Quick Pitch: Tencent Music Entertainment Group ($TME)

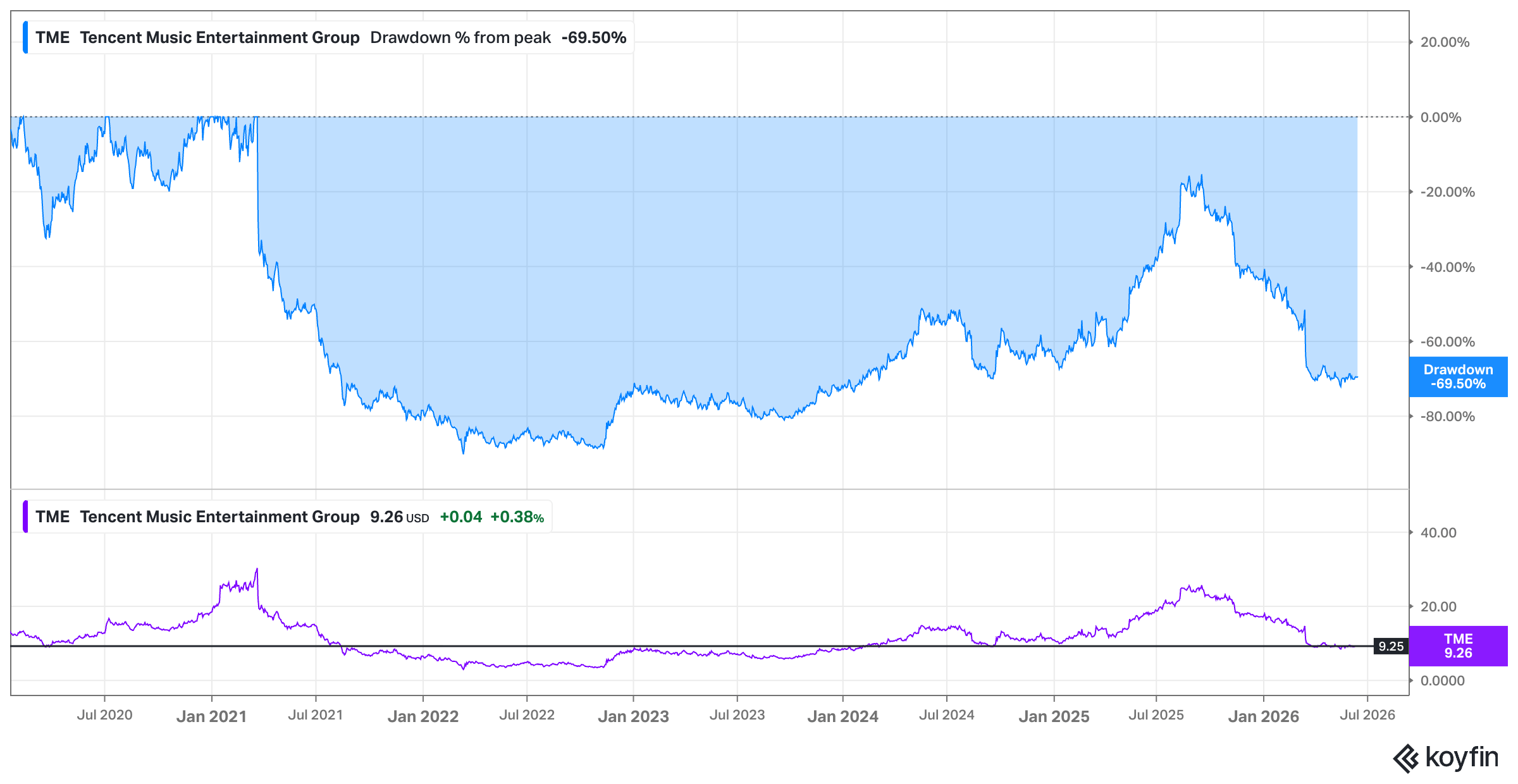

Too Attractive to Ignore After a 69% Drawdown?

Imagine owning the dominant music streaming platform in a country of 1.4 billion people – a business so structurally entrenched it operates parts of itself with negative working capital, throws off roughly $1.5 billion in earnings attributable to shareholders annually, and sits on a balance sheet stuffed with $6 billion in net cash plus equity stakes in both Spotify and Universal Music Group.

Now imagine that the market is pricing all of that at roughly 9x forward earnings – and that once you start digging past the headline multiple, the true price you’re paying for the actual streaming engine is even more jaw-dropping than that already-cheap number suggests (to be discussed below).

That is the Tencent Music Entertainment (ticker symbol TME 0.00%↑) situation today.

The stock has gone nowhere for over five years. It currently sits 69% below its all-time high. In just the ten months between August 2025 and June 2026, more than 63% of the stock’s value has been wiped out – a collapse that would feel right at home in a speculative biotech bust, not in a cash-generative, monopoly-like platform business beating analyst estimates on both revenue and earnings per share for six consecutive quarters.

So what is going on?

The short answer: the market is reacting to a cocktail of anxieties rather than the underlying business reality. When you layer these concerns (to be discussed below) on top of a persistent “China discount” – VIE structure anxiety, memories of the 2021 regulatory crackdown, rock-bottom Chinese consumer confidence – you get a reflexive sentiment vortex. The street sells first and asks questions later.

The question worth asking, I believe, is: at what point does the geopolitical discount become too much of a discount?

Disclaimer: As of the date of publication the author owns no shares in TME; but that may change. The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

The Business of Tencent Music Entertainment Group

Tencent Music Entertainment Group (TME) is listed on both the NYSE under the ticker symbol TME as well as the Hong Kong Stock Exchange under the ticker 1698. TME dominates the Chinese audio landscape through an ecosystem of powerhouse applications like QQ Music and Kugou Music.

Think of it as a much more versatile version of Spotify operating within a highly protective domestic duopoly alongside NetEase Cloud Music. For years, in fact, China’s digital music landscape was highly fragmented and plagued by piracy. The market consolidated rapidly due to two major events:

Tencent’s Consolidation: In 2016, Tencent merged its own streaming service (QQ Music) with China Music Corporation (owners of Kugou and Kuwo). This brought China’s three largest music apps under one corporate roof (TME), giving them an overwhelming market share.

The Exit of Competitors: Smaller platforms simply couldn’t keep up with the soaring costs of licensing music; there’s a natural winners-take-most dynamic at play in this industry (think of Spotify’s massive, dominant lead in “the West” (estimated 40% market share) alongside Apple, Amazon and YouTube music). The duopoly became firmly cemented after Alibaba shut down its music streaming platform, Xiami Music, leaving NetEase as Tencent’s only viable, scale-driven competitor.

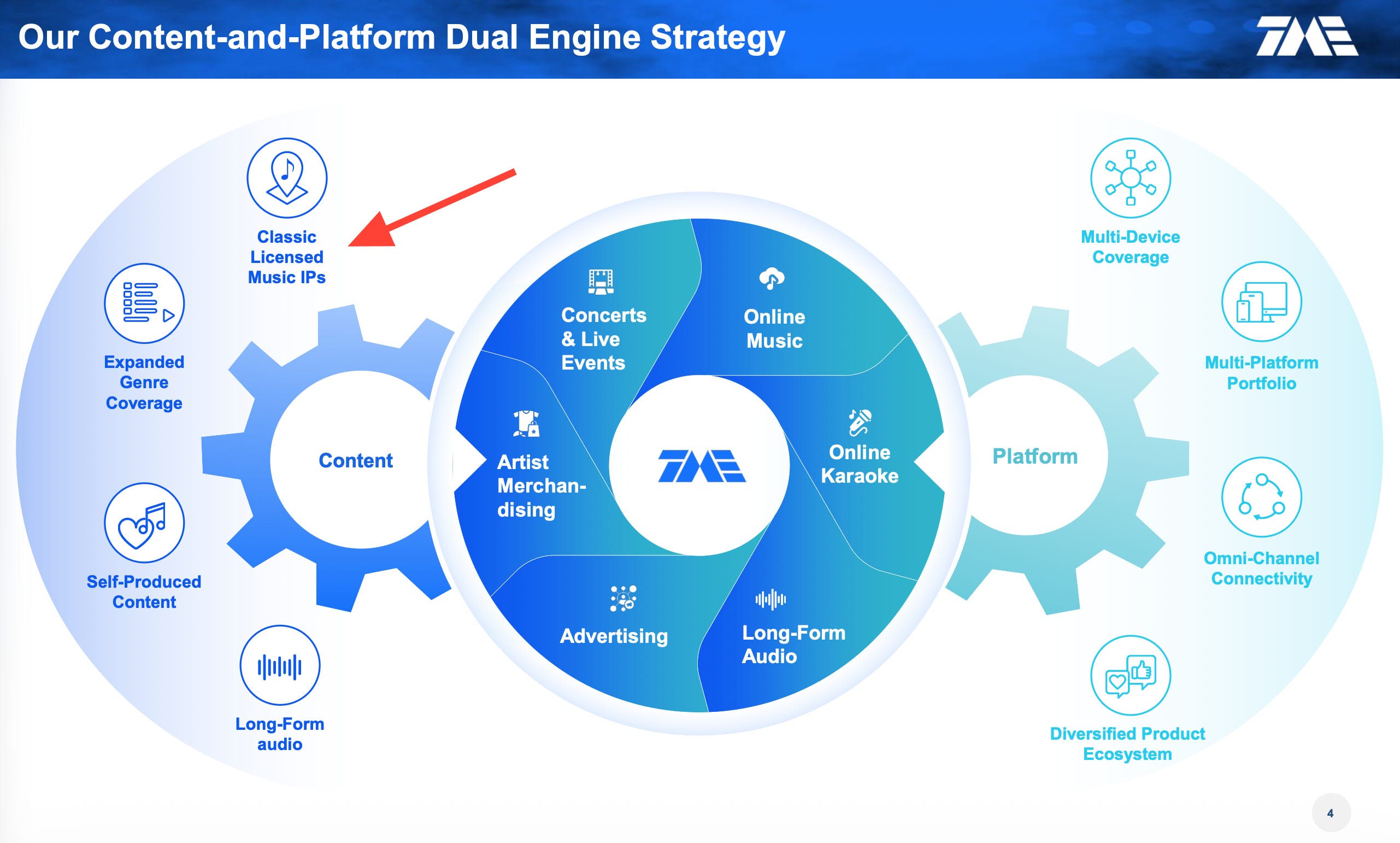

But back to TME’s business. Rather than relying strictly on the standard freemium streaming model, TME is best thought of as a dual-engine machine that actively pairs a massive digital platform with both sub-licensing and direct content ownership.

Yet Tencent Music Entertainment does not operate as a traditional, singular record label in the same way that a “Major” (like Universal, Sony, or Warner) does. Instead, it employs a hybrid strategy that combines large-scale distribution with an internal production ecosystem.

Its structural integration with Tencent’s WeChat ecosystem provides a virtually unassailable distribution moat, converting casual video and social interactions into sticky, high-margin music subscribers.

“In the competitive world of business, having a superior product isn’t always enough to guarantee success. Often, the ability to distribute a product widely and efficiently can create a significant competitive advantage known as a ‘distribution moat.’ A distribution moat refers to a company’s capacity to leverage its extensive distribution network to dominate a market or quickly penetrate new markets, making it exceedingly difficult for competitors to gain a foothold.“ - from my investing framework

By managing its own in-house music labels and locking down early-release windows for tier-one artists, the business keeps its content procurement costs low while keeping user retention incredibly high.

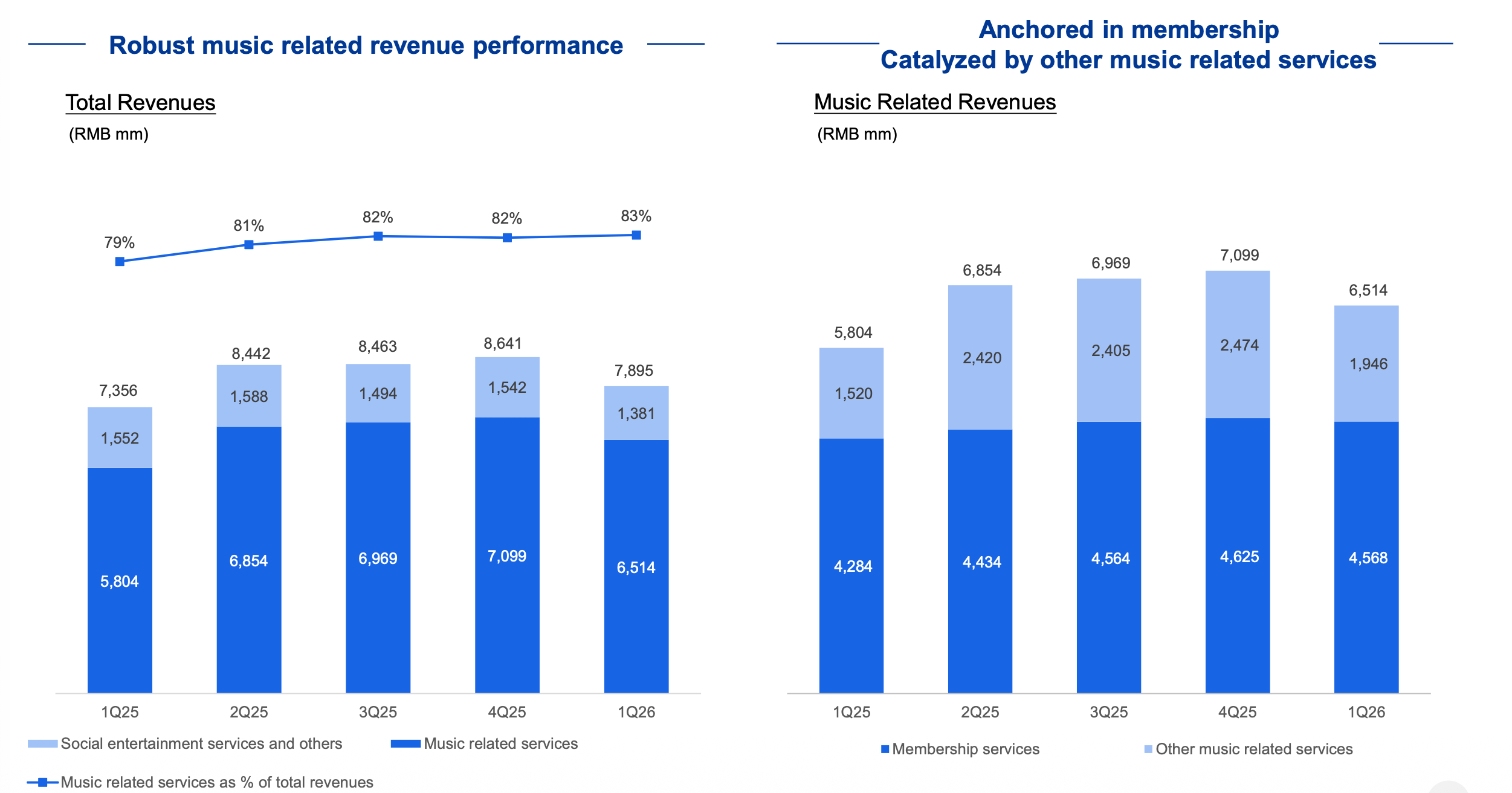

When you look at how the revenue flows, the business splits its operations into two primary reporting segments:

Music Related Services (82.5% of Q1 revenue; further broken down into “membership services” (58% of total revenue) and other “music related services”) – formerly known as Online Music – …

… and Social Entertainment (17.5% of Q1 revenue).