Most great businesses don’t announce themselves. They get dismissed early on, repeatedly, by people who later wish they’d looked harder.

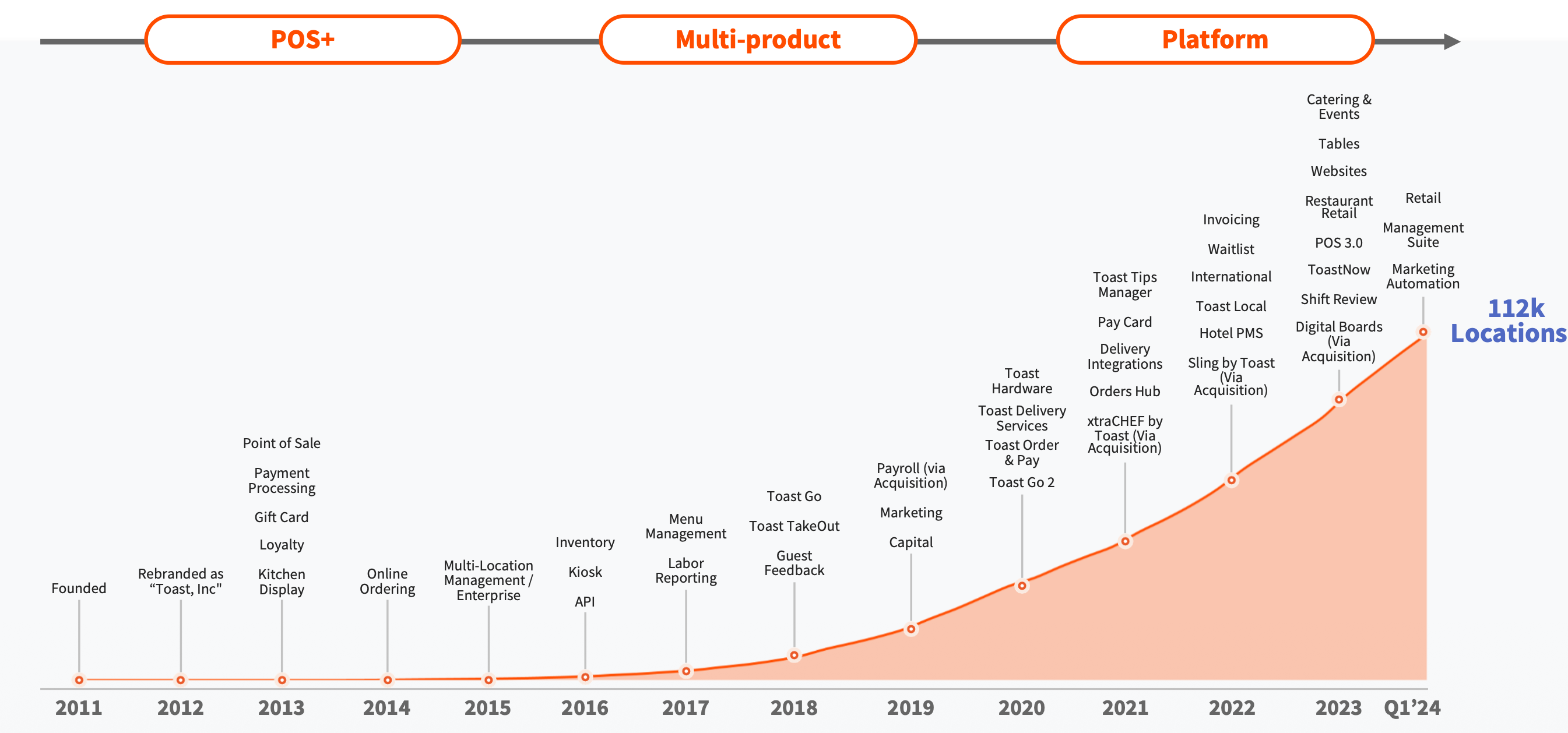

Toast is a near-perfect specimen. Roughly twelve years ago, three MIT graduates, Steve Fredette, Aman Narang, and Jonathan Grimm, started the company in Aman’s basement in Burlington, Massachusetts. Their first idea failed. They had set out to build a consumer app that let diners skip the agony of waiting for the check, only to discover that the legacy restaurant systems they needed to plug into were too clunky to integrate with anything. So they threw the idea out and did something far more ambitious. They rebuilt the entire restaurant technology stack from the ground up.

2024 Investor Day

When they went looking for money, most investors said no, and not politely. Selling software to small restaurants was, in the prevailing wisdom, a terrible idea. Owners weren’t tech-savvy. Margins were razor-thin. The whole category was a graveyard waiting to happen.

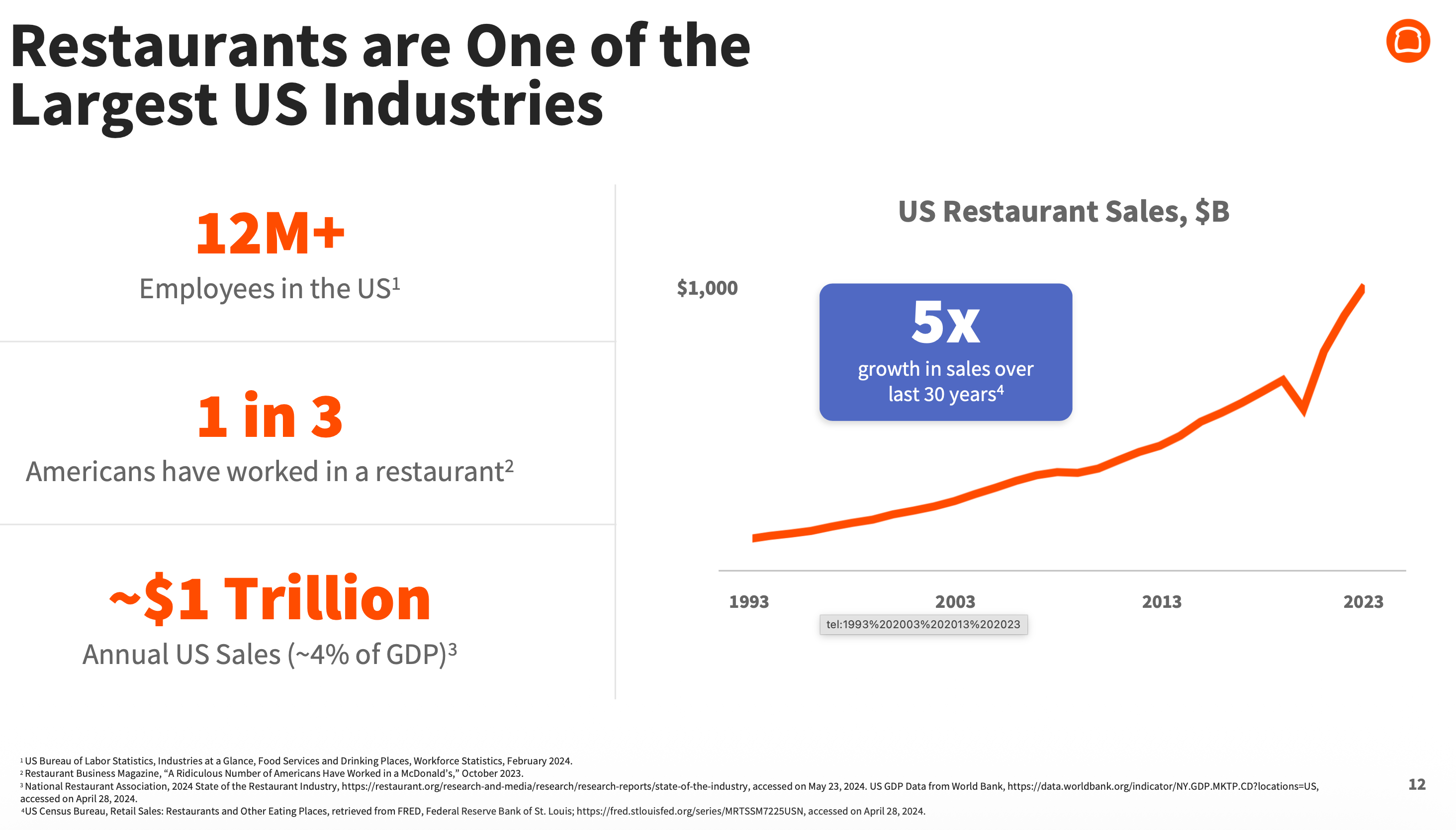

Look at what that “terrible idea” became. Today Toast powers roughly 171,000 locations, up from a single customer in 2013 and up +22% YoY. Over the trailing twelve months, it processed a staggering $204 billion in gross payment volume. Something close to half a percent of total U.S. GDP now flows across its platform.

And this isn’t a tool reserved for corner delis and food trucks, though it serves plenty of those. Toast runs more than half of all Michelin-starred restaurants in the United States, and over a third of all James Beard Award winners. The finest kitchens in the country, the ones obsessed with every gram and every second, chose the same operating system.

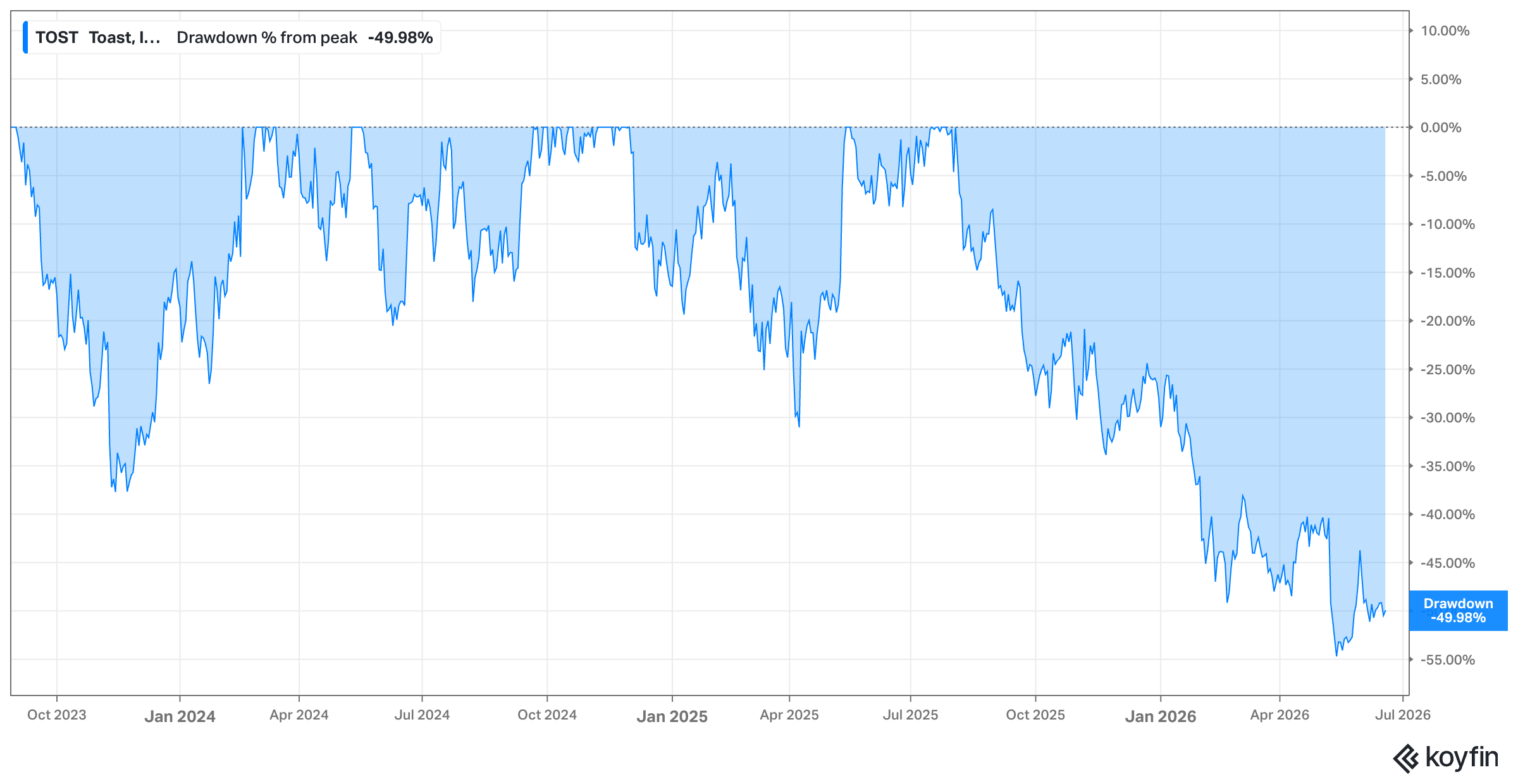

So here’s the puzzle that pulled me in. If Toast is this entrenched, this profitable, this dominant in a $1 trillion industry, an industry it has barely begun to penetrate, why was the stock cut roughly in half over the last year, trading close to record-low multiples?

Because that’s where the stock is at as I write this.

Toast traded down around 50% from its all-time high, languishing in the mid-$20s ($14B market cap) while the business underneath it posted record results, grew subscription services and financial technology solutions gross profit 32% YoY, and added a record number of locations.

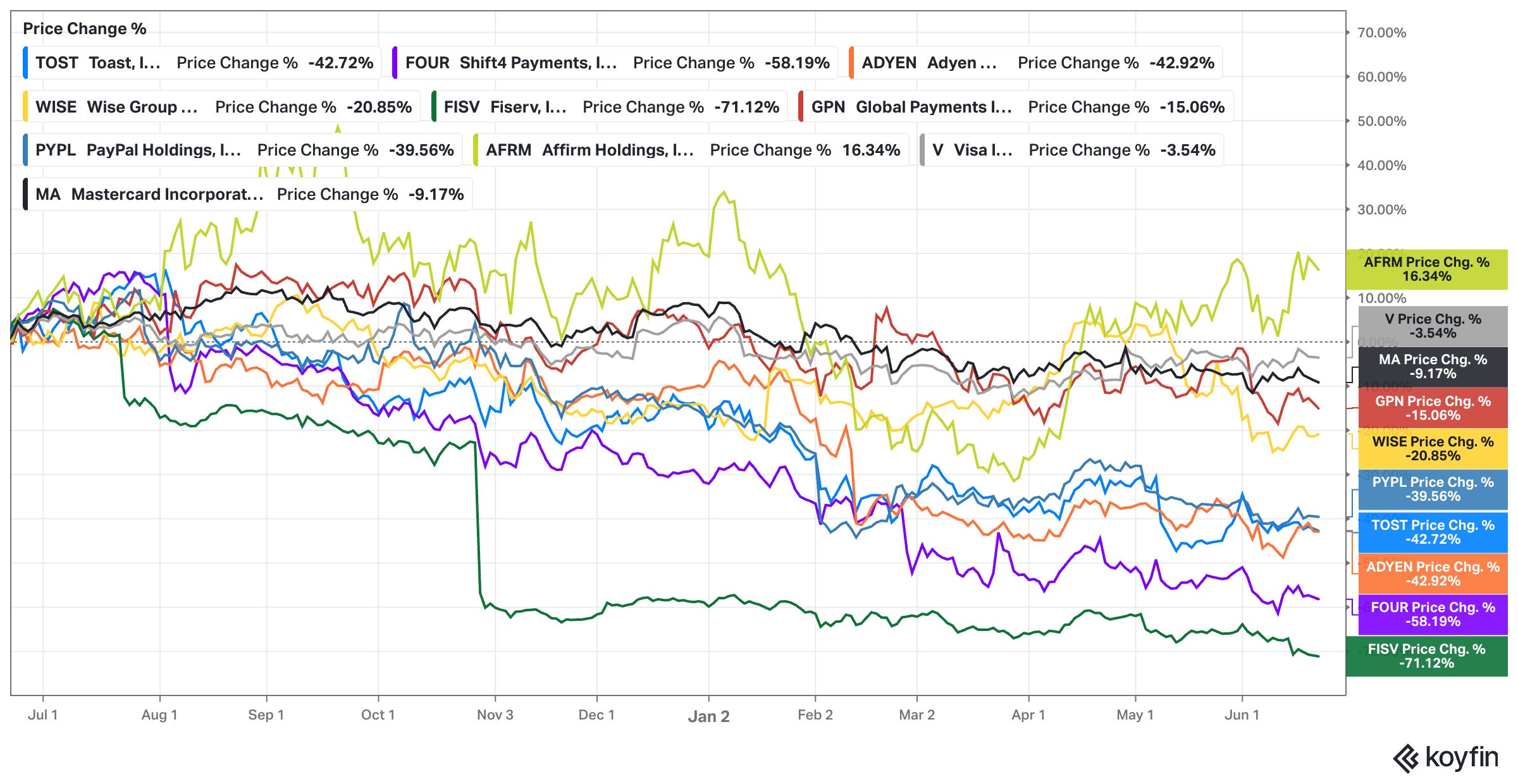

Arguably, the drawdown wasn’t triggered by anything “breaking.” I believe, it might have been triggered by the market deciding it would rather own something else. And this is where Toast’s situation gets genuinely interesting, because the company has the misfortune of sitting at the intersection of two of the most unloved corners of the market right now. It is part payment processor and part vertical-market software company, and capital has been fleeing both.

Payment stocks’ LTM performance

Money is being pulled out of fintech and SaaS at a remarkable clip and funneled into anything that can credibly attach the letters “AI” to its story.

Toast, ironically, is quietly building one of the more compelling vertical AI businesses around. The market just hasn’t decided to pay it for that yet. It’s been too busy selling.

That dislocation is the reason I’m writing this. When a high-quality business gets sold off for reasons that have little to do with the business, you get the rare setup every investor claims to want and few actually act on: a chance to buy something excellent while the crowd looks the other way.

Whether that’s what’s happening here, or whether the bears have spotted something real about competition, margins, and a stretched valuation, is exactly what I intend to find out.

I’ll lay out the bull case in five “Bams,” then spend the rest of this deep dive trying to break it. Understanding the business. The moat. Management. The risks. And finally, what it’s all worth.

By the end, you should be able to decide for yourself whether the market is handing you a gift or a warning.

Let’s get into it! (This was another fun one, and I hope you find it as enjoyable)

What this deep dive covers:

The five-part bull case (”Bam Bam Bam Bam Bam”)

What went wrong

The origin story

The business itself

Unit economics analysis

The moat

The customer

Is it a good business in a good industry

The spawner thesis

Growth drivers and forecasting

Margins outlook

Valuation

Disclaimer:

As of the date of publication the author doesn’t own shares in the company; but that may change. The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

As always, before I get into the weeds, a quick word on how I like to frame these deep dives:

I always come back to Bill Miller’s take on pitching a stock. His point is brutally practical. Portfolio managers have ultra-short attention spans, and as he tells it, there is basically no successful PM he’s ever met who wanted to hear a story longer than 90 seconds. Peter Lynch apparently kept an egg timer on his desk. An analyst walked in, the timer started, and the pitch had to be done in 90 seconds flat. The format Miller recommends is disarmingly simple: here’s the company, here’s the price, here’s the 52-week range, and here are the five reasons it’s a buy. Bam. Bam. Bam. Bam. Bam. Then what it’s worth, why, and the risks.

So that’s the structure I’ll borrow for this opening section. Five pillars. Five reasons Toast (NASDAQ: TOST) deserves a spot on your radar right now, each one a “Bam” that I’ll fire off before going deep on the business later in the post.

One semantic point that matters more than it might seem. I’m deliberately calling this an investment hypothesis rather than a thesis. A thesis is a statement of belief, and the word quietly nudges you toward hunting for information that confirms what you already think. A hypothesis is something you’re actively trying to break.

With that out of the way, let me load the first round.

Bam #1: The Generational Shift from Legacy to Cloud

The restaurant industry is one of the largest sectors of the U.S. economy, somewhere around $1 trillion in annual sales, or roughly 4% of GDP.

2024 Investor Day

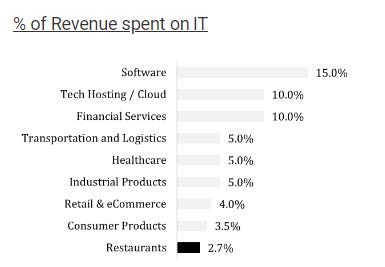

And yet it sits near the back of the class when it comes to technology. Most industries spend something like 5% of revenue on IT. Some (significantly) more. Restaurants, according to a 2022 VIC writeup, spend less than 3%, around 2.7%.

Avasant’s annual IT spending and staffing benchmarks study covers over 25 industry sectors, including food and beverage, and continues to confirm this structural gap: IT spending as a percentage of revenue deviates far more by industry sector than by company size or geography.

That gap didn’t appear by accident. For decades, the industry ran on manual paper processes and a fragmented collection of “point solutions” that never really talked to one another, so the under-investment compounded year after year.

The restaurant management software market was valued at about $6.54 billion in 2025 and is projected to grow from $7.49 billion in 2026 to $14.73 billion by 2031, at roughly a 14.5% CAGR, with cloud technology identified as the driver. Critically, cloud solutions accounted for 60.87% of that market’s revenue in 2025 and are growing faster than hybrid and on-premise alternatives.

Picture the setup that dominated for most of that period. Incumbents like Oracle, through its Micros division, and NCR, with its Aloha product, owned the market with on-premise architecture. The hardware lived on dedicated physical servers, frequently parked in a restaurant basement or a sweltering back closet. Those boxes fail. They’re expensive to maintain. And when one goes down, so does a chunk of the operation. Worse, the legacy stack lacked modern APIs, which forced operators into an inefficient patchwork of separate vendors for online ordering, payroll, and inventory. Staff ended up manually re-entering the same data across systems that refused to communicate, a recipe for errors and constant operational friction. The data itself sat trapped in disconnected silos, which meant owners historically made decisions on gut feel rather than anything resembling real-time analytics. A legacy nightmare, basically.

This is the opening Toast walked through. The company is replacing those clunky terminals with a cloud-based “restaurant operating system” meant to act as the central brain of the business.

2024 Investor Day

What makes it more than a generic cloud play is the vertical-specific depth. Toast obsesses over the thousand little things that are specific to restaurants: hardware engineered to survive grease and heat, software that handles the genuinely messy problem of complex menu SKU modifications and ingredient-level inventory. It pulls the front of house (the POS, the handhelds) together with the back of house (kitchen display systems, payroll, supplier management) so data finally flows across the whole ecosystem instead of dying in a silo.

And it’s built for high-stakes conditions. The “Offline Mode” is a good tell here. If the internet drops in the middle of a packed Friday night, the restaurant keeps taking payments and firing orders to the kitchen anyway. For an operator, that reliability isn’t a nice-to-have. It’s the difference between a normal shift and a catastrophe.

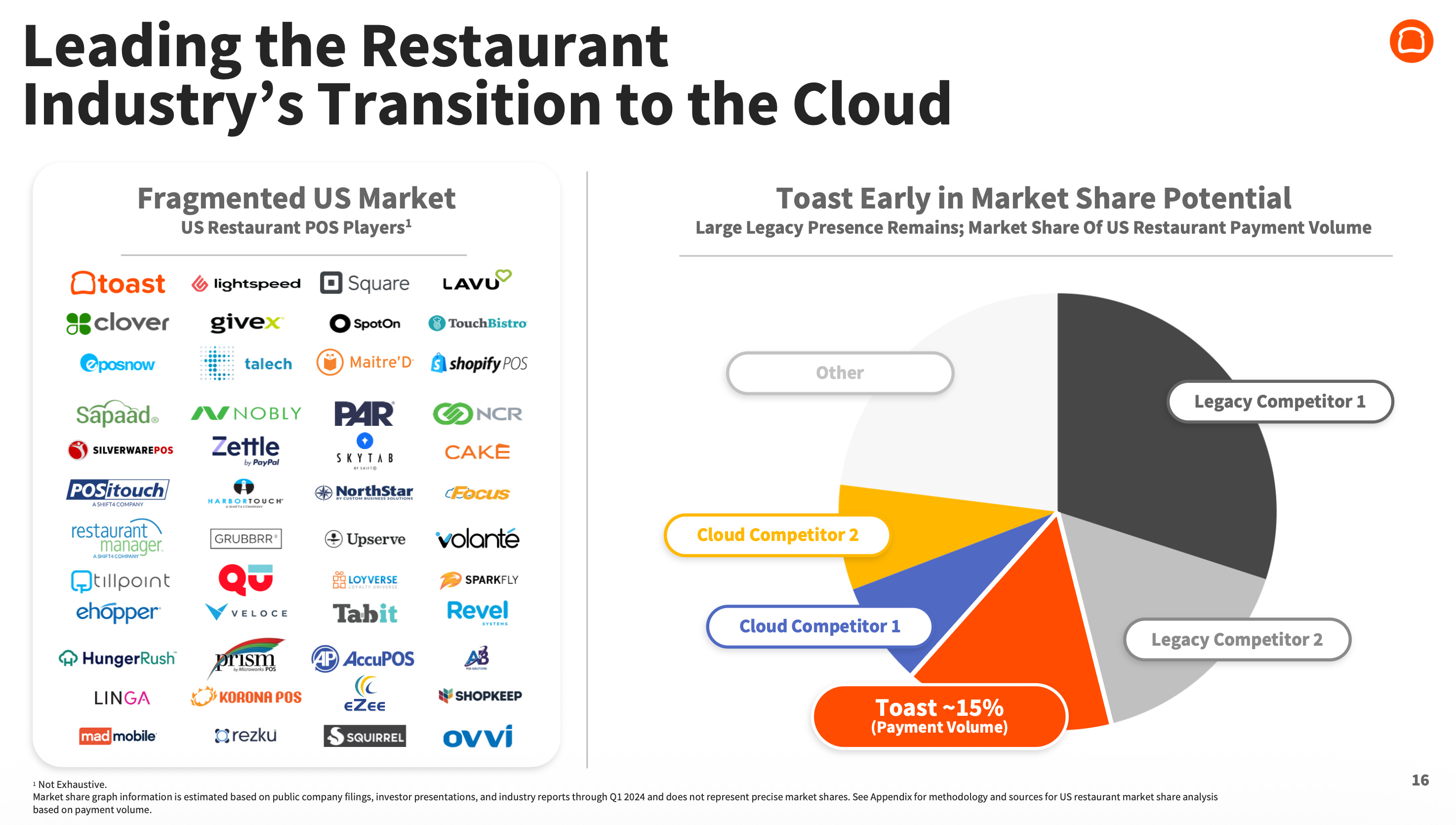

Here’s the part that makes this a hypothesis worth the effort, though. The generational shift is still in its early innings. The legacy players still hold close to 50% of the market. They are, in effect, the share donors, and Toast is the primary beneficiary as their increasingly frustrated customers go looking for something modern and flexible.

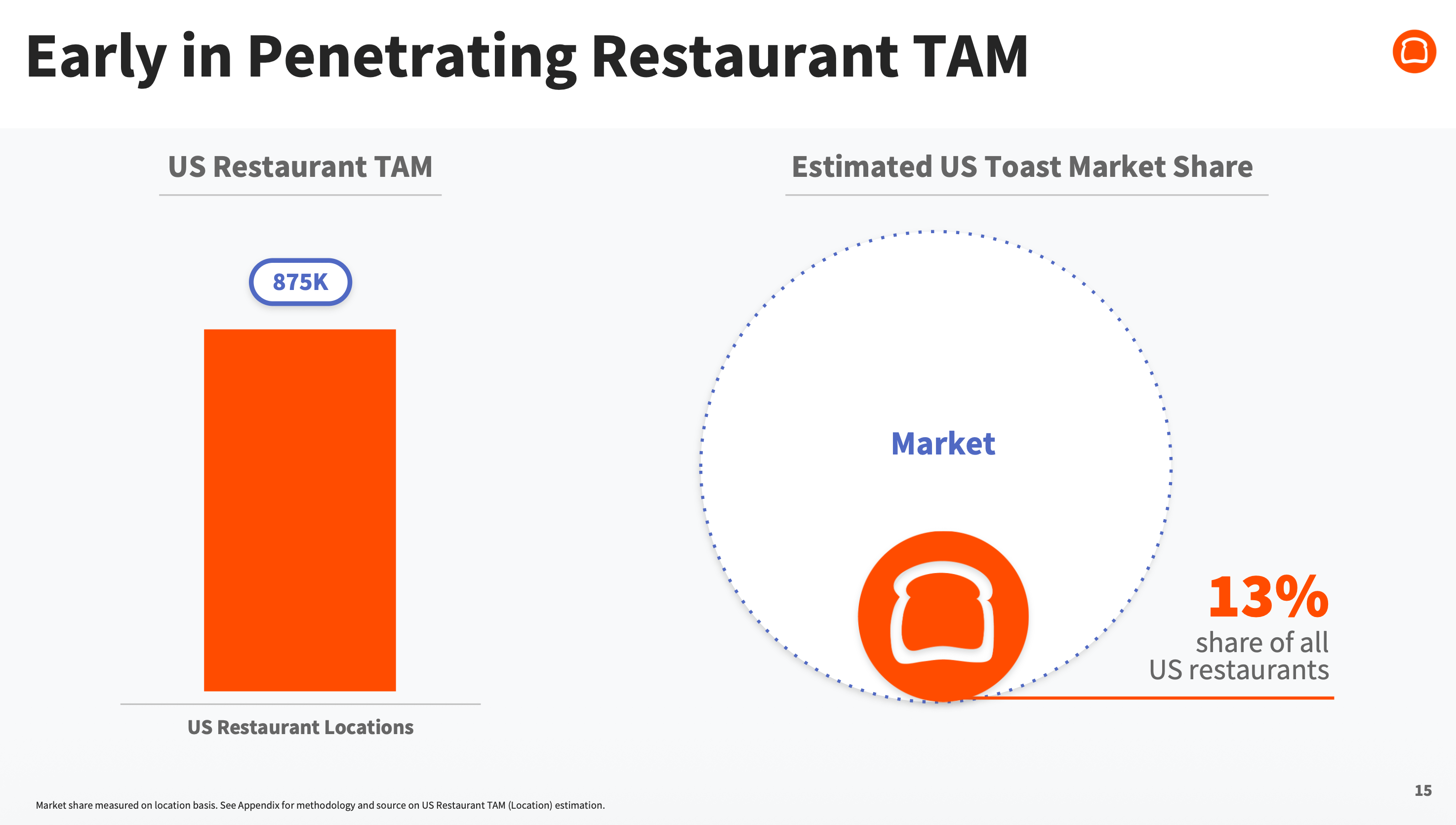

Consider the runway. For all its growth, Toast today powers only about 13% of U.S. restaurant locations (as of the 2024 Investor Day), roughly 170,000 of them (as of the latest quarter).

2024 Investor Day

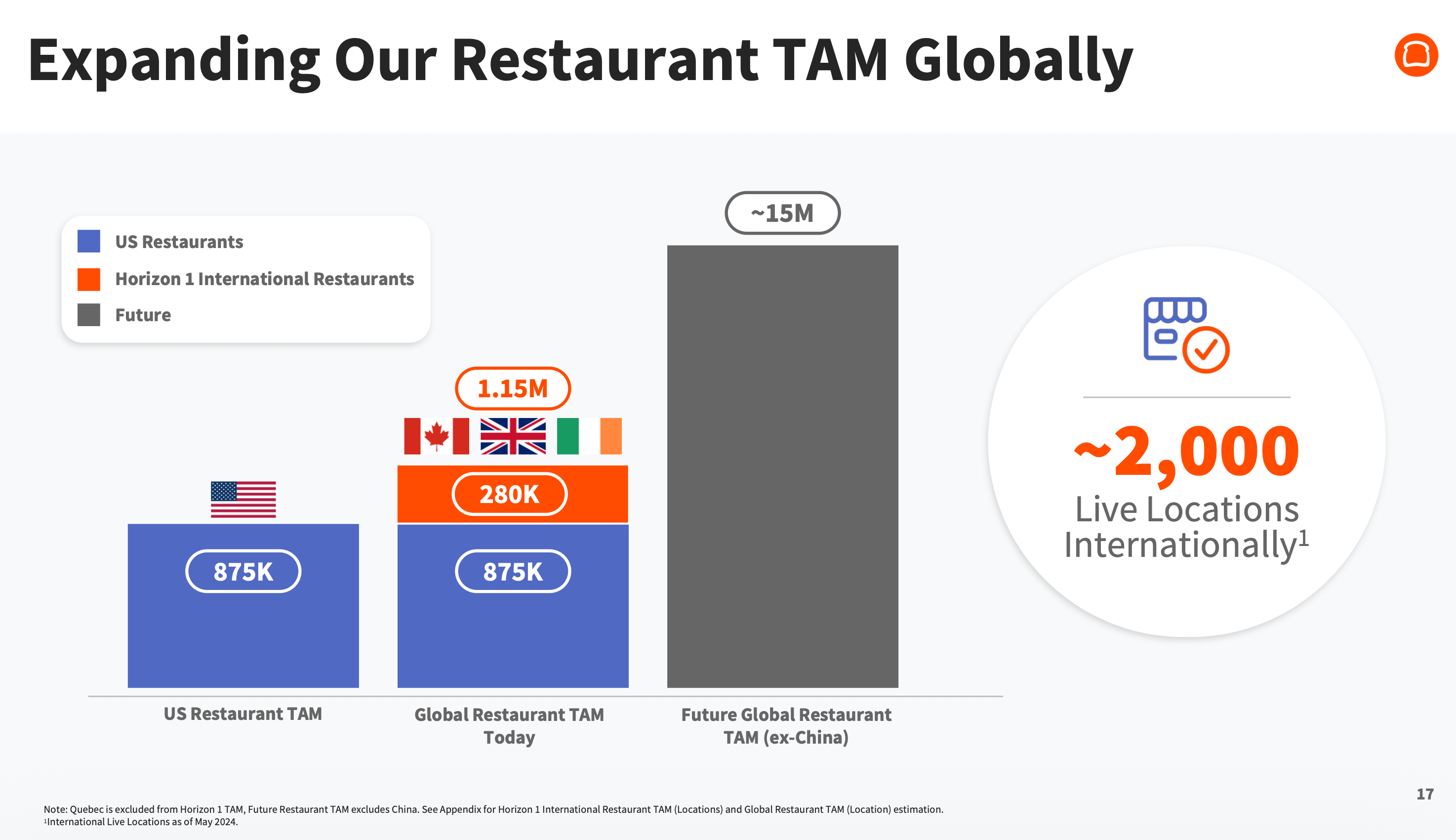

Management frames the rest as a vast greenfield, pointing toward a global TAM they peg at something like 15 million locations as international markets eventually march through the same legacy-to-cloud transition the U.S. is living through now.

2024 Investor Day

Whether you take that 15 million figure at face value is a fair question (what % of the TAM is actually obtainable?).

But the direction of travel is hard to argue with.

This is where it gets interesting

Become a paying subscriber to read the rest of this post and get access to all of my other research, including valuation spreadsheets, deep dives (e.g. well-known mid- and large caps such as LVMH, Duolingo, Meta, Edenred as well as more hidden gems such as Tiger Brokers, Digital Ocean, Ashtead Technologies, InPost, Timee, and MANY more), and powerful investing frameworks.

As a member, you get:

Complete Access: Every deep dive in our library

The WhatsApp Community: Real-time discussion and networking with like-minded investors.

Digital Investing Conferences: Around three times a year, we also hold digital conferences where members present and share stock ideas, and discuss broader themes, and we’d love for you to join in!

Incredible Value: Full access to all of this for less than $1/day.

PS: Using the app on iOS? Apple doesn’t allow in-app subscriptions without a big fee. To keep things fair and pay a lower subscription price, I recommend just heading to the site in your browser (desktop or mobile) to subscribe.