Symbolic Penalties and Maximum Fear: Why I Am Not Selling My Tiger Brokers Shares

When Fear Decouples from Fundamentals

Those who have followed my portfolio for a while might know that I am invested in Tiger Brokers.

Last Friday, after another regulatory crackdown that seemingly came out of the blue, the stock plummeted 40% in pre-market trading alongside its close peer, Futu. There was a major intra-day recovery, and UP Fintech ended the day “only” down 25%, but clearly, there are a lot of moving pieces that need to be processed.

Hence, my goal today is to look directly past the initial panic and analyze the actual structural impact of the latest round of sanctions on Tiger Brokers and Futu. To me it seemed like everyone was simply “selling the headline” because there was maximum fear, and at the time the news dropped, A LOT of uncertainty (especially regarding the size of the fine), …

… but a close examination of the enforcement details reveals that the narrative requires a massive dose of nuance.

There is an ancient Chinese proverb that perfectly captures this exact tension:

“In every crisis, there is an opportunity.”

To find that opportunity, however, you have to bypass the immediate chaos that followed the bombshell news release, and exercise some critical thinking. This is what we are attempting to do in this write-up.

A Word of Caution

Before jumping into the numbers and the actual impact on Tiger and Futu’s businesses, though, I want to be entirely transparent with you. Tiger has been a painful, outright catastrophic investment for me so far, and there is absolutely no way to deny that reality. I’m the first one to admit that!

And if you do not understand what you own, an abrupt 40% drop can leave you feeling sick to your stomach. In fact, when the news broke, I published a detailed thought on X regarding why most retail investors should honestly stick to indexing. Tracking complex, highly scrutinized businesses demands specialized skills, a strict baseline of emotional control, and the ability to think in shifting probabilities.

And even when you behave rationally, you are dealing with a range of outcomes where certain variables remain outside of your control.

First, I believe there is a fundamental temperament problem in retail investing. I consider myself a fairly rational and emotionally stable investor. I played poker for many years when I was younger, which thoroughly trained me to process financial losses without panicking. It forced me to assess outcomes based strictly on the quality of the underlying decision, completely ignoring whether the immediate result was positive or negative. Yet, even with that specific background, I could still feel the heavy, visceral impact of Friday’s 40% drop. When a stock plummets like that – and it happens far more frequently than you may think, as Wix recently demonstrated during one of its many own brutal trading sessions – it is incredibly easy to turn off your rational brain. You let raw emotion take the wheel, and when emotions start controlling your decision-making, the quality of your decisions vanishes.

Second, tracking individual businesses takes serious time and specialized skill. Understanding corporate fundamentals, accurately assessing the quantitative impact of breaking news, and evaluating the embedded expectations in a stock price are attributes you have to actively train. Investing comes with inherent risks. You better understand what you are doing and what you own very well. And even then, there is always a probabilistic range of outcomes and structural macro forces that you simply cannot control.

Also, as some of my followers on X rightfully pointed out, on the spectrum of single stocks you can invest in, Tiger certainly falls into a very unique and inherently more risky bucket. It’s very important to be aware of the games you are playing and the risks you are taking on.

There’s no crying in the casino!

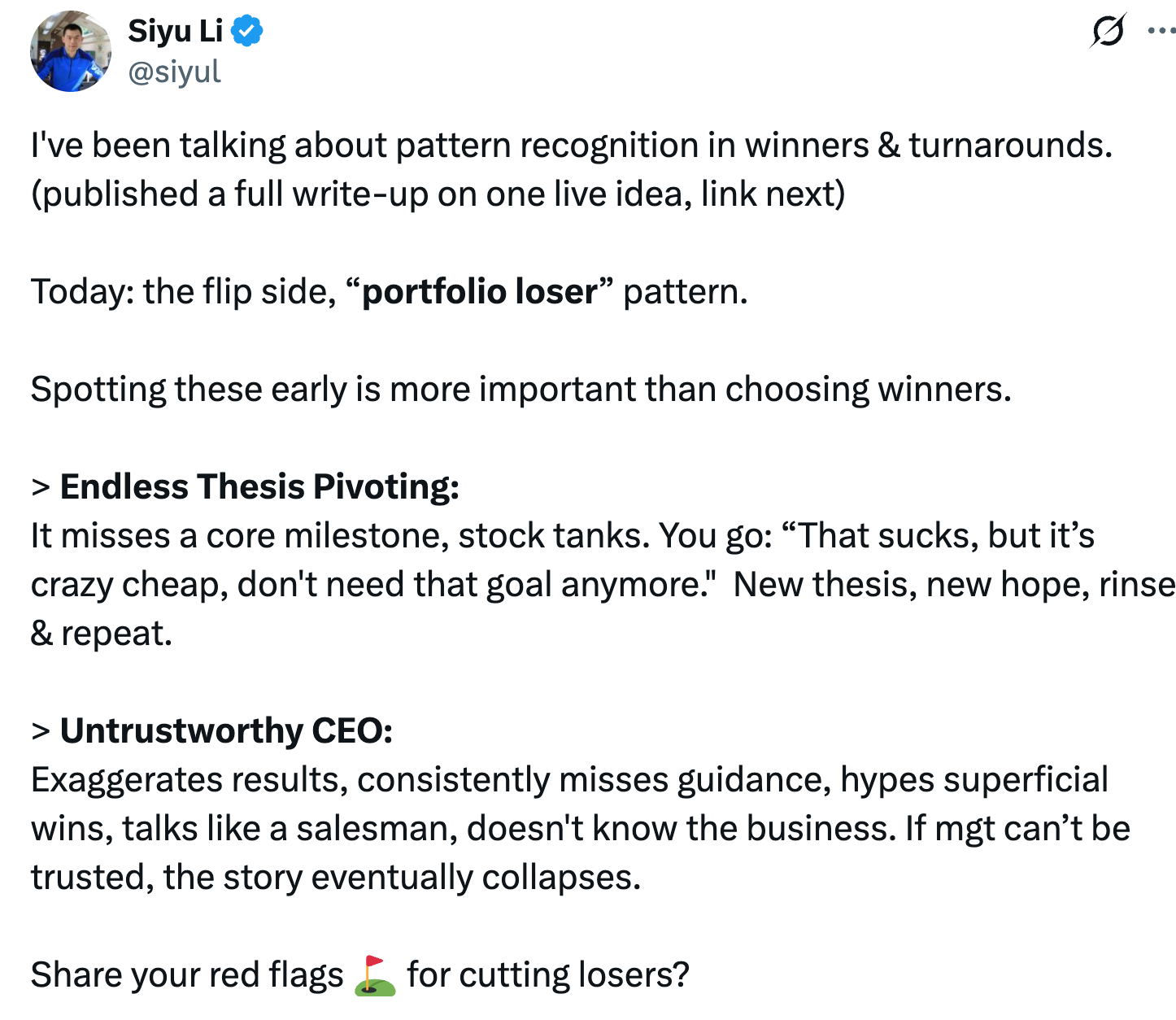

Yet, despite the temporary emotional impact of seeing my portfolio take a heavy blow, I have no intention of selling a single share of Tiger. I am convinced the market overreacted in textbook fashion. At the same time, when I saw a recent tweet from investor Siyu Li, I was immediately forced to look at the mirror and question my own assumptions.

Be Aware of “Endless Thesis Pivoting”

The other day, Siyu Li published a brilliant framework on pattern recognition in portfolio losers, warning against the trap of “endless thesis pivoting.”

The pattern is dangerously familiar: a company misses a core milestone, the stock tanks, and the investor immediately rationalizes the disaster by telling themselves the asset is now crazy cheap, concluding they did not need that specific milestone anyway. A new thesis is born, new hope emerges, and the destructive cycle rinses and repeats.

Siyu may very well be right. In investing, turnarounds seldom turn. The first loss is often the best loss, precisely because unexamined losses have a habit of getting worse and worse over time.

I think it is absolutely critical to keep this counterargument in mind as we evaluate the business of Tiger Brokers. This is a business and investment thesis with a lot of hair on it. And arguably, the thesis has changed from a “growth at a reasonable price” play to more of a special situation case with a lot of regulatory hair on it. Even though I think that’s still not a perfect description of what we are witnessing here, as anyone who owned Tiger and/or Futu, should’ve been very much aware of the hostile stance the CCP has (and had) towards these offshore brokerage firms. This isn’t new at all.

But back to Siyu’s point … Is my insistence on holding Tiger a rational calculation, or am I falling face-first into an endless thesis pivot? That’s something to keep in mind when reading the rest of this post.

So let us dive into the actual context of the crackdown to find out.

Disclaimer:

I own Tiger Brokers shares. The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also, double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

Contextualizing the Development: A Reality Check

To assess where Tiger Brokers stands today, we must strip away the emotional noise and look at the exact operational and macroeconomic mechanics of the latest regulatory action.

The market panicked on Friday, sending shares of Tiger and Futu down by more than 40% in pre-market trading, because it interpreted the news as a sudden, unpredictable death blow.

However, a systemic review of the enforcement details reveals that this is not an arbitrary corporate execution, but a highly coordinated, macroeconomically driven policy containment.

Here’s my attempt at summarizing the key aspects every investor needs to understand regarding the scope, mechanics, and drivers of this regulatory sweep:

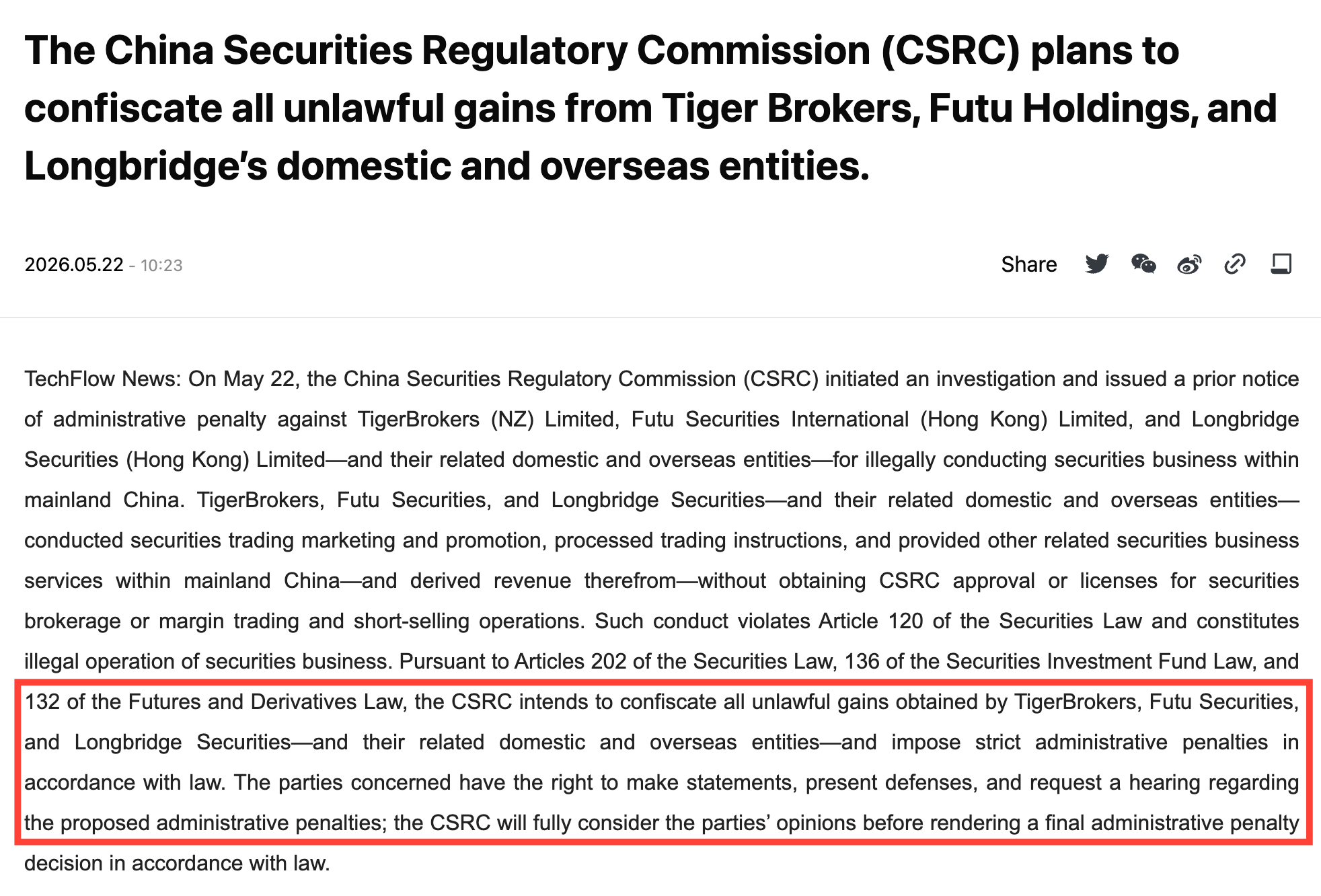

The Core Action and Penalties: Led by the China Securities Regulatory Commission (CSRC), Chinese authorities announced an aggressive, multi-agency campaign targeting unlicensed cross-border brokerage activities inside the mainland. The regulator named Tiger Brokers, Futu Holdings, and Longbridge Securities, stating intentions to impose severe administrative penalties and confiscate what they classified as “illegal gains” accumulated from domestic and offshore entities.

The Inter-Agency Coordination: This is not a standalone statement by a single financial regulator. The implementation plan was jointly issued by eight government departments – including the CSRC, the People’s Bank of China (PBOC), the Ministry of Public Security, and the Ministry of Industry and Information Technology – with the formal approval of the State Council. It represents an ironclad, multi-dimensional firewall designed to target the entire cross-border ecosystem, from the digital apps down to domestic banking rails.

The Two-Year Liquidation Timeline: Regulators have established a definitive two-year transition period to wind down existing non-compliant mainland accounts. During this phased window, affected overseas brokerages are strictly prohibited from processing new buy orders or accepting fresh capital inflows from onshore investors. Onshore clients are legally restricted to one-way sell trades and capital withdrawals to ensure an orderly wind-down without triggering an abrupt liquidity crisis. Following the expiration of this window, these platforms must completely dismantle and shut down their mainland-facing websites, trading applications, and local support servers.

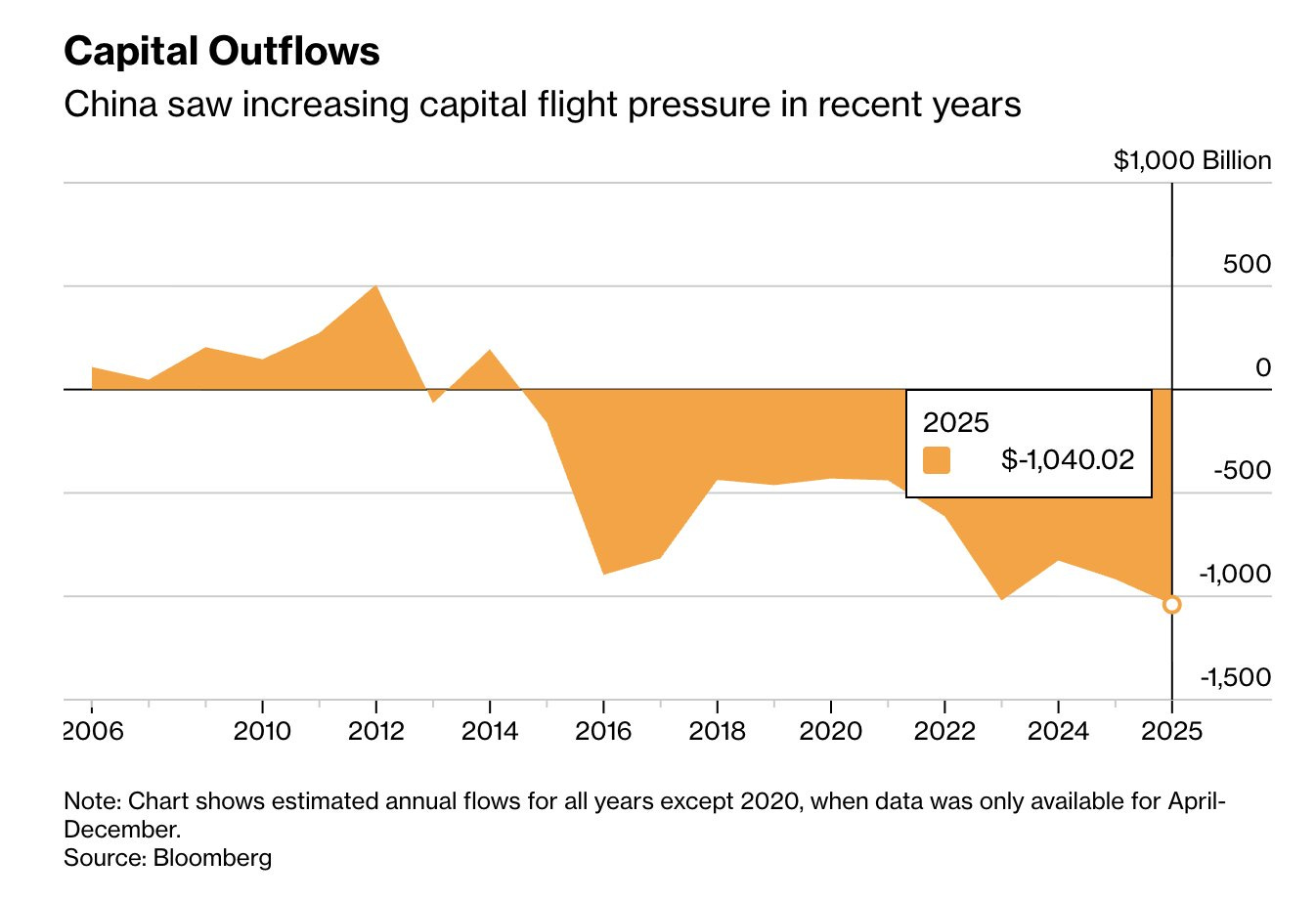

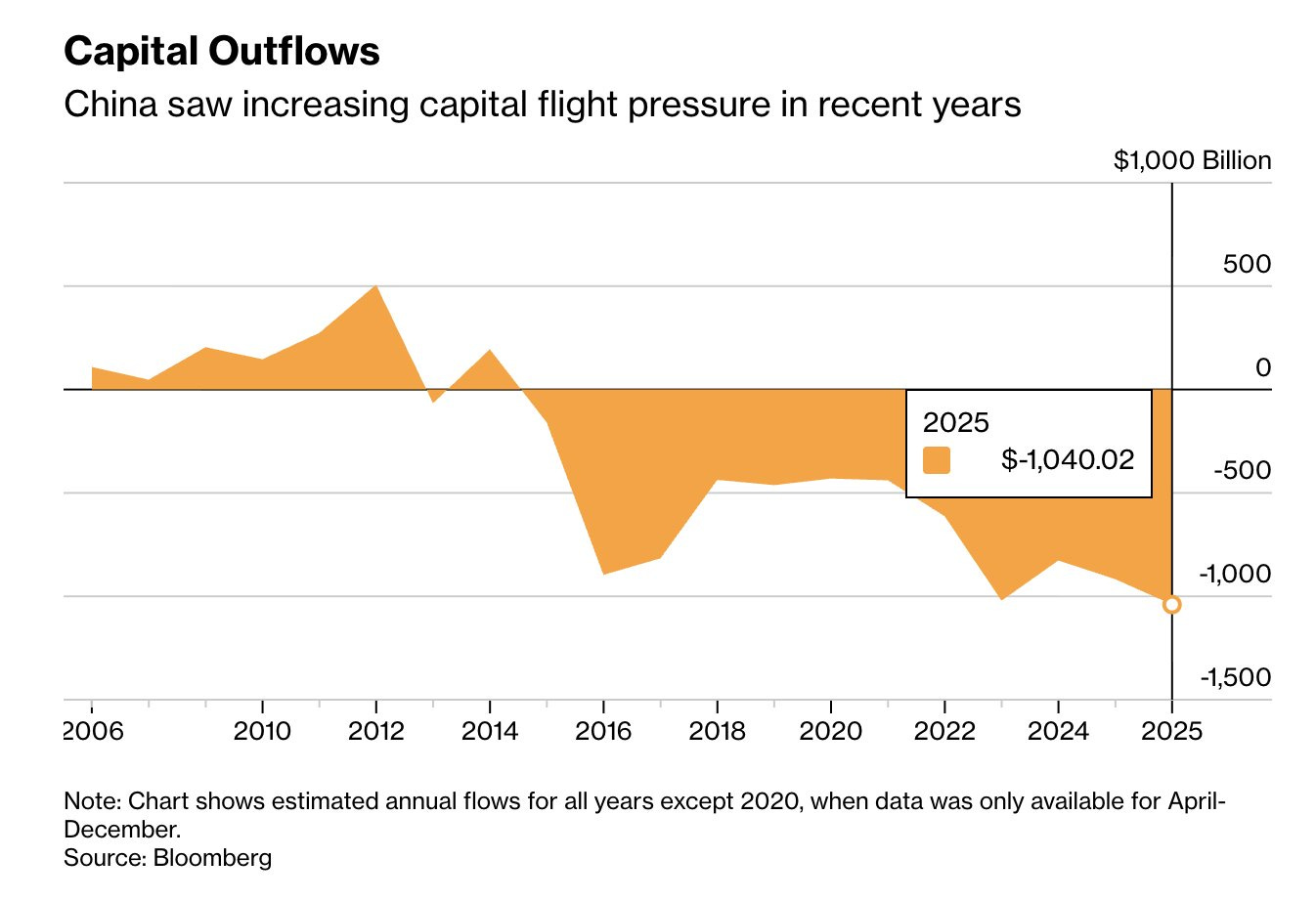

The Macro Context of Capital Flight: The underlying driver of this heavy-handed intervention is a severe macroeconomic vulnerability. Driven by a lagging domestic stock market and falling fixed-income yields, …

… mainland capital flight accelerated dramatically, with outflows, according to Bloomberg, exceeding 1 trillion dollars in 2025 alone. Onshore residents have aggressively bypassed capital controls using underground money changers, corporate swap agreements, offshore insurance policies, and online brokerages to move liquidity offshore.

Source: Bloomberg Analysis I’ll point you to this thread by Brad Setser in the context of this aspect, as I believe he’s adding some important nuance to the figures shared by Bloomberg:

Brad Setser@Brad_SetserEquity outflow from China last year was $ 200b. Big but not unmanageable. Relative to GDP, nothing like the flow out of South Korea 1/

Brad Setser@Brad_SetserEquity outflow from China last year was $ 200b. Big but not unmanageable. Relative to GDP, nothing like the flow out of South Korea 1/

Richard Casey @Richard_CaseyBeijing tightens capital controls despite large current account surplus and supposedly undervalued currency. China launches crackdown on cross-border stock trading to stem capital outflows. An estimated $1 tn flowed out of country last year, biggest capital outflow since data7:54 PM · May 25, 2026 · 28.6K Views10 Replies · 21 Reposts · 121 Likes

Richard Casey @Richard_CaseyBeijing tightens capital controls despite large current account surplus and supposedly undervalued currency. China launches crackdown on cross-border stock trading to stem capital outflows. An estimated $1 tn flowed out of country last year, biggest capital outflow since data7:54 PM · May 25, 2026 · 28.6K Views10 Replies · 21 Reposts · 121 LikesThe Total Scale of Impacted Assets: According to estimates from CITIC Securities, the cumulative investment scale of mainland investors across Futu and Tiger sits between HKD 200 billion and HKD 250 billion (approximately 32 billion US dollars). Out of this total, Futu accounts for the lion’s share at roughly HKD 150 billion to HKD 180 billion, while Tiger represents a smaller footprint of around HKD 45 billion to HKD 50 billion. Given that the daily average turnover of the Hong Kong stock market alone regularly hovers around 260 billion US dollars, the systematic wind-down of these assets over two full years is calculated to have a thoroughly controlled, negligible impact on broader market liquidity.

Going forward, the perimeter has been clearly drawn with zero room for corporate maneuver. Mainland residents seeking global equity exposure will be restricted strictly to highly regulated, state-sanctioned channels such as the Qualified Domestic Institutional Investor (QDII) program, the Cross-boundary Wealth Management Connect, and the established Stock Connect mechanisms.

An Important Lesson on the Signal Value of “Price”

There is a dangerous arrogance that easily creeps into the mind of any investor who spends hundreds of hours reading regulatory filings and building complex valuation models. We tend to fall in love with our own depth of knowledge, gradually convincing ourselves that the market is simply an inefficient collection of panicked retail traders who do not understand the underlying asset.

When a stock collapses, our immediate psychological defense mechanism is to assume that everyone else is acting out of irrational fear while we possess the superior long-term vision.

The trading volume leading up to Friday’s announcement offered a brutal, humbling reality check to that worldview. Many investors, including myself, couldn’t make sense of the price at which Tiger Brokers’ stock traded.

Interestingly, before the regulatory hammer fell, the options market for Tiger began flashing highly anomalous signals. The open interest on the put side expiring over the subsequent two-week window surged to a staggering multiple of over 25 times the call volume. This was not a standard macro hedge. It was a highly concentrated, deliberate positioning by accounts that evidently possessed a structural information advantage.

When you see that level of asymmetry right before a major market-moving event (Tiger’s earnings release on June 2), you have to acknowledge a fundamental truth: inside information and information asymmetry are structural realities of the public markets, and even more so in small caps. The “tape” often registers the corporate reality long before small, independent investors have a chance to access inside information.

This is precisely why we should train ourselves to respect the market’s pricing signals most of the time. Michael Mauboussin, one of the sharpest minds in investment theory, constantly urges investors to ask a simple, clarifying question whenever they think they have found a massive mispricing:

“Who is on the other side of the trade?”

If you believe a stock is absurdly cheap and the sellers are completely mistaken, you are implicitly assuming that the institutional fund managers, algorithmic traders, and connected insiders executing those sell orders are collectively foolish.

And that is simply not true.

Fundamentals alone lose their predictive power when you are operating in an environment defined by severe information asymmetry. If you possess only 90% of the relevant operational information, and that 90% looks incredibly bullish, the absolute valuation numbers on your spreadsheet can lead you into a false sense of security. The critical, often unanswerable question is always what exists inside the missing 10%. In highly regulated, geopolitically sensitive sectors, that missing information is a blind spot that remains entirely invisible until the specific structural risk materializes and hits your portfolio like a freight train. Understanding your own ignorance is far more valuable than pretending you can model a regulatory landscape with absolute certainty.

The hidden trap of deep fundamental analysis is that it frequently morphs into an elaborate exercise in confirmation bias. We conduct massive deep dives, compile exhaustive research notes, and answer hundreds of granular operational questions, only to use that data to justify a pre-determined conclusion that a low valuation represents a safe margin of safety.

Discussing The Extent of the Fines

When the initial panic gripped the tape, one of the first mental exercises I ran through was a basic probability matrix regarding the scale of the impending fine.

Looking at the sheer violence of the pre-market sell-off, bankruptcy was clearly on the menu of market fears. To be entirely fair to the bears, a terminal outcome was not a zero-probability scenario in the absolute earliest hours of the panic when all we had was the initial statement by the CSRC.

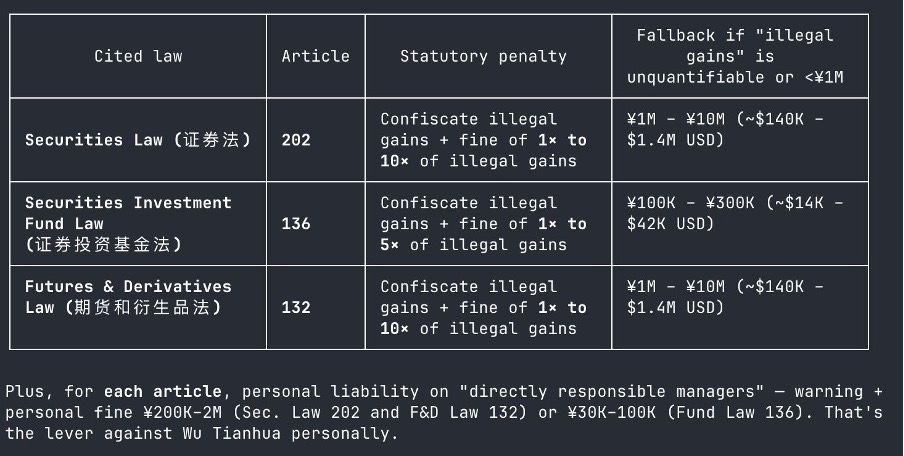

Under China’s statutory legal frameworks for unlicensed financial activities, penalties calculated as multiples of illegal income can theoretically scale up to five or ten times the underlying figures. Furthermore, administrative enforcement can vary drastically depending on whether regulators choose to punish gross revenue or allow a deduction for operational expenses – two doctrines that are actively applied across different domestic legal precedents.

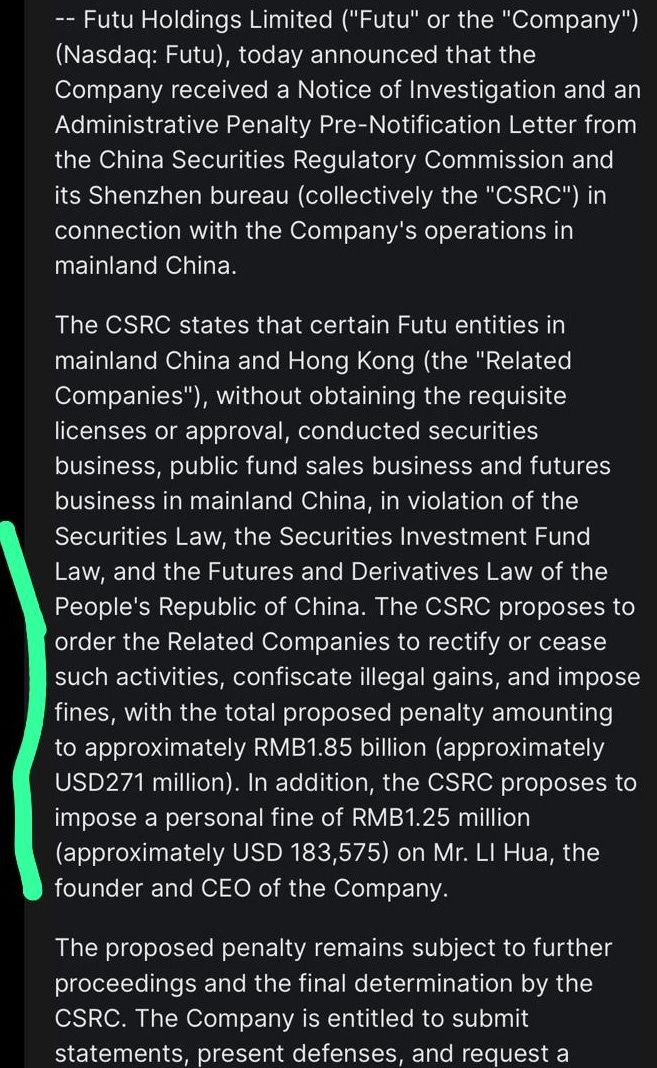

When the exact regulatory details finally materialized later in the day – first revealed by Futu …

and later by Tiger …

… –, the reality turned out to be a more than manageable corporate hit rather than an existential execution.

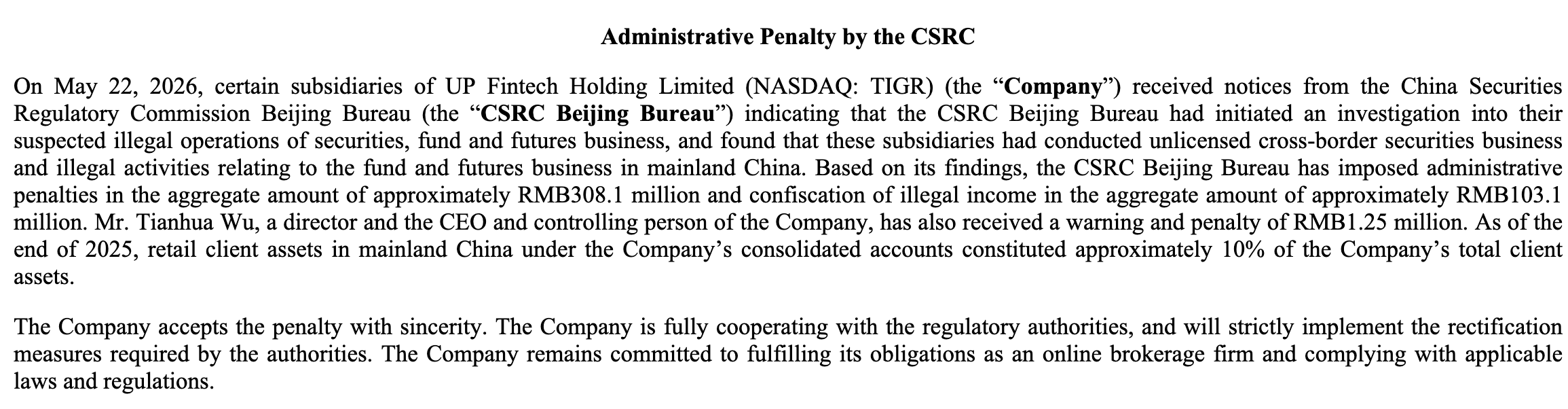

The CSRC Beijing Bureau issued Tiger a fine of approximately RMB 308 million alongside the confiscation of RMB 103 million in illegal income, translating to a total penalty of roughly 57 million US dollars.

While certainly a substantial chunk of change, this bill represents roughly four months of net income for the 2025 fiscal year, or approximately 10% of Tiger’s total cash reserves. If you isolate their idle, uncommitted corporate cash, the penalty absorbs maybe between 20% and 25% of that buffer.

Yes, it is an expensive parking ticket, but not a death sentence, and my concerns regarding the immediate survivability of the firm evaporated almost instantly.

Games Being Played

The sheer speed of the corporate response tells you everything you need to know about how the regulatory game is actually played in Beijing. Within hours of the public announcement, Tiger published an official statement noting that the company accepted the penalty with absolute sincerity. No corporate legal team reviews a massive, multi-jurisdictional administrative penalty and issues an official corporate surrender on a Friday night unless the terms were negotiated, drafted, and signed months in advance.

This follows standard domestic regulatory theater. The authorities first quietly identify and then plan to contain the structural problem behind closed doors, determine a manageable penalty that establishes a public example without collapsing the underlying enterprise, and then release the news to signal absolute enforcement intolerance to the rest of the market.

In my view, the fine is largely symbolic.

Playing Devil’s Advocate

To play devil’s advocate, it is crucial to address the structural counterargument. Bears will reasonably point out that regardless of whether the fine is “survivable,” it confirms a deeply hostile regulatory stance toward the business model.

Tiger’s services are fundamentally unaligned with Beijing’s current macroeconomic goals of retaining domestic liquidity. Because the founder’s roots, along with the core engineering and research and development teams, remain physically anchored in Beijing, there is no simple way for the corporate entity to fully escape the geographic reach of the state. Never.

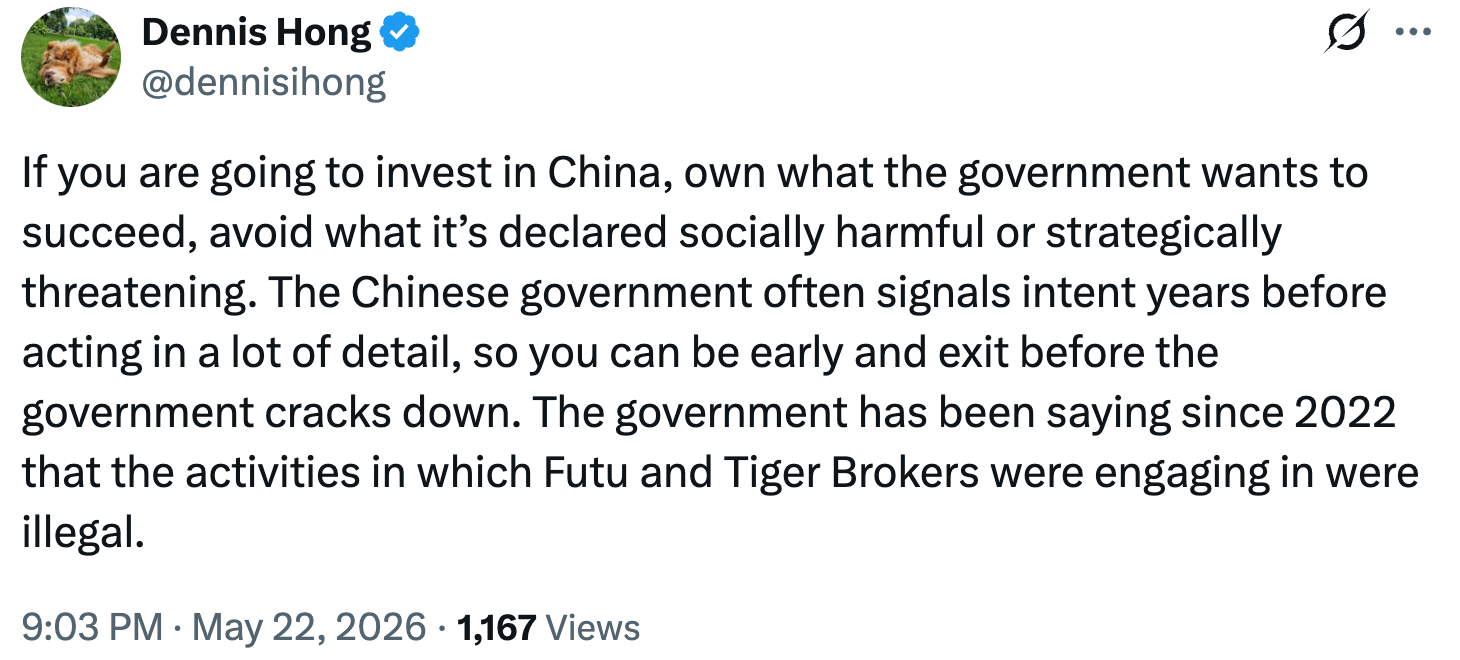

Investor Dennis Hong perfectly summarized this reality in a response to one of my updates on X, noting that when investing within the broader Chinese economic ecosystem, you must own what the government actively wants to succeed and fiercely avoid what it has explicitly declared to be socially harmful or strategically threatening.

The state typically signals its policy intent years in advance with immense detail, offering ample warning to exit before the hammer falls. In this specific case, regulators have been explicitly stating since late 2021 and 2022 – and then again in 2025 – that the cross-border activities of Futu and Tiger were operating outside the law. Full stop.

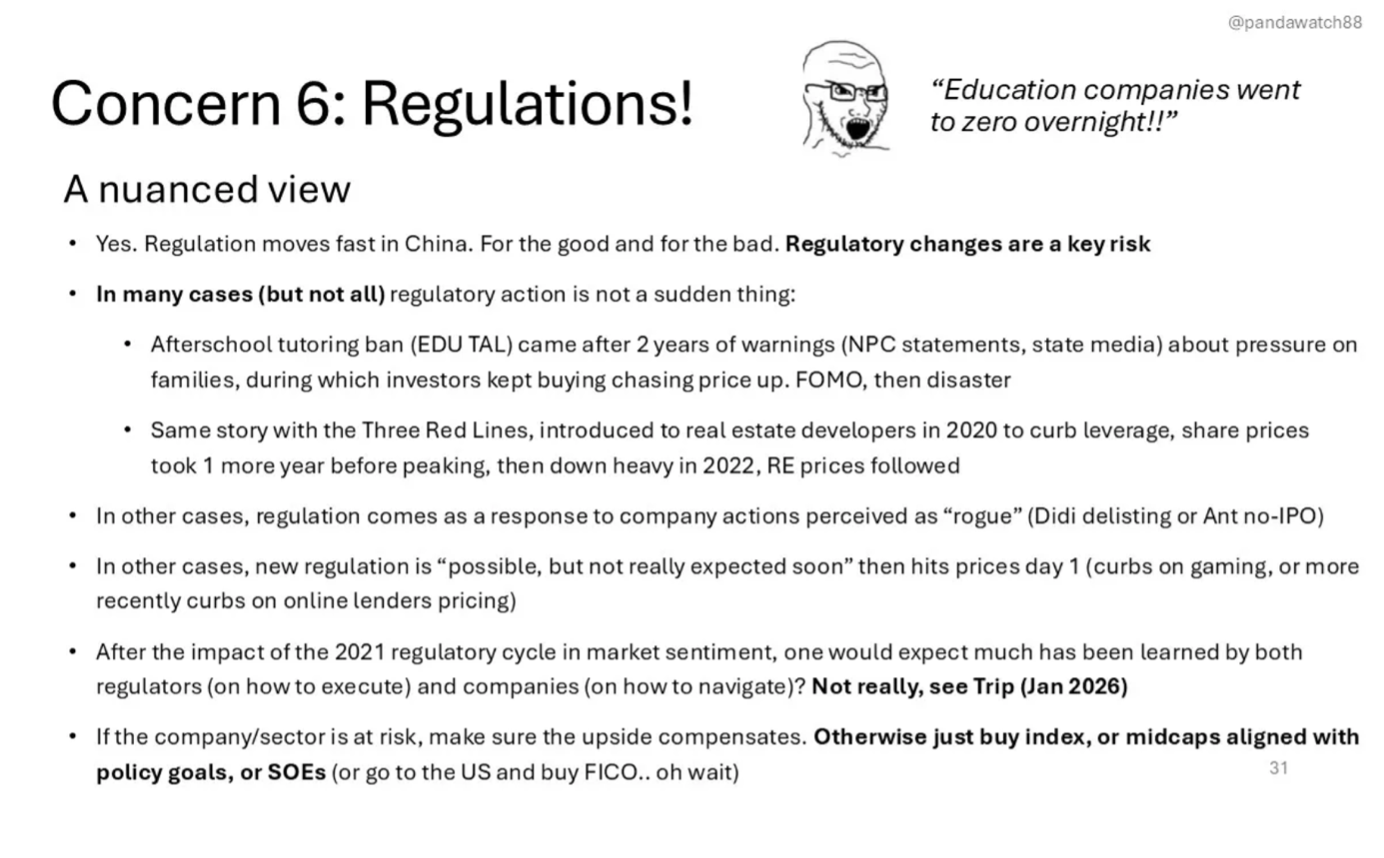

The two slides below shared by Pandawatch reinforce this exact same lens to view China-related stocks with.

You can find Pandawatch’s entire slide deck here:

Moreover, we must establish a sharp intellectual boundary between standard regulatory compliance risk and systemic country risk. The market treated Friday’s crash as if it were the ultimate “China Risk” playing out – the terrifying scenario where an entire equity structure is rendered worthless overnight due to geopolitical shifts, Variable Interest Entity (VIE) de-listings, or an escalation over Taiwan.

That’s not what we witnessed on Friday. This was localized regulatory risk that shouldn’t come as completely unexpected to anyone owning these stocks. As mentioned, the CCP signalled its long-term intent well in advance. Anyone who deployed capital into Tiger over the past three years had to know that Beijing disapproved of these platforms servicing mainland retail clients; that reality was thoroughly documented.

The rules were tightened, an enforcement boundary was established, a fine was levied, and a grandfathered transition period was set.

It is an operational hurdle that clears a multi-year cloud of uncertainty, allowing us to finally analyze the business impact based on its true (international) fundamentals.

The full analysis starts here:

The rest of this post covers the actual impact on Tiger Brokerage in six chapters. If you’re serious about sharpening your investing edge, the full post (and all my previous premium content, including valuation spreadsheets, deep dives (e.g. well-known mid- and large caps such as LVMH, Duolingo, Meta, Edenred as well as more hidden gems such as Digital Ocean, Ashtead Technologies, InPost, Timee, and MANY more) and powerful investing frameworks are just a click away. Upgrade your subscription, support my work, and keep learning.