Tencent Music Entertainment (Follow-Up): 4 More Developments That Matter!

What to Know About TME Right Now

A few days ago I put out a “Quick Pitch” on Tencent Music Entertainment. It was meant to be a starting point, not the final word, and the comments proved exactly why I love writing these in public. One reader in particular, Pitc2d, left a sharp note pointing to a handful of developments I’d skated past: the company’s ongoing share buyback, and the much larger story of the Ximalaya acquisition. Both deserved more than a footnote. So consider this the follow-up I owe him.

This post is where I go deeper on three more subjects related to TME.

I’ll spend most of my time on the Ximalaya deal, because the more I dug into it, the more I realized how big of a deal this may turn out to be. My first instinct was skepticism. Long-form audio looked, on paper, like a structurally worse business than music streaming, and I went in expecting to talk myself out of liking the acquisition. What I found instead was something more layered. I assess this acquisition from multiple angles.

Before that, I’ll pick up the thread Pitc2d started on the buyback, and untangle the gap between what TME has authorized and what it has actually spent.

And to close, a shorter flag. My friend Niklas raised a point about TME’s 2025 earnings that I think a lot of investors will miss on a first pass, the kind of thing that sits in a footnote, but shouldn’t be missed. I’ll keep that one brief, but I’d argue it’s as important for anyone building a valuation model as the Ximalaya deal. I also added another interesting recent development last-second (the fourth subject we discuss) – a tie-in into Tencent’s ecosystem.

Let’s get into it.

Disclaimer: As of the date of publication, the author owns no shares in the company; but that may change. The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

#1: $1 Billion Share Buyback Program

When a Chinese tech company announces a billion-dollar buyback, I’ve learned to do two things before getting excited. First, I read the fine print. Then I check whether they actually spend the money. With Tencent Music, both questions turn out to be more interesting than the headline suggests, and the gap between what was announced and what’s been executed says more about the company than the press release ever could.

Let me walk you through the details and my thoughts.

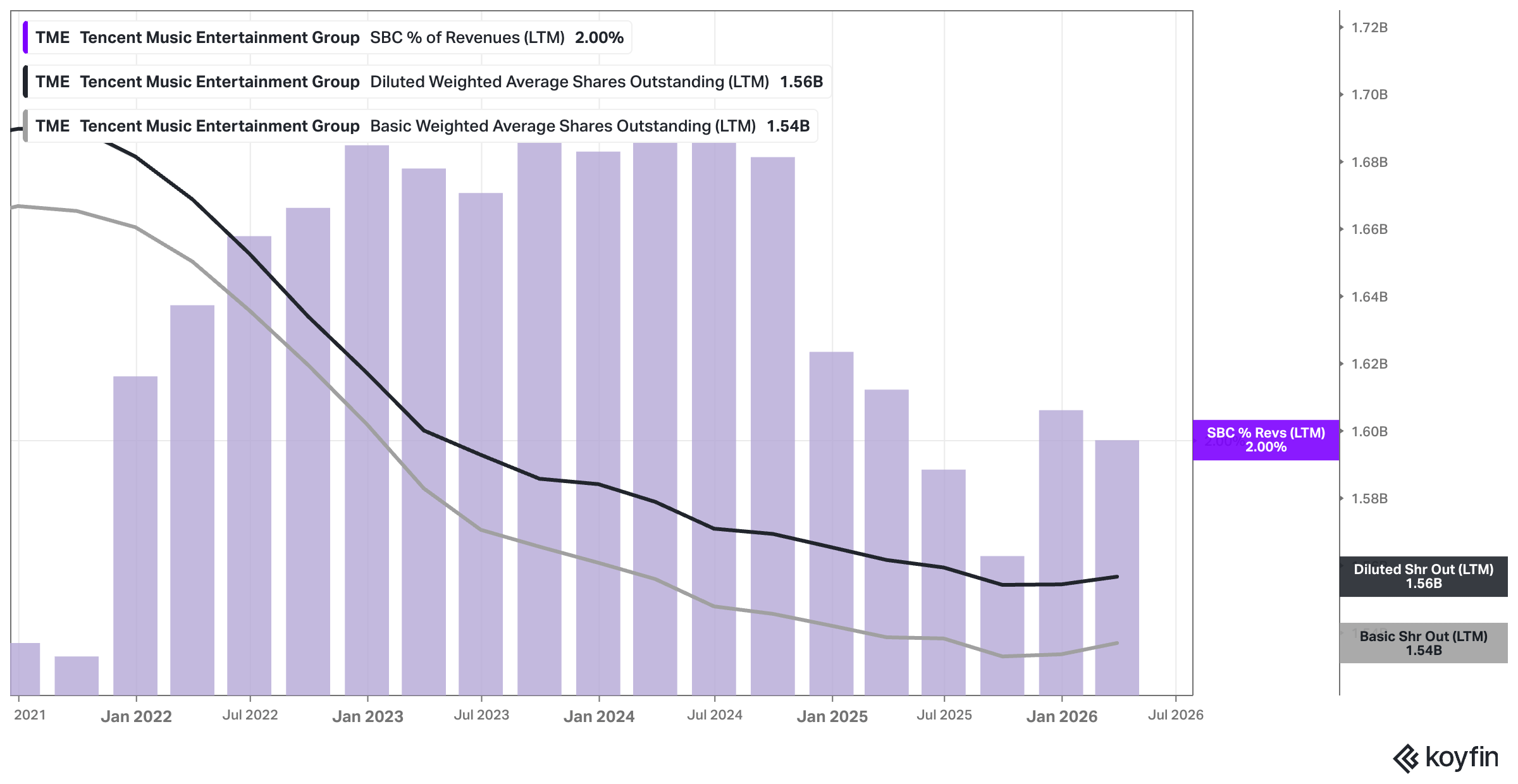

Let’s start with TME’s buyback history: Back in March 2021, in the middle of the brutal selloff in Chinese ADRs, TME’s board authorized a $1 billion repurchase over a twelve-month window. That one came and went. So did a $500 million program announced in March 2023. Over the last five years, TME’s share count is down around 8%.

The one that actually matters today was authorized alongside the Q4 2024 results: a fresh $1 billion authorization running over a 24-month period that began in March 2025. That puts the clock ticking toward roughly March 2027.

“The Company’s board of directors approved an annual cash dividend of approximately US$273 million for the year ended December 31, 2024, and authorized a new Share Repurchase Program up to US$1 billion during a 24-month period commencing from March 2025.”

A board authorization gives management permission to buy up to a dollar amount. It commits them to nothing. Companies announce these things constantly, especially when the stock has been beaten up, precisely because the announcement itself can prop up sentiment at zero immediate cash cost. The real tell however is execution.

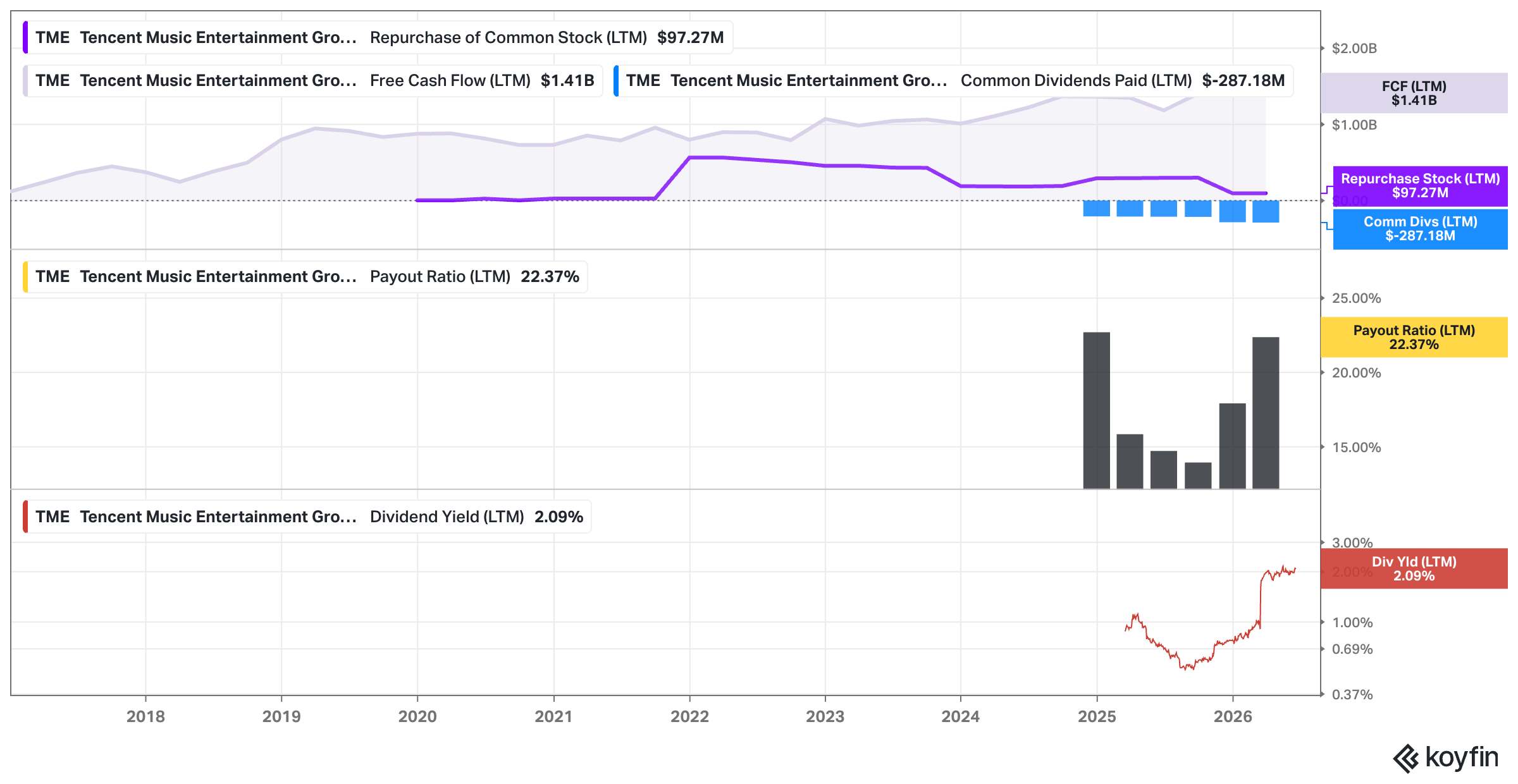

So what has TME actually done? In the first quarter of 2025, the company repurchased 5.9 million ADSs for roughly $64.5 million, at an average price of about $10.8 per ADS.

“Under our previously announced share repurchase programs, during the three months ended March 31, 2025, we repurchased a total of 5.9 million ADSs in the open market with cash for an aggregate consideration of approximately US$64.5 million at an average price of US$10.8 per ADS.“

Worth noting: that disclosure referenced “previously announced share repurchase programs” in the plural, so some of that spend may have closed out the tail of the older $500 million program rather than the new one.

After that, TME stopped breaking out quarterly buyback dollars in its non-SEC PRs/earnings releases. You can still triangulate. For full-year 2025, net cash used in financing activities came to about $665 million. That bucket includes the dividend plus repurchases of roughly $57 million; which is just a drop in the bucket compared to the size of the authorized program.

As a result, weighted-average basic ADS barely budged, drifting from about 1,542 million in 2024 to roughly 1,534 million in 2025. That’s a net reduction of only around eight million ADSs. Eight million. On a base north of 1.5 billion. For a company brandishing a billion-dollar authorization, that is a remarkably small dent.

So is it actually accretive?

But then again, during the Q1 call, management said that it intends to actually complete the program.

“… as part of our long-term commitment to shareholder returns, we plan to complete the 2-year stock repurchase program that we announced in March 2025 on time.“

So if we assume the $1 billion program will be executed and that the majority of the “buyback dry powder” hasn’t been used, let’s run the numbers to determine how accretive it might be at the current valuation.

If TME deployed a full $1 billion at recent prices around the $9 mark, you’d retire on the order of 110 million ADSs ($1B ÷ $8.70 share price = ~114.9 million shares), give or take depending on where the stock trades during execution.

Against roughly 1.53 billion ADSs outstanding, that’s a reduction of about 7.5 percent, which translates into an EPS lift in the neighborhood of 7 to 8 percent if net income holds flat. 7-8 percent in EPS growth without requiring any topline growth; that’s far from trivial for a profitable, cash-generative business trading at a dirt-cheap valuation.

Of course, there is some dilution from SBC, and there’s not a full $1 billion left, and the Ximalaya deal (to be discussed next) will also have a dilutive effect, but still, I think this program is very much noteworthy and should be highly value accretive at the current share price.

“Q: And partly relating to that what’s management latest thought on the share repurchase program, we noticed that there’s still a large quota left?

A: Well, we’re still communicating with the regulator on the Ximalaya deal. If there is any update, we will disclose at that point.“ - Q4 Call

The most attractive moment to retire stock is when it’s cheap. TME spent part of early 2025 buying around $10.8 per ADS; the stock has since spent stretches trading below that. If management leans into the program while shares are depressed rather than mechanically spreading purchases evenly, the per-dollar value created climbs. Buybacks executed into weakness are worth far more than buybacks executed into strength.

#2: The Ear Economy – TME Paid Billions for Ximalaya & Whether It’s Worth It

This is where it gets interesting

Become a paying subscriber to read the rest of this post and get access to all of my other research, including valuation spreadsheets, deep dives (e.g. well-known mid- and large caps such as LVMH, Duolingo, Meta, Edenred as well as more hidden gems such as Tiger Brokers, Digital Ocean, Ashtead Technologies, InPost, Timee, and MANY more), and powerful investing frameworks.

As a member, you get:

Complete Access: Every deep dive in our library (65+ and counting).

The WhatsApp Community: Real-time discussion and networking with like-minded investors.

Digital Investing Conferences: Around three times a year, we also hold digital conferences where members present and share stock ideas, and discuss broader themes, and we’d love for you to join in!

Incredible Value: Full access to all of this for less than $1/day.

PS: Using the app on iOS? Apple doesn’t allow in-app subscriptions without a big fee. To keep things fair and pay a lower subscription price, I recommend just heading to the site in your browser (desktop or mobile) to subscribe.