From U.S. Premium to Global Paranoia: A New Era for Investors?

Why Geography Deserves a Closer Look

Let me start this blog post with a confession: I’ve never been a fan of broad diversification.

In fact, I’ve always found the industry's obsession with it a little overdone – almost like a safety blanket for those unwilling to do the work. That may sound harsh, but hear me out.

Theoretically, you can slice and tag every single stock in your portfolio by dozens of different “risk factors”:

Market cap

Liquidity

Leverage

Regulatory environment

Geographic exposure

Currency risk

Sector concentration

Tax treatment

Political stability

Central bank policy exposure

Supply chain dependence

And on and on. Financial advisors love this sort of thing. It gives them a dashboard to tinker with. But the practical reality? If you wanted to “optimize” for every one of those factors, you’d need a portfolio with 100 or more stocks – maybe even more.

And then what are you really doing? You’re being the market. Which, by definition, means you’ve relinquished any attempt to beat it.

Warren Buffett said it best in his 1965 Partnership Letter:

“If good performance of the fund is even a minor objective, any portfolio encompassing one hundred stocks is not being operated logically. The addition of the one hundredth stock simply can’t reduce the potential variance in portfolio performance sufficiently to compensate for the negative effect its inclusion has on overall portfolio expectations.”

In other words: dilution kills alpha. Not risk.

That’s why I’ve always been a bottom-up investor at heart. I spend my time understanding businesses. I care about the incentives of management, the durability of returns, capital allocation, competitive advantage, and the price I’m paying relative to intrinsic value…

If I get those pieces right – if I find a great business run by competent people and buy it at a fair price – I will do well.

I believe that’s where my edge lies. Not in fiddling with my correlation matrix.

Of course, I’m not suggesting you should go all-in on one idea. I don’t believe in recklessness either. There’s a balance. Rob Vinall captured this nicely when he said:

“Diversification needs to be sufficiently high that a failure in one part of the portfolio does not lead to the whole edifice collapsing.”

That’s been my framework too. Not maximum diversification, but sufficient diversification. And yes, I’m aware that for most investors, that level will differ depending on experience, temperament, and knowledge.

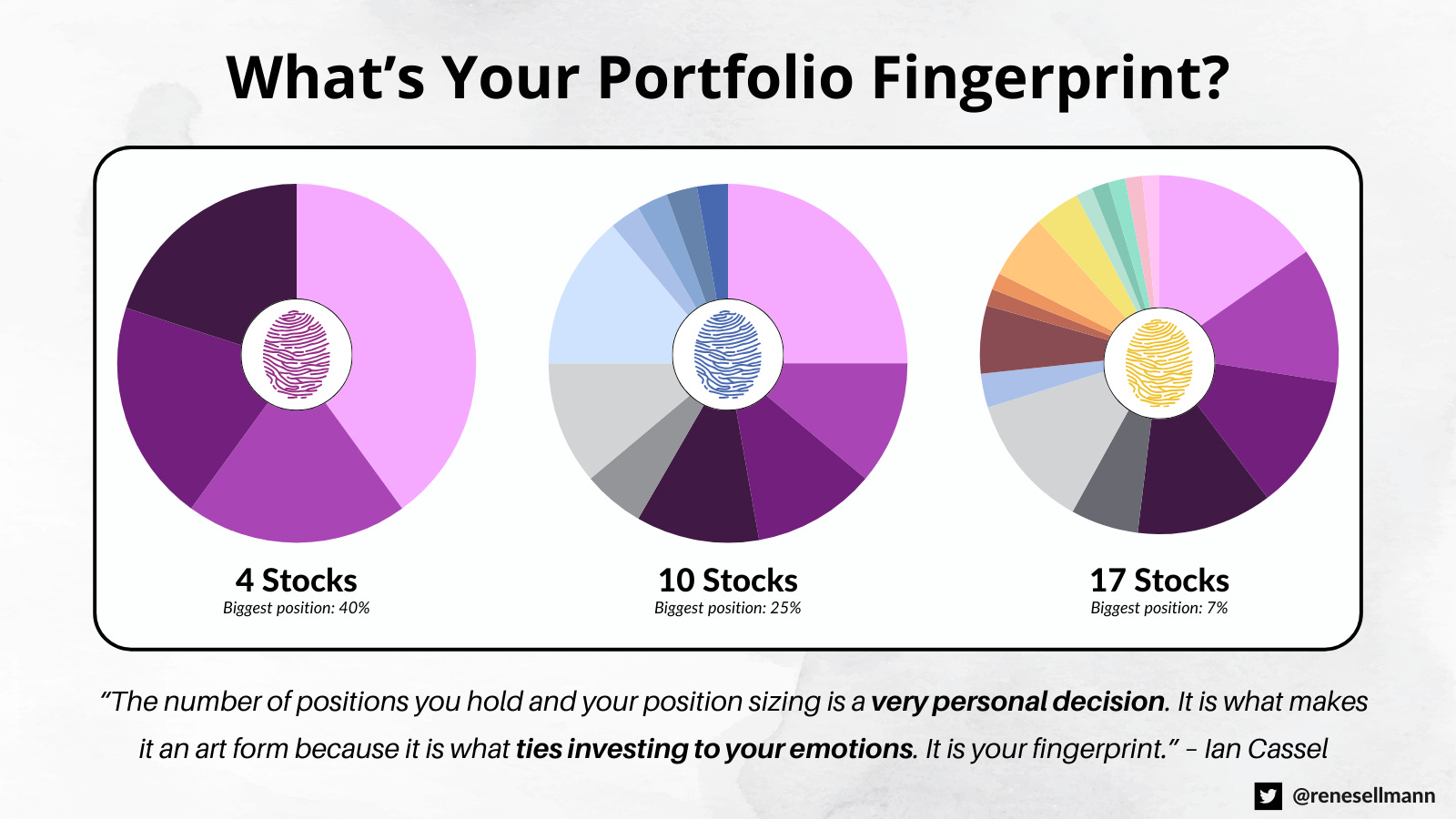

But for me, it’s never been a number like 30, 50, or even 100.

Mohnish Pabrai once referenced Charlie Munger's view of diversification like this:

“Charlie Munger considers that a portfolio of four stocks is a well-diversified portfolio. He says, you don’t even need a 5th stock. He goes on to say that if you lived in a small town, and if you owned the best apartment building in town, the highest quality office building, the McDonalds franchise, the Ford dealership — if you owned this collection of assets, even though they're all geographically concentrated, you will do very well. You will not need to do much else beyond that to have an interesting investing career.”

That image always stuck with me. A few great assets that you truly understand. That’s the game.

So no — I’ve never believed in major diversification. I’ve long ignored geography as well. If a business was great, I didn’t care whether it was based in Ohio, Osaka, or Oslo. If it printed free cash flow, had pricing power, and reinvestment opportunities, that was good enough for me.

But recently, I’ve started to ask a new question. Not one that contradicts this philosophy, but one that builds on it – or so I think.

What if the ground beneath even the best businesses starts to shift?

And what if that ground just happens to be where a large chunk of the world’s capital is currently parked?

That’s what I want to explore in the rest of this post.

Geography Wasn’t a Problem – Until It Became One

For most of my investing career, geography barely registered on my mental checklist. Sure, I’d note where a company was headquartered or where most of its revenue came from, but that was it. I didn’t assign much weight to it. My assumption was simple: if the business was good, the numbers strong, the industry enjoying secular tailwinds, and the management competent, it didn’t really matter where the company was based.