've been at it for years, understanding how probabilistic thinkers in other fields manage decisions, edge, and emotion can dramatically sharpen your own process.

Part I: The Nature of Probabilistic Disciplines

At the core of investing, poker, and horse betting lies one uncomfortable truth: you can do everything right and still lose.

That’s because these are probabilistic disciplines, not deterministic ones.

The outcomes – at least over smaller sample sizes – aren’t guaranteed, no matter how good your decision-making process is. And for many people, especially those new to investing, that’s a hard pill to swallow.

Let’s define what that actually means.

What Makes a Discipline Probabilistic?

In a deterministic world, A leads to B. If I turn the key in my car’s ignition (and nothing’s broken), the engine starts. Every time. No uncertainty, no randomness.

In contrast, probabilistic environments are governed by chance, variability, and incomplete information. You can stack the odds in your favor, but there’s still a roll of the dice.

You make decisions based on what’s likely, not what’s certain.

Here’s how that plays out in our three domains:

In investing, you may have a strong thesis about a company’s future cash flows, a solid margin of safety, and a compelling valuation, but the stock still drops because of macro headwinds or a black swan event you couldn’t predict.

In poker, you might get all your chips in as a 91% favorite and still lose the pot; because the 9% outcome happens.

In horse betting, your analysis might be spot on, but an unexpected stumble at the gate or a brilliant ride from a competitor’s jockey turns your high-probability pick into a second-place finisher.

The implication here is profound: results in the short term are not reliable indicators of skill. You can win with a bad process and lose with a good one. That messiness is part of what makes probabilistic domains so difficult … and so fascinating!

It’s also why many participants in these fields fall into a dangerous trap: outcome bias.

They evaluate decisions based on what happened, rather than what was likely to happen at the time.

In poker, that leads to “tilt.”

In investing, it leads to abandoning a strategy right before it pays off, or doubling down on a lucky win that had no foundation.

The antidote is thinking in expected value.

Thinking in Expected Value (EV)

In both poker and investing, I try to evaluate decisions through the lens of expected value (EV), not outcome.

EV = (Probability of Outcome A × Payoff of Outcome A) + (Probability of Outcome B × Payoff of Outcome B) + ...

You will never know the exact probabilities in investing the way you do in poker, but the mindset still applies. If you’re making decisions where the expected value is positive, and you repeat those decisions often enough, you’ll come out ahead in the long run.

This is what separates professionals from amateurs in all three fields. Professionals understand that a single outcome doesn’t define the quality of a decision. It’s the underlying process – the logic, the discipline, the reasoning – that determines whether you’re playing a winning game.

Embracing the Noise

The hardest part about probabilistic disciplines is learning to live with the noise. Especially when money is on the line, it’s emotionally painful to watch a good bet go south. It’s tempting to second-guess yourself, abandon your framework, or seek false certainty where none exists.

But here’s the truth: in investing, poker, and horse betting, the goal is not to be right all the time. The goal is to be right enough, often enough, with a large enough edge, over a large enough sample size, to come out ahead.

In other words, you need to think like a statistician, not a fortune teller.

Part II: Understanding Variance and the Role of Sample Size

If you’ve ever lost money on a well-researched investment or had a great poker hand cracked by a miracle river card, you’ve felt the sting of variance.

And if you reacted emotionally – blaming yourself, changing your process, or swearing off the game altogether – you’re not alone.

Variance messes with our heads.

But understanding it is absolutely critical to surviving in probabilistic domains.

What Is Variance, Really?

Variance is the statistical concept that measures the spread between expected outcomes and actual outcomes. In simpler terms: it’s how much “noise” surrounds your signal.

In poker, you might make the same +EV decision a hundred times and see wildly different results each time. You could win 10 times in a row or lose 20 times straight. That’s not a reflection of your skill; it’s just how probability works.

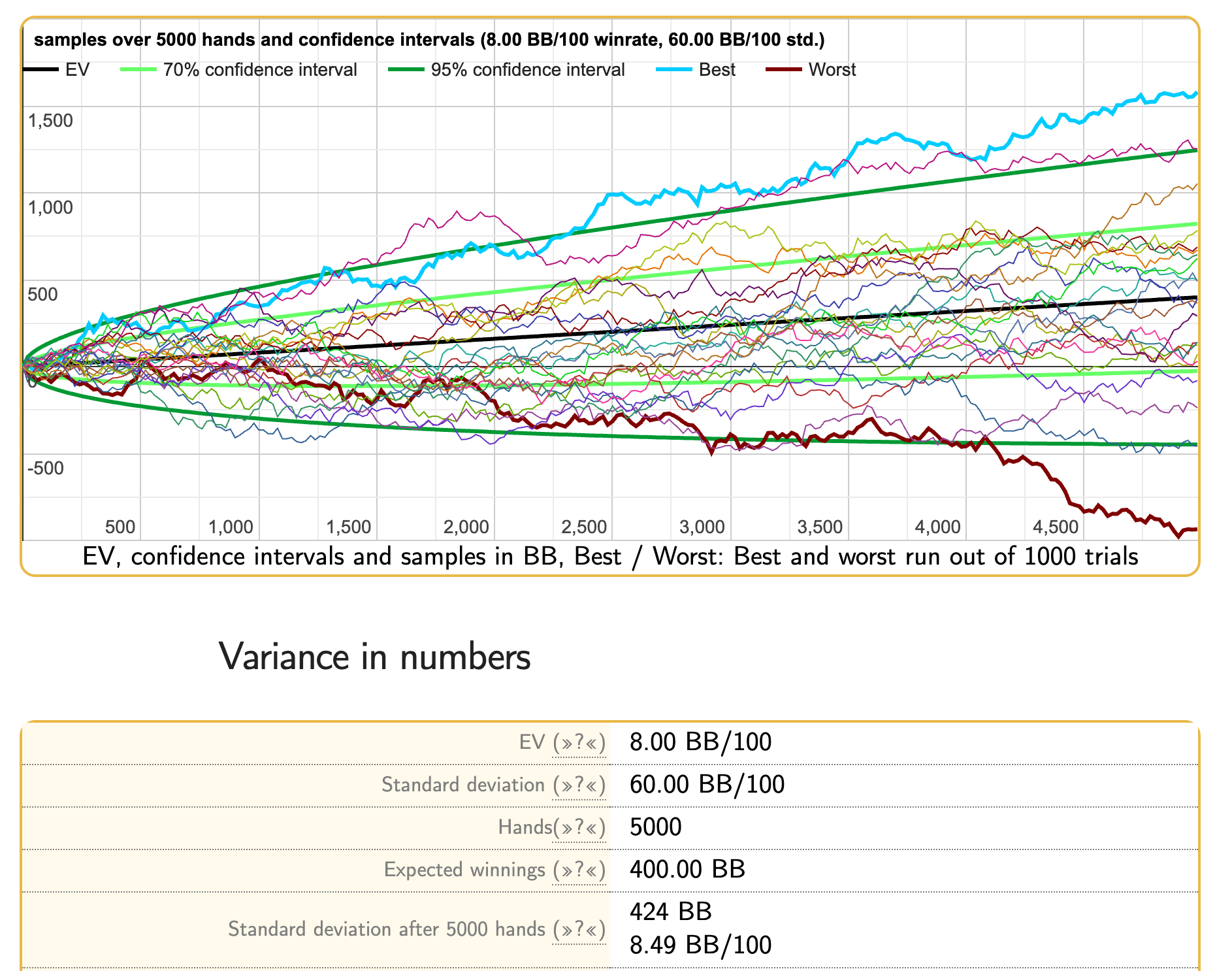

Take the example below: It shows a range of possible outcomes for a poker player who beats the game by 8 big bets over 100 hands and who plays 5,000 hands. His expected value is 400 big bets (8*5,000), but as you can see he will also lose money in various scenarios.

In investing, you can buy high-quality businesses at attractive valuations and still see negative returns for months, or even years, due to market sentiment, macro shocks, sector rotation, or most importantly, the businesses do not develop the way you anticipated (for whatever reason! – e.g. unlikely regulatory changes). Again, not a reflection of your process. Just variance doing what variance does.

Poker’s Hierarchy of Variance

Poker offers a perfect laboratory for studying variance, especially when you compare its different formats:

Limit Hold’em: Relatively low variance. Betting is capped, so pots are smaller and the swings more manageable.

No-Limit Hold’em: Higher variance. One mistake (or one cooler) can cost your whole stack.

Pot-Limit Omaha (PLO): Even higher variance. More starting cards, more drawing potential, and more action mean that even strong hands are rarely more than 60-65% favorites.

PLO players, in particular, understand that their edge plays out over massive sample sizes. You can be an elite player and go on brutal downswings simply because the standard deviation is so high. Consider the same inputs we used before, but we increase the standard deviation from 60 to 160 to account for the variance in PLO. This time, a player who should expect to win 400BBs over 5,000 hands may end up losing 3,000BBs!

That’s why pros often talk about needing hundreds of thousands of hands to confirm an edge.

The 50,000-Hand Challenge: Tom Dwan and the Reality of Long-Term Skill

During the online poker boom of the late 2000s, few players captured the imagination of the community like Tom Dwan, better known as “durrrr.”

(Image source: Wikipedia)

A fearless, aggressive high-stakes phenom, Dwan famously issued a public challenge: he would play anyone heads-up over 50,000 hands of online No-Limit Hold’em and give them 3-to-1 odds on a $500,000 side bet. In other words, if his opponent finished ahead after 50,000 hands, they’d win $1.5 million on top of their poker winnings.

The purpose of the challenge wasn’t just to stir up action – it was a live demonstration of variance vs. edge. Dwan believed that over a large enough sample size, his skill would prove itself. While you could beat him over a week or even a month of play, 50,000 hands was long enough to remove most of the noise and surface the signal.

Fwiw: Dwan started this challenge twice, but didn’t complete either.

Dwan also took this concept into the live arena. In November 2009, he played a series of three high-stakes live heads-up matches in London, each with a $250,000 buy-in at $500/$1,000 stakes:

In Match 1, Marcello "luckexpress" Marigliano finished up $22,500.

In Match 2, Dwan beat Ilari "Ziigmund" Sahamies, finishing up $68,000 after 12 hours of play.

In Match 3, Dwan crushed Sammy "Any Two" George, taking down a staggering $750,000.

He ended the live series with $795,500 in profit, winning two out of three matches.

Then came Part 2 of the original online challenge in 2010: a showdown with Dan “Jungleman” Cates, one of the sharpest young players of that era. Cates quickly took a commanding lead, up more than $1 million after just under 20,000 hands at $200/$400 stakes (that’s 2,500BBs, which equals a winrate of $5,000 per 100 hands, or a winrate of 12.5BBs/100 hands, which again seems high and shows that Jungleman certainly “ran good” over this sample size).

And then… the match stalled.

Allegedly, Dwan became increasingly difficult to reach. Despite efforts to resume the challenge, by 2013 only another 1,500 hands had been played; with Cates winning an additional $200,000. As of 2021, the challenge still hasn’t been completed, and Doug Polk even called it “the biggest scam in poker history.”

But the lesson still holds: these matches weren’t about who could win on any given day – they were about who had a real edge that could survive thousands of iterations. Because in a high-variance environment like poker—or investing—only large sample sizes reveal true skill.

Now Let’s Bring That Back to Investing

Here’s the challenge: in investing, you don’t get 50,000 reps!

Most investors will only make a few hundred truly meaningful decisions in their lifetime. Maybe a thousand if you’re extremely active. That’s it. And only a handful of all of these decisions may actually matter!

During a recent presentation at The University of Nebraska, Mohnish Pabrai shared how he believes Warren Buffett actually only made twelve (!) truly great investing decisions that mattered.

That limitation makes variance even more insidious. A poor outcome on a single stock could dominate your returns for a year or more. A lucky break could make you look like a genius.

But in truth, neither tells you much about your skill level unless you look at a long trail of decisions (for most investors that would be a decade or more) – and even then, context matters.

Take Cathie Wood, for example: her flagship fund ARKK outperformed the S&P for 7 years! Personally, I don’t believe that this outperformance was based on sound decision-making processes.

This is one reason I’ve always been cautious about performance-based narratives. “This stock doubled, therefore I’m smart” is one of the most dangerous traps in investing.

Much like in poker, you can’t judge the quality of a decision based solely on the outcome.

Part III: The Misunderstood Role of Luck

Luck has a bad reputation. It’s uncomfortable to acknowledge how much it affects our outcomes, especially in areas where we like to believe skill is king.

But whether we’re talking about investing, poker, or horse betting, luck is always in the room.

The only question is how much influence it has, and over what time frame.

Why We Downplay Luck

There’s a strong psychological drive to believe that we’re in control. When things go well, we attribute it to skill, foresight, and hard work. When things go poorly, we look for external factors or blame ourselves in ways that often aren’t productive.

In investing, this manifests as the classic trap: “I’m up, therefore I’m smart.” The markets hand out rewards that often look like signals but are really just noise. And if you don't distinguish between the two, you risk anchoring your confidence to outcomes that had more to do with timing or sentiment than skill.

Poker players deal with the same delusion. A recreational player might go on a heater and think they’ve cracked the code—until variance humbles them. In both fields, luck can mimic skill for frighteningly long stretches.

In poker, there are actually tools that track all of your hands and allow you to compare your actual performance to the “expected value performance” based on your decision-making. You cannot do that in investing.

Success = Luck × Opportunity

One mental model I find helpful is the idea that:

Success = Luck × Opportunity

You can’t control your luck but you can control your positioning.

You can seek out asymmetric opportunities.

You can work to be ready when opportunity arises.

And you can manage your downside so that bad luck doesn’t take you out of the game (position sizing!).

Think of it this way:

Opportunity is how often and how big your edge is.

Luck is the variance around the outcome of that edge.

You can’t remove luck from the equation but you can stack the odds in your favor and be in position when favorable variance hits.

The Chris Moneymaker Effect & What Happens When Competition Tightens

Let’s take a step back to the poker boom of the early 2000s. In 2003, Chris Moneymaker, an amateur who won a $39 online satellite tournament, went on to win the World Series of Poker Main Event. The story had everything: underdog narrative, massive prize, and a catchy last name that sounded made for headlines.

After that, poker exploded.

Everyone and their mother jumped online to try their luck. And for a while, you didn’t have to be that good to win. If you had a basic understanding of odds, positional play, and didn’t tilt too hard, you could grind out profits.

This was a unique moment: a wide-open field, low average skill level, and huge inflow of inexperienced money. Opportunity was everywhere. You didn’t need to be elite – you just needed to “not suck.”

But fast-forward to the 2010s and beyond, and things changed. The average player got much better. Solvers and coaching tools emerged. HUDs (Heads-Up Displays) tracked every stat imaginable. The edges shrank, and the rake (the fee taken by the casino) stayed the same or increased.

Today, even at low stakes, only a small percentage of players beat the game over the long run. Why? Because the edge just isn’t there anymore – at least not without putting in serious work and finding soft tables. Your skill might still be decent, but if everyone else leveled up, you’re back to break-even or worse.

This same principle applies to investing.

Competition Kills Easy Edges

Markets are adaptive systems. As more smart people enter a space and chase the same inefficiencies, those inefficiencies disappear. When everyone’s reading the same earnings transcripts, using the same valuation screens, and competing over the same popular stocks, the edge erodes. You might still be “right,” but you won’t be right enough to overcome trading costs, taxes, and opportunity cost, or you may simply not find opportunities that will deliver 20%+ compounded returns.

That’s why I’m always on the hunt for less crowded areas – underfollowed companies, strange geographies, neglected industries. That’s where the edge lives. Not because I’m guaranteed to be right, but because there’s less competition, and therefore a higher chance that mispricing still exists.

How Luck Shrinks With Sample Size

Here’s the kicker: luck never disappears, but its influence fades as your sample size grows. Over 10 trades, you might get lucky. Over 100, maybe. Over 1,000, your process starts to show. Over 10,000, luck is still there—but now it’s riding in the passenger seat, not driving the car.

Here’s another poker-related EV chart: We’re looking at the same 8BB winrate poker player, but we increased the sample size from 5,000 hands to 10,000 hands (standard deviation of 60):

This is why professionals, whether savvy investors or professional poker players, don’t just think in terms of wins or losses. They think in terms of long-term expected value and repeatable edges.

You can beat a world-class poker pro over 100 hands. Maybe even 1,000. But over 50,000 hands, your luck will run out if your edge isn’t real.

In investing, your sample size is lower, but the lesson holds: luck may swing things in the short run, but over time, edge + discipline is what separates good from great.

Investing has far more variables than poker, but the core idea still applies. We don’t get to know our opponent’s hand but we can still build mental models, think in probabilities, and weigh risk-reward tradeoffs.

I try to ask myself:

Was my thesis based on logical assumptions?

Did I size the position appropriately?

Did I account for the most important risks?

Did I give myself a margin of safety?

Was my variant perception justified?

If I can answer “yes” to most of those, I’m satisfied, even if the investment didn’t pan out. Because in a probabilistic environment, a good process will produce good outcomes over time, even if individual bets go against you.

What separates seasoned investors and poker players from the rest isn’t perfect foresight—it’s emotional detachment from short-term results. They’re not indifferent to outcomes, but they know that judging themselves on every win or loss is a fast track to madness.

Instead, they focus on:

Making consistently good decisions

Managing risk

Staying rational under pressure

Reflecting honestly on their thinking – not just what happened

In other words, they build robust decision-making systems that are designed to handle the uncertainty and noise that are baked into these environments.

Part IV: Risk vs. Uncertainty – The Critical Distinction

If there’s one mental model that’s been truly transformative for my investing framework, it’s the distinction between risk and uncertainty. The terms are often used interchangeably, but in the context of probabilistic decision-making, they couldn’t be more different.

Understanding this distinction is what allows you to realize why poker, horse betting, and investing each operate on different levels of predictability – and why investing, in particular, is so challenging to model.

Risk Is Quantifiable. Uncertainty Is Not.

The economist Frank Knight was one of the first to make this explicit distinction back in the 1920s:

Risk refers to situations where you know the possible outcomes and their probabilities. It’s measurable. It’s modelable.

Uncertainty refers to situations where you don’t know all the possible outcomes, and you certainly can’t assign reliable probabilities to them.

On top of this, you may highlight that one can distinguish between known unknowns and unknown unknowns.

Put bluntly:

Risk is roulette. Uncertainty is life.

Poker: A Risk-Dominant Game

Poker is mostly a risk-dominant game. The number of possible hands is finite. The rules are fixed. With enough experience, you can become extraordinarily good at estimating the likelihood that your opponent has a certain range of hands. That’s why advanced players talk in hand ranges, not individual hands. And you can model the expected value of your decisions against a determined range.

You’ll often hear someone say something like:

“I put him on a range of TT+, AK, and AQ suited. Against that range, shoving here is +EV.”

This is a probabilistic calculation based on known variables. Skill in poker means understanding those ranges, recognizing betting patterns, and estimating how your hand performs against that distribution.

Even when you're unsure of your opponent’s exact cards, the boundaries of the game allow you to make reasonably accurate estimates.

Yes, variance exists. Yes, luck plays a role. But the playing field is well-defined, and over time, skill prevails.

Investing: A Playground of Uncertainty

Investing, by contrast, is filled with unknowable unknowns. Businesses don’t operate in a closed system like a poker table. They exist in the real world, a chaotic, adaptive, nonlinear ecosystem of human behavior, technological change, regulation, geopolitics, and macroeconomics.

You don’t know:

What the competition will do in two years

What new regulation might appear

Whether a founder will leave or have an accident

How interest rates will evolve

Whether a once-in-a-century pandemic will hit

Or whether, and that’s my most favorite example taken from a Joel Greenblatt lecture, the HQ of a company will disappear due to a sinkhole!

“Well, the interesting thing, a Harcourt Brace Jovanovich, which was a publisher, but also owned amusement parks in Florida, believe it or not, went to buy a very small company called Florida Cypress Gardens, which I remembered as a kid going to, and they had water skiing Santa Claus, during Christmas time, and all kinds of water shows and beautiful gardens. It was a very unique, interesting, and very memorable place to visit when you’re five or six years old.

When I saw they were getting taken over, and this was literally in the first month I went into business for myself. I was pretty nervous. I was 27 and I had gotten money from a very famous guy and I want to do a good job. I saw this opportunity where Florida Cypress Gardens was being taken over, and there was a nice spread in that deal where I could make a lot of money if it went through. I thought the deal made a lot of sense at the time. I was able to have a big smile on my face and buy Florida Cypress Gardens as one of the first investments I made when I went out on my own.

A few weeks before the deal was supposed to close, unfortunately, Florida Cypress Gardens fell into what’s called a sinkhole, meaning the main pavilions of Florida Cypress Gardens literally fell into a hole that appeared out of nowhere. Apparently that happens a lot in Florida, I wasn’t that familiar with it, and thank God I wasn’t at Florida Cypress Gardens when it happened, but the Wall Street Journal wrote a real humorous story about it. I was like, “Why is this funny? I’m about to lose my business. I had taken a pretty decent sized bet in the deal.”

It just tells you, things can happen that you don’t anticipate, that it’s not really your fault. I’d never even heard of a sinkhole before I read about this happening, so it’s a risk that I… When you’re doing a merger deal, you’re not really saying risk of sinkhole is in your checklist of things to look for, so stuff happens, less kind words for that. It’s a good lesson to learn, especially out of the box. I was sweating pretty good. They ended up re-cutting the deal at a lower price and I lost money, but not that terrible.“

You can make educated guesses. You can study patterns. You can assign broad scenario probabilities. But ultimately, you’re dealing with uncertainty, not risk.

And because of that, models built on perfect-looking spreadsheets are often exercises in false precision.

You can tweak a DCF until the output tells you what you want to hear (“to a man with a hammer, everything looks like a nail”), but that doesn’t make the future more knowable.

Black Swans and the Fat Tails of Reality

This brings us to Black Swan events, a concept popularized by Nassim Taleb. These are high-impact, hard-to-predict, and rare events that lie outside the realm of regular expectations. They matter disproportionately, and yet they’re almost impossible to forecast with traditional tools.

Poker doesn’t have Black Swans. The cards are fixed. The probabilities are bounded.

Investing is full of them.

Consider:

The collapse of Lehman Brothers

COVID-19’s market impact

The sudden rise of generative AI

Regulatory whiplash in Chinese tech stocks

These are events that fundamentally change the game and often invalidate your priors.

As an investor, you have to build a process that is robust to uncertainty, not just optimized for risk; and usually this involves buying cheap.

The Danger of Overmodeling

A classic mistake I see in investing circles is to overmodel risk while ignoring uncertainty. We build intricate models with dozens of assumptions, pretending we can know the unknowable. But as Howard Marks put it:

“You can’t predict. You can prepare.”

That’s why I’ve grown increasingly skeptical of hyper-detailed financial modeling. It gives the illusion of control, but it often fails to account for the wildcard events that drive real-world outcomes (also on the upside!).

Instead, I try to think in broad scenarios:

What could go right? (are “free call options” maybe not embedded in the price?)

What could go wrong?

How sensitive is my thesis to changes in key variables?

What are the second- and third-order effects?

This approach doesn’t eliminate uncertainty … but it respects it.

Investing Is an Adaptive Game

Another wrinkle: unlike poker, investing is a game where the rules change, the players evolve, and your strategy has to adapt constantly. There is no fixed deck. There is no “solved” approach. The market is a living organism, part rational, part emotional, and it punishes rigidity.

In poker, if your strategy is winning, you just keep running it mostly (one exception would maybe be a heads-up match with another player for 100,000 hands where you constantly need to adapt to possible exploitations by your opponent).

In investing, if too many people adopt the same strategy, the edge disappears. That’s why so many quantitative edges – momentum, value, small cap premiums – fade over time.

This makes investing not only uncertain, but reflexive. As George Soros noted, the act of participating changes the game.

Part V: Why Investing Is Not Poker (But Horse Betting Might Be Closer)

Given everything we’ve explored – variance, sample size, the role of luck, and especially the distinction between risk and uncertainty – it becomes clear that investing and poker, while sharing many surface-level similarities, are fundamentally different games.

And ironically, the better analogy for investing might just be found at the racetrack.

That may sound strange at first. After all, poker is a game of decision-making under uncertainty, betting odds, reading opponents, and managing risk; just like investing.

But there are a few critical distinctions that make horse betting a more useful mental model for long-term investors.

Let me explain why:

1. Sample Size and Repetition

As discussed earlier, poker offers something investing can’t: volume. A professional poker player can play tens of thousands – sometimes hundreds of thousands – of hands in a year. They get feedback on their edge quickly. They can iterate and adjust.

In investing, your lifetime sample size is small. Even a highly active investor might only make a few hundred serious bets in their career. More focused, long-term investors might only make a few dozen. That makes outcome randomness even harder to smooth out.

This limited sample size reduces the power of mathematical tools like the Kelly Criterion for instance – something even investors like Mohnish Pabrai have acknowledged. The Kelly formula assumes repeatable, independent bets and clearly defined probabilities. In the messiness of investing, those assumptions break down.

That’s where horse betting comes in.

2. Horse Racing Is a Game of Expectations vs. Reality

When you bet on a horse, you’re not just guessing who will win. You’re comparing your estimated probability of that horse winning against the market’s implied odds.

If a horse has 10-to-1 odds, the market thinks it has about a 9% chance of winning. If your analysis suggests the real probability is closer to 15%, you have an edge, even if the horse doesn’t win that particular race.

Sound familiar?

That’s essentially what we do in investing:

A stock trades at a valuation that implies a certain level of growth, profitability, or stability.

If our analysis suggests the company will outperform those expectations, we have a variant perception.

And if we’re right over time, that mispricing will correct and we’ll earn an excess return.

This dynamic (expectations vs. reality) is the heart of both horse betting and successful investing.

3. Horses as Businesses: The Analogy Deepens

Each horse is like a company. It has underlying fundamentals that determine its performance. For horses, those might include:

Recent form = earnings trend and business momentum

Top speed = efficiency and competitive advantage

The trainer = CEO or management team

The track conditions = macroeconomic environment

The draw (gate position) = industry dynamics or regulatory setup

The jockey = execution skill, capital allocation

The horse’s age and history = business maturity, product lifecycle

Injury record or recovery = prior business crises or turnarounds

Just like in horse racing, no single factor determines the outcome. You’re analyzing a complex mix of attributes to make a judgment call. Then you compare that call to what the market believes (i.e., the betting odds or current stock price).

If your estimate of the horse – or the business – is materially better than what’s implied by the price, and you’ve accounted for the risks, you place your bet.

4. The Role of the Crowd

In horse betting, like in markets, the odds reflect the crowd’s belief. The more efficient the betting market, the harder it is to find mispriced horses.

In a tiny local race with only a few bettors, the odds might be all over the place, giving you a better shot at finding edge. But in the Kentucky Derby, with millions of dollars wagered by pros, sharps, and algorithms, your edge is likely gone.

The same logic applies to investing:

Microcaps, obscure foreign equities, or unloved sectors = small track with amateur bettors

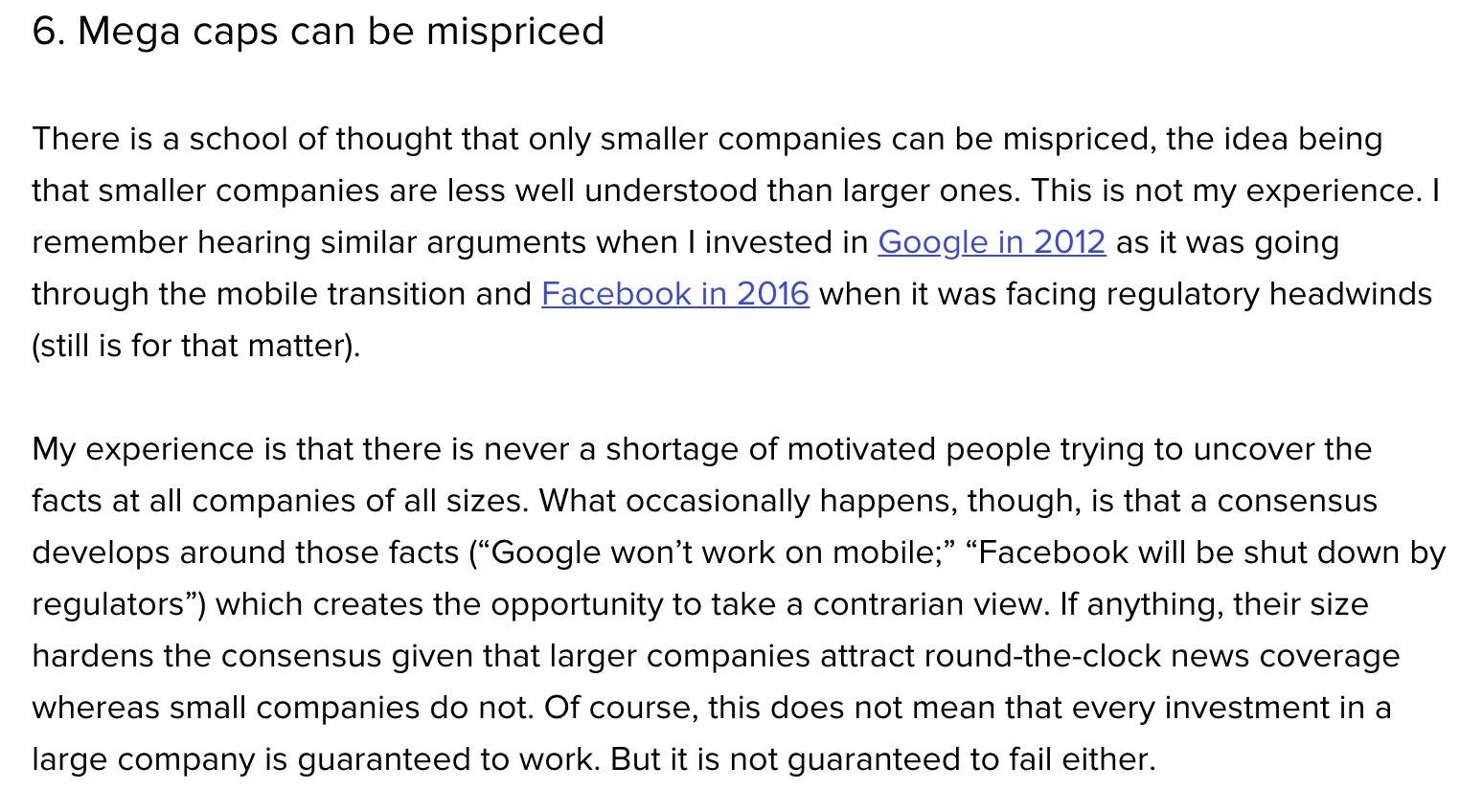

Mega-cap tech stocks followed by 30 analysts = the Kentucky Derby

Where do you think you’re more likely to find mispricing? That doesn’t mean there are no mispricings in mega-caps, but they are rarer.

(Source: A Robert Vinall shareholder letter)

5. Betting Against the Odds – Not the Outcome

The beauty of both horse betting and investing is that you don’t need to be right often. You just need to be right when the odds are wrong.

You can be wrong most of the time and still win, if your wins are big and your losses are small. This is why I care more about asymmetric payoffs than win rate. I want to find situations where:

The downside is limited (margin of safety)

The upside is mispriced

My perception of reality is different from the market’s … and more accurate

Closing Thoughts: Thinking Like a Probabilistic Decision-Maker

To be clear: poker teaches incredible lessons about probability, discipline, edge, and emotional control. It’s a fantastic training ground. But when it comes to building a mental model for long-term investing, I think horse betting better captures the dynamic between intrinsic attributes and market expectations.

It acknowledges that:

Your analysis is inherently flawed and partial

You’re betting against a market, not just on an outcome

The key is edge, not certainty

That’s the mindset I bring to markets.

If there’s one thing I hope you take away from this entire post, it’s this: great investing isn't about being certain… it's about being directionally right in a world full of uncertainty.

That’s what links investing, poker, and horse betting at their core. They are all disciplines where the right decisions don’t always lead to the right outcomes, and the wrong decisions sometimes get rewarded. They require you to operate in environments where luck, variance, and competition blur the connection between cause and effect.

The Edge Is in Your Thinking, Not Your Forecast

You don’t need to predict the future to be a great investor. You just need to:

Make decisions with positive expected value

Avoid situations where the downside overwhelms the upside

Stick to a process that tilts the odds in your favor, even when results don’t cooperate

The best poker players don’t win every hand – they fold most of them.

The best horse bettors don’t bet every race– they wait for mispriced opportunities.

The best investors don’t buy everything – they hunt for edge where expectations are wrong and the payoff justifies the risk.

One of the biggest differences between gambling and investing is that in investing, you don’t have to bet every day. You can wait patiently. You can say “no” 99 times and “yes” once—if that “yes” is a high-quality bet, it can carry your entire year.

That’s why temperament matters more than intelligence. If you chase outcomes, get impatient, or overreact to short-term variance, you’ll erode your edge over time.

But if you think in long arcs – if you understand that variance is inevitable, that luck never fully goes away, and that your competition is constantly evolving – you can build a sustainable edge over time.

Recapping the Mental Models

Let’s bring it full circle. Here are the core mental models we explored throughout this post:

Probabilistic Thinking: All three domains are governed by odds, not certainties.

Variance: Good and bad outcomes can both be misleading in the short term.

Luck x Opportunity: Success often hinges on both, but you can position yourself to capitalize on luck when it arrives.

Process Over Outcome: Evaluate the decision, not just the result.

Risk vs. Uncertainty: In investing, most outcomes are unquantifiable. Prepare, don’t predict.

We all want certainty. We want to believe there’s a secret formula, a guru with the answers, a backtested strategy that will work forever. But in a probabilistic world, those things don’t exist. What does exist is process, patience, and perspective.

Whether you’re at the poker table, placing a bet at the track, or allocating capital in the market, the principle remains the same:

Make the best possible decision with the information you have, manage your downside, respect uncertainty, and let time do the heavy lifting.

If you can internalize that mindset, you’ll already be ahead of most of the field.

Family, Passion, and Generational Wealth

What if you could invest in a way that secures your family’s future while freeing up time for what you love most? My Mental Models Investing Mentoring program teaches successful professionals and entrepreneurs like you a proven framework to build generational wealth through super high-quality stocks. This isn’t about chasing tips—it’s about mastering a system that delivers results, so you can step away from the grind and focus on your passions. Ready to make your highest-ROI investment? Click here to join me at MentalModelsMentoring.com.