Strategic Minorities: How "Toehold" Investments May Predict Multi-Bagger Returns

Why Competitors Make the Best Auditors

You can read this article entirely for free. If you find value in this research, consider becoming a Premium Member to unlock our full archive and join our growing circle of investors (I highly recommend checking out “The Library” to see what’s inside; you can find it right on the homepage).

Why join the community, you may ask? Our library is fast approaching 70 comprehensive deep dives, providing institutional-level research on some of the world’s most fascinating businesses. Most recently, we’ve dissected companies like Grab Holdings ($GRAB), Fair Isaac ($FICO), and Topicus.com ($TOI).

As a member, you get:

Complete Access: Every deep dive in our library

The WhatsApp Community: Real-time discussion and networking with like-minded investors.

Incredible Value: Full access to all of this for less than $1/day.

If you want to see the level of research we provide before committing, the following deep dives are, for instance, free to read:

InPost ($INPST) - generated an IRR of >400% as an acquisition offer emerged 2-3 months post write-up

DigitalOcean ($DOCN) - up 5x in less than a year post write-up release

In my view, the primary job of an investor is not to find reasons to buy, but rather to find every possible reason to say no.

The investment landscape is one where the default state is noise – an endless stream of pitches, charts, headlines, CNBC interviews, engagement-bait on social media platforms, and quarterly updates designed to make you feel like you are missing the next great multibagger.

In my experience, the only way to survive this onslaught without diluting your capital into mediocrity is to develop a set of filters so rigid and so uncompromising that they feel almost violent.

The Violent Art of Saying No

I spend the vast majority of my time looking for the exit door on a research project. If I can find one structural flaw, one misaligned incentive, or embedded expectations that require too good an execution, I move on.

It is a superpower.

I was recently listening to an interview with Andrew Hollingworth, the founder of Holland Advisors. He operates with a very similar philosophy, specifically regarding his heavy bias toward owner–operators.

For him, and for me as well, seeing a founder with significant skin in the game is a signal that cuts through the static. It is a filter that allows you to ignore 90% of the public markets immediately. Of course, the risk is that you will brush off a valid idea too quickly. You will watch stocks you passed on at $10 run to $50. That is the price of admission.

However, a strong filter protects your downside and ensures that when you finally do say yes, you are standing on a foundation of high conviction. Your job is to pass. You must try to break the thesis.

Why I Am Selfishly Writing This Post

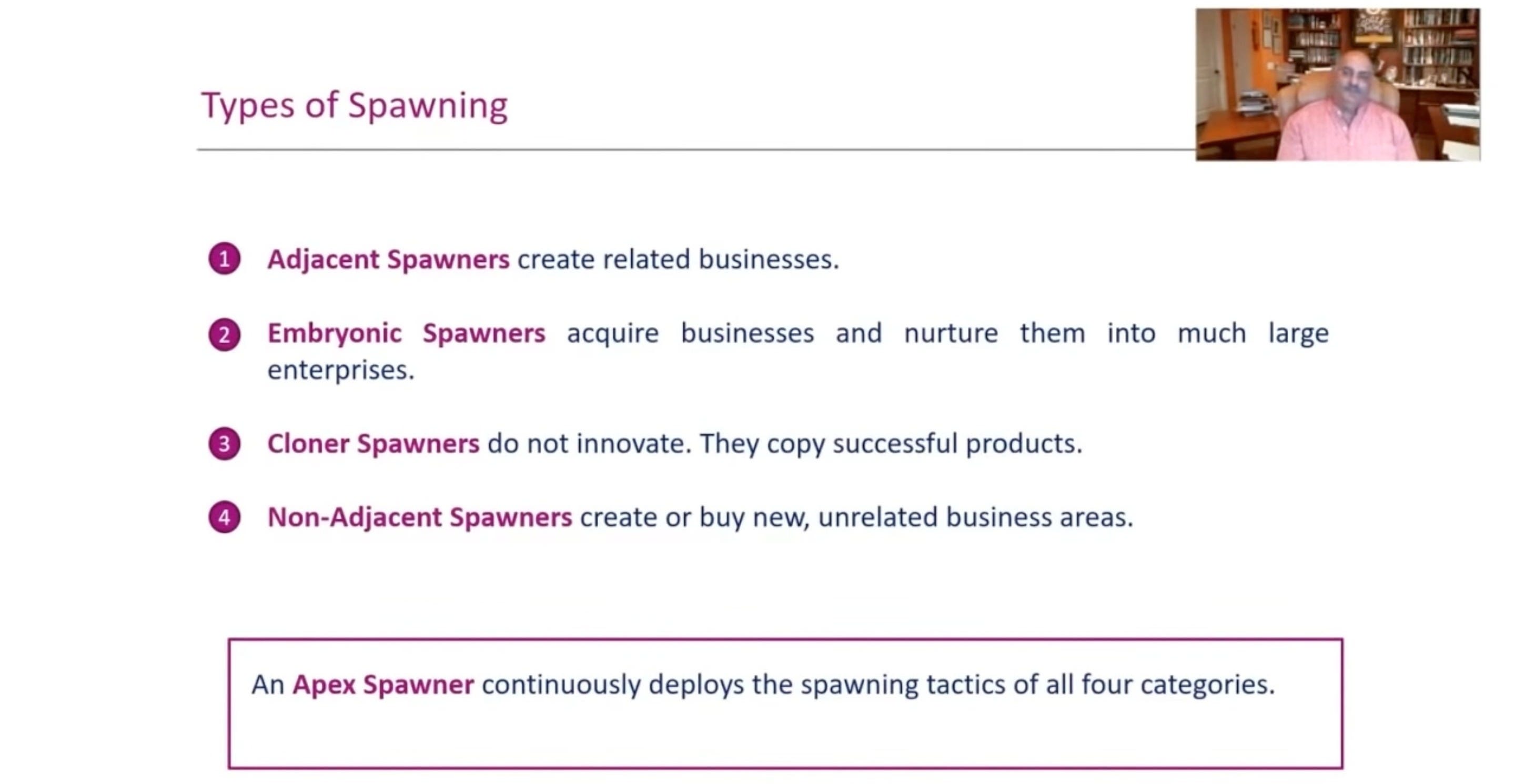

This leads me to a new mental model I have been grappling with this week. I have my usual list of high–quality signals – e.g. (strong) secular tailwinds, above-average industries, founder–led businesses, share cannibals that aggressively retire their own stock, and “spawners” that have the DNA to create new business lines from scratch.

But while reading a post by a fellow author who goes by the name Unemployed Value Degen, I stumbled upon a concept I had never formally integrated into my framework: the “toehold.”

He is one of the very few writers covering Tiger Brokers, a company I have discussed frequently on this blog and one that I currently own in a significant position in my portfolio. I had to read his take.

I found his analysis of the core thesis excellent, but what really stuck in my mind was his mention of IBKR’s small ownership stake (which I was of course aware of), but the idea that the ownership might be a (strong) predictive signal for superior future performance.

It was a “lightbulb” moment. In the spirit of Mohnish Pabrai, whenever I encounter a new mental model that carries genuine weight, I want to punch it into my brain. I want to do everything humanly possible to ensure it sticks. Thus, this post is, quite frankly, born of a very selfish motivation. I am writing this to force myself to memorize the concept, to test the logic, and to ensure that the next time I see a toehold in a filing, I recognize it as the potentially powerful signal it might be.

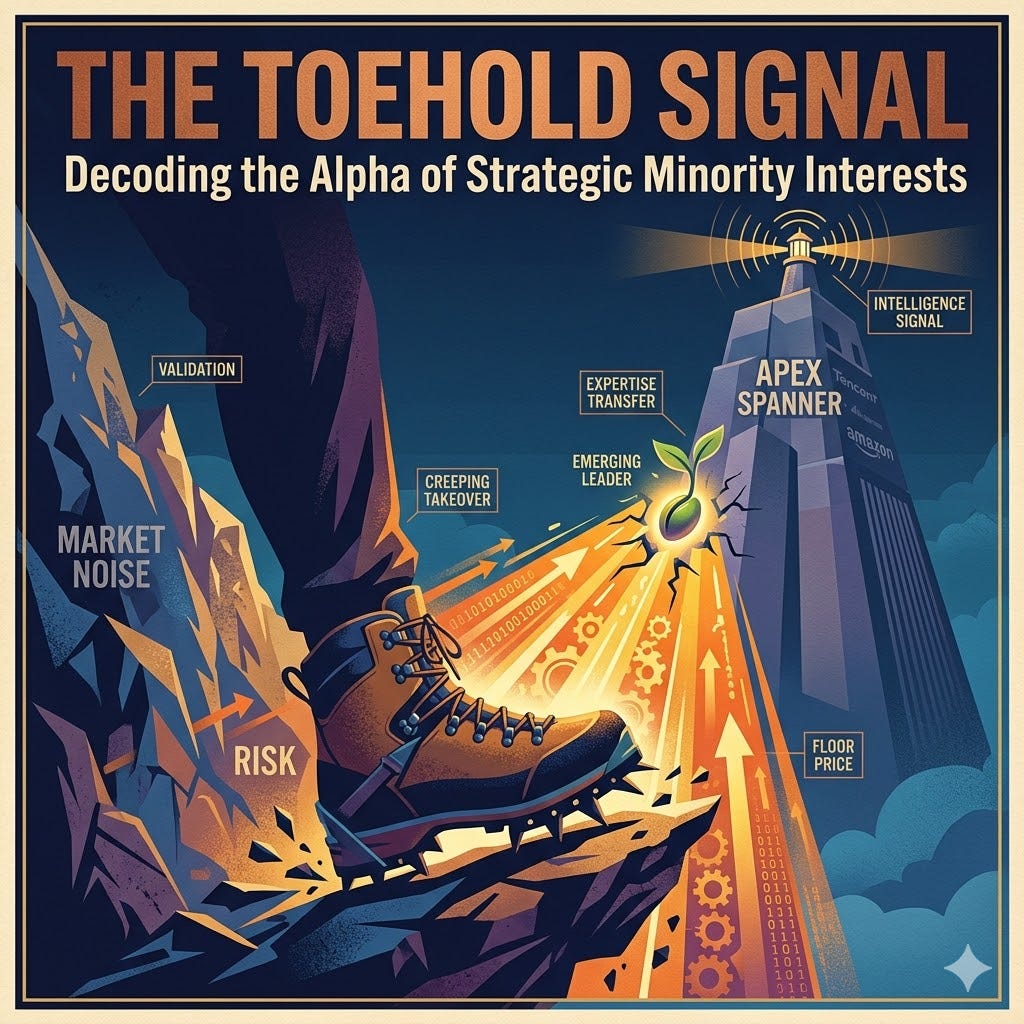

The concept of a toehold is deceptively simple, yet it carries implications that most retail investors completely overlook. If we can identify why a larger, more sophisticated competitor is willing to take a minority stake in a smaller peer, we gain access to a level of due diligence that no individual investor could ever hope to replicate. It is a form of validation that goes beyond what any spreadsheet can tell us.

Over the following segments, I want to explore why this happens, look at the historical evidence of outperformance, and understand how we can use this to sharpen our filters even further.

More Than a Minority Interest: The Anatomy of a Toehold

To understand why this concept carries such weight, we first need to define what we are actually looking at. In the blog post that sparked my curiosity, Unemployed Value Degen laid out the case for UP Fintech (TIGR) by highlighting a specific shareholder:

“UP Fintech holdings is still controlled by its founder, Tianhua Wu, with over 12% of economic ownership, and voting control with class B shares that have 20x voting rights. There are also strategic ownership stakes held by Xiaomi, the mobile phone / automobile manufacturer, and Interactive Brokers. When looking at the Interactive Brokers’ ownership stake in particular, it qualifies as a “toehold” – a small ownership stake by a larger competitor. This is usually accompanied by technology and expertise transfers, indicating a bright future for the smaller company, and sometimes foreshadows an eventual acquisition. Sure enough, Interactive Brokers assisted TIGR with the US compliance and Know Your Client rules. The last time I bought a stock with a toehold, it was VitaCoco at $9, and today it trades at $65. Toeholds were a primary area of research of my former PhD advisor, and whenever I stumble across one, it immediately catches my attention.”

This passage touches on the idea of asymmetrical information. When a large, established player like Interactive Brokers takes a stake in a younger, more nimble competitor, they are frequently doing more than just parking capital. They are performing a level of due diligence that you and I, as outside investors, simply cannot access. They are looking under the hood, so to speak. When they write that check, they are effectively telling the market that this smaller company has passed the most rigorous audit possible – one conducted by its own rivals.

Why Competitors Make the Best Auditors

Most investors spend their time tracking institutional ownership – looking for which superstar investor is buying which stock – everyone gets excited during 13-F season!

And while that can be a useful signal, it is fundamentally different from a toehold. A professional (fundamental-oriented) fund manager is an expert in realms such as business and competitive advantage analysis, portfolio management, valuation, or capital allocation, but a competitor is an expert in the actual field the business operates in. If a dominant player in an industry decides to own a piece of a smaller challenger rather than trying to crush them out of existence, we should pay attention. It suggests that the smaller company possesses something the larger one lacks: perhaps a more efficient tech stack, a better user acquisition strategy, or a specific geographic advantage.

This is a kind of “validation signal” in its purest form. A toehold suggests that the incumbent sees the smaller company as a peer or a future partner rather than a nuisance.

In the case of Tiger Brokers, having Interactive Brokers – the gold standard for discount brokerage infrastructure – assist with US compliance is not just a “nice to have” partnership. It is a massive operational lift. It removes the execution risk that plagues so many high–growth fintechs.

“We currently rely on Interactive Brokers to execute, settle and clear a portion of the trades of the U.S. and Hong Kong stocks and other financial instruments, and to comply with certain federal, state and other laws, as discussed more fully in Item 4.B “Business Overview-Our Core Products and Services-Brokerage Services. ” For the years ended December 31, 2023, 2024 and 2025, 16.6%, 10.6% and 6.6% of our total net revenues were executed and cleared by Interactive Brokers. For consolidated accounts, the information of which is not fully disclosed to Interactive Brokers, we receive commission fees and direct a pre-determined portion to Interactive Brokers.“ - Tiger’s 2025 Annual Report

For us, the filter is simple. If one of the best brokerage businesses, one of the best brokerage infrastructure providers in the world, is betting on their regional competitor’s success, the probability of that competitor being a “fraud” or a “failure” drops meaningfully.

The Call Option on a Future Acquisition

Beyond the operational validation, a toehold represents a very specific type of financial optionality. It is sometimes (or rather often?) the first step in a “creeping takeover” attempt or a pre–negotiated path to an acquisition. When a larger company takes a 5% or 10% stake, they are often buying a seat at the table. They get a front–row view of the financial performance. Possibly a board seat. They build relationships with the management team. Most importantly, they often secure “right of first refusal” or “right of first offer” clauses that give them a massive advantage if the company ever decides to sell.

As an investor, owning a company with a strategic toehold means you are essentially “piggybacking” on a future M&A event. You are holding a stock that has a built–in floor price because there is a logical, deep–pocketed buyer already sitting on the cap table.

This can create an interesting risk–reward profile. You get the upside of the smaller company’s organic growth, supplemented by the expertise of the larger partner, all while holding a “call option” on an eventual buyout at a premium. It is a powerful combination. It turns a standard equity investment into a strategic play.

Conceptualizing the toehold also requires us to look at it through the lens of signaling. In a world of “pump and dump” schemes and management teams that over-promise and under-deliver, the toehold is a concrete action. It is a “hard” signal. It costs the larger company real money and reputation. They are putting their name next to the smaller company. This isn’t a vague press release about a “strategic partnership” that leads nowhere. This is a real monetary commitment.

A toehold is a vote of confidence in the management’s integrity and the product’s longevity. It serves as a filter that filters out the “wannabes.” It is very rare for a world–class organization to take a minority stake in a mediocre business. They want the best. They want the winners. By identifying these stakes early, we are essentially letting the most successful companies in the world do our screening for us. We are leveraging their vast resources, their industry knowledge, and their strategic foresight to improve our own hit rate.

This is how we move from being “dumb money”, from “retail”, to being “informed.”

Case Studies

If a mental model is to be useful, it must move beyond theory and prove its worth in the cold reality of the tape.

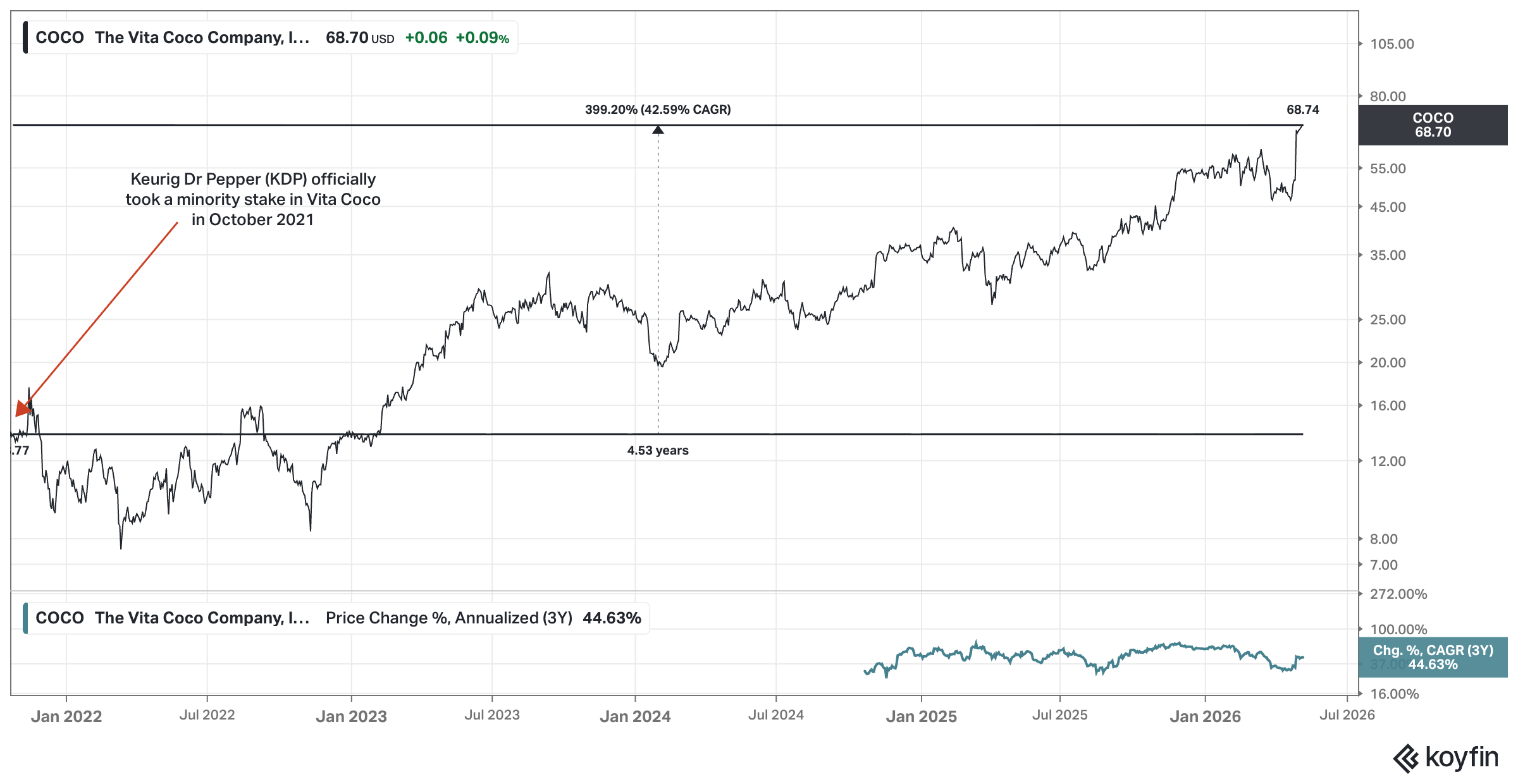

One of the most profound examples in recent history, and one brought up by Unemployed Value Degen in the excerpt below, is the relationship between Keurig Dr Pepper and Vita Coco.

When a massive distributor and manufacturer takes a strategic stake in a category leader, they are not only betting on a trendy product; they are betting on the supply chain, the brand’s resonance with a specific demographic, and the potential to scale that brand through their own superior distribution network.

For the smaller company, it provides an immediate “inflection point” where their operational ceiling is effectively removed. As the stock moved from under $10 to over $60, it became clear that the toehold might have been the early signal for a massive compounding story.

The Constellation Software Playbook: Public Equities as a Lab

When we talk about capital allocation, the conversation among value investors will most likely eventually shift to Mark Leonard (I hope he recovers quickly!) and Constellation Software (CSU) and the accomplishments of Leonard and his team.

I believe a fascinating shift has occurred recently with both Constellation and its spin–off, Topicus. Traditionally, these companies were focused on acquiring 100% of small, “boring” vertical market software (VMS) companies. But lately, they have begun to flex their muscles in the public markets, taking strategic stakes in larger VMS peers.

I see this as a natural evolution of their acquisition approach.

By taking a minority interest in a public competitor, CSU and Topicus are essentially running a real–time laboratory. They get to observe the management’s discipline, the stickiness of the software, and the pricing power of the business from a privileged vantage point. At the same time, they can share their expertise with them. If the company performs well and fits the culture, the toehold might become the foundation for a full acquisition. If it doesn’t, they have still invested in a liquid high–quality asset that they understand better than almost anyone else in the market. It is a “try before you buy” strategy at a multi–million/billion dollar scale.

The Tencent Ecosystem: Minority Stakes as Call Options

Tencent has arguably perfected the “toehold” strategy more than any other firm in history. Instead of trying to build every service themselves, they took a minority stake in companies like Sea Limited, JD.com, and Meituan. They then integrated these companies into the WeChat ecosystem, providing them with a massive firehose of traffic. This didn’t just help the smaller companies grow – it allowed Tencent to build a “synthetic” monopoly where they owned a piece of everything (good) their users touched without the regulatory headache of owning the entire entity.

Tencent eventually divested some of these stakes or, in other cases, deepened them. But the signal was always there: if Tencent is taking a 5% or 10% stake in your business, they are essentially providing you with their “Seal of Approval.” They are saying that your tech, or your product offering, is very good.

More Examples

To give you a sense of just how widespread this phenomenon is, I’ve put together a few more examples where a strategic toehold was the precursor to a massive run or an eventual takeout. Notice how in each case, the “parent” company brought more than just cash to the table – they brought expertise, distribution, or technology.

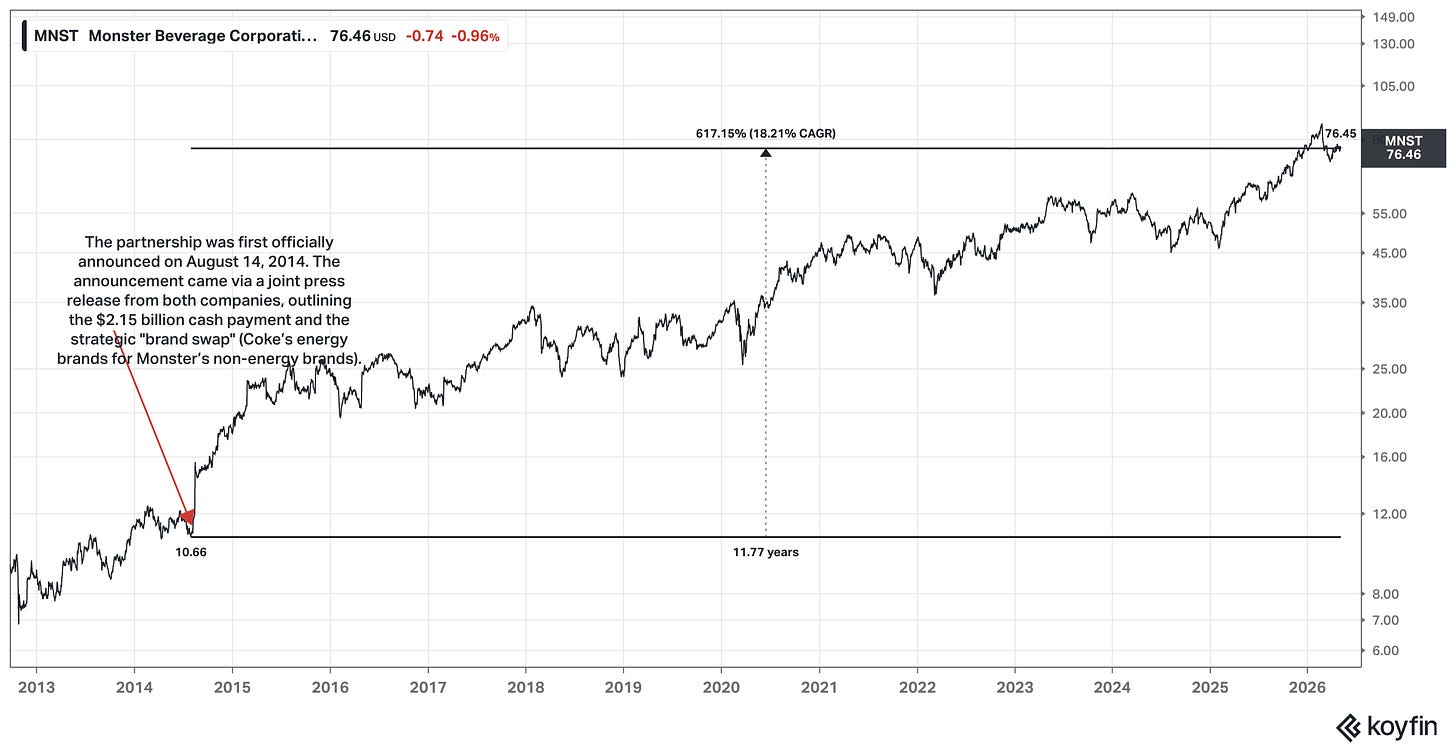

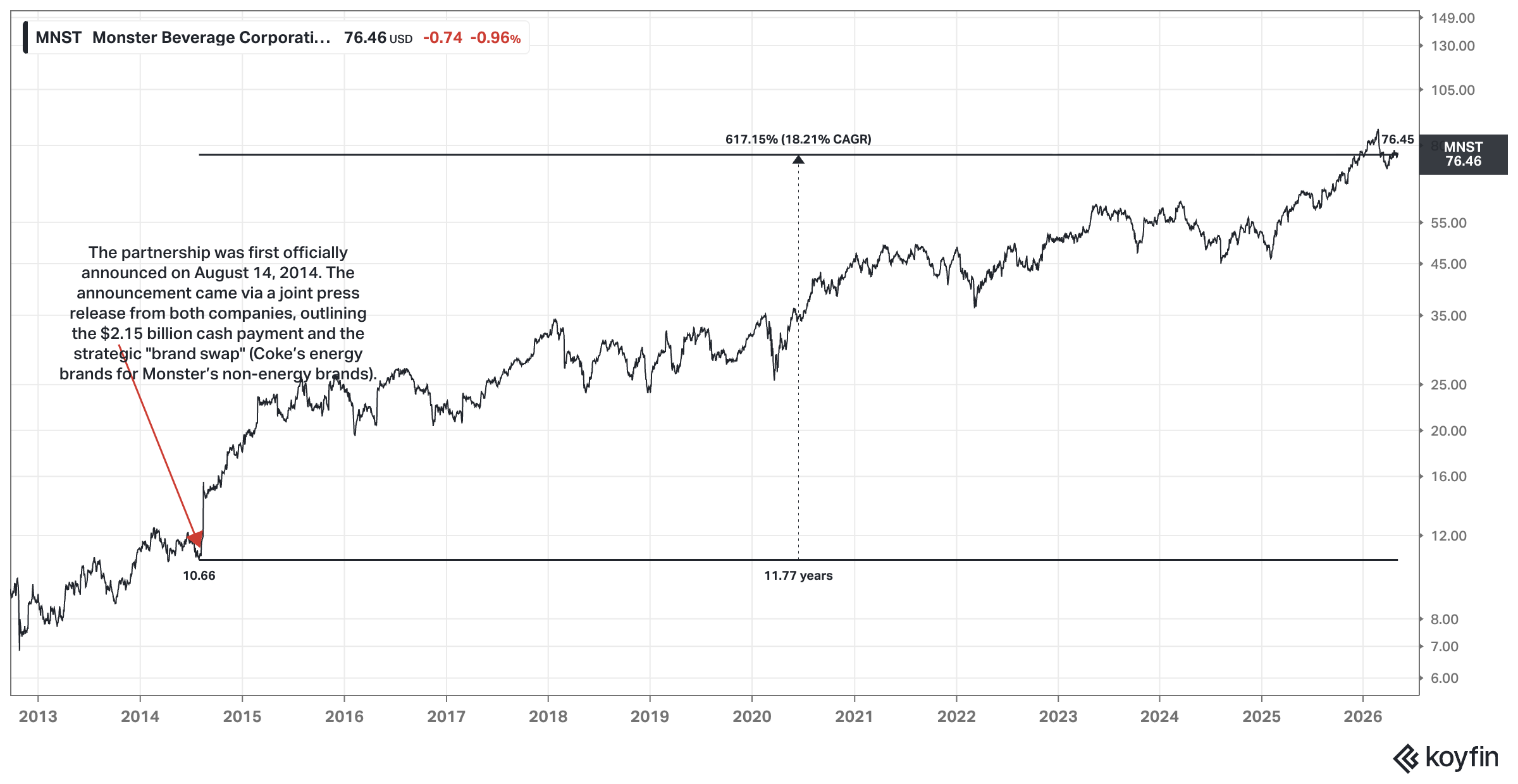

Coca–Cola & Monster Beverage: In 2014, Coke took a roughly 17% stake in Monster. They swapped their energy brands for Monster’s non–energy brands and took over global distribution. The stock has been a multi–bagger since, fueled by the “Coke System” acting as a global accelerant.

Disney & BAMTech: Disney initially took a 33% stake in BAMTech – which was never a public company – to power its streaming aspirations. That toehold provided the technical foundation for Disney+, and Disney eventually bought the whole company. The minority stake was the “due diligence” period for their entire future strategy.

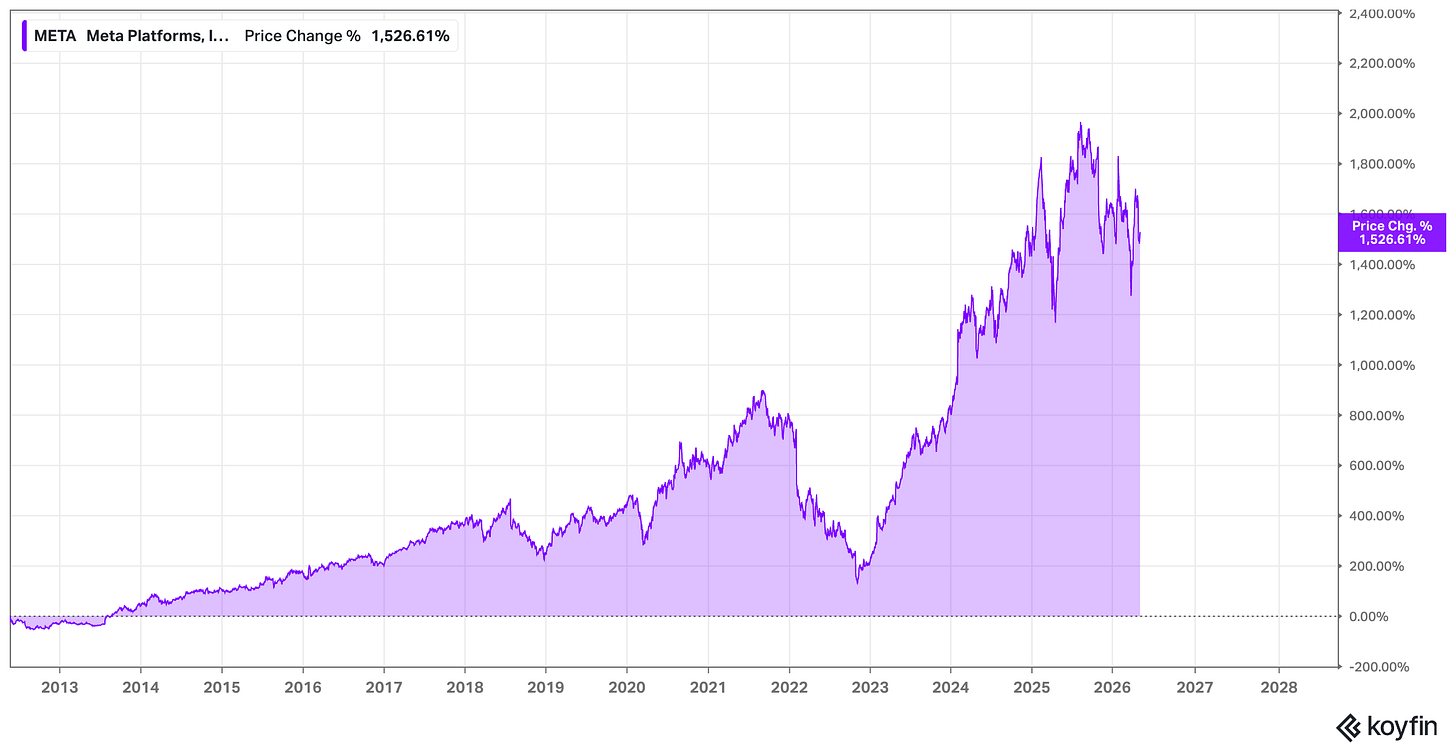

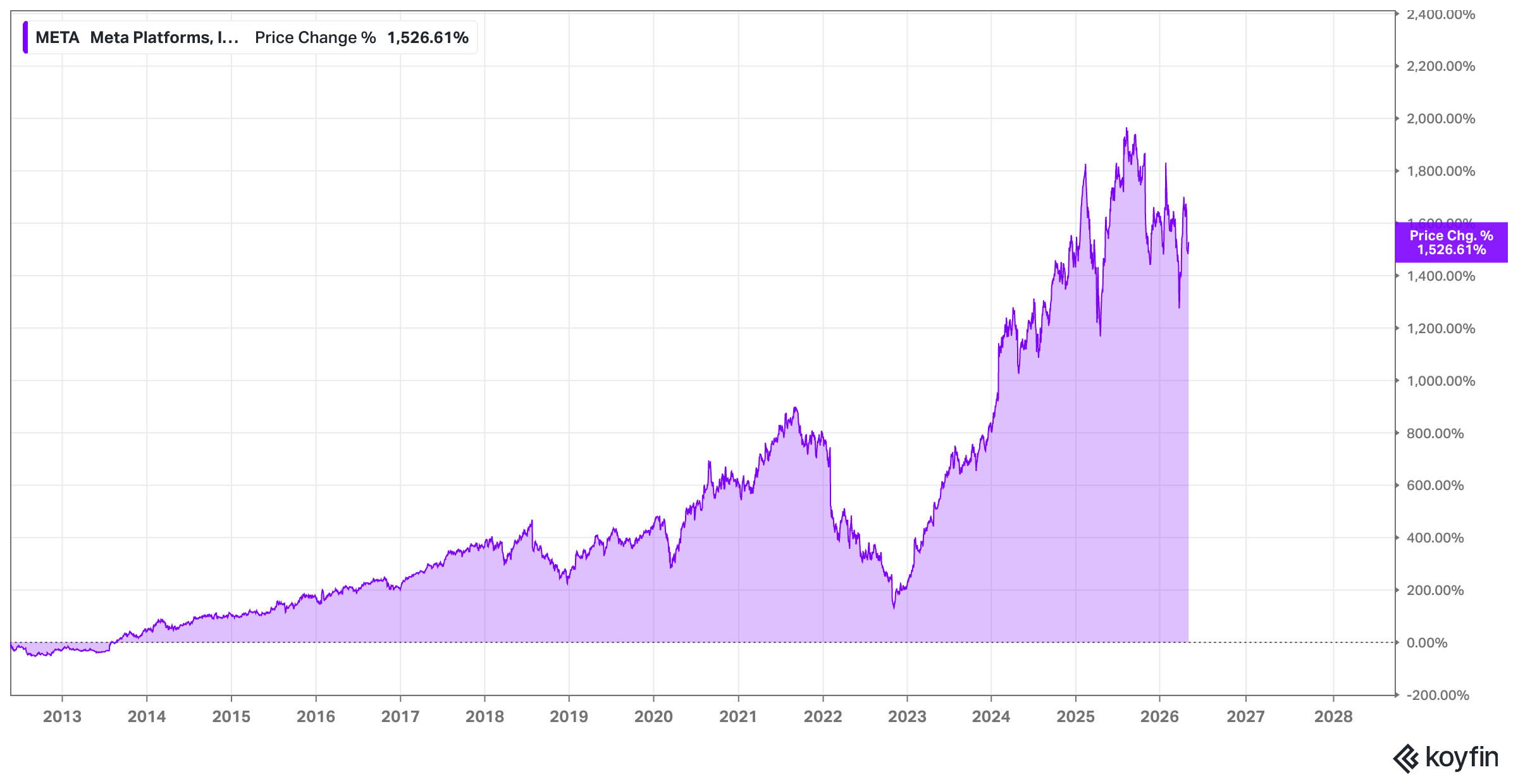

Microsoft & Facebook (2007): Long before Facebook was the giant it is today, Microsoft took a 1.6% stake for $240 million. While small, it was a massive signal to the market that the social graph was the next frontier of computing.

Delivery Hero & Glovo: This started as a 15% minority interest. Delivery Hero used that position to coordinate strategy and eventually moved to take full control.

Celsius (CELH) & PepsiCo: This is perhaps the most striking modern parallel to the Monster/Coke deal. In 2022, PepsiCo took a strategic minority stake in Celsius – roughly 8.5% – worth about $550 million. On the surface, it may seems as only a capital injection. In reality, it was a total transformation of the business as the deal came with a long–term distribution agreement that plugged Celsius into Pepsi’s massive, world–class logistics machine. For an energy drink company, the ability to get “eyes on the shelf” is the ultimate “moat.” The toehold was possibly a signal that Celsius is graduating from a niche fitness brand to a global contender.

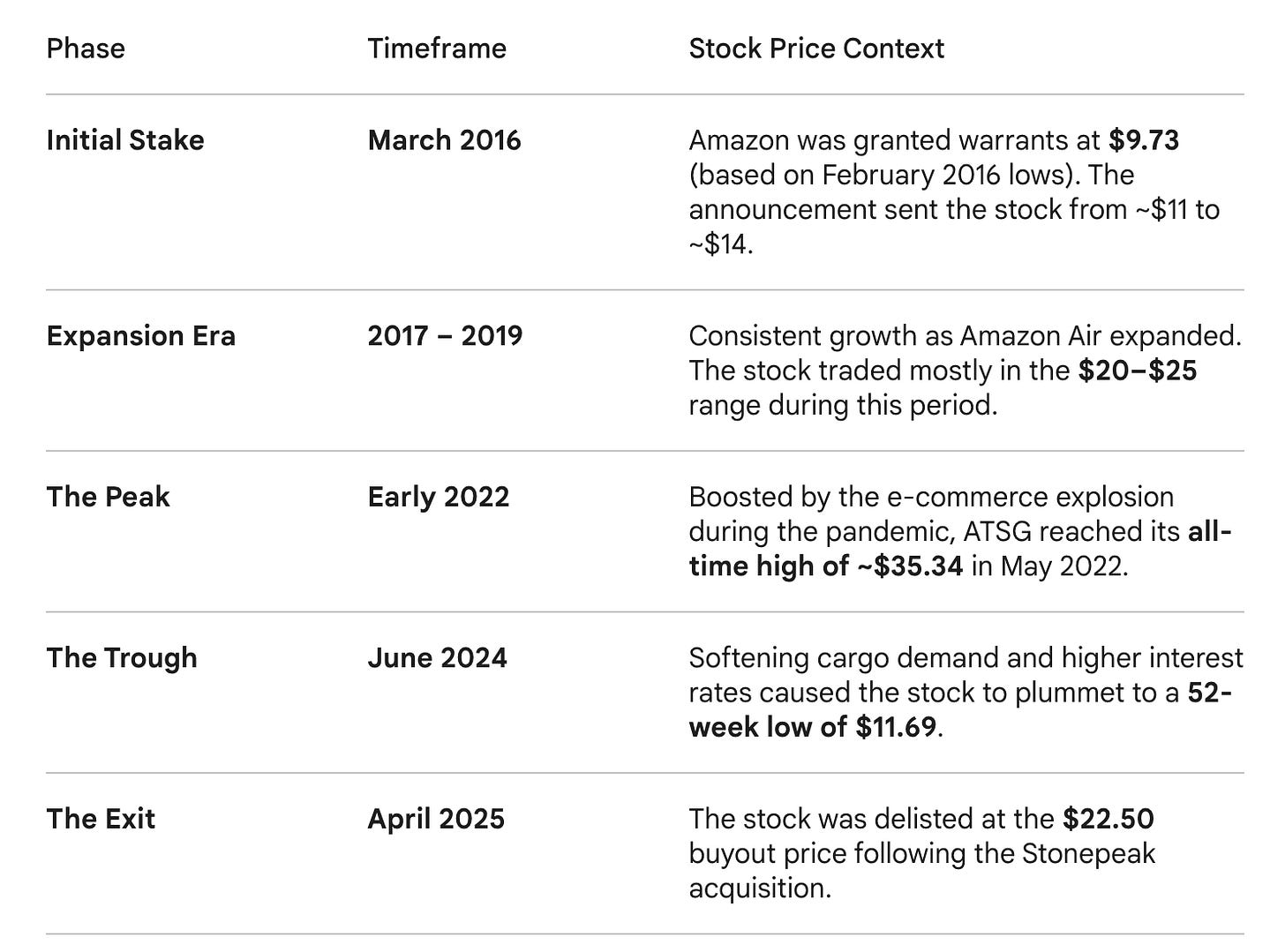

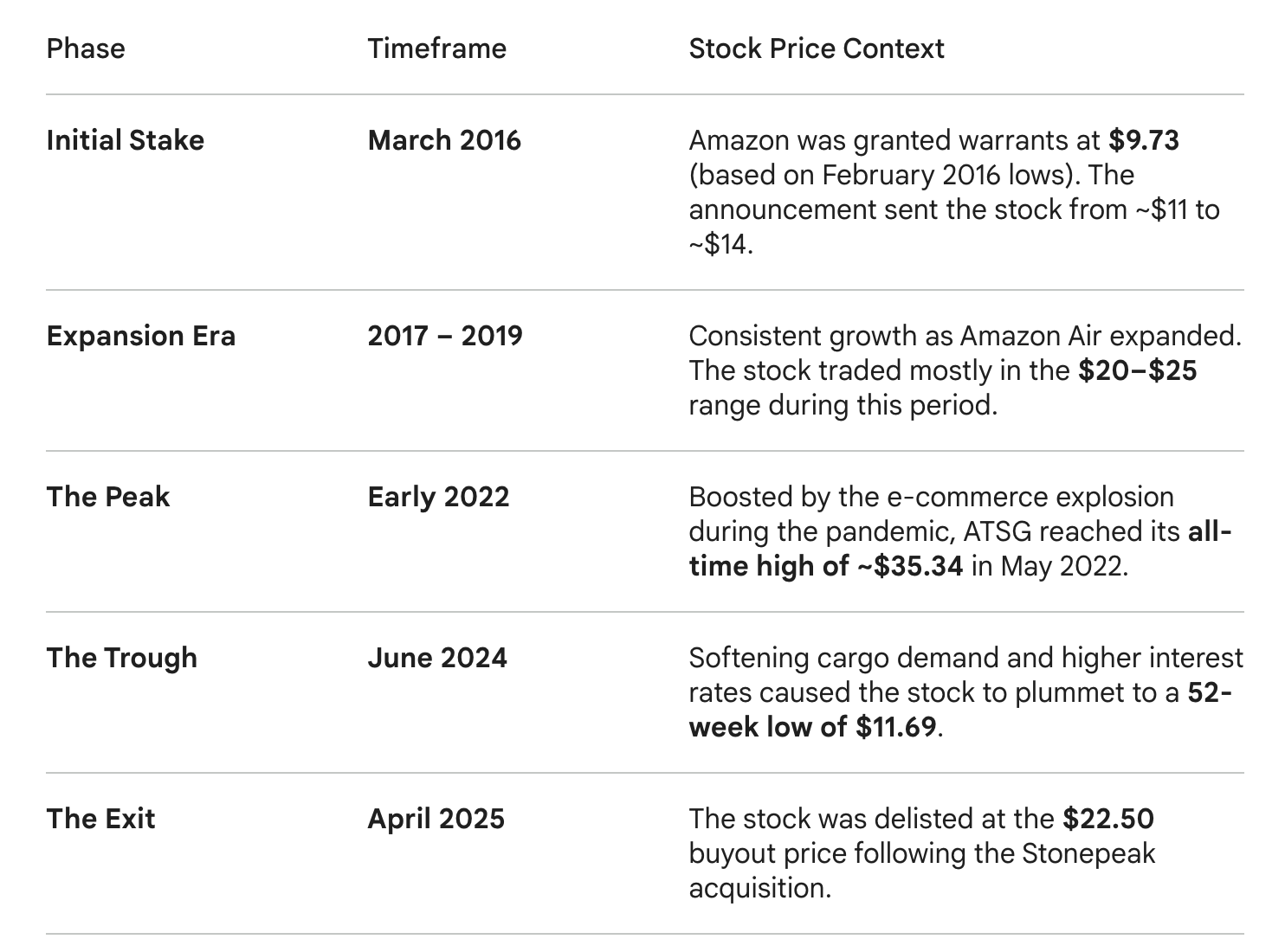

Amazon & the Warrant Strategy: Amazon has perfected a very aggressive form of the toehold. They often take minority stakes – or warrants that can be converted into stakes – in their most critical infrastructure partners. One notable example is Air Transport Services Group (ATSG).

They have done similar moves with hydrogen fuel cell providers like Plug Power. Here we might also bring up Amazon’s grocery (ad)ventures: While the 100% acquisition of Whole Foods was a massive, headline–grabbing event, Amazon’s quieter moves in the grocery sector are even more indicative of the toehold strategy. I’ve noticed they frequently use warrants and strategic investments to align themselves with essential partners. For example, they secured the right to acquire a minority stake in SpartanNash, a major US grocery distributor and retailer, a move to integrate Amazon’s logistics with a massive, pre-existing food distribution network. They executed a similar strategy in India with Future Retail, where they took a minority position through a subsidiary to navigate complex regulatory environments. In both cases, the investment served as a "backdoor" into a difficult industry where local expertise and existing infrastructure are the primary moats. It allowed Amazon to "learn" the supermarket business from the inside before committing to a full-scale assault on the market.

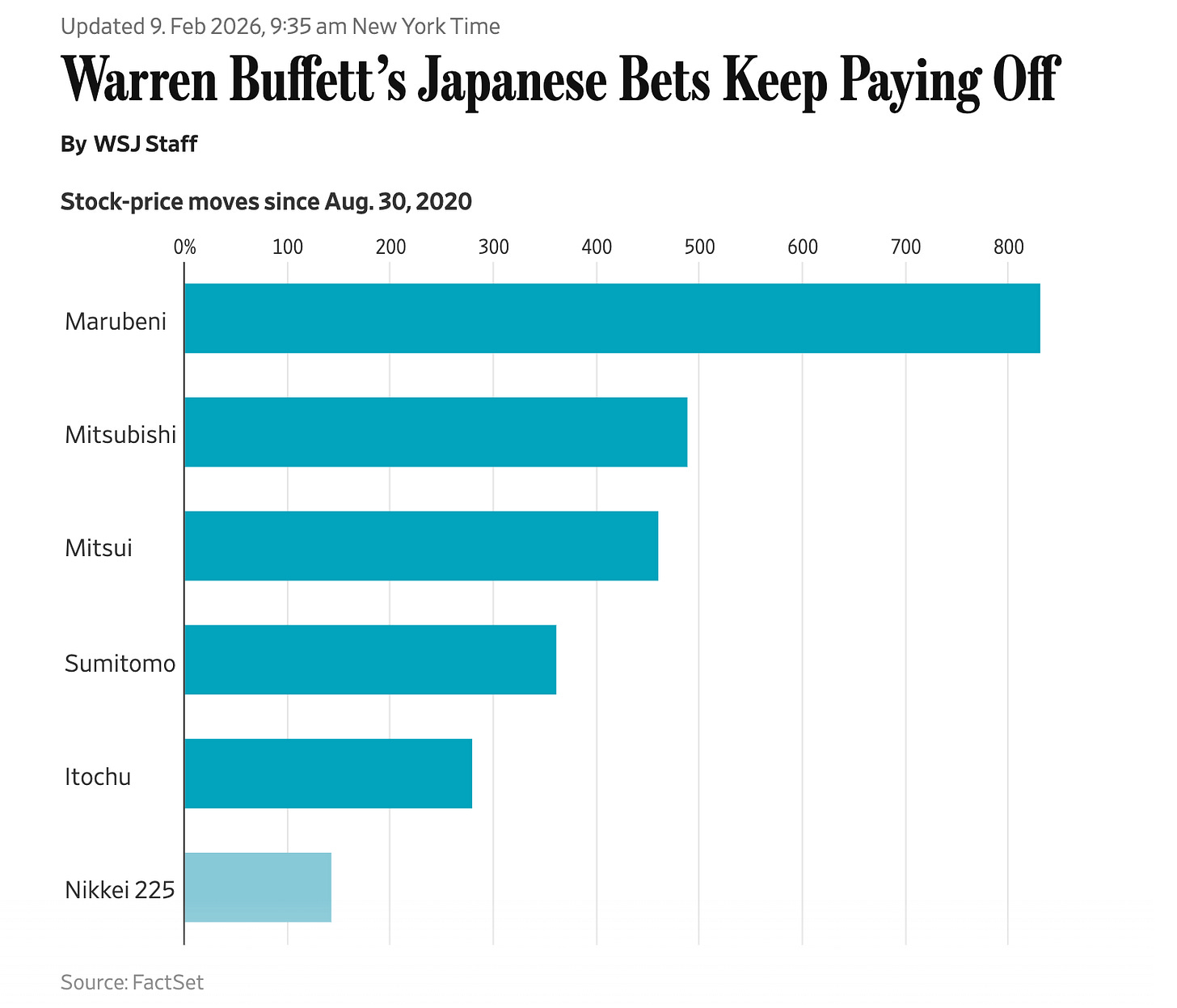

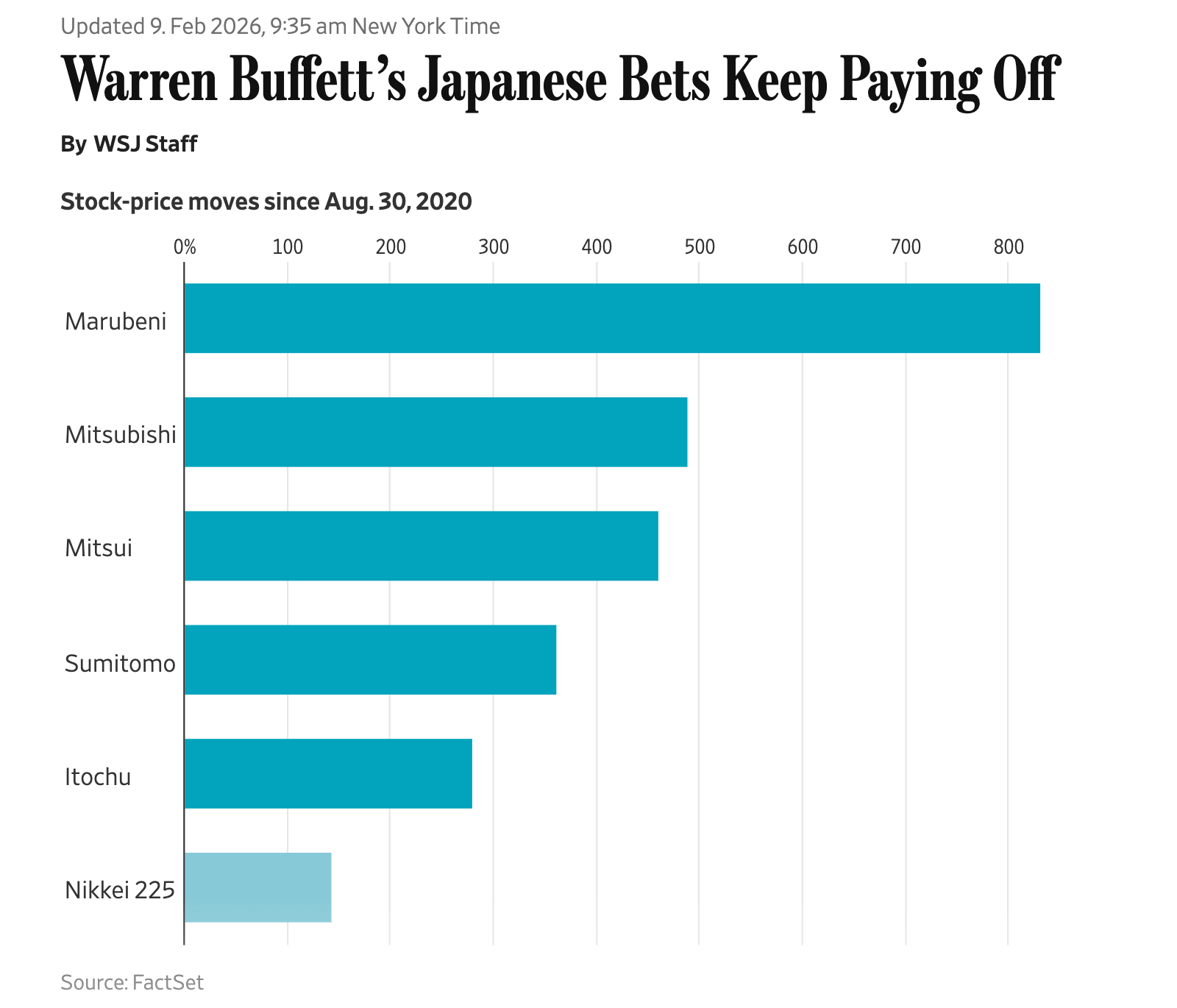

Berkshire Hathaway & the Japanese Sogo Shosha: In 2020, Warren Buffett announced that Berkshire had acquired 5% stakes in each of Japan’s five largest trading houses. It was a classic toehold. He signaled to the market that these were high–quality, undervalued “share cannibals.” Since then, he has slowly increased those stakes toward 9%, and the performance has been spectacular. It was a vote of confidence in an entire sector that the rest of the world had ignored.

Source: https://www.wsj.com/livecoverage/stock-market-today-dow-sp-500-nasdaq-02-09-2026/card/warren-buffett-s-japanese-bets-keep-paying-off-bFA45Z0A3PRqnBOJAELO Volkswagen & XPeng: In the automotive world, the toehold is often a confession of a technological gap. VW recently took a 4.99% stake in the Chinese EV maker XPeng. This wasn’t because VW needed a financial investment; they needed XPeng’s software and E/E architecture for the Chinese market. For an investor, seeing one of the world’s largest legacy manufacturers pay for the “intelligence” of a smaller, younger peer is a massive signal of who actually owns the superior tech stack.

You could continue this list almost indefinitely. What strikes me about these examples is the asymmetry. As an investor, you don’t need to be right about the eventual acquisition to win. You just need to be right that the toehold signals a high–quality business with a long runway. If the acquisition happens, it’s a bonus – a “pop” in valuation that serves as the cherry on top; or sometimes, you might not even want the company to be acquired, as it hinders you from compounding with the company for decades to come.

So the key benefit of the returns comes from the operational validation that the toehold provides in the first place. It narrows your universe of potential investments down to the ones that have already been vetted by the best in the business.

Putting It Into Practice

To wrap up this piece, we need to move even further from the conceptual theory to the practical side of things. The logical next step is to institutionalize this signal by adding it to your formal investment checklist.

Every time you open a new filing or begin a deep dive into a small–cap name, you now want to find yourself asking a pointed question:

I have looked at the cap table to identify whether a strategic peer or a dominant industry competitor holds a non–controlling interest or warrants that serve as a validation signal for the company’s underlying technology or operational model. When was the position established and was it increased/decreased over time?

You might frame this in a few different ways.

Is there a sophisticated competitor holding a non–controlling interest that suggests a hidden technology transfer?

Does the ownership structure reveal an “unspoken” partnership that hasn’t yet hit the income statement?

Or, perhaps most provocatively: If I were the CEO of the industry leader, what do I see in this smaller challenger that I cannot build myself?

These questions serve as another “violent filter.” They force me to look for the “smart money” that isn’t just looking for a quick trade, but for a structural, long–term advantage, and that may actively contribute to the thesis playing out; it’s a silent vote of confidence before it becomes common knowledge.

In one’s investing routine, this fits perfectly into the “turning over a lot of rocks” philosophy famously championed by Peter Lynch. As he often said, the person who turns over the most rocks wins the game. Your process maybe should include a mandatory stop at the ownership tables for every single company you look at.

I’ve found that tools like Koyfin make this process incredibly frictionless. Instead of wasting ten minutes digging through a dense proxy statement to find the relevant tables, I can pull up the institutional and insider ownership instantly.

I use my common sense. I look for the anomalies. If I see a tier–one competitor or a world–class strategic partner holding a 4.9% stake, my interest is immediately piqued.

I want to know since when and why they are there.

It should become a simple habit, but one that has the potential to reveal massive outliers that the rest of the market is ignoring because they are too busy looking at the quarterly earnings beats.

Another highly effective way to generate new investment ideas is to reverse the process entirely. Instead of searching for the toehold in a vacuum, you may start by identifying companies with what Mohnish Pabrai calls "Spawner DNA" – the rare breed of organizations like Amazon, Tencent, or even Nvidia that are culturally programmed to plant strategic seeds.

Look directly at the publicly traded minority investments these giants have made.

If you share this post with like-minded investors who may find value in this piece, it helps to spread the word 🙏🏻