Deep Dive: Nintendo ($NTDOY)

Despite near-term volatility, Nintendo's evolving business is poised to return to peak profitability

Nintendo is no ordinary company. Founded in 1889 as a playing card manufacturer, it’s a story of survival, reinvention, and unlikely triumph.

Over the years, it has weathered near-bankruptcy, transformed from a niche card business into the world’s leading entertainment company, and solidified its place as a titan of the gaming industry.

What’s most striking, though, is how Nintendo continues to reinvent itself while staying true to its core philosophy: long-term survival over short-term gains.

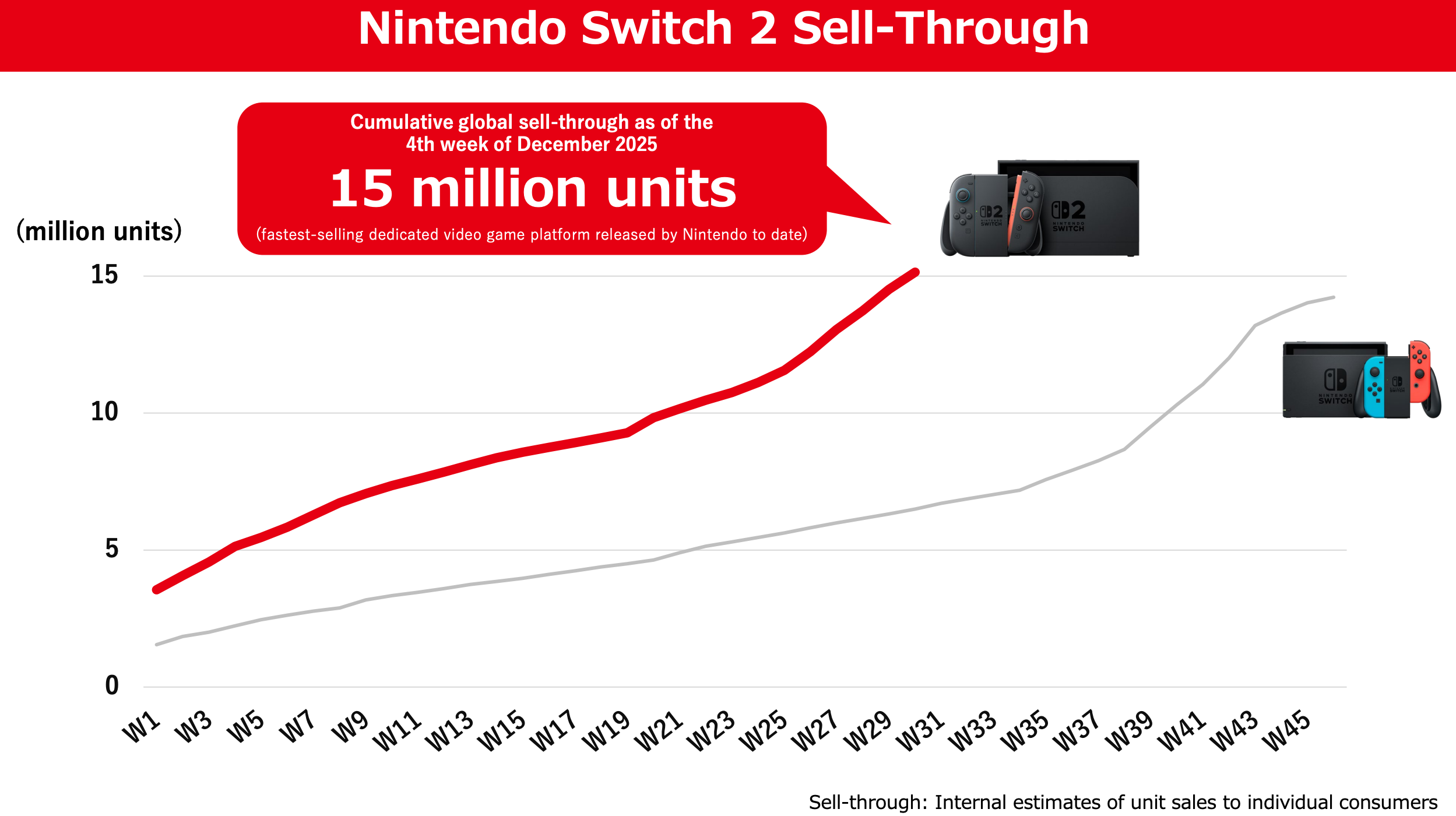

Fast forward to 2025. The Nintendo Switch 2, launched with skepticism from critics, has shattered all expectations. It has become the fastest-selling console in history – 3.5 million units sold within just four days, 15 million in six months.

This is a company that’s not just surviving but thriving, breaking records and pushing boundaries.

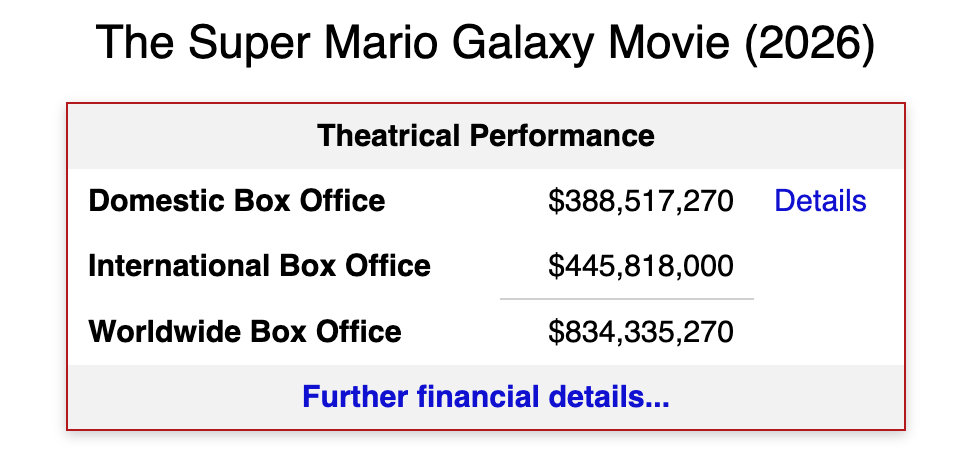

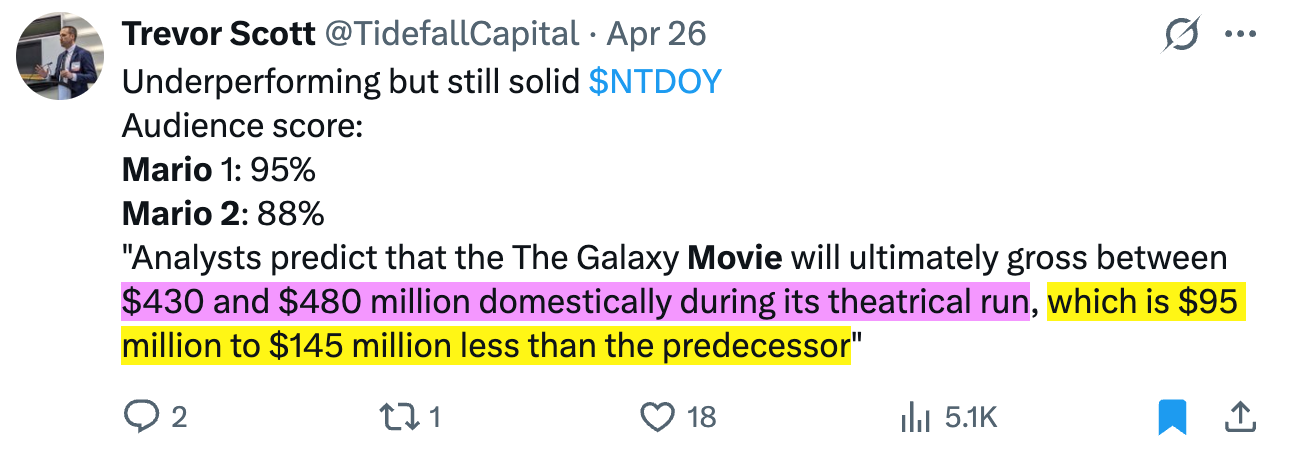

And of course Nintendo’s recent success is not just about the recent hardware sales records – if anything, hardware is the enabler of the broader Nintendo thesis –; no, Nintendo has become a self-funding marketing machine. The success of The Super Mario Bros. Movie, which grossed over $1.36 billion, directly boosted game sales, essentially turning its own movies into profit-generating advertisements.

This is the kind of business model that’s rare in any industry.

Perhaps most impressive of all is Nintendo’s $13-14 billion fortress balance sheet. With zero long-term debt and a robust cash position, the company has the freedom to weather any storm and invest in its future, whether that’s through new IP or expanding its already vast gaming ecosystem. Add to that its 400 million Nintendo Accounts, ensuring customer retention across platform generations, and the company is in a much stronger position than it was during the cyclical “boom-bust” hardware cycles of the past.

From a strategic point of view, Nintendo is also positioned well. While Sony and Microsoft continue to duke it out in the performance arms race, Nintendo has carved out a unique niche, competing on intuitive gameplay and portability, not raw hardware specs. This deliberate choice has given Nintendo a near-unassailable lead in the family-friendly gaming space, where it faces little direct competition.

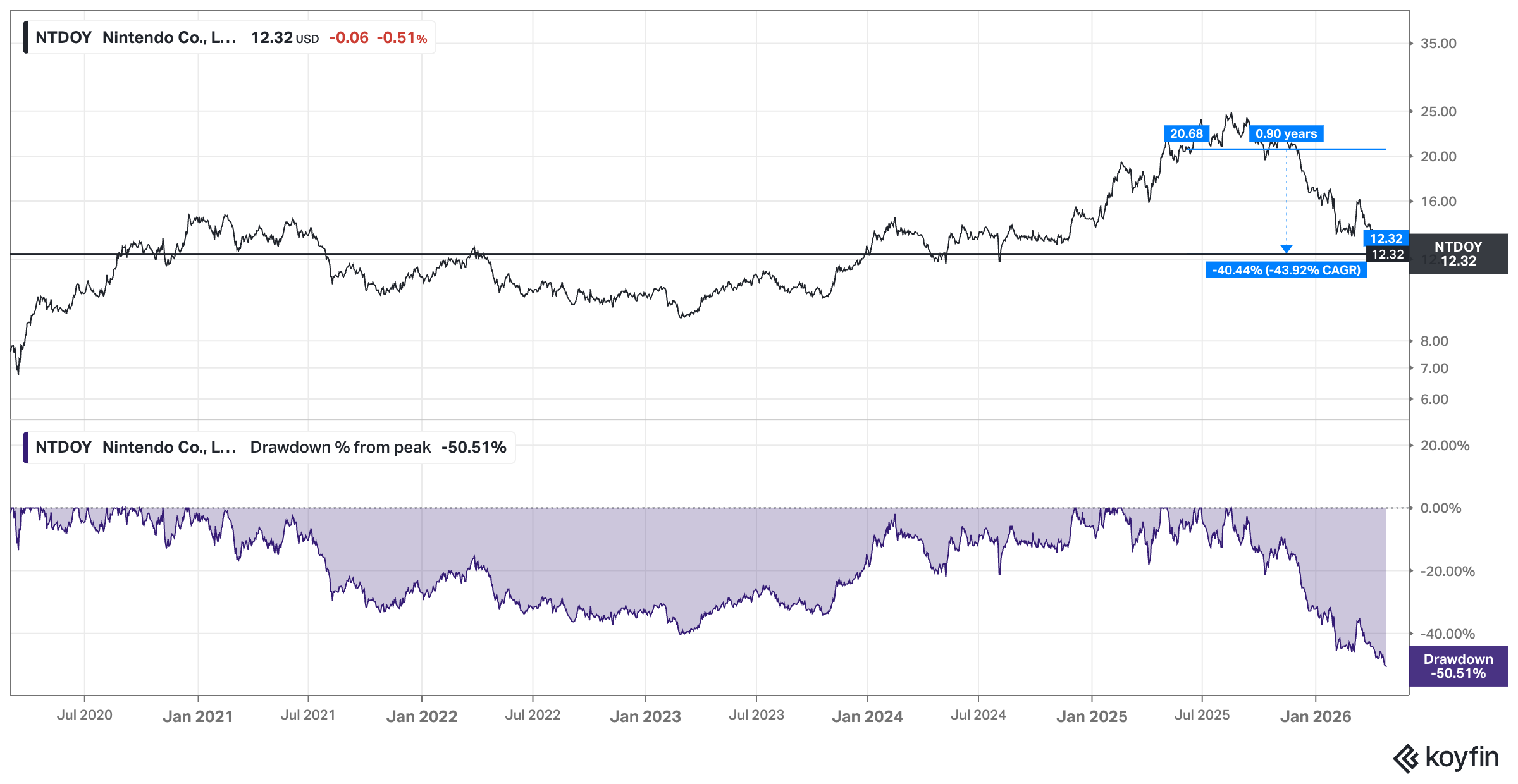

In this post, I’ll explore how Nintendo’s unique approach to business, combined with its world-class intellectual property, gives it an edge that few companies can match. From the fastest-selling hardware in history to a growing digital ecosystem and unparalleled financial stability, Nintendo is shaping up to be one of the more interesting opportunities in the entertainment sector. What makes the setup especially compelling right now is the disconnect between the business and the stock. Despite the strong fundamental backdrop, the shares have recently seen a drawdown of roughly 50%, now trade about 40% below the level around the Switch 2 release, and have effectively round-tripped back to 2020 levels.

To me, that is exactly where things start to get interesting. So stick around – I’ll show you why I believe the market is missing the full potential of this global powerhouse.

High-Level Thesis: “Bam Bam Bam Bam Bam”-90 Second-Hypothesis

Nintendo is currently undergoing a massive growth inflection point that the market is still (or once again?!) mispricing as a standard, legacy hardware cycle.

“Case in point, this is now the fourth time this cycle that false Nintendo narratives have been proven wrong.“ - Ryan O’Connor