Below you find my April reading (and listening) list: a handful of recent finds that offer valuable context on market trends and the frameworks driving them.

Articles:

New and updated Bessembinder report: “One Hundred Years in the U.S. Stock Markets“

“Abstract: This study summarizes investment outcomes for 29,754 common stocks listed on the public U.S. stock markets over the 100-year period from 1926 to 2025, reporting on both compound (buy-and-hold) percentage returns and shareholder wealth enhancement measured in dollars. While the cross-stock mean buy-and-hold return is over 30,000%, the median is -6.9%. Shareholders’ wealth was enhanced by $91 trillion over the century, but long-term investors in nearly 60% of stocks incurred wealth reductions. The degree to which wealth creation is concentrated in a few firms has increased sharply in recent years. Over the 1926 to 2016 period studied in Bessembinder (2018), 89 firms accounted for half of the $43 trillion in net wealth creation. After including outcomes for the most recent nine years, just 46 firms account for half of the $91 trillion in net wealth creation over the full century.“

“As many of you are aware, the portfolio remains focused on companies outside of the more fashionable sectors, emphasising businesses with straightforward models operating in traditional industries such as cement, food, luxury goods, and glass, among others.“

“The pace of change within the software industry has accelerated in recent months, leading to heightened uncertainty and prompting us to reassess moat ratings.

Why it matters: The capabilities of large language models are rapidly advancing and seem primed to cause at least some disruption within the industry, or at worst drive massive dislocation for many software firms.

After an in-depth review of the software and services firms covered throughout Morningstar, we are downgrading moat ratings, reducing fair value estimates, and increasing uncertainty ratings for our immediate coverage of a variety of companies.“

In case you are having a tough time so far in 2026: “What to do when you’re underperforming - Thinking straight when you’re on a bad run.“ by The Intellectual Edge

Great sector analysis of the payment sector: “The Industry That Will Benefit The Most From AI“ by Normandie Research

Podcasts & Videos:

Interactive Brokers’ founder Thomas Peterffy on the Odd Lots podcast discussing prediction markets.

Some highlights:

“A broker always has to worry about providing leverage. So most brokerage firms, they go bust, because of the leverage they provide, and if you look at the big Wall Street crisis, they all have to do with leverage - always. But eventually, we will have to provide leverage [note: he’s referring to prediction markets]. The question is, how do you structure that? (…) I’m sure there will be some firms that will go bust on leverage in prediction markets, yes.“ […]

“So insider trading has always been an issue. I mean, early on when I started my career, Ilost half my initial capital based on insider trade. So I’m extremely familiar with the damage it can cause. But on the other hand, and in spite of that, I’m in favor of not having any rules against insider trading. I would like all the information out there as soon as it’s available. Because look, as a society, we’re better off knowing as soon as possible anything that is knowable. Right? So why do we have to wait several, first of all, when you face with a merger or acquisition situation where most of the insider trading is happening, right? The secretaries, the lawyers, everybody knows about it. They go home, they tell their wives, their husbands. So it eventually always filters out. So it’s almost impossible to avoid. It’s very, very difficult and cumbersome. Why don’t we just do away with it and let the information come out as soon as possible?“

Pabrai Wagons ETF Shareholder Call Replay:

Brett Caughran on markets’ becoming LESS efficient (short video clip):

“I would very much challenge the premise that these tools will lead to more efficiency.”

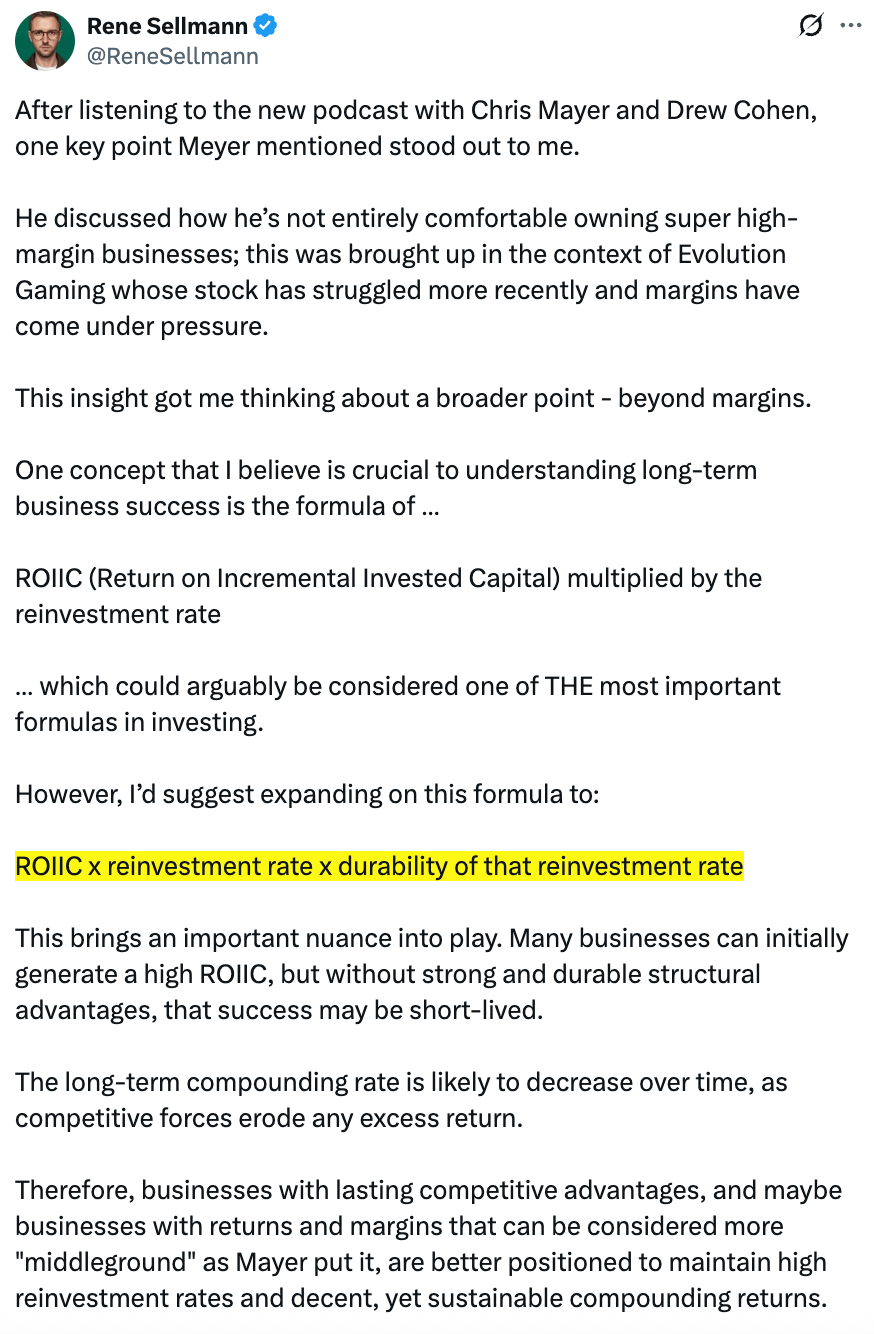

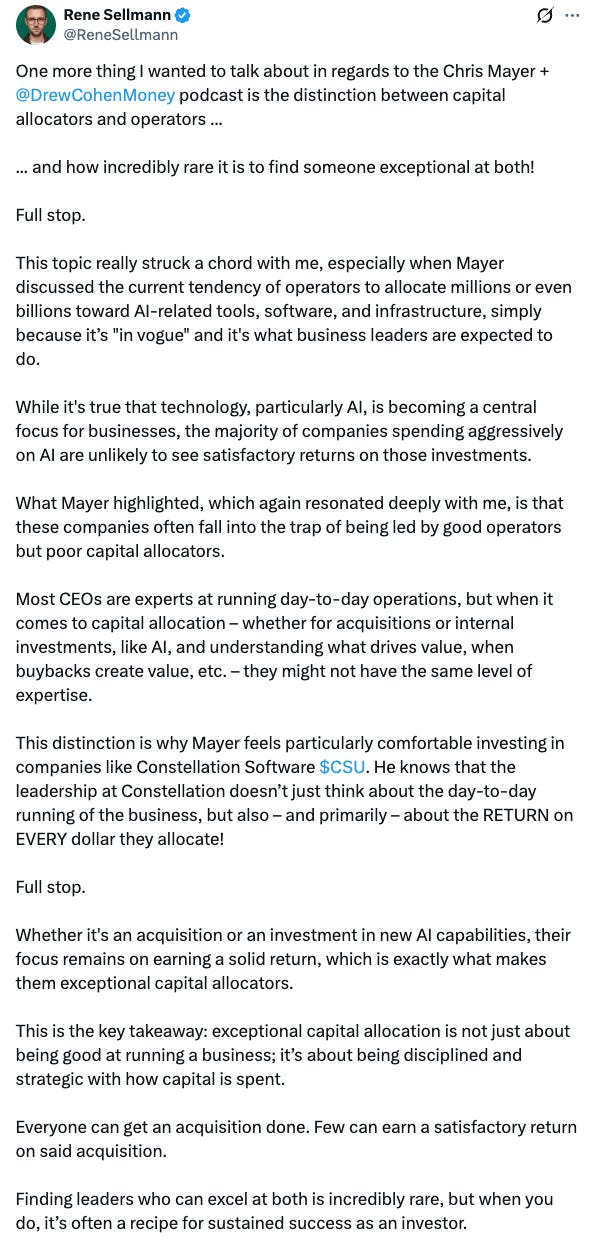

Chris Mayer’s interview on Drew Cohen’s platform:

The episode made me think of two things, which I shared on X (attached below). First, the fact that the formula below may be the most important in all of investing:

a) ROIIC x b) Reinvestment Rate x c) Durability of the combination of a) + b)

Secondly, VERY high margins and VERY high growth businesses are inherently risky/riskier (and hence shouldn’t necessarily be your favorite hunting ground) – the “middleground” (i.e. above-average margins and growth – but not excessively high) might be the more attractive hunting ground as those tend to be often more sustainable:

Other:

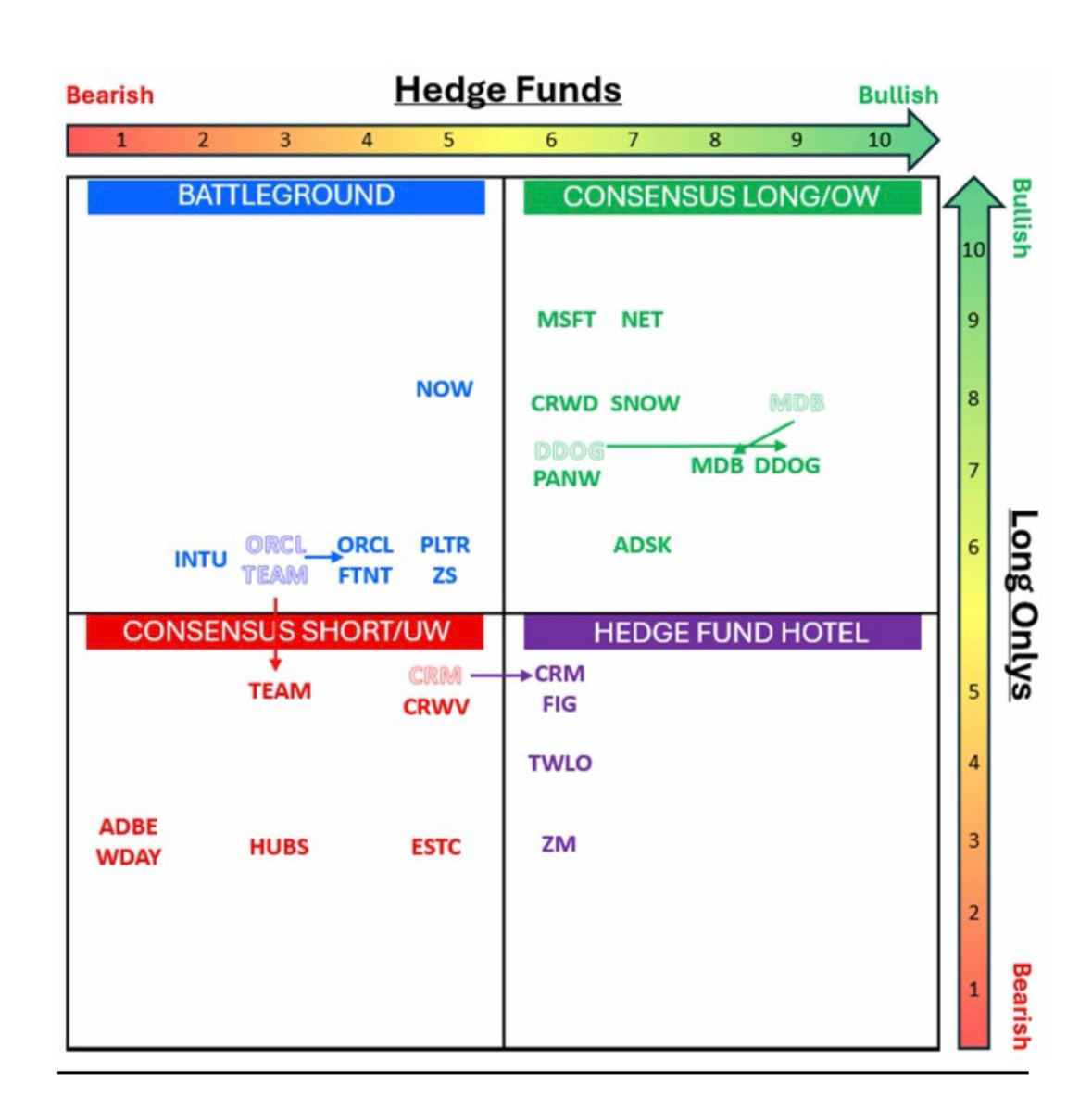

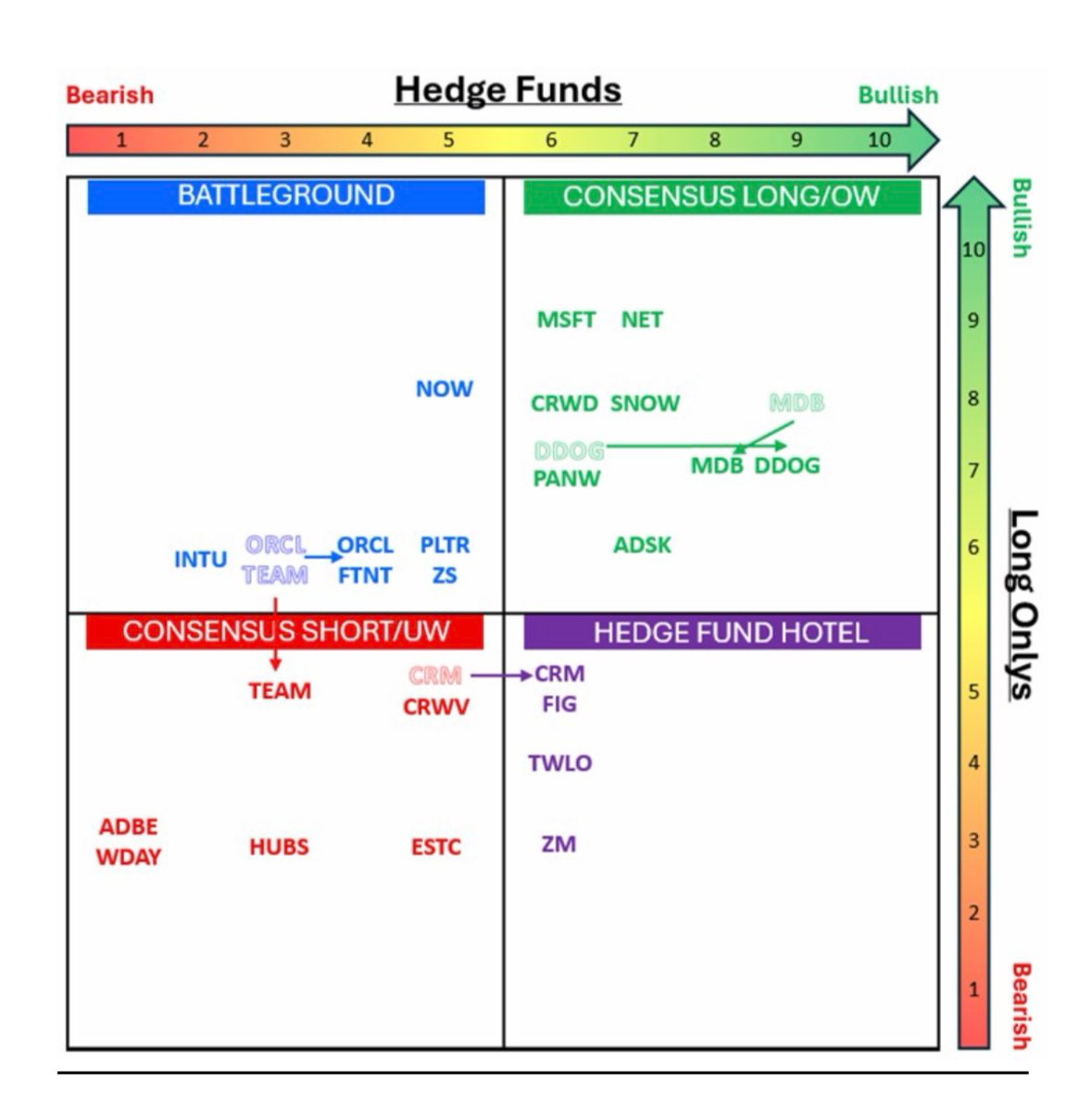

The Software Sentiment Matrix by J.P. Morgan

If you own luxury (fashion) stocks, you should read this thread:

Intern Pierre@internpierrePeople called me a dipshit for shorting $LVMH / $MC. The stock is down 40% since I took the position and just had its worst first quarter in history, worse than 2008. Q1 numbers drop Friday. I don't think the market is bearish enough. A thread 🧵

Intern Pierre@internpierrePeople called me a dipshit for shorting $LVMH / $MC. The stock is down 40% since I took the position and just had its worst first quarter in history, worse than 2008. Q1 numbers drop Friday. I don't think the market is bearish enough. A thread 🧵 10:40 AM · Apr 6, 2026 · 197K Views43 Replies · 31 Reposts · 720 Likes

10:40 AM · Apr 6, 2026 · 197K Views43 Replies · 31 Reposts · 720 Likes

I hope these resources provided as much food for thought for you as they did for me. If you found this month’s insights valuable and want to stay ahead of shifting industry dynamics, consider subscribing. You’ll get every new edition, and all the other write-ups I produce, delivered straight to your inbox so you never miss it.