South Sea Bubble 2.0? Notes from the 2026 Fundsmith AGM

Why Your Index Fund Might Be a Ticking Time Bomb

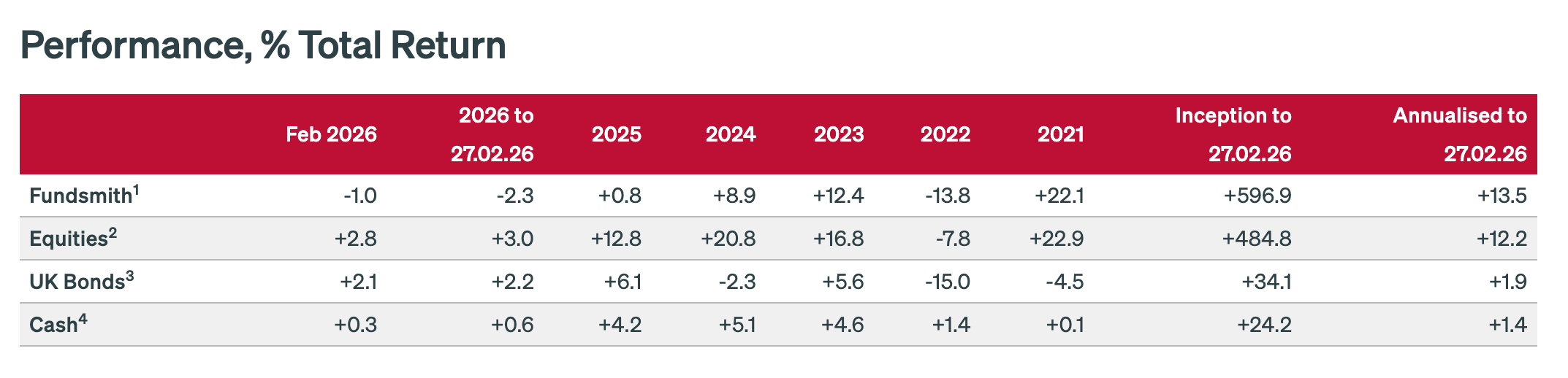

To me, it seems as if Terry Smith is currently the favorite punching bag of the value investing community. It is a role he seems to accept with a mixture of dry wit and a stubborn refusal to pivot. After a significant period of underperformance, his “Quality” strategy is under heavy fire from the usual suspects in the financial press.

I’ve noticed a curious phenomenon that repeats every cycle: price drives narrative. When a fund is soaring, every investor is a cheerleader, but when it stalls, the silence is deafening. My X feed used to be littered with Fundsmith content during the peak of the quality bubble a few years ago, yet today I see … nothing.

It is as if the investing community has collective amnesia regarding the principles that made Smith legendary. But if you actually take the time to watch the 2026 Annual General Meeting, you won’t find a man in retreat. Instead, you’ll encounter one of the most rational voices in a market that feels increasingly unhinged.

While much of the world is currently drunk on AI hype, Terry is soberly dissecting the data and looking back at 1929 and 2000 for clues on what happens next.

“So why study history? We study history not to know the future but to widen our horizons, to understand that our present situation is neither natural nor inevitable, and that we consequently have many more possibilities before us than we imagine.” - Yuval Noah Harari

He didn’t mince words during the opening of the meeting. “The one [word] I would use to describe it for the last 12 months is poor,” he admitted, “if we keep going like that we will all become poor.”

It was a refreshingly honest take in an industry where managers usually bury bad numbers under a mountain of jargon. He isn’t making excuses, even as the “commentariat” accuses him of precisely that.

He’s providing context. He emphasized that “what will determine the outcome... is not what’s happened in the last 12 months but what we do in the next 12 years.” I find that perspective invaluable. He has clearly internalized the timeless principles that work over decades, even if they hit rough patches in between.

In this post, I’ll explore the five most thought–provoking insights from this year’s session and why Terry is willing to look like a “loser” today to avoid the carnage tomorrow.

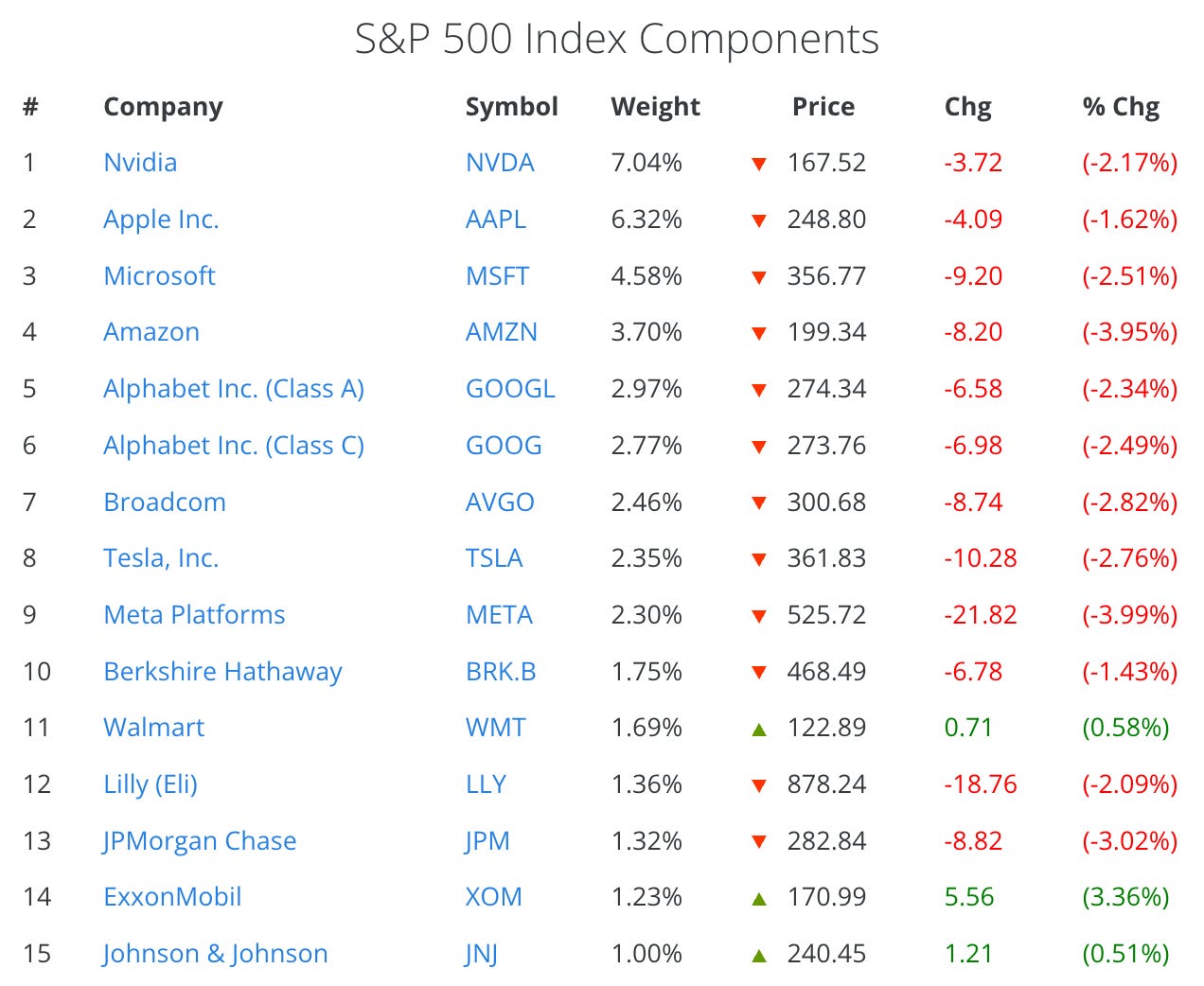

#1 – Why Global Giants are Suddenly Trading Like Penny Stocks

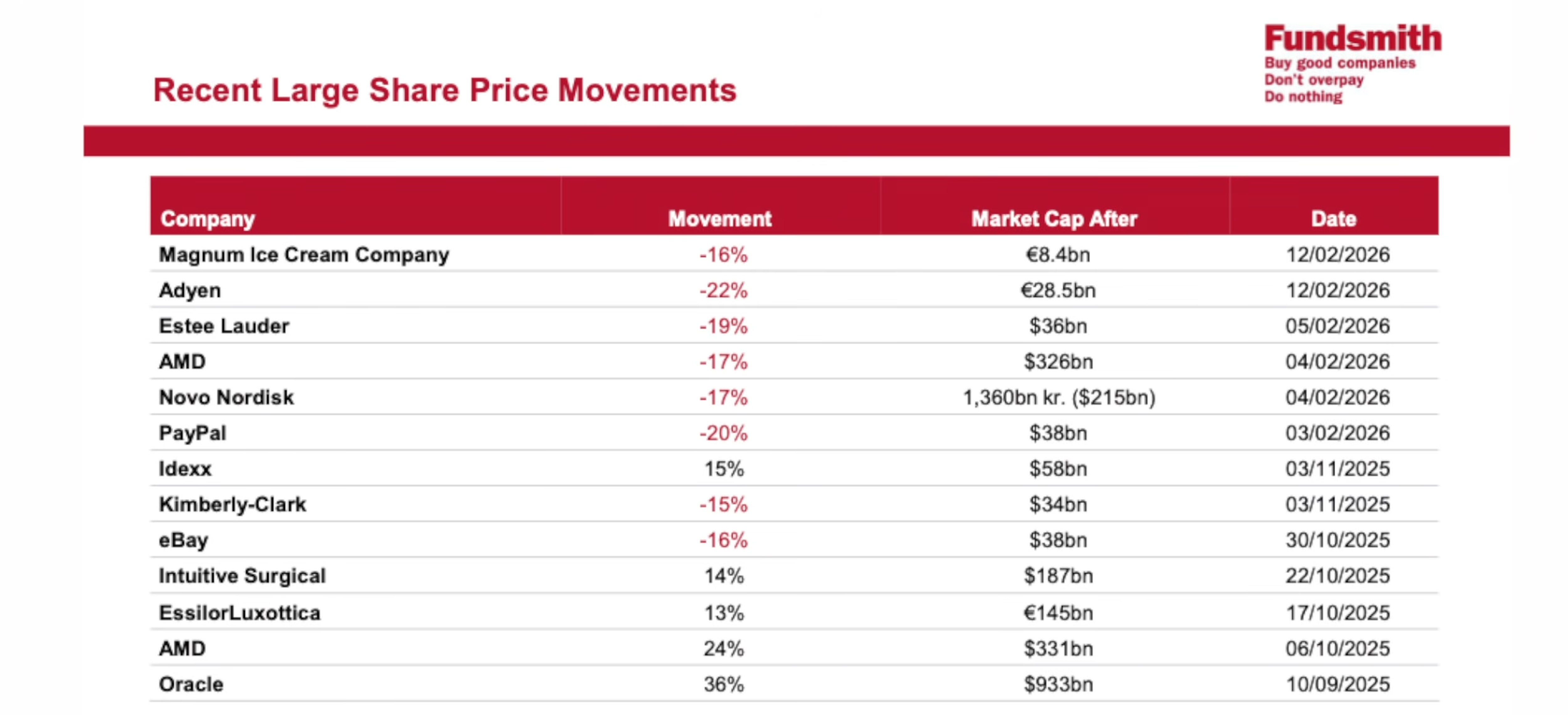

Something about the market’s current structure feels fundamentally off to Smith. It should feel off to you, too. We have reached a point where multi–billion dollar daily moves in single stocks – once once–in–a–generation anomalies – have become routine. It certainly feels this way to me. And the data Smith presented was confirming this “hunch”: More recently, Adyen fell 22% in a single session, Oracle surged 36%, Estée Lauder dropped 19%, and AMD saw a 17% slide.

These aren’t speculative penny stocks; they are some of the largest enterprises on the planet. As Terry noted with his characteristic bluntness, “Something’s not right when a multi–billion dollar company’s share price can move 36% in a day”.

This isn’t just volatility in the traditional sense. It is a structural failure driven by what academics call the “Inelastic Markets Hypothesis.” Because more than half of all equity assets are now held in passive index funds, there may simply not enough active liquidity to settle the price fairly. Index funds are mandated to buy or sell regardless of valuation, which creates a massive imbalance. Smith pointed to research by Gabaix and Koijen suggesting a multiplier effect of roughly 5x – meaning every dollar of active trading can impact a company’s market cap by five dollars.

“You know, if I go and sell Microsoft this evening and put it all into PepsiCo tomorrow, it doesn’t aQect the valuation of either Microsoft or PepsiCo. It’s unaffected. However, these people have looked at the data and discovered that the actual market impact for a dollar going from one security to another in recent years has been a multiplier of somewhere between three and eight times. So when you took your money out of us and the dollar went into Nvidia, the effect on the Nvidia price was somewhere between $3 and $8 on average $5 between those. That’s a startling number.

And the reason for it is, as I tried to explain in the in the title, the inelastic markets hypothesis, because the well, if you take the dollar out of their out of our fund and put it in the passive fund, it doesn’t make any difference. works providing there are people in a in a position to take the opposite view. So if you think that something is vastly overvalued uh it can by being driven by the momentum of index funds that will be bought down to earth by people who are running active funds who will sell it or even short it in the case of hedge funds. What they’re pointing out is there are increasingly fewer of those people because of the rise of index funds. There are increasingly fewer active funds to do that. And even within those active funds, there are an awful lot of people who’ve become index closet index trackers. They’re running an active fund, but they stay pretty damn close to the index for for survival reasons.”

I have read that markets remain theoretically efficient as long as roughly 10–15% of assets are still actively managed (I cannot recall the exact figure), since passive funds are, by nature, price agnostic. But that theory feels increasingly detached from the reality I’m seeing on the ground. It isn’t just the sheer volume of indexing that is the problem; it is the changing nature of the remaining active capital. The rise of multi–strategy “pod shops” and high–frequency players has likely shifted the remaining active liquidity from long–term price discovery to short–term momentum chasing. We discussed these changes in market structure in the series below:

Playing a Different Game: When Fundamentals Aren’t Enough Anymore! (Part 1)

This will be a 3-part series. If you don’t want to miss the follow-up pieces, make sure to subscribe to the blog.

Julian Robins touched on this when he described the current environment as a “feedback loop on steroids.” When everyone is crowded into the same few names, and even the “active” players are often just front–running index flows or managing tight risk limits in a pod, the traditional stabilizer is gone. As Terry put it, there are “increasingly fewer of those people” left in a position to take the opposite view and sell an overvalued stock. We are witnessing a new, much more dangerous arena where price discovery has been sacrificed at the altar of indexing.

#2 – The Seduction of Performance Chasing

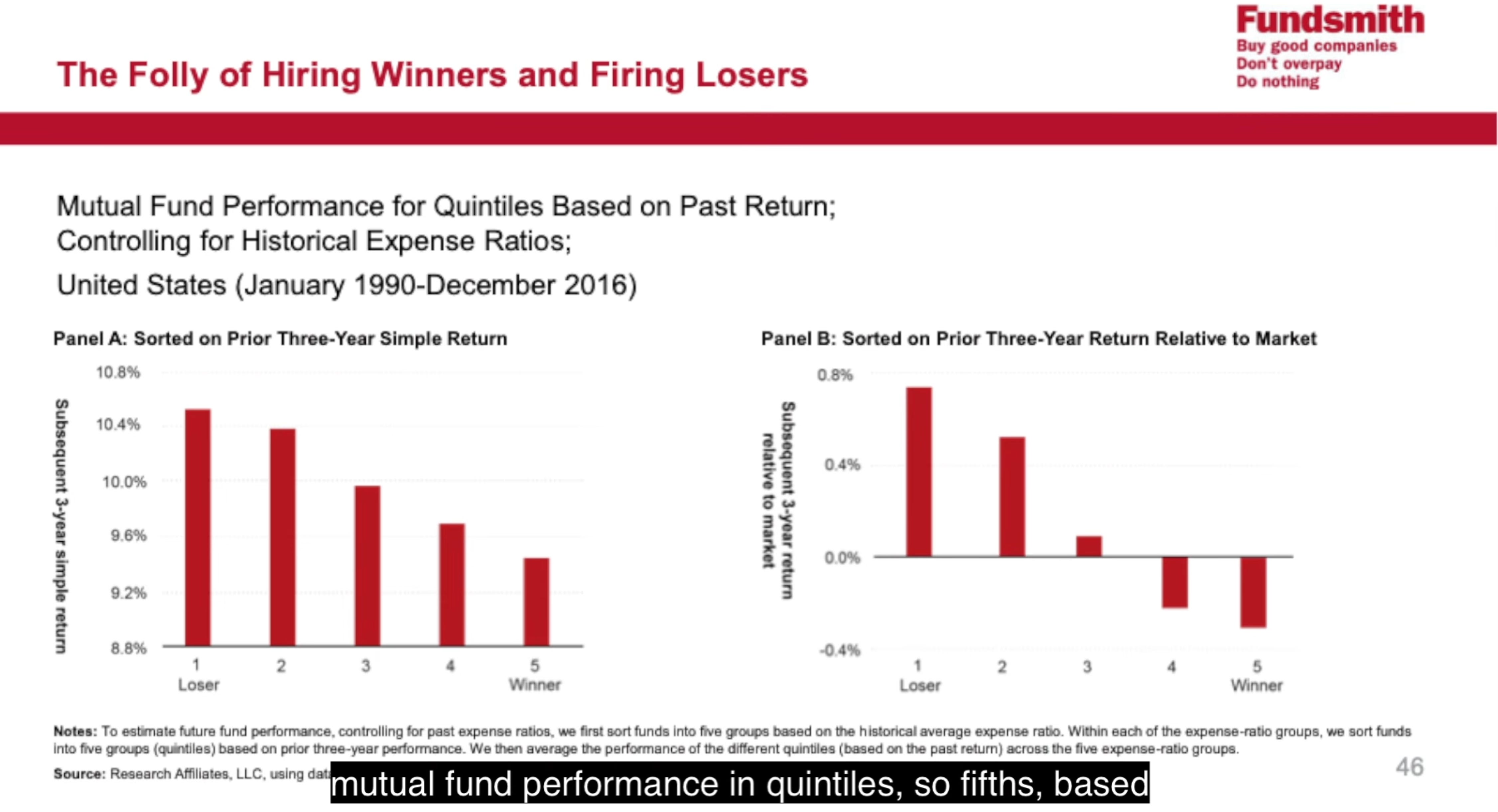

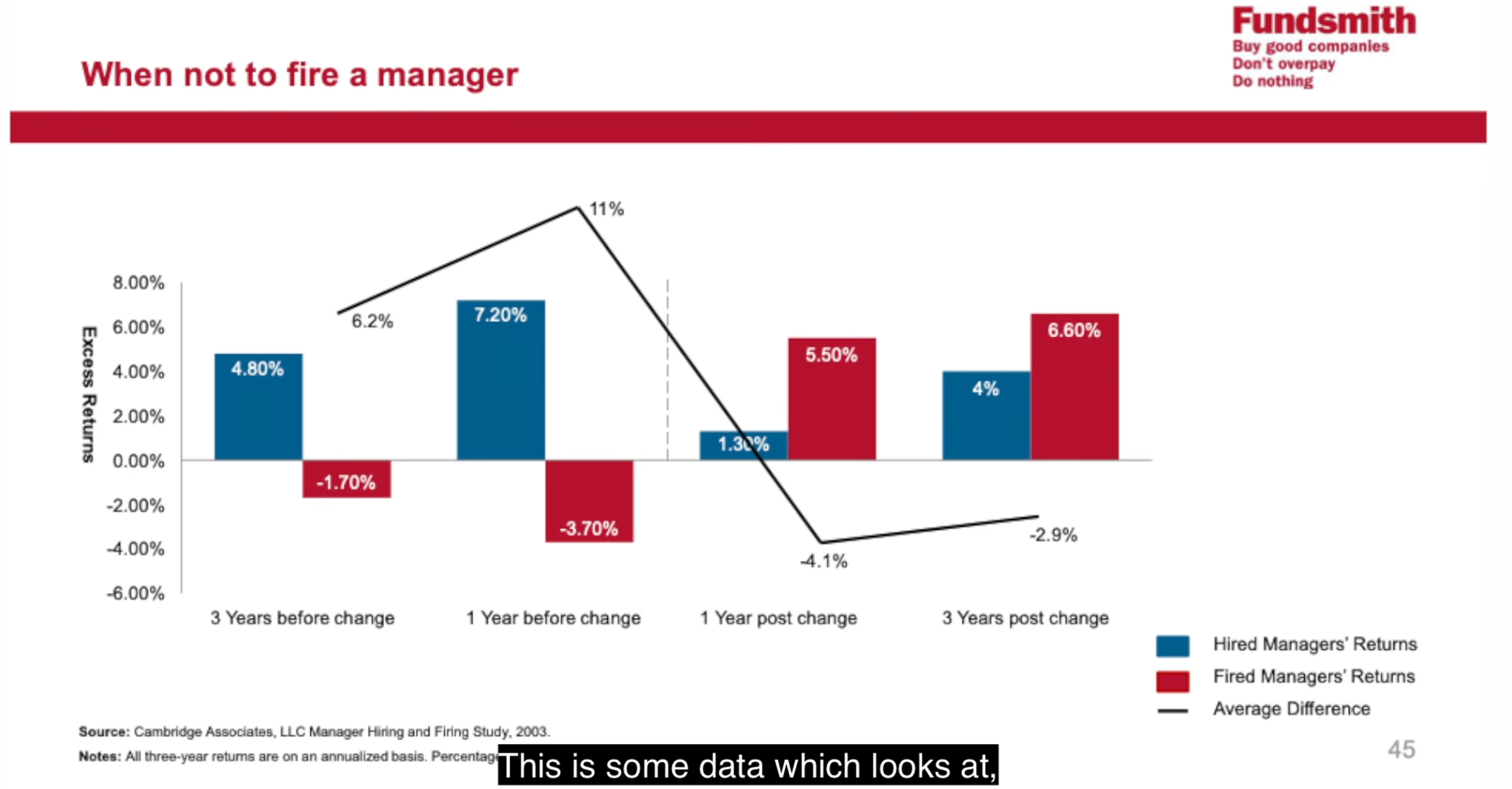

I have always found it fascinating how investors treat fund managers like football coaches – as soon as you have a bad season, the fans want you sacked. This “hire the winners and fire the losers” mentality is the most common way to destroy wealth in the long run.

During the meeting, Terry shared a chart that should probably be pinned to the monitor of every retail investor in the country. It showed that the top–performing quintile of funds over a three–year period often becomes the worst–performing group in the following three years.

Mean reversion is not just a theory; it is a brutal, impartial law of finance. As Terry dryly noted, “It’s a very natural human reaction to want to move to what’s working now, but in investment, that’s usually a recipe for disaster.”

You see this happen every time a specific style–be it Value, Growth, or Quality–goes out of favor for a few quarters. The pressure to pivot is immense.

It isn’t just about the numbers; it is about the psychological toll of underperforming when everyone else seems to be getting rich on something you don’t own. You start to doubt the process.

“Question: ‘Is the most diQicult part of underperforming a benchmark the psychological pressure of doing something different to catch up?’

Answer: […] Yes, it is a simple answer… look, […] it’s better in career terms to fail conventionally than is to succeed unconventionally. Because even if you’re successful, I mean, you saw during the 10 years when we were doing very well in the lead up to this, the amount of criticism that we got then for doing something different … and now it’s just easier to criticize because you’re doing something different and it doesn’t work. But yeah, the psychological pressure is considerable.“

You wonder if the “Quality” factor has finally been “solved” by the market or rendered obsolete by new technology. But as Smith argued during the Q&A, the moment you pivot to chase the current fad is the exact moment you lock in your relative underperformance.

Julian Robins reinforced this, pointing out that “most investors spend their lives running toward where the puck was, rather than where it is going.”

Smith remains incredibly disciplined here. He is willing to look like a “loser” today because he knows that today’s laggards are often tomorrow’s leaders, provided the underlying business quality remains intact. He knows that “if we keep going like that we will all become poor,” but he also knows that the cure is not to chase the latest high–flyer, but to wait for the inevitable return to the mean.

One of the most telling moments was when Terry addressed the “commentariat” and the critics who claim he has lost his touch. He didn’t offer a complicated defense. He simply pointed back to the historical data. He mentioned that “what will determine the outcome... is not what’s happened in the last 12 months but what we do in the next 12 years.” It takes a certain kind of professional arrogance – the good kind – to stand in front of a room of disappointed shareholders and tell them that the best thing they can do is absolutely nothing.

You have to admire the conviction, even if it makes for a boring headline. Most people can’t handle the boredom of a winning strategy when it hits a rough patch. Terry can.

#3 – The Great Infrastructure Gamble

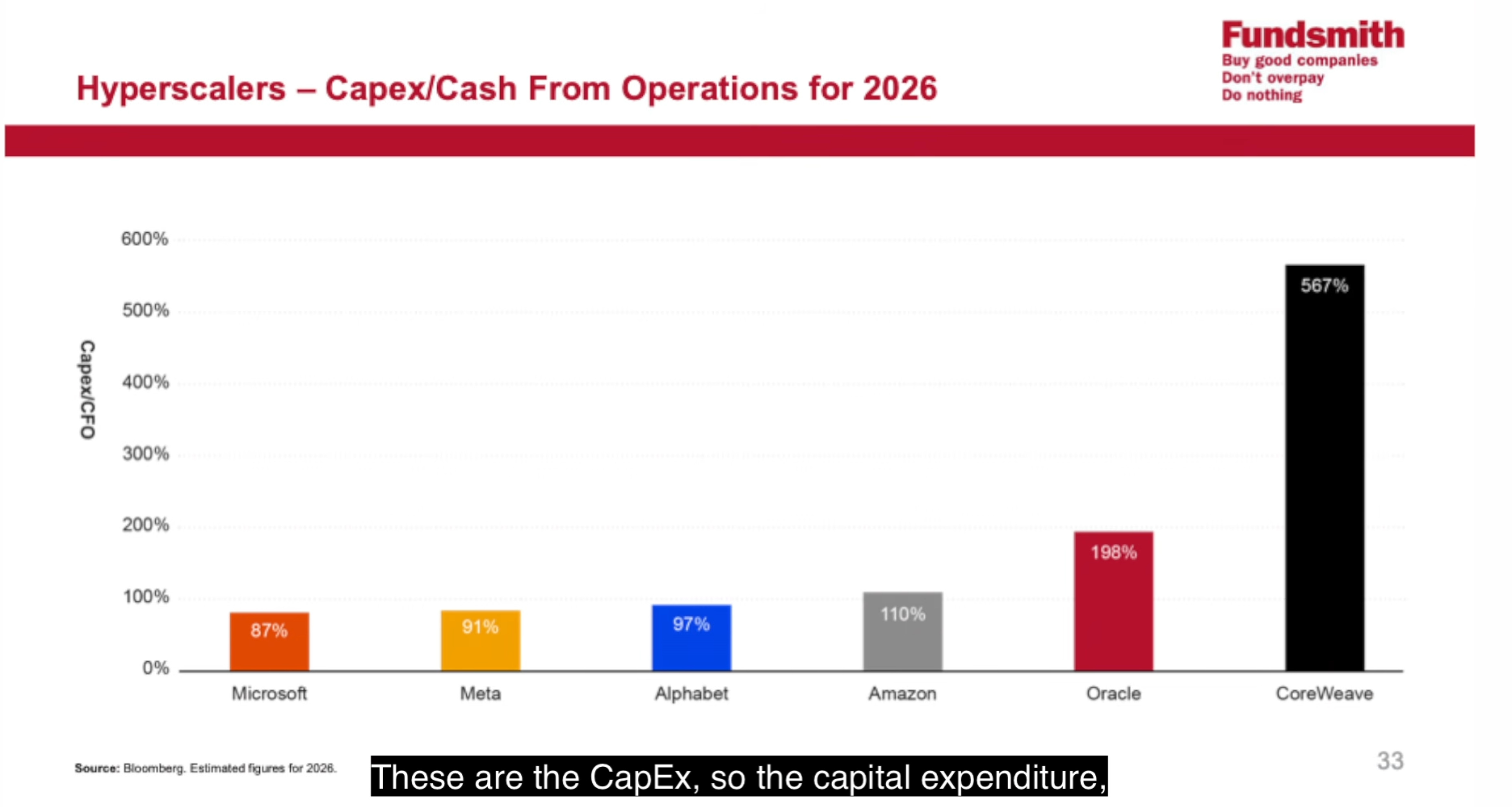

The sheer scale of the current AI infrastructure build–out is difficult to comprehend until you look at the capital expenditure (Capex) relative to operating cash flow. We are witnessing a high–stakes gamble where the world’s largest companies are betting their entire cash piles – and then some – on a future that has yet to materialize in the bottom line.

I was particularly struck by the “Capex vs. Cash from Operations” ratio Terry presented. While Microsoft and Meta are reinvesting roughly 90% of their operating cash back into the business, others have moved into the realm of the truly extraordinary. Oracle is spending nearly double its operating cash (198%), while the private cloud provider CoreWeave is at a staggering 567%. This isn’t just growth; it is an all–in bet on an AI arms race that requires massive external financing to sustain.

This level of spending has real–world consequences for fund construction, most notably the triming of Microsoft from Fundsmith’s Top 10 holdings. This was a move that raised many eyebrows in the room. Terry was candid about the rationale, stating, “Microsoft has moved out of our top 10 for the first time in many years... It’s really to do with the amount of money they’re spending.” He is clearly worried that the relentless pursuit of AI dominance is beginning to erode the very thing that made these companies “Quality” in the first place: their superior Return on Capital Employed (ROCE). When you are spending 90% of your cash just to stay in the race, your ability to generate excess returns for shareholders is naturally diminished.

“… we did so because of concerns about what we’re seeing sitting there in terms of the spending and we’re seeing $600 billion […] if we’re looking for a 30% return on capital say um you know those companies are going to need to generate $180 billion of new cash flow not from the things that they’ve already got not by cannibalizing what they already have to justify that in terms of return on capital … that’s quite a lot actually and at the moment we’re not really paying for AI mostly … we’re users of it … and we are paying but not not to anything like a degree that could possibly justify that and we are probably unusual in paying because we’re a business most consumers are probably not paying at all. I mean, as a consumer, I don’t pay for using it. Um, and um, so that’s tricky.

And I know there have been models historically where people have given you things and got you hooked on them and then later on told you what the price is uh, and started to make lots of money from it, but they’re relatively unusual and they do usually involve the person who manages to accomplish that achieving a dominant position in the industry.“

The Oracle situation is even more fascinating. It seems driven by a fear of past failures as much as a hope for future gains. As Terry dryly noted during the Q&A, “Larry Ellison... is not going to miss the cloud twice.” It is a classic example of corporate FOMO (Fear of Missing Out) played out on a multi–billion dollar stage.

During the discussion, Julian Robins pointed out that we are essentially in a gold rush where the only people currently making guaranteed money are those selling the “picks and shovels” – namely Nvidia. For the rest, the path to profitability remains obscured by a mountain of expensive GPUs.

I find it telling that Smith is willing to walk away from a long–term winner like Microsoft because the math of the AI cycle no longer squares with his requirement for capital efficiency.

‘“We’re not AI deniers.” - Terry Smith

It is a lonely position to take, but one rooted firmly in a timeless investing principle.

Before we dive back in, a quick note…

Want to compound your knowledge – and your wealth? Compound with René is for investors who think in decades, not headlines. If you’ve found value here, subscribing is the best way to stay in the loop, sharpen your thinking, avoid costly mistakes, and build long-term success – and to show that this kind of long-term, no-hype investing content is valuable.

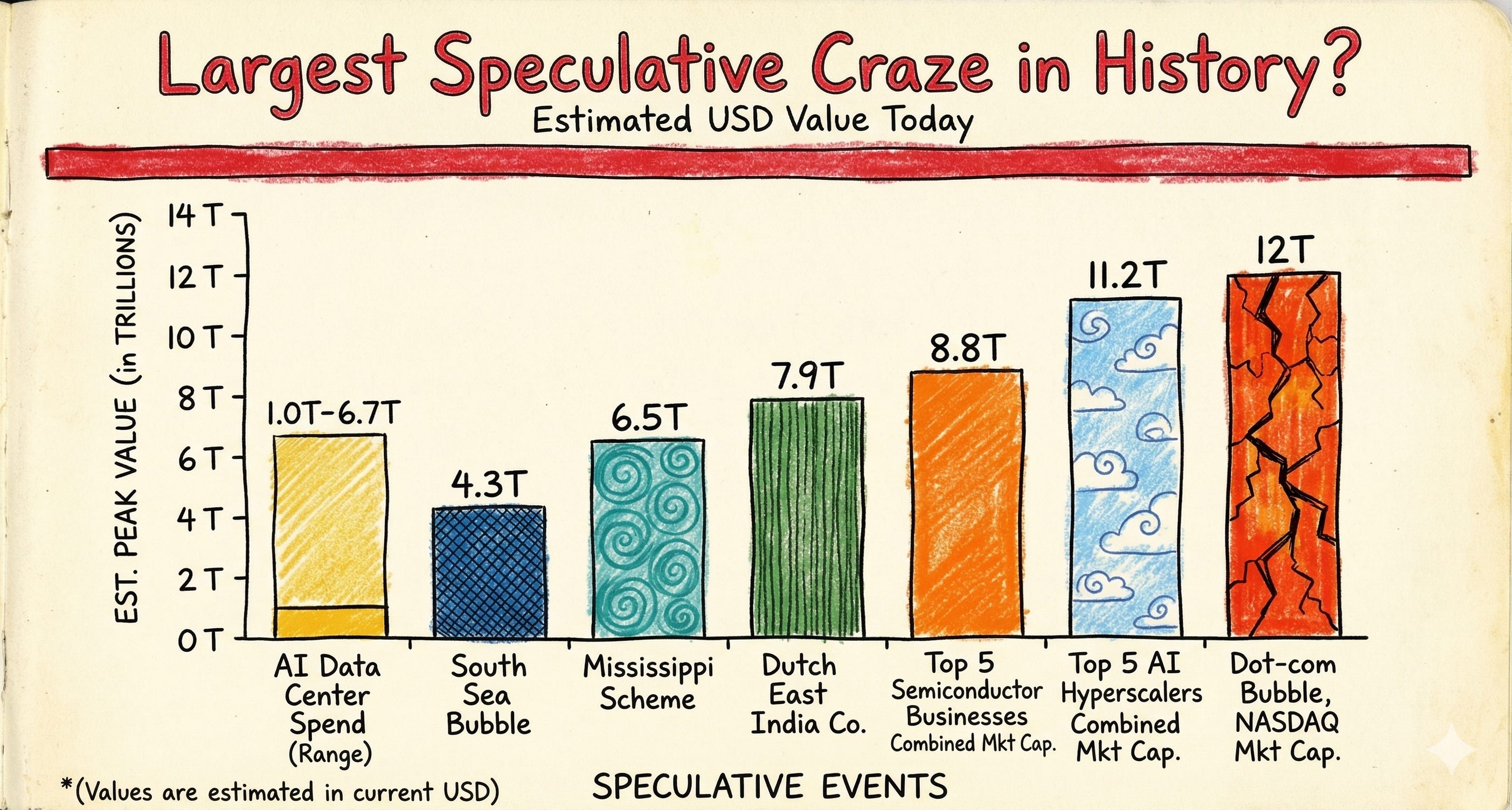

#4 – Echoes of the South Sea Bubble?

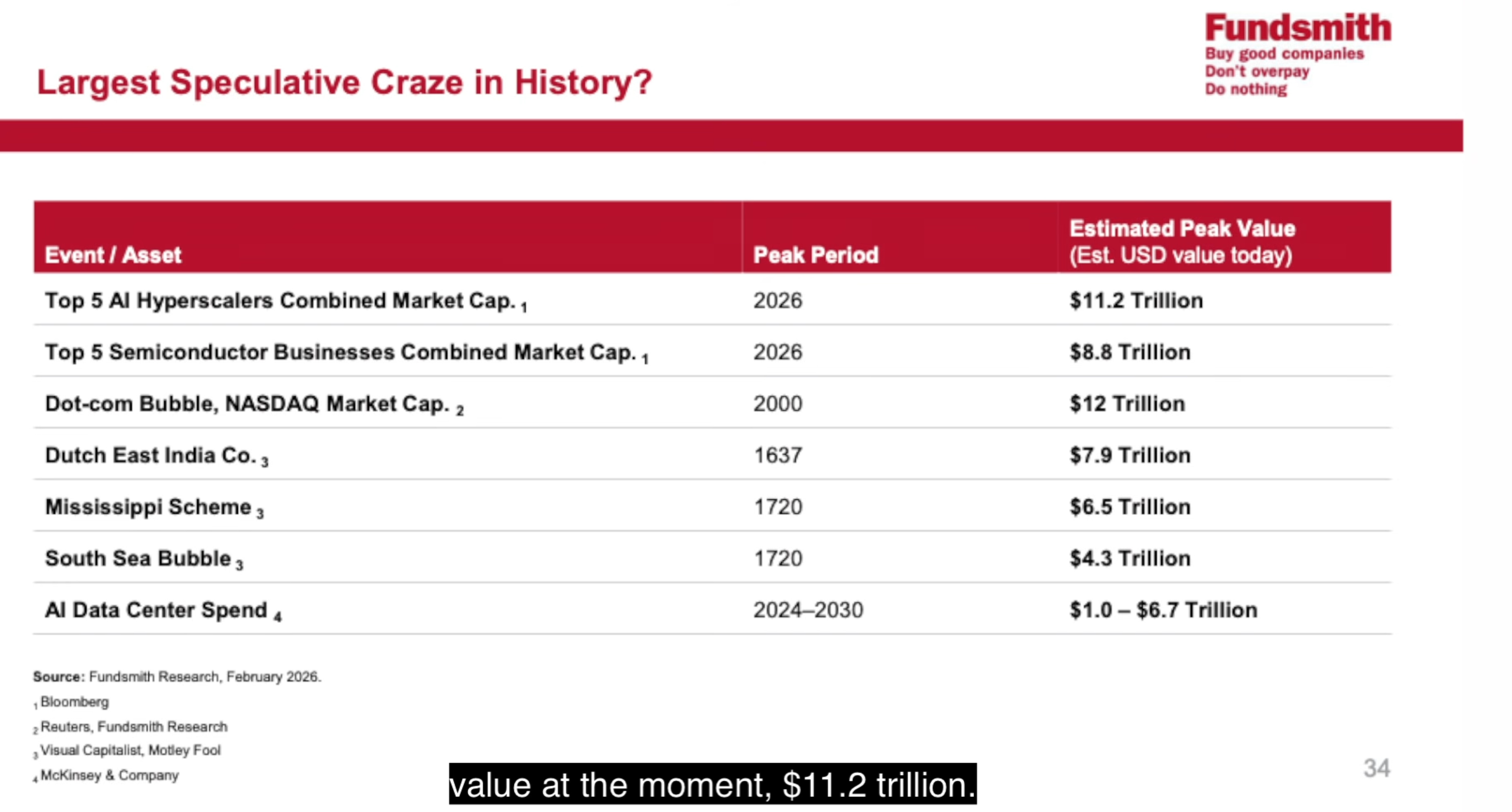

If the Capex figures I just mentioned represent the “hope” part of the current market equation, the valuations represent the hallucination.

We have moved beyond simple optimism into a territory that history suggests is rarely sustainable. The combined market cap of the top five AI hyperscalers has reached a dizzying $11.2 trillion.

To put that in perspective, Terry shared a slide that adjusted historical speculative manias for inflation, and the results were chilling. Even the legendary South Sea Bubble of 1720 and the Mississippi Scheme – the gold standards for financial insanity – look relatively modest by comparison. We aren’t just looking at a sector–specific rally; we are looking at a historic concentration of capital that rivals the absolute peak of the 2000 Dot–com bubble.

As Julian Robins noted during the session, “We have reached a level of concentration where the top few stocks are effectively the market, and that has never ended well for the latecomers.”

Terry’s skepticism isn’t born of a dislike for technology, but of a deep respect for the lessons of historical cycles. He highlighted that while the “new era” proponents claim this time is different because of the massive cash flows, the valuation multiples are reaching levels where the math simply stops working.

The math shared above is a sobering reality check. You have to ask yourself if you’re comfortable holding the bag when the narrative finally catches up to the numbers. I suspect many investors today are so blinded by the potential of AI that they’ve forgotten that even the best companies can be terrible investments if you pay the wrong price.

Smith seems perfectly content to sit on the sidelines of this particular mania, even if it means underperforming while the bubble continues to inflate. As he put it, “I’m quite happy to look like an idiot for a while if it means I don’t go over the cliff with everyone else”.

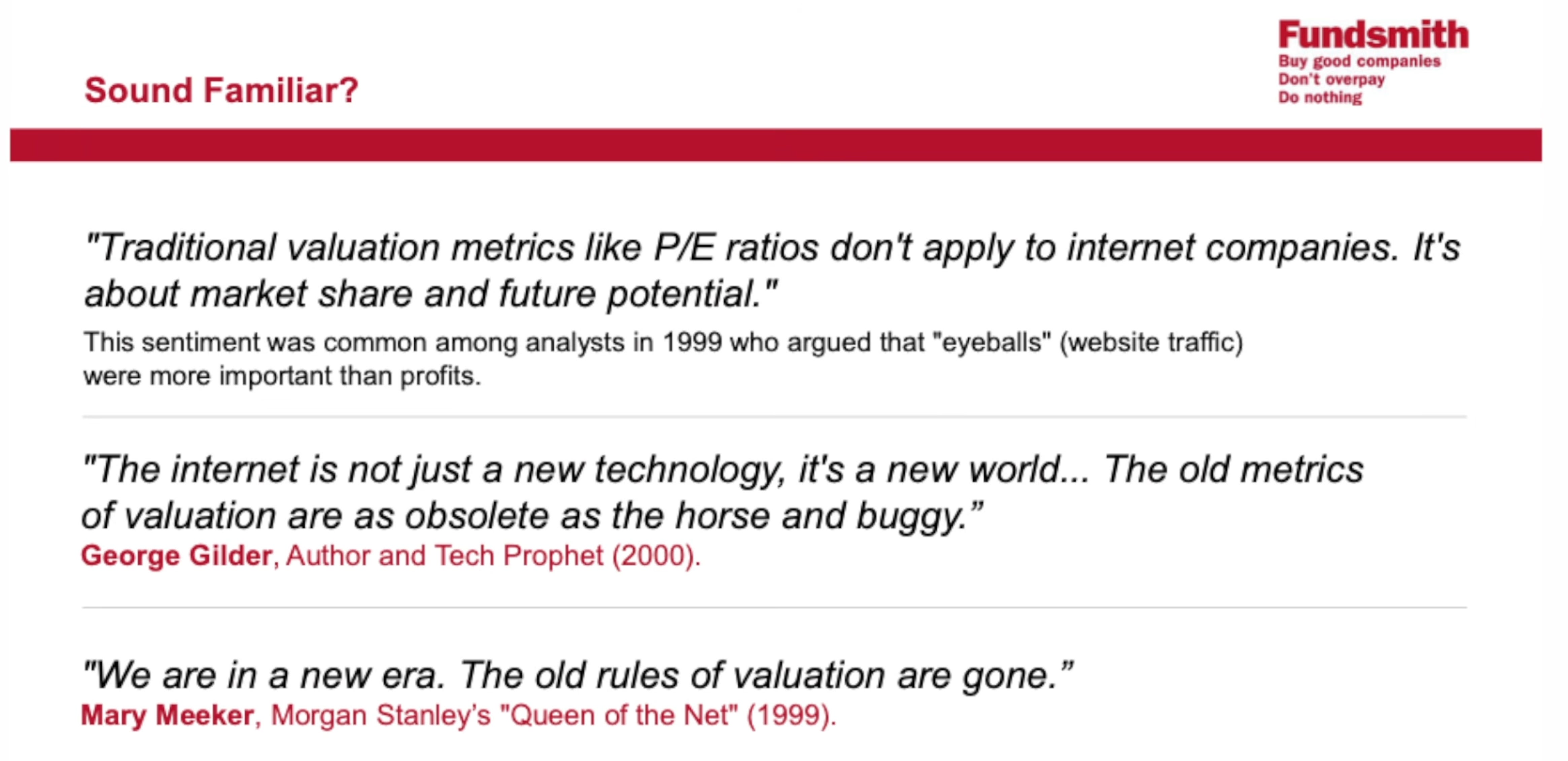

#5 – Paying 1999 Prices?

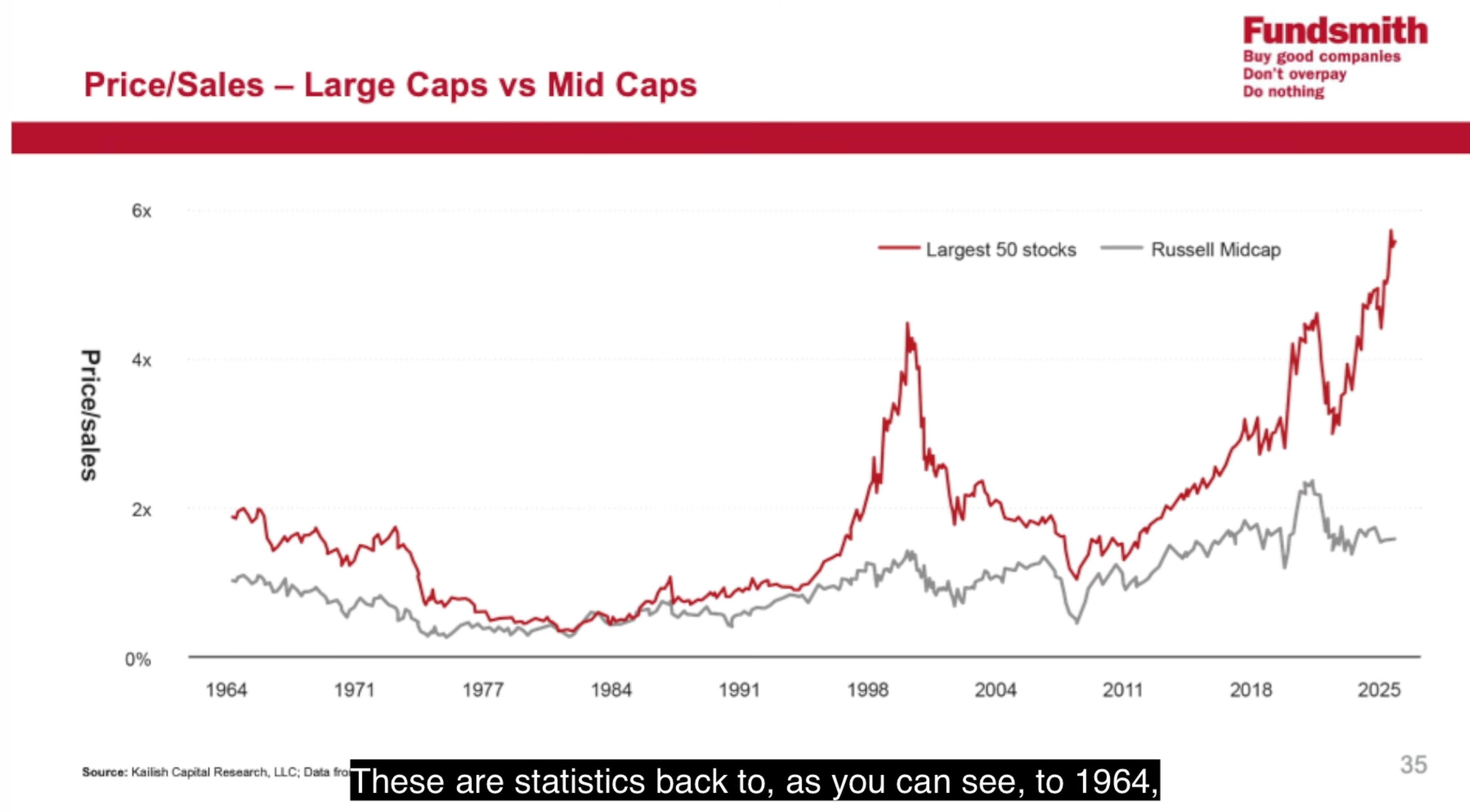

It is one thing to talk about trillion–dollar market caps in the abstract, but it’s quite another to see what investors are actually paying for every dollar of revenue. Price–to–sales is often the last metric people look at during a bull market because it is the hardest to justify with clever accounting or “adjusted” earnings. Or if you go one step further, you’d attempt to “value” businesses based on the TAM potential or other fancy metrics.

During the meeting, Smith pulled up another interesting chart that should make anyone with a memory of the year 2000 feel a bit nauseous. The Price/Sales ratio for the largest 50 stocks in the S&P 500 has effectively completed a round trip back to the peak of the Dot–com bubble. We are paying as much for a dollar of sales today as we were when the market was at its most “irrational” point in modern history. Sure, a few things have changed, businesses are even leaner and more profitable, and they often operate globally, but many investors have expressed concerns about “peak margins” and the trend of de-globalization should be obvious to anyone by now.

Hence, this is a historic divergence. The gap between the giants and the rest of the market is no longer a small crack; it is a canyon.

As Terry noted during the presentation,

“We are seeing a return to the sort of valuation levels for the largest companies that we last saw in 1999 and 2000.”

It was a simple statement delivered without hyperbole, which somehow made it more alarming. I’ve noticed that when people talk about the “Magnificent Seven” or the AI leaders, they always point to the cash flows – as we discussed earlier – but they ignore the price of admission.

Julian Robins was even more pointed during the Q&A when discussing the concentration risk. He remarked that “the market is currently paying a premium for size that defies historical precedent.” We are in a regime where being big is seen as a guarantee of safety, leading to a crowded trade where everyone is paying record prices for the same 50 names.

I think it is worth pausing on that. If you are buying the index today, you aren’t just buying “the market.” You are buying a highly concentrated bet on 50 companies at valuations that have historically preceded massive drawdowns.

It’s a game of musical chairs played at 1999 prices. Smith’s point is clear: the fundamentals might be better than they were in 2000, but the price you are paying for those fundamentals has reached a point of extreme fragility.

“History doesn’t repeat, but it rhymes,” he reminded the audience, and right now, the rhythm sounds a lot like a bubble about to burst.

Conclusion

I’ve sat through enough of these meetings to know when a manager is bluffing. Terry Smith isn’t bluffing. He is genuinely concerned about the mathematical reality of the current market. It is easy to dismiss him as a manager stuck in a bygone era, but the historical parallels he shared are simply too obvious, too fitting to ignore. We are living through a period of extreme concentration and valuation expansion that mirrors the most dangerous moments in financial history – from the South Sea Bubble to the peak of the Dot–com mania. I find his willingness to look like a “loser” today in order to avoid being a casualty tomorrow to be his greatest strength. It’s a lonely path, and it requires an iron stomach to watch the indices climb while you sit on the sidelines. But as 2000 taught us, survival is the ultimate form of alpha. I’m content to follow the lead of a man who would rather be wrong for a year than wrong for a decade.

Really interesting. This is not the first time I've read a serious critique of index fund investing. I have yet to hear of an alternative with a similar risk/reward profile.

Chris Hohn has operated during the same period as Terry Smith, bought quality names, and has not underperformed. It is possible that Terry Smith has simply made poor picks and overdiversified his fund. It can be easy to blame AI mania or passive funds for one's underperformace. Ultimately, long time scales of 5-10 years will reveal the truth.