Microsoft, Apple, and Nvidia combined have crossed the USD 10 trillion mark!

Arguably, this milestone has significant implications for investors and the broader market. Hence, today I’m going to delve into what this means, provide numbers and context, and explore why comparing these companies' market caps to the GDP of entire nations can be misleading.

Finally, I'll also examine the basket's PE ratio and share some final thoughts on the sustainability of their current valuations.

Looking at the Numbers!

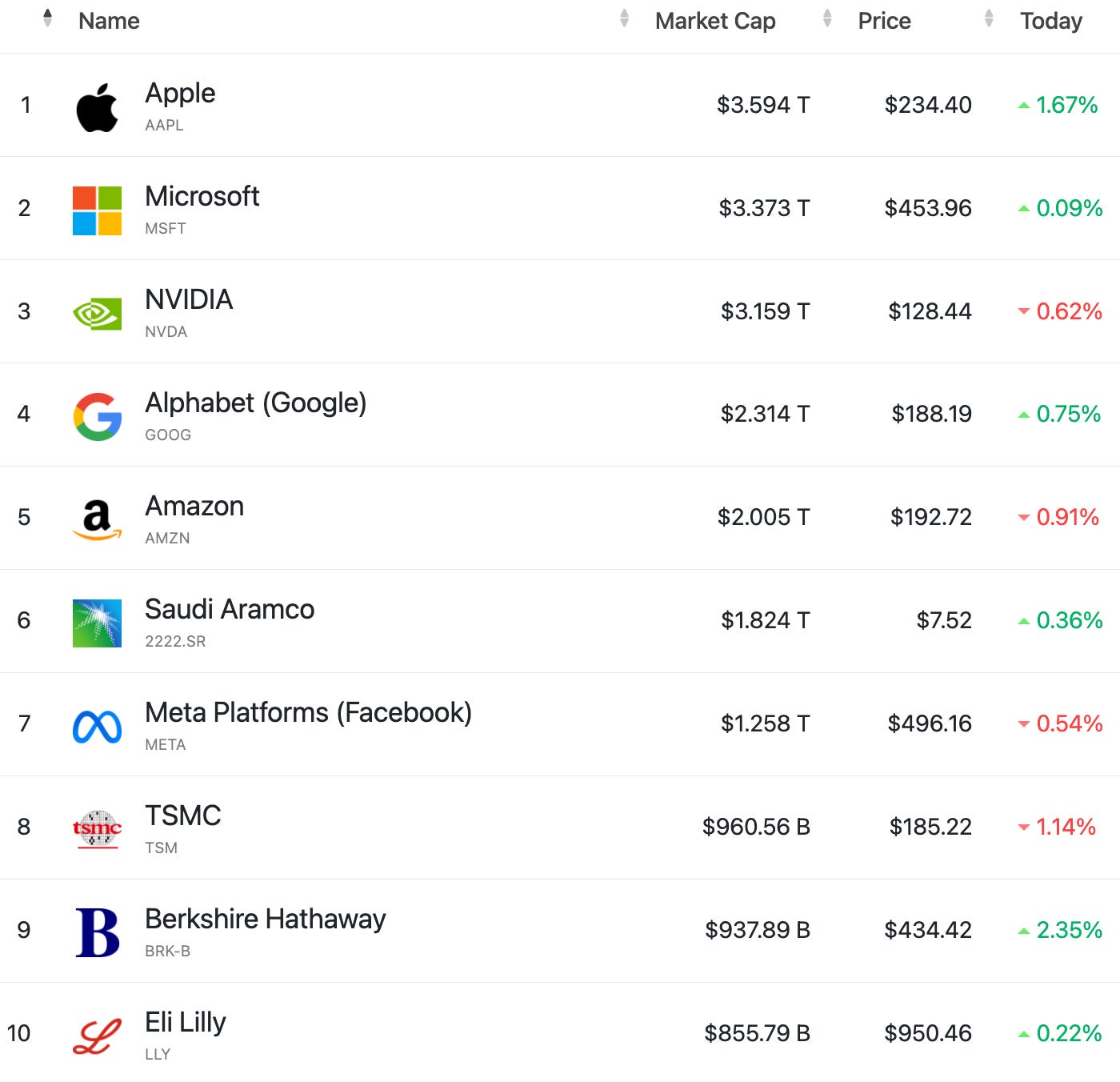

The three most valuable publicly traded companies currently are:

Apple: $3.594 Trillion

Microsoft: $3.373 Trillion

Nvidia: $3.159 Trillion

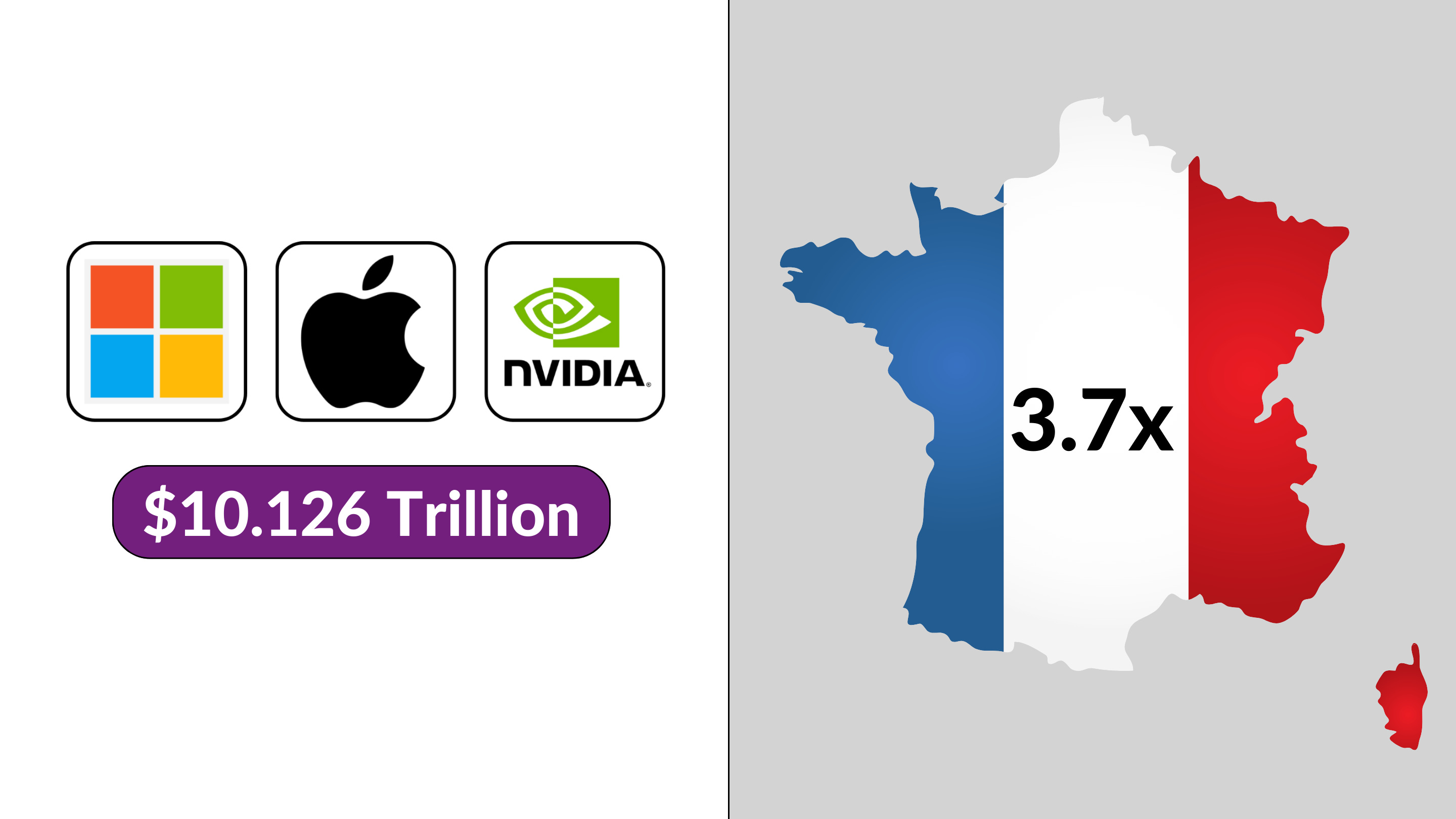

Combined, these tech giants boast a market capitalization of $10.126 trillion. To put this staggering number into perspective, …

… it represents nearly 22% of the entire S&P 500’s market cap:

Additionally, this sum is approximately 3.7 times the GDP of France, the second-largest economy in the European Union …

… and more than 2.5 times the GDP of Germany, the EU's largest economy. Put differently, these three companies are worth as much as 2.5x times the value of ALL goods and services produced by the German economy over a 1-year period.

The Misleading Nature of GDP Comparisons

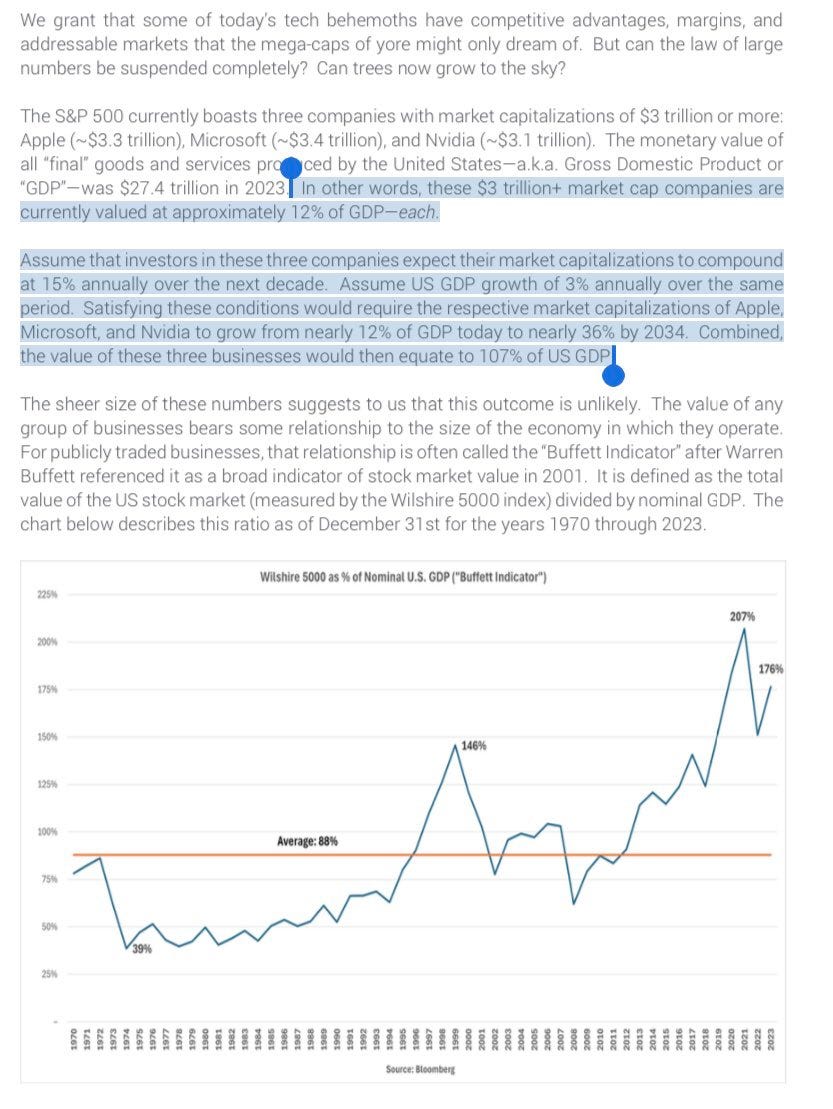

If you follow financial media, you will come across comparisons between stocks’ market capitalization and countries’ GDP all the time. And I myself am guilty of using such a comparison myself now.

And even investors who I look up to like John Neff from Akre Capital sometimes make use of this technique. @JRogrow shared the following excerpt from an investor letter for instance:

“Satisfying these conditions would require the respective market capitalizations of Apple, Microsoft, and Nvidia to grow from nearly 12% of GDP today to nearly 36% by 2034. Combined…would then equate to 107% of US GDP.”

However, I’d argue comparing the market cap of a stock to the GDP of a country is like comparing apples to oranges.

The market cap of a stock theoretically represents the present value of all future cash flows that the business will generate, discounted back to the present value.

This calculation encompasses cash flows over many years and decades.

On the other hand, GDP is a metric that focuses solely on the economic output of a country within a single calendar year. Thus, juxtaposing the two can be misleading and doesn’t provide a fair comparison of value in my opinion.

The Basket's PE Ratio

To assess whether the current valuations are sustainable, let's consider the earnings produced by these companies. For this analysis, we will stick to earnings rather than cash flows, as it offers a clearer picture.

Here are the NTM earnings estimates for the three companies:

Apple: $101B

Microsoft: $88B

Nvidia: $67.5B

Combining these figures gives us a total net profit of $257.3 billion, which translates to a NTM PE ratio of around 39x.

In simpler terms, this means that if Microsoft, Apple, and Nvidia were to distribute their entire earnings, it would take investors 39 years to recoup their investment, assuming no growth.

Of course, it is likely that all three companies will continue to grow. As an aside, Nvidia is probably the only company of the three where I have less confidence that the company will produce as much in profit in 2034 as it does today.

For the current price levels to be justified (assuming to demand a decent return), these companies need to sustain double-digit growth rates over a long period, despite their already massive size. Failure to do so could result in underperformance relative to the market.

Keep in mind that investors’ expected return equals the current (earnings) yield (2.5%) + (long-term) growth – assuming no changes in valuation. So to get a market-beating return, these companies need to deliver around 10% compounded growth over the next ten years (and make sure the multiple doesn’t compress). If Apple can grow its earnings at a rate of 10% a year over the next ten years, the Cupertino-based company will earn $261 billion in ten years.

My Thoughts

There’s no denying that we are looking at extremely high-quality companies here, but I have my doubts about whether their current prices are justified. The recent upward trend, with increases of 22%, 41%, and 221% over the last twelve months, is heavily influenced by the buzz around artificial intelligence (AI).

However, predicting the returns businesses in general will generate from AI investments is challenging.

As the CEO of Anthropic noted in a recent interview, the future impact of AI on businesses is uncertain:

I believe with regard to AI investors in Microsoft, Nvidia, or Apple must consider several critical questions when evaluating whether they want to hold onto these stocks (or invest at current levels):

To what extent does the success and growth of the business depend on AI?

How much revenue can AI potentially generate?

How will AI technology specifically alter their business models?

To what extent does AI expose the business to the risk of being disrupted?

Conclusion

In conclusion, while these companies are currently delivering strong quarterly results (with the exception of Apple), the sustainability of their valuation multiples is somewhat questionable.

Microsoft seems to have the most stable outlook, while Apple's sales have stagnated (or even declined) more recently, and Nvidia's future is the hardest to predict due to potential market saturation.

Investors should be cautious, as the current price development is not “normal”. The market’s enthusiasm for AI may be driving valuations beyond sustainable levels, and any loss in operating momentum could lead to significant declines.

Therefore, while I acknowledge the quality of these companies, I remain skeptical about their current valuations and am not a buyer at these levels (and I own none of the three companies as of today).

What do you think? Are you optimistic about the stock performance of Microsoft, Nvidia, or Apple?