For over 300 years, LSEG has been the backbone of global finance, beginning as a small coffeehouse trading post in 1698.

Today the company is almost unrecognizable to its founders. Its bold 2021 all-shares $27 billion acquisition of Refinitiv transformed LSEG into a global leader in financial data and infrastructure, now deriving nearly 98% of its revenues from proprietary data and market infrastructure.

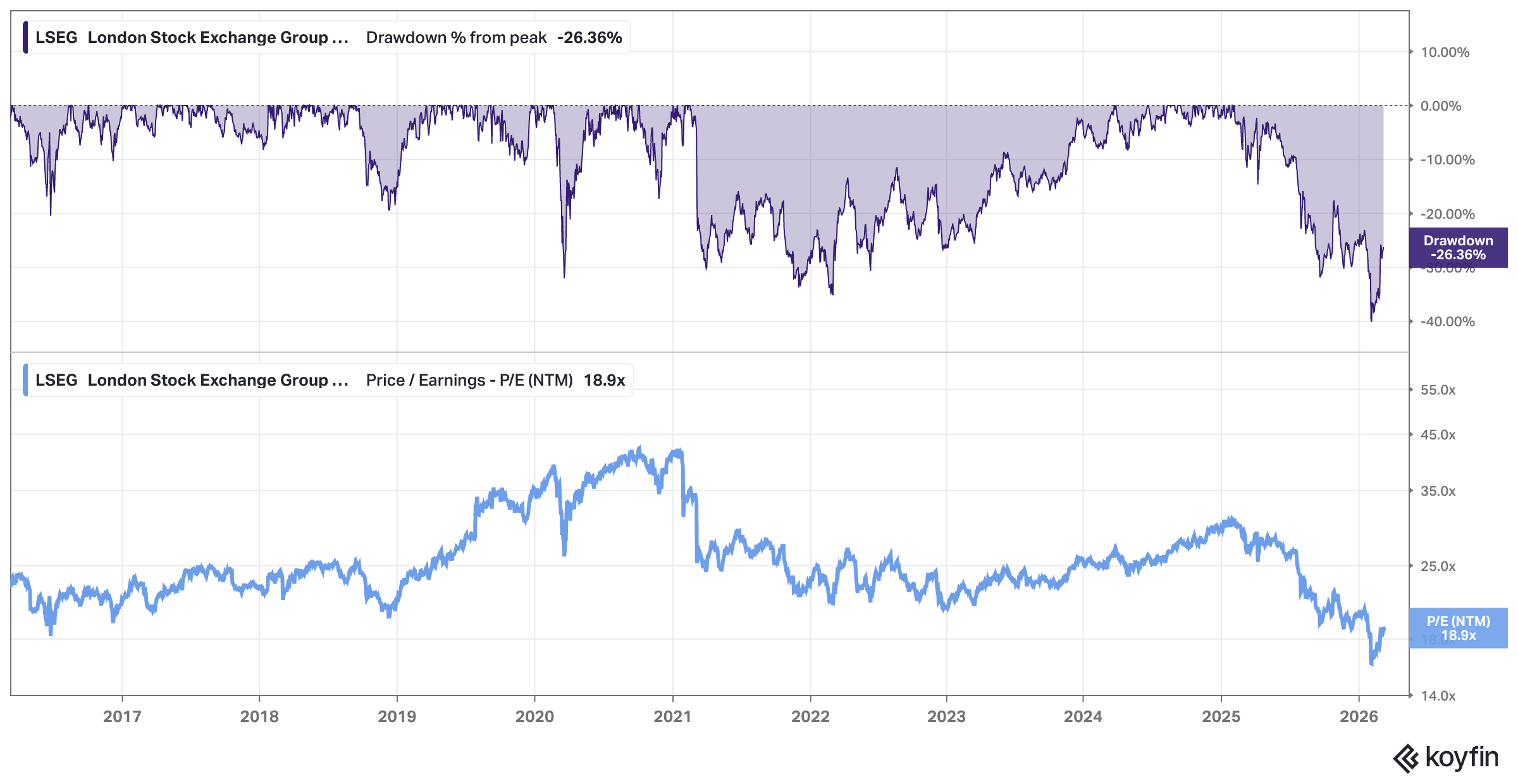

Over the last year, however, the London Stock Exchange Group (LSEG) has faced a turbulent ride in the stock market. Trading at an all-time high back in 2025, the company has now seen its stock price fall by 25%, even dropping as much as 40% at its lowest point – reaching a 10-year low valuation.

LSEG’s stock price has now also been flat for almost six years, while its NTM P/E has come down from above 40x at one point to 19x now.

At the heart of this downturn, I believe, lies a growing fear among investors that artificial intelligence (AI) will disrupt LSEG’s core business, especially its Data & Analytics segment, which makes up nearly half of its total revenue. The launch of Claude’s Co-Work agents and the hype surrounding AI’s potential to commoditize financial data have led to indiscriminate selling, as investors worry that LSEG’s user lock-in might no longer offer the same competitive edge. As mentioned, the company’s price-to-earnings ratio (P/E) has fallen from >40x to 19x, reflecting the growing skepticism.

But is this really the beginning of the end for LSEG, or has the market overreacted?

Management argues that LSEG is more valuable in an AI-driven world, but a contrarian narrative suggests otherwise. Some critics contend that LSEG might have traded away capital-light exchange monopolies for heavy debt obligations tied to capital-intensive data assets.

Despite the panic, LSEG’s business model – heavily reliant on proprietary data, intellectual property, and market infrastructure – remains solid and highly diversified, and much of the fear revolves around whether AI could erode its core data services. Ironically, AI companies – the very entities some view as a threat to LSEG’s business – are also its clients, relying on the company for high-quality data to power their models.

It’s a somewhat complicated dynamic: AI disruption versus AI dependence.

So, as the stock plunges, it’s important to ask: are investors missing the bigger picture?

Adding fuel to the fire, Elliott Management, the activist hedge fund, has recently taken a position in LSEG, pushing for changes, signaling that the company’s current valuation might be undervalued.

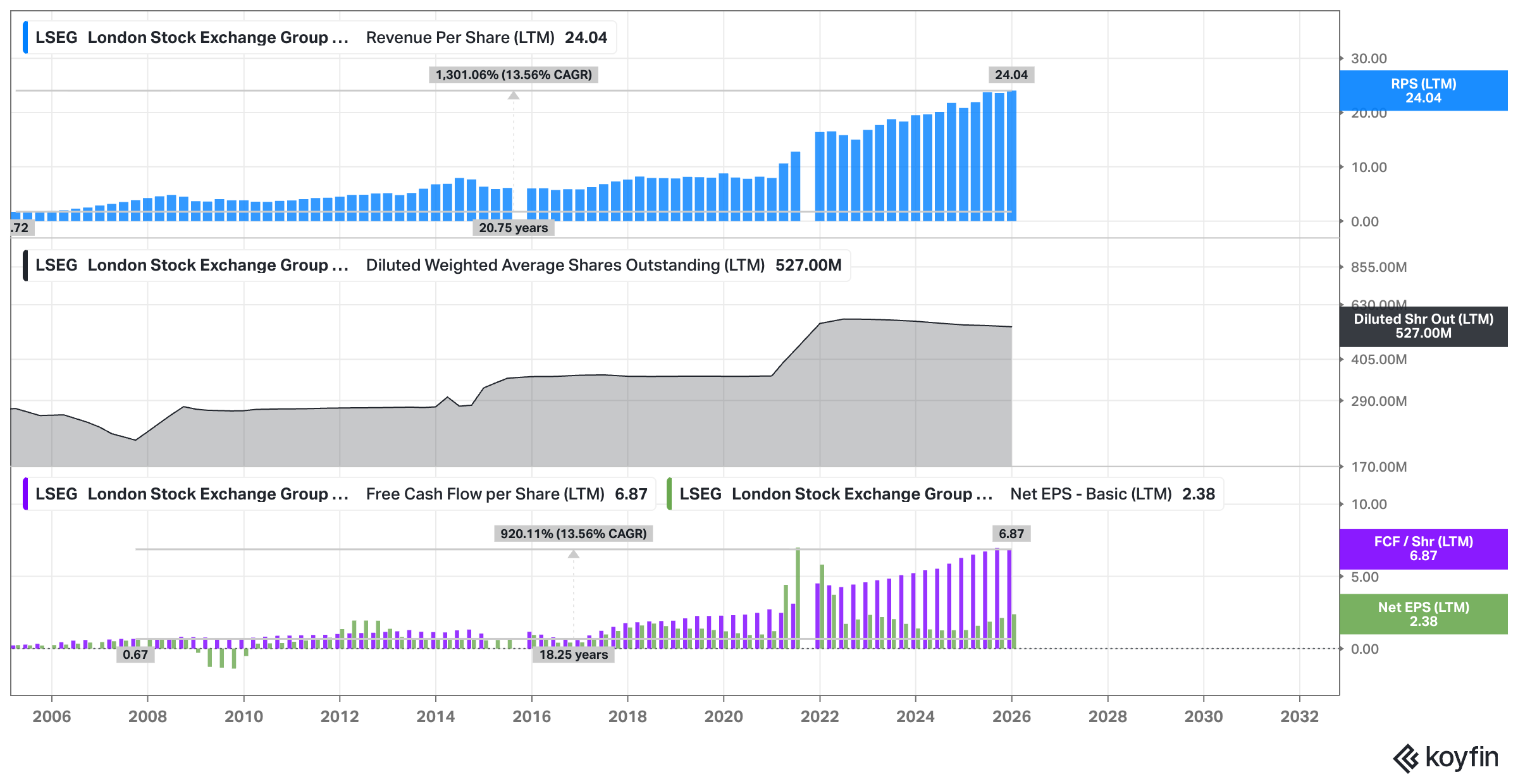

This post goes beyond LSEG’s prestigious brand and delves into the core investment hypothesis. Rather than simply confirming well-understood “beliefs,” we’ll take a critical look at whether LSEG is truly an “all-weather” compounder – EPS CAGR-ed at 15% over the last 20 years – poised for double-digit returns or a “fixer-upper” masking weaknesses through inflated “adjusted” metrics.

Drawing inspiration from Bill Miller’s famous 90-second pitch approach, we’ll – as always – at first break down five key pillars that could either make LSEG a great business pitch or a cautionary tale of private equity wealth transfer. We’ll also highlight the four key narratives that are dragging the stock down. In short, we’ll build a hypothesis that will then be tested throughout the comprehensive analysis that follows.

We’ll address the AI anxiety that has led to a valuation dislocation of course, and evaluate whether the Microsoft partnership will turn out to be a strategic masterstroke or a costly gamble, locking in billions in capital, to rescue a cracking narrative. With management pushing for AI integration and expansion into new markets, is LSEG positioned for a high-growth future, or will its fundamental weaknesses hold it back?

Disclaimer: The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

Here’s what I cover in this 18,000-word deep dive:

“BAM BAM BAM BAM BAM” 90-Second Pitch – Why LSEG and Why Now?

1) Understanding the Business of the LSEG

Business History

Product

Business Operations

Customers

Industry & Competitive Landscape

2) Business Quality

Competitive Advantages Analysis

Pricing Power

Quantitative Indicators of a Moat

Durability and Direction of the Moat

3) Management

4) Risks & Financial Health

5) Balance Sheet Perspective

6) Other Items

7) Valuation

Past Growth

Future Growth (including a TAM analysis and identifying key growth drivers)

My Valuation Work (true owner earnings, scenario analysis)

Conclusion

Appendix