Deep Dive: Wise Plc. – Betting on the Unexpected?!

How, why, and when Wise may exceed market expectations going forward

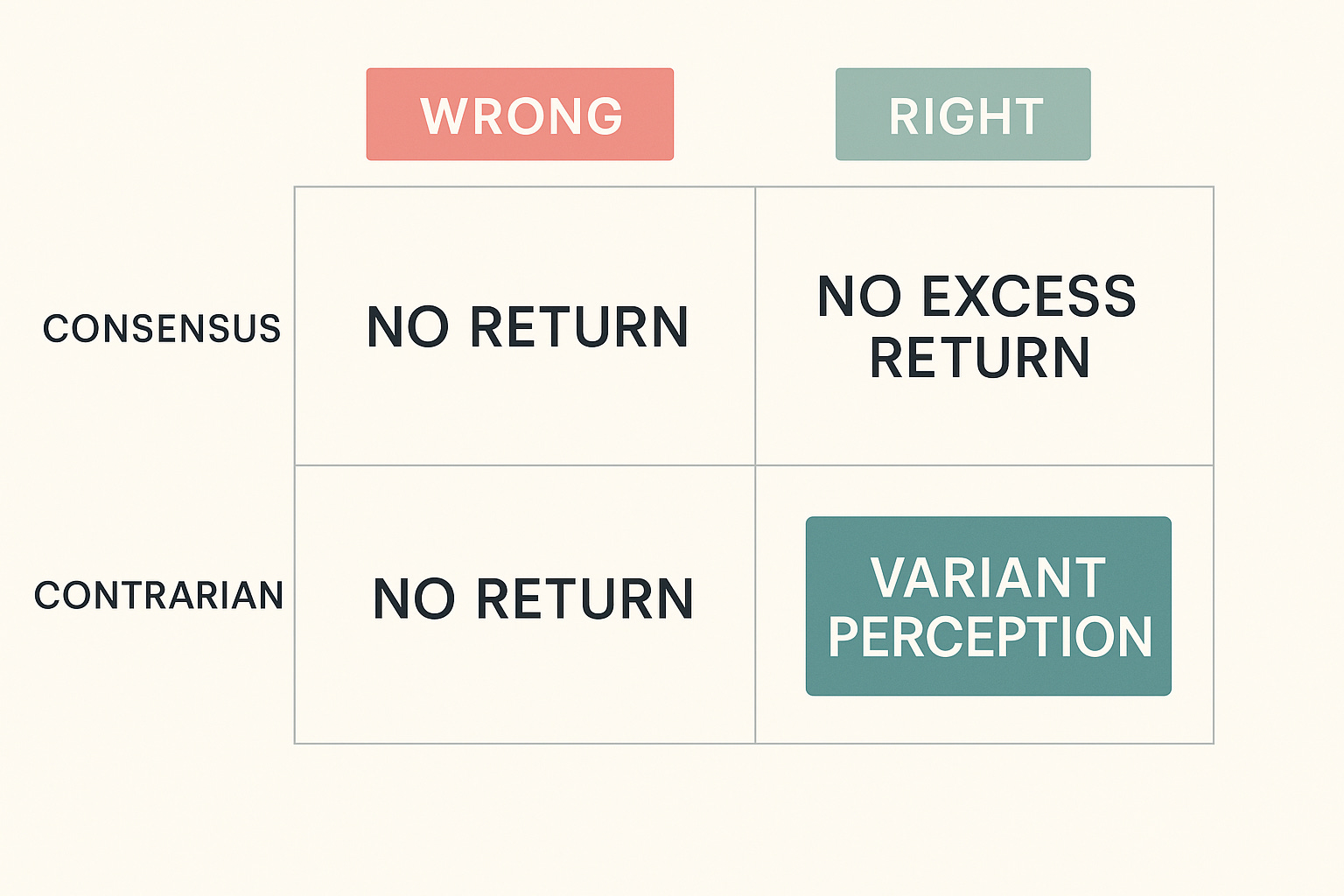

Investing at an elite level is an exercise in understanding embedded expectations in a stock price rather than simply identifying strong companies (they may be too richly priced!) OR optically cheap stocks (they may be cheap for a reason!).

Most market participants spend their time operating within the comfortable confines of first-level thinking.

They ask a straightforward, reactive question, such as …

Is this a good asset?

The answers to that query fill hundreds of generic media headlines, financial blogs, YouTube videos, and podcasts every single day, often culminating in a crowded consensus where everyone stares at the identical set of obvious variables.

“Costco is a high-quality compounder!“

Or what about …

“Adobe is an AI loser!“

If the game were that simple, research analysts and/or historians would easily be the wealthiest individuals on Wall Street instead of working for a fixed salary. As always, Buffett has expressed this view many decades ago already:

"If past history was all that is needed to play the game of money, the richest people would be librarians."

Thus, generating alpha requires more.

True outsized equity returns are born from an entirely different analytical filter. To win, you must step into second-level thinking. You must systematically ask what everyone else is assuming about that stock, what exact expectations are already embedded in the current price – this goes back to the concept of expectations investing by Michael Mauboussin –, and who you are betting against (and why they view the asset the way they do).

And then, when you form a contrarian, non-consensus view, you additionally have to be right!

All/most of the above was shared by Tiho Brkan recently on X in a short, but punchy tweet (all the credits belong to him here), and he wrapped it up beautifully by referencing George Soros: he summarized this beautifully by stating that money is made by discounting the obvious and betting on the unexpected.

I figured this would be a very fitting way to start this post, focused on Wise Plc. The recent dual listing of Wise plc on the Nasdaq on May 11, 2026, alongside its secondary listing on the London Stock Exchange, provides a textbook example of first-level market noise completely blinding participants to a generational asset. When the ticker tape flashed on American screens, the financial media and algorithmic trading desks focused almost exclusively on immediate liquidity dynamics and mechanical price action. As outlined in my recent write-up on Wise’s Nasdaq listing presentation and special call, at first, the stock shot up by 7%, but it quickly encountered structural selling pressure over the subsequent trading days.

Check out my latest piece on Wise here:

Deep Dive: Wise Plc. ($WISE) – 10 Critical New Insights!

You can read a good chunk of this article entirely for free. If you find value in this research, consider becoming a Premium Member for less than $1/day to unlock our full archive and join our growing circle of investors (I highly recommend checking out “The Library” to see what’s inside; you can find it right on the homepage).

First-level commentators instantly pointed to the bleeding tape – which is just a fancy way of saying “the stock is down (big)” – as definitive proof that the entire cross-border payment sector was structurally doomed.

If you only evaluate companies through headline narratives and short-term stock charts, you will completely miss the structural transformation taking place inside this network. They missed it. I have closely tracked Wise’s global infrastructure build since its initial public listing in 2021, and I believe there’s a massive disconnect between current market perception and fundamental operational reality.

This deep operational disconnect is part of my investment thesis. The market is fundamentally mispricing Wise because traditional analysts continue to treat it as a standard, sleek retail remittance application. They see a simple consumer tool and completely fail to comprehend the massive, proprietary payment infrastructure humming quietly beneath the application layer.

My Hypothesis

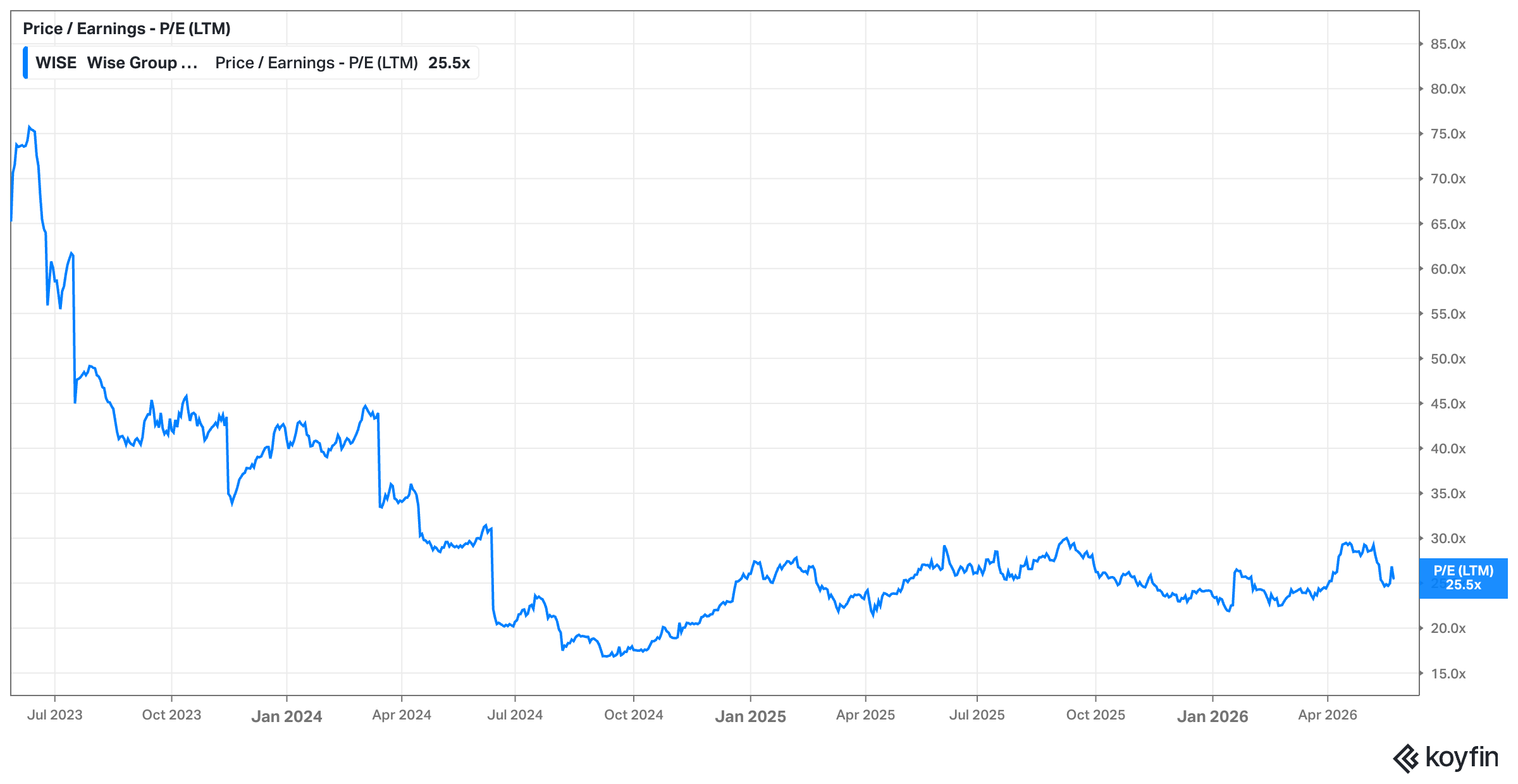

What I plan to focus on in this article is to outline a bullish hypothesis that I have never seen discussed by anyone following Wise. I’d argue many market observers do actually have a decent grasp on the competitive advantages of Wise and the length of the runway. That’s why if you believe in Wise’s guided underlying EBT margins of 15-20% (keep in mind that Wise is currently “overearning”), Wise isn’t clearly cheap as the implied current Price-to-Earnings ratio would sit somewhere in the range of 30-40x earnings.

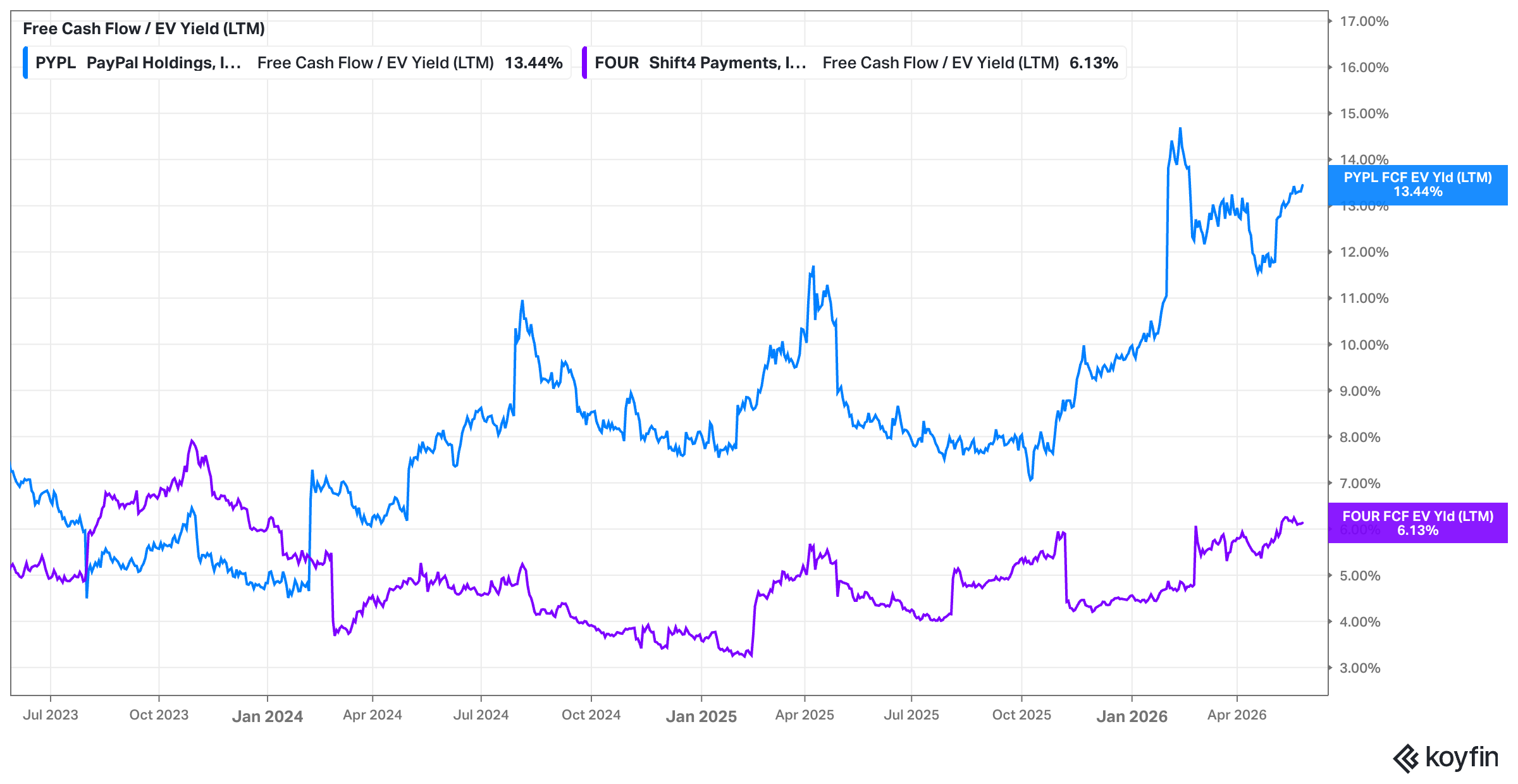

This seems particularly “rich” in light of the pressure one can witness in the payments sector and the valuation multiple some “peers” currently demand (to be fair, what Shift4Payments or PayPal really have in common with Wise is simply the industry they operate in).

So the bullish hypothesis I want to discuss stands on two highly contrarian predictions that run directly counter to current Wall Street consensus models (where bears would argue Wise’s very mission of driving take rates to zero will eventually kill its own business).

First, while the prevailing consensus assumes that Wise, like most businesses, will eventually be entering a permanent growth deceleration phase where revenue trends down (or plateaus in the low teens sooner than later), I predict that we might eventually see top-line growth reaccelerate comfortably above 20% – a pattern you wouldn’t normally find in your Econ 101 textbooks – as its global scale takes effect.

Second, the consensus believes that Wise’s unique cost-plus pricing strategy naturally limits its ultimate profitability, but in this write-up, I argue that the business might reach a point where it will post long-term profit margins vastly superior to current market assumptions – potentially reaching 40% (or more!) as its massive operating leverage unlocks. Why should Wise not achieve 40% pre-tax margins once it captures a dominant share of the global money movement market? The consensus assumes that aggressive price cuts destroy terminal value, failing to recognize that lowering fees is actually a powerful customer acquisition tool that widens an unassailable structural moat.

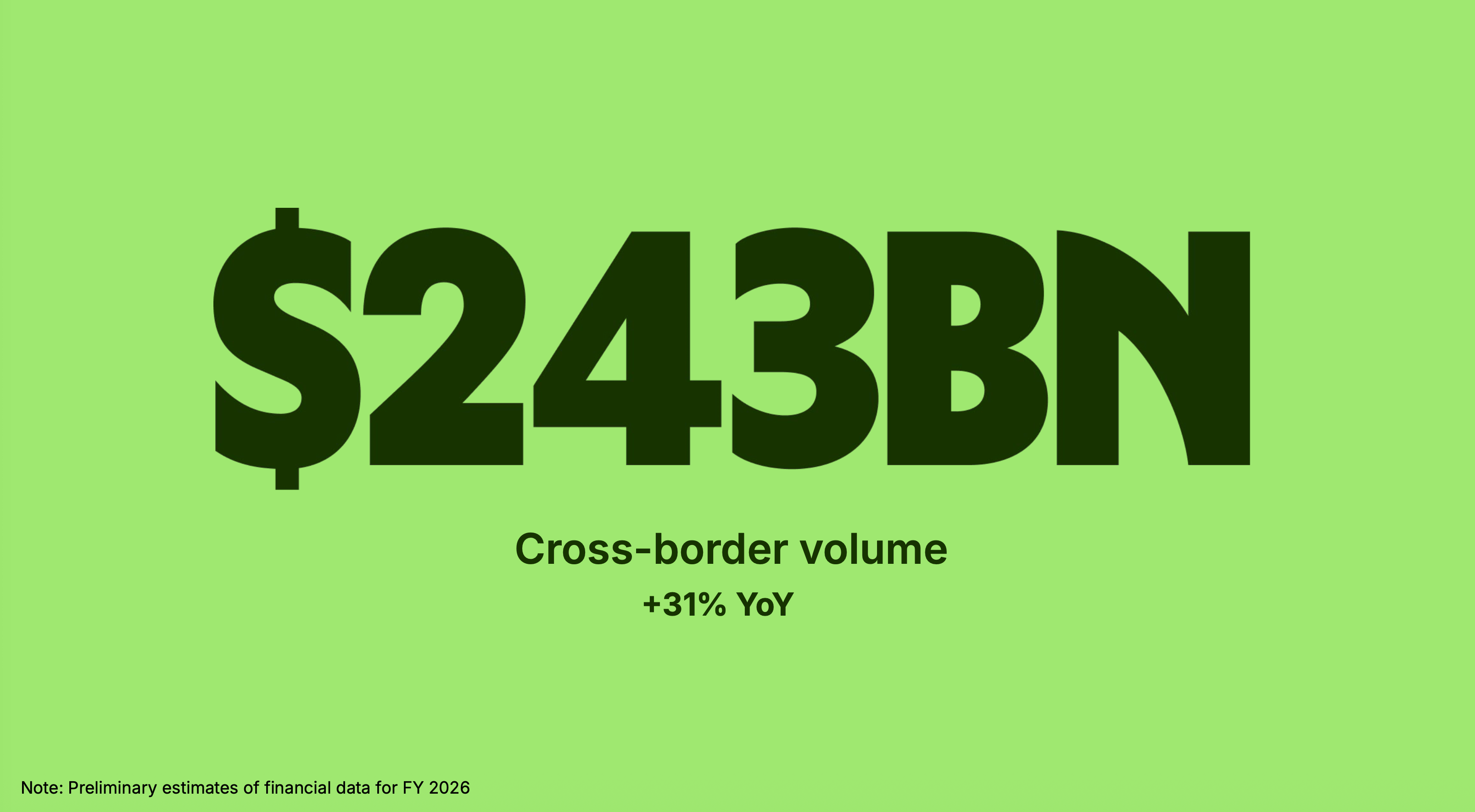

Consider the incredible journey of this enterprise. Wise has scaled from absolute zero fifteen years ago to processing a staggering $0.25 trillion – trillion with a “T” – in transaction volume today.

The bull hypothesis is based on the idea that, despite its massive operational expansion, the company has only begun to tap into its total addressable market.

You are looking at a scaling cross-border payments infrastructure monopoly that is being valued like a soon-to-be maturing, legacy money transmitter.

That is the essence of a second-level thinking arbitrage, and it is precisely why the current market setup potentially offers an interesting entry point for disciplined, long-term capital – again, remember, IF (!) that hypothesis proves to be true.

Here’s what we will cover in this analysis:

Why the post–Nasdaq listing selling pressure represents a classic first–level market trap, hiding a world-class asset behind short–term liquidity noise.

A granular cost-layer audit isolating Layer 1 variable gross margins from Layer 2 administrative expenses to map out Wise’s latent profitability tier.

Benchmarking Wise against the automated clearing engine of IBKR to demonstrate how scale economies shared unlock “elite” corporate operating leverage.

Deconstructing the strategic shift from pure word–of–mouth acquisition to an aggressive 52% year–on–year boost in global brand campaigns.

Evaluating Wise’s massive structural runway against digital peers – analyzing high–growth, high–fee competitors like Remitly alongside the sheer volume potential proven by Revolut’s 6 billion dollar revenue base.

Exposing the technical Platform disclosure changes that hide the volume acceleration inside Wise’s B2B enterprise division.

Tracking the rapid, quiet onboarding cadence of marquee global Tier–1 institutions

How deep background optimization vectors – such as large language model chat assistants and algorithmic compliance screening – systematically collapse processing costs.

Wise’s path to becoming a $100B company

Disclaimer: I own Wise shares. The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.