Shameless Cloning 2.0: Pabrai’s Idea, Upgraded for 2026

Pabrai’s original insight still holds – but the way I clone in 2026 looks entirely different

A few of my most recent investments – Timee and InPost – started with me doing something many investors quietly do but few admit: shamelessly copying others.

I first came across Timee when Jake Barfield mentioned it in one of his investor letters a few months ago. I found the business intriguing but didn’t act immediately as I was less excited about the current share price. Then, when the stock dropped by almost 40% a few months later, I started digging in properly, using Barfield’s original analysis as the foundation for my own research.

Later, while chatting with Jake in the DMs on X, discussing Timee, the name InPost came up. Both businesses, Timee and InPost, we agreed, show signs of intense network activity – a dynamic that might be an expression of moat strength.

Until that moment, I had never even heard of InPost. But again I decided to be a shameless cloner and within days, I was deep into the filings, building my own thesis.

That sequence – one idea leading to another, sparked by someone else’s insight – perfectly captures the spirit of what I’m about to discuss in this post, but with a modern twist to it!

But let’s go back a few steps… A few years ago, Mohnish Pabrai said something that stuck with me: “I liberally swipe investing ideas from other value investors.” The first time you hear this idea, it may almost sound too simple. Surely great investors are original thinkers, right? They uncover hidden gems no one else sees, build models from scratch, and spend years studying industries others ignore. Right?

But then you realize – many of the greats are, in fact, world-class imitators. They study what works, internalize it, and apply it ruthlessly. Buffett cloned Ben Graham. Munger cloned Fisher. Akre cloned Buffett. And on it goes.

In a field obsessed with novelty, cloning feels like cheating. But the more you think about it, the more obvious it becomes: investing is a game of pattern recognition, not invention. Why waste years reinventing the wheel when you can stand on the shoulders of those who’ve already built a Ferrari?

“Start looking at what other people that you know and respect are buying.” - Charlie Munger

That’s what this post is about – re-examining what it means to be a modern shameless cloner. Not a lazy copycat, but an intelligent learner. Someone who understands that cloning, done thoughtfully, isn’t about outsourcing your thinking; it’s about compressing decades of experience into months of study.

Here’s what I’ll explore:

Where the idea of shameless cloning comes from – and why Mohnish Pabrai, Charlie Munger, and Warren Buffett all practiced it long before it had a name.

Why idea generation is the ultimate edge – and how cloning helps you turn over more rocks, faster, without sacrificing depth or originality.

How to clone intelligently – including which legendary investors are actually worth studying (spoiler: few are) and what to watch out for when interpreting their 13F filings.

The modern twist – how private investors today can go beyond the billion-dollar names to clone smaller, lesser-known managers who operate with fewer constraints and often more transparency.

Why cloning is not imitation but synthesis – how to build your own process around it, adapt it to your style, and use it as a framework for continuous learning.

The rest of this post is my attempt to capture what I’ve learned – and what I’m still learning – about shameless cloning in a world where every great investor leaves digital breadcrumbs behind.

The Cloner’s Mindset: Why Originality Is Overrated

In investing circles, few ideas have been as simultaneously misunderstood and underappreciated as “shameless cloning.” The phrase was popularized by Mohnish Pabrai, who has never been shy about borrowing ideas – whether from Warren Buffett, Charlie Munger, or other investors he admires. But cloning, as Pabrai defines it, isn’t mindless mimicry. It’s the disciplined practice of recognizing what works, understanding why it works, and then unapologetically applying it.

Pabrai himself copied Buffett’s original 0/6/25 partnership fee structure, built a concentrated, low-turnover portfolio inspired by the Buffett–Munger playbook, and even described his entire investing philosophy as “being a copycat at scale.” He’s quick to point out that the best ideas in life are almost never new; they’re just reinterpreted for a different context. Whether it’s the way you invest, structure your business, or even decide where to live and how to allocate your time, cloning the best versions of existing ideas can save years of unnecessary trial and error.

I’ve always found that liberating. In a world obsessed with originality, it feels almost rebellious to admit that the smartest thing you can often do as an investor might be to copy.

Most people equate imitation with intellectual laziness. But in markets – where the scoreboard never lies – it’s the results that matter, not whether the idea was “yours.”

If you can identify what works for those who have already proven their skill, why reinvent the wheel? As Charlie Munger once put it, “Warren has made a number of people rich who have just copied his investments.” The data backs him up. A study by researchers at the University of Nevada, Las Vegas, found that if you had started cloning Buffett’s trades one month after Berkshire’s public filings in 1976, you would have compounded at roughly 24% annually for the next 30 years. That’s an extraordinary outcome for someone doing little more than following a public trail.

But cloning is more than a shortcut to performance. It’s a mindset. It requires humility – the willingness to accept that others may be better equipped to find and analyze great businesses than you are. It also demands patience and discernment. You can’t copy just anyone. You need to filter for the few who’ve shown skill, integrity, and alignment with your own philosophy.

I often think of investing as a lifelong apprenticeship. The difference is that your mentors don’t even need to know you exist. The world is full of silent teachers: Buffett, Akre, Marks, Vinall, Klarman, and countless others who share their thinking in letters, interviews, and filings. Their decisions are public case studies waiting to be reverse-engineered. Learning from them is one of the greatest free lunches in finance – if you have the discipline to do the work.

“We look at what other people we respect own.” - John Fox

The irony is that cloning requires more thinking, not less. It’s easy to copy blindly, but it’s hard to copy intelligently. To do it well, you need to understand the reasoning behind each investment, not just the ticker. As they say, “you can borrow ideas, but you cannot borrow conviction.”

You must ask: what’s the thesis here? What are the key variables? What time horizon or risk tolerance does this investor operate under?

Once you’ve done that work, cloning becomes a framework for learning. It’s how you internalize others’ wisdom without paying the tuition of their mistakes.

That’s what being a modern shameless cloner is about. It’s not about giving up your individuality – it’s about anchoring it in proven foundations. As investors, we’re in the business of making probabilistic bets about the future. Why wouldn’t you start with the people who’ve already shown a consistent ability to be right more often than they’re wrong?

From Rock Turning to Copying Greatness

One of the most underappreciated skills in investing is simply finding ideas. Peter Lynch famously said that investing is about “turning over as many rocks as possible,” because somewhere underneath, one or two might hide a gem.

Most investors never build that muscle. They spend all their time polishing the few rocks they already know, rather than searching for new ones.

Idea generation should sit at the heart of every investor’s process. The more ideas you expose yourself to, the more patterns you begin to recognize – patterns in business quality, capital allocation, and valuation that train your intuition. Over time, that pattern recognition becomes a genuine edge.

But here’s the problem: turning over rocks takes time, and the supply of new rocks is almost infinite.

That’s where cloning comes in.

When I first started investing, I did what everyone does: ran stock screeners, scrolled through lists of 52-week lows, and browsed financial media for inspiration. These tools are useful, but their outputs are often noisy. Great businesses rarely screen well as I discussed in this recent write-up (and present a workaround).

Value Investing 3.0 & The Next Evolution of Stock Screening

Note: The voiceover above is a custom-made version of the blog post created with ElevenLabs. It’s one of the perks available to paid subscribers, as I’m always focused on adding as much value to my subscribers as possible. Enjoy!

Long-term compounders usually don’t look optically cheap on backward-looking metrics. As a result, many of the market’s long-term compounders never even show up in a traditional screener. You have to know where to look, and more importantly, who to look at.

“I’d rather steal a good idea than generate a bad one myself.” - Steve Morrow

Over the years, I’ve come to rely on a mix of sources for idea generation. I still use quantitative filters occasionally, but the truth is that the most interesting ideas rarely come from a screener. They come from conversations with other investors, posts I stumble upon on X, annual letters I happen to read, or – maybe most often – from shamelessly cloning people who have already done the hard work.

There’s a simple thought experiment that captures the essence of this. Imagine Warren Buffett calls you every quarter to tell you exactly what he bought and sold. That would be an incredibly valuable phone call, right? How much would that be worth to you? Well, the reality is that you already get it … for free. It’s called a 13F filing. Every quarter, professional money managers disclose their holdings. The information arrives with a short delay, but that doesn’t make it useless. Studies consistently show that simply cloning a handful of top-tier investors with a one-month lag can produce above-market returns over long periods.

Cloning also lets you tap into research networks that you could never afford on your own. A top-tier fund manager has access to management teams, industry experts, and analysts that collectively represent hundreds of thousands of dollars in research expense. By studying what they buy, you effectively hire that network for free. It’s a bit like being handed the homework of the smartest kid in class – you still need to understand it, but it gives you a huge head start.

Of course, there’s a spectrum of cloning. At one end are the “dumb copiers” who blindly buy whatever a famous investor buys. At the other are the “thoughtful cloners” who treat each disclosure as an invitation to investigate.

The latter is where you want to be. Blind imitation will never lead to conviction, and without conviction, you’ll sell at the first sign of trouble. But if you use cloning as a starting point – to narrow your universe to ideas already vetted by people you trust – you dramatically increase your efficiency.

“Generally, I think it’s quite smart to identify some investors you regard as very skilled, and carefully examine everything they’re buying, and copy what you please.” - Charlie Munger

Modern cloning isn’t about copying a stock; it’s about copying a thought process. I’m trying to reverse-engineer the logic: what moat does this business have? What earnings power are they underwriting? What return profile must they be seeing to make this position size rational? That’s how cloning becomes a learning exercise rather than a lazy shortcut.

The key is to use cloning to sharpen your own thinking, not replace it. Once you’ve done that, you realize that the difference between “idea generation” and “idea cloning” is smaller than most think. Both are ways of turning over rocks – it’s just that cloning lets you start with the rocks already picked up by the best treasure hunters in the game.

How to Clone Intelligently

Cloning well is an art form. It’s not about copying someone else’s portfolio – it’s about learning to see the world through their eyes. Most investors misunderstand this. They imagine cloning means mindlessly mirroring another person’s trades. In reality, intelligent cloning is about discernment:

choosing who to learn from,

understanding how they invest,

and knowing why their approach fits (or doesn’t fit) your own philosophy.

When I started building my own investing process, I probably followed far too many fund managers. Every quarter I’d open Dataroma or Whalewisdom, scroll through dozens of 13Fs (Dataroma currently tracks portfolios of 81 “superinvestors”), and convince myself that I needed to track almost all of them.

That approach is useless.

The point isn’t to create a watchlist of every manager with a decent reputation – it’s to narrow your field to those a limited number of “GOATs”, those who are truly worth studying, the ones who think like owners, understand valuation like no other, and play long-term games.

Over time, I’ve refined that list of “superinvestors” to a smaller group of investors whose thought processes I find both rational and instructive. These are the “big boys” I used to – more on this below – keep a close eye on during 13F season (the AUM figures are based on their last 13F filings – which do not include non-US holdings):

Warren Buffett (Berkshire Hathaway) – Portfolio value: $257,521,771,000

David Einhorn (Greenlight Capital) – $2,325,916,000

Guy Spier (Aquamarine Capital) – $317,370,000

Mohnish Pabrai (Pabrai Investments) – $271,602,000

Chuck Akre (Akre Capital Management) – $10,210,810,000

Polen Capital Management – $32,586,433,000

Seth Klarman (Baupost Group) – $4,114,419,000

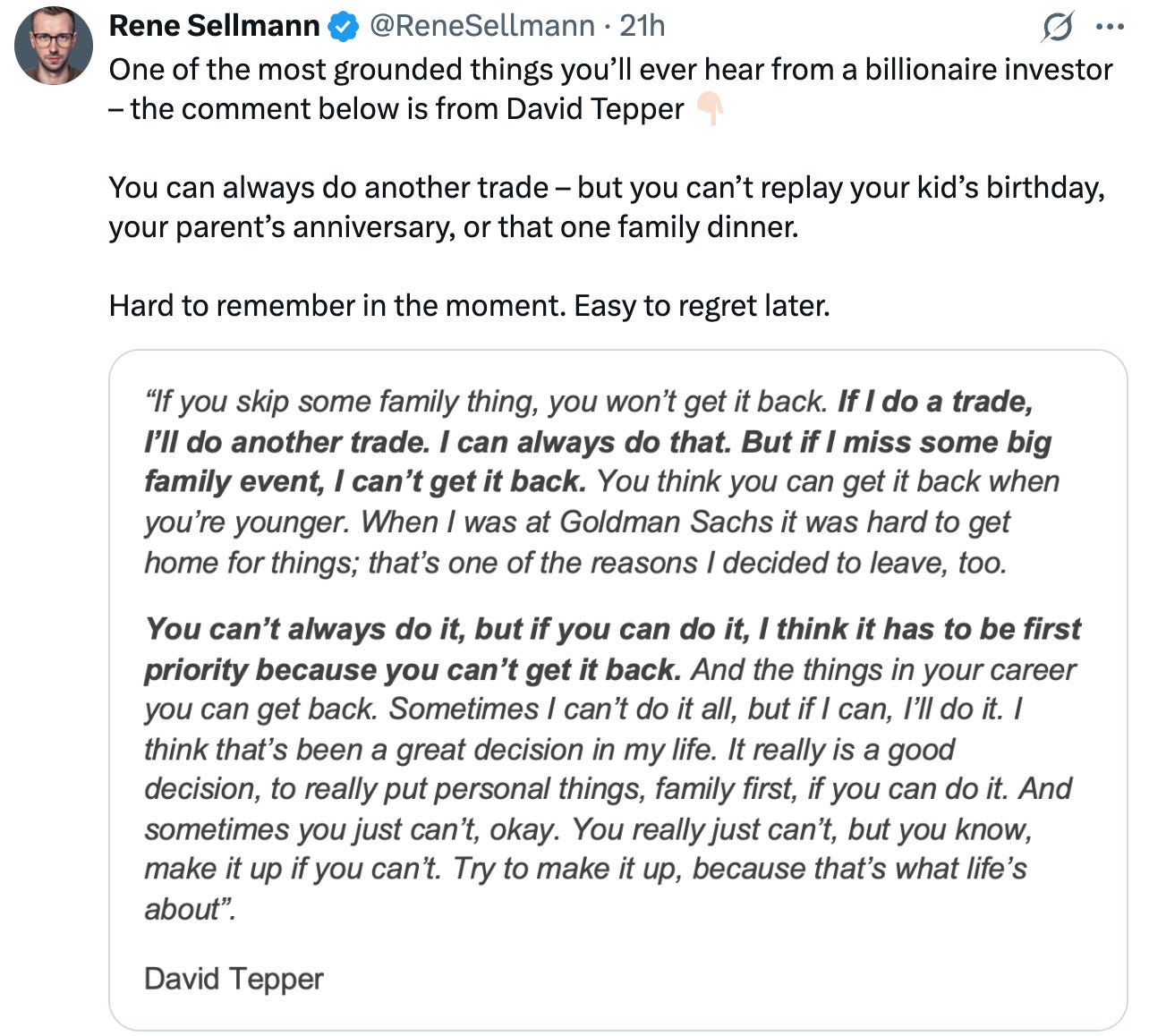

David Tepper (Appaloosa Management) – $6,448,962,000

Bill Ackman (Pershing Square Capital Management) – $13,729,120,000

Dev Kantesaria (Valley Forge Capital Management) – $4,527,265,000

Brad Gerstner (Altimeter Capital Management) – $6.93 billion

Norbert Lou (Punch Card Management) – $309,882,000

Alex Roepers (Atlantic Investment Management) – $195,982,000

Francois Rochon (Giverny Capital) – $2,915,806,000

Each of these managers offers something distinct. Buffett is the timeless blueprint of patience and rationality. Einhorn adds a contrarian streak rooted in deep valuation work. Spier represents the temperament side of the craft – the art of doing nothing & staying calm and humble in a noisy world. Pabrai embodies concentrated opportunism, while Akre perfected the “compounding machine” framework of high-return businesses run by trustworthy managers. Polen Capital is a model of quiet discipline and process-driven growth investing. Klarman represents rigor and margin of safety. Tepper and Ackman are masters of opportunistic boldness; Kantesaria and Rochon embody thoughtful, long-duration quality investing. Together, they form an intellectual composite that captures quite a lot of angles of thoughtful stock picking.

Intelligent cloning also means knowing when not to follow. As I wrote above, I used to track the “big boys” mentioned above. But I’ve updated my view on some of them over recent months and years. For instance, I’ve admired Pabrai for years, but his time horizon tends to be shorter. He looks for opportunities that can double in three years and then recycles capital. My own bias is toward long-term compounders – companies I can own through multiple cycles. His track record more recently has also been rather lackluster. I still find Pabrai’s thought process deeply useful, but I don’t copy his trades anymore. Similarly, Howard Marks focuses on credit and distressed assets, while Seth Klarman hunts for spinoffs and event-driven mispricings. So their portfolio activity isn’t necessarily relevant for my idea generation process anymore.

As private investors, we possess many advantages over professional investors (I’m not going to get into the details of this topic here). But one advantage we possess is certainly that our investable universe is much bigger. We have no limits. No limits in terms of size, industry, or geography.

Yet, the fund managers I cited above often do. Many manage multiple billions in AUM.

Nowadays, of the list above, I really only pay attention to the portfolio activity of Ackman, Polen Capital, Rochon, Dev Kantesaria , Norbert Lou, and the Akre Fund team.

The Modern Twist: Cloning in the Age of Infinite Access

The beauty of being an investor today is that there’s almost no excuse for not knowing what the best in the world are doing. Transparency has gone from privilege to default. Fund letters, interviews, podcasts, regulatory filings, social media – they all converge into one enormous open-source intelligence network. If you’re willing to spend a few hours digging, you can follow the footprints of nearly every great investor alive.

That accessibility has completely changed what it means to be a modern shameless cloner. In Pabrai’s early days, you had to wait for print filings or rely on financial media summaries. Today, you can monitor global fund movements in real time. The barriers between professionals and private investors have largely evaporated.

That’s both a gift and a trap. A gift because the information advantage is gone, which means edge increasingly comes from interpretation. A trap because abundance breeds noise, and noise tempts laziness.

For me, the best way to balance those forces has been to move away from cloning billion-dollar managers altogether. Not because they’re not worth studying – they absolutely are – but because the constraints they face often make their portfolios less relevant for smaller, private investors with a much larger opportunity set.

A concentrated fund managing $10 billion can’t really buy a $400 million company, no matter how promising. Its liquidity needs force it into large caps, where opportunity is thinner and competition is ruthless.

That’s why my focus has gradually shifted toward smaller, lesser-followed investors who operate with the same mindset but far more flexibility. These are people who manage smaller pools of capital – often their own money – and who still think and write like business owners. They don’t have marketing departments or investor relations teams. They’re usually a one-man team. What they have is focus, skin in the game, and an investing style that mirrors what most of us as private investors can actually emulate.

Below are 20 of them that I pay attention to, roughly from larger to smaller in scale.

I included a link to their websites, where you can (usually) find their investor letters

If available, I included their track record

the AUM figures may be off at times, but were my best guess based on their latest letters of public filings

This is where it gets interesting.

Become a paying subscriber to read the rest of this post and get access to all of my other research, including valuation spreadsheets, deep dives (e.g. well-known mid- and large caps such as LVMH, Duolingo, Meta, Edenred as well as more hidden gems such as Tiger Brokers, Digital Ocean, Ashtead Technologies, InPost, Timee, and MANY more), and powerful investing frameworks.

Annual members also get access to my private WhatsApp groups – daily discussions with like-minded investors, analysis feedback, and direct access to me.

PS: Using the app on iOS? Apple doesn’t allow in-app subscriptions without a big fee. To keep things fair and pay a lower subscription price, I recommend just heading to the site in your browser (desktop or mobile) to subscribe.