Deep Dive: Grab’s Q1 Paradox – Record Profits Meet the Indonesian Regulatory Wall

The Implications of Grab’s Indonesia "Shock"

Investing in Southeast Asian tech can feel like navigating a monsoon – high visibility one moment, total chaos the next.

On one hand, the latest results in Grab posted (Q1 of FY26) reveal a business that is firing on all cylinders, delivering a massive $120 million profit for the period.

“Q1 is off to a fantastic start for us across all the financial fundamentals of our business.“ - Q1 Earnings Call

On the other hand, a sudden political intervention from Jakarta and a bruising regional oil shock have created near- and medium-term challenges.

President Prabowo Subianto’s announcement of a commission cap on ride-hailing services – effective immediately and specifically targeting the “ojol” motorcycle sector – briefly wiped 7% to 8% off the market capitalization as the news broke. When you combine that with a fuel crisis that saw prices spike sharply across the region in March, the bearish narrative had plenty of ammunition.

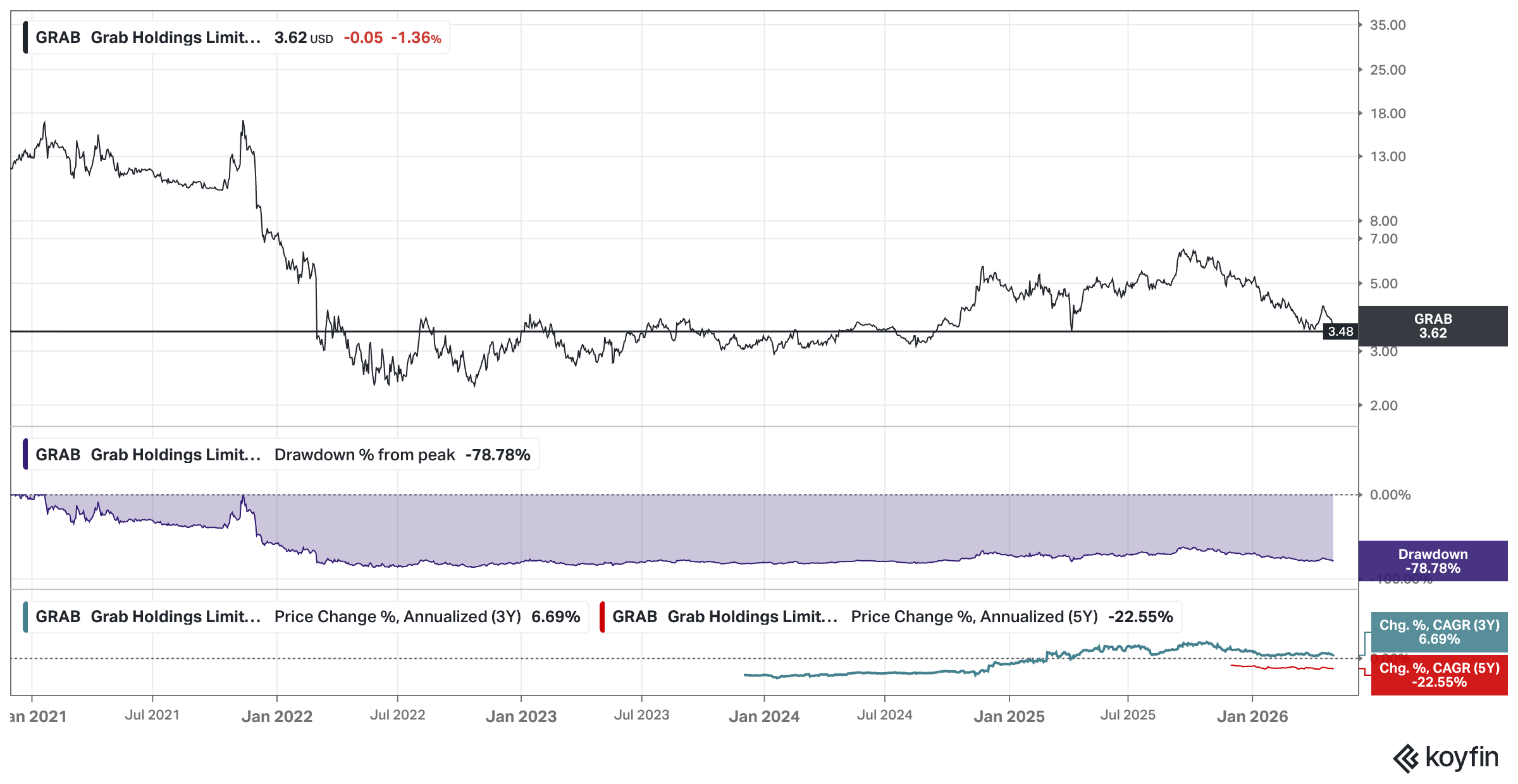

Market volatility is nothing new for Grab shareholders. If you look at the historical chart, the story is one of persistent struggle against gravity. We are, in fact, currently hovering around a critical support line that has been tested repeatedly over the last twelve months.

The technical picture remains bleak for long-term holders. A negative five-year CAGR is a tough pill to swallow for anyone who bought into the initial listing hype.

However, price and value are frequently distinct entities. While the stock initially buckled under the weight of the Indonesian news and the fuel headwinds during last week’s trading sessions, today’s pre-market reaction – up roughly 2% – suggests a more nuanced interpretation might be beginning to take hold.

This feels like a defensive posture. It is the sound of investors weighing a localized regulatory headwind and a short-term margin squeeze against a group-level performance that, frankly, exceeded some investors’ expectations.

Before I peel back the layers of this quarterly report, I recommend revisiting my broader thesis. You can find the foundational details in my Grab Holdings Deep Dive Series (four parts), where I explore the business model, the ecosystem’s structural moats, and the long-term unit economics of the superapp model, the management team, and the stock’s valuation.

Deep Dive: Grab Holdings Ltd ($GRAB) – Part 1

Imagine two Harvard Business School students, sitting together, brainstorming ideas that would go on to reshape the landscape of Southeast Asia’s transportation, food delivery, and financial services.

What I will discuss in this analysis is that, personally, I view the “Indonesia shock” and the fuel crisis not as terminal blows, but as “Darwinian filters.” The panic selling we saw earlier this week stems from Indonesia’s significant footprint. It accounts for roughly 21% of group revenue, with mobility specifically representing 36% of that total. A mandated drop in platform commissions from 20% to a mere 8% for motorcycle rides is, on the surface, a brutal hit to the top line. But as I’ll explore in the coming segments, the mechanical reality is far more complex.

I am increasingly convinced that we are seeing a “scale economies shared” business in the making. Much like the regulatory shifts that have historically impacted companies like Edenred, these interventions – alongside the exogenous pressure of rising fuel costs – often end up entrenching the dominant player. When margins are squeezed by decree or by the pump, only the most efficient, best-capitalized, and technologically superior operators survive.

The question is whether the market can look past the immediate revenue “shock” and see the reinforced moat being built underneath. I think we are seeing a fundamental decoupling of operating results from share price sentiment.

I find myself surprisingly relaxed. The runway is long. The flywheel is accelerating. And as we transition into the granular details of the Q1 results, I want you to keep one thought in mind: in a world of 8% commission caps and expensive fuel, the only thing that matters is who has the lowest cost of operation. Right now, that is Grab.

Disclaimer: I own Grab shares. The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

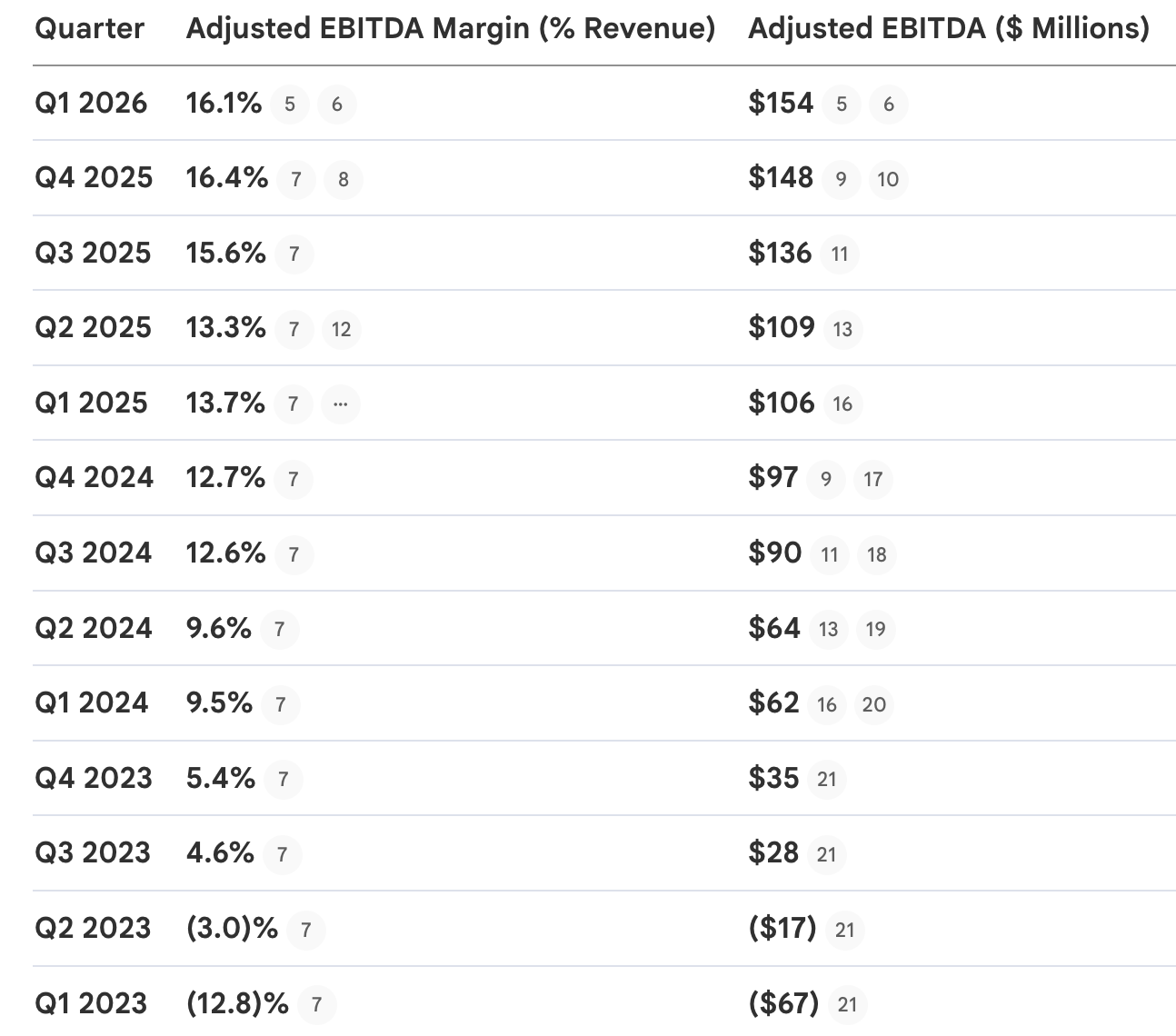

Q1 2026 Highlights: Seventeen Quarters of Momentum

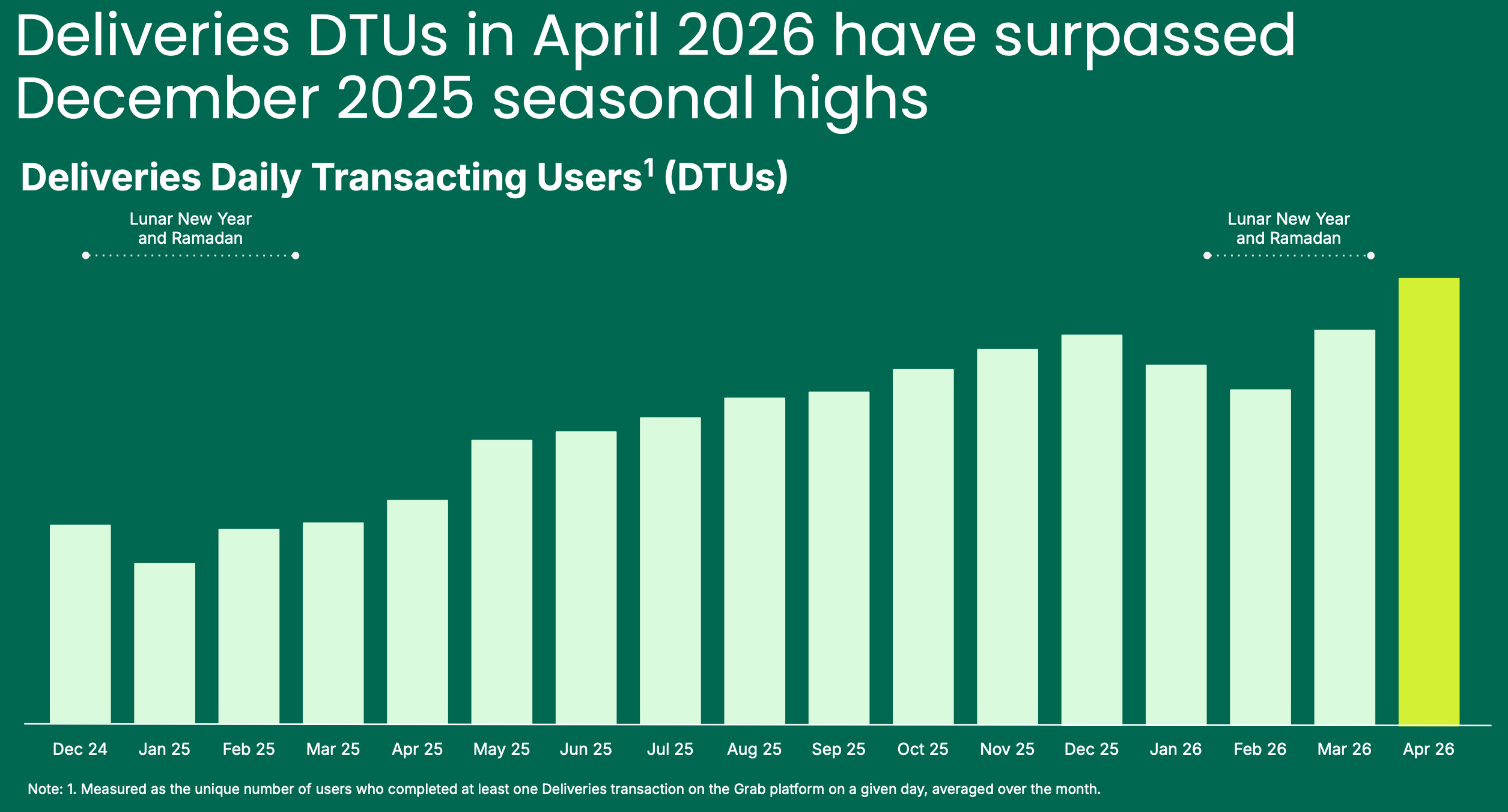

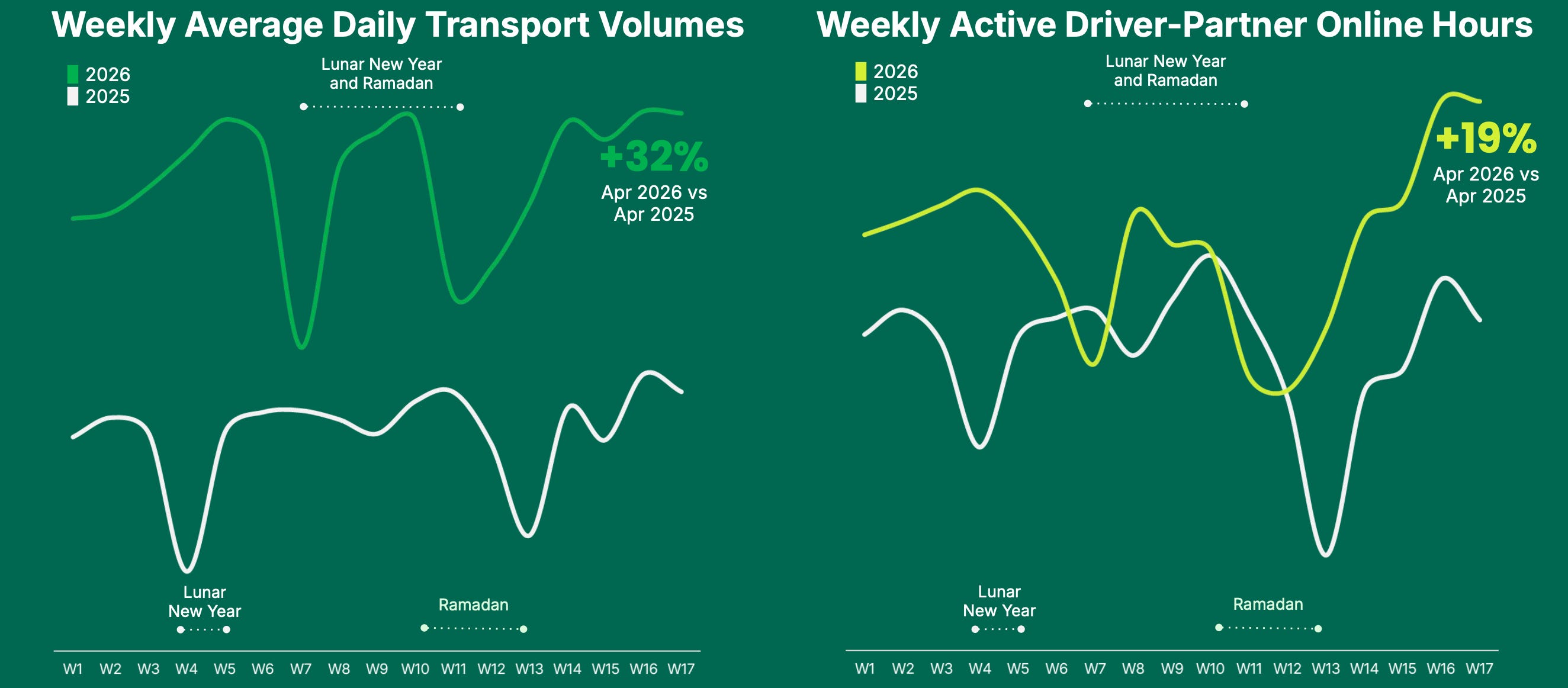

Usually, the first quarter in Southeast Asia is a period of “holiday hangovers” where the festivities of Lunar New Year and Ramadan dampen both delivery demand and driver availability.

“… the confluence of Lunar New Year and Ramadan within the first quarter, both in the first quarter this year, creating acute supply pressures as usual during those 2 festive periods.“ - Earnings Call

Yet, the latest Grab results tell a different story.

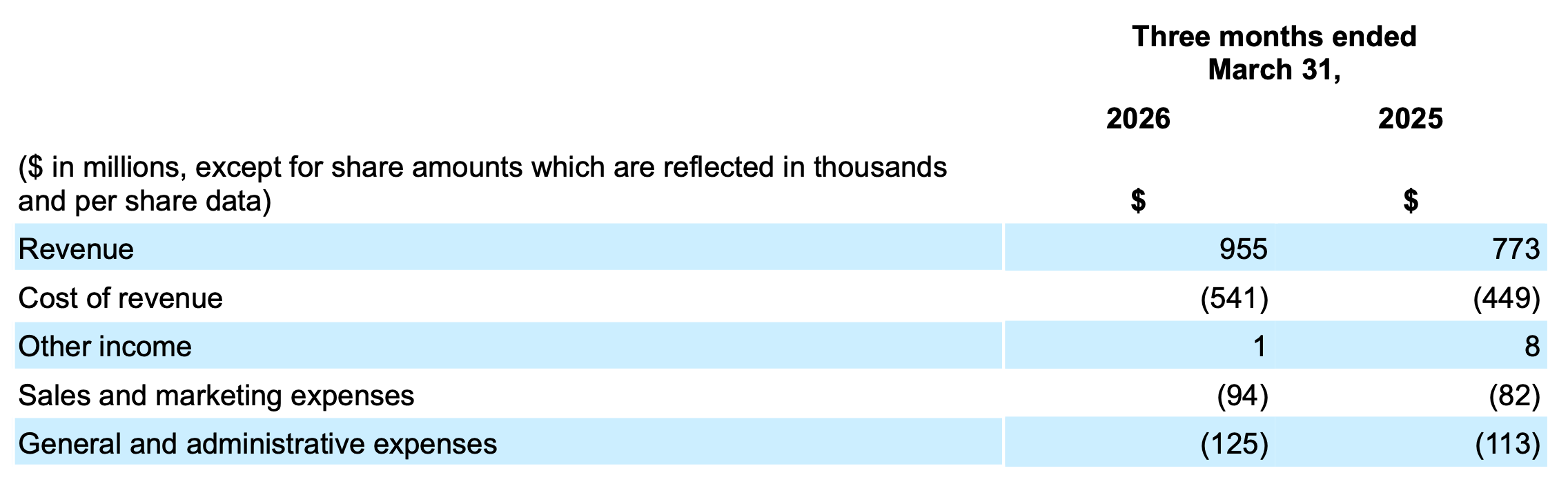

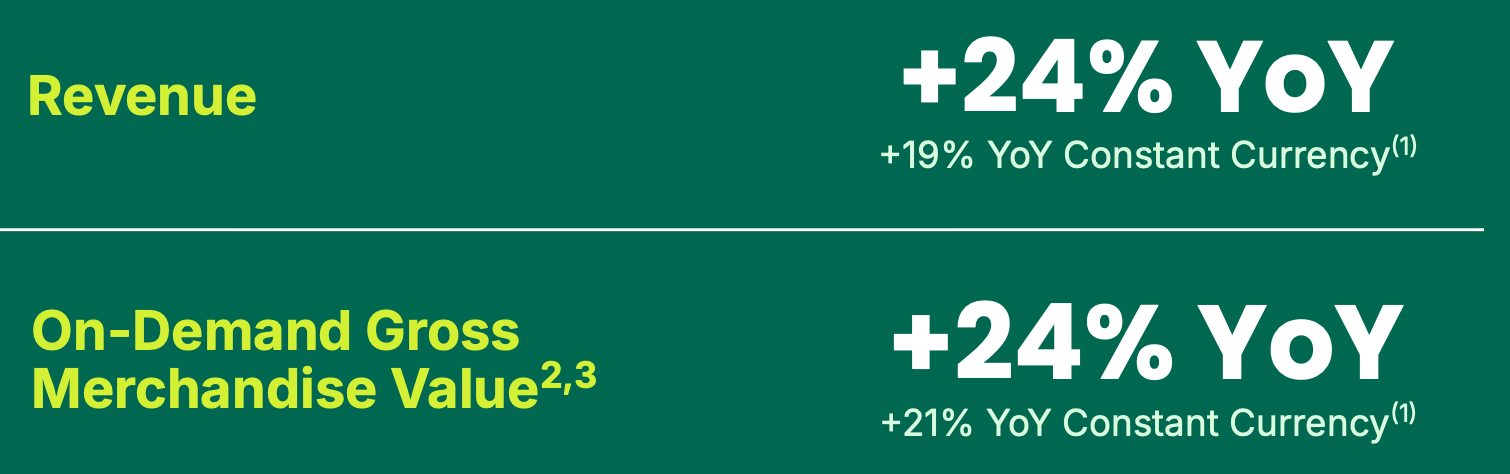

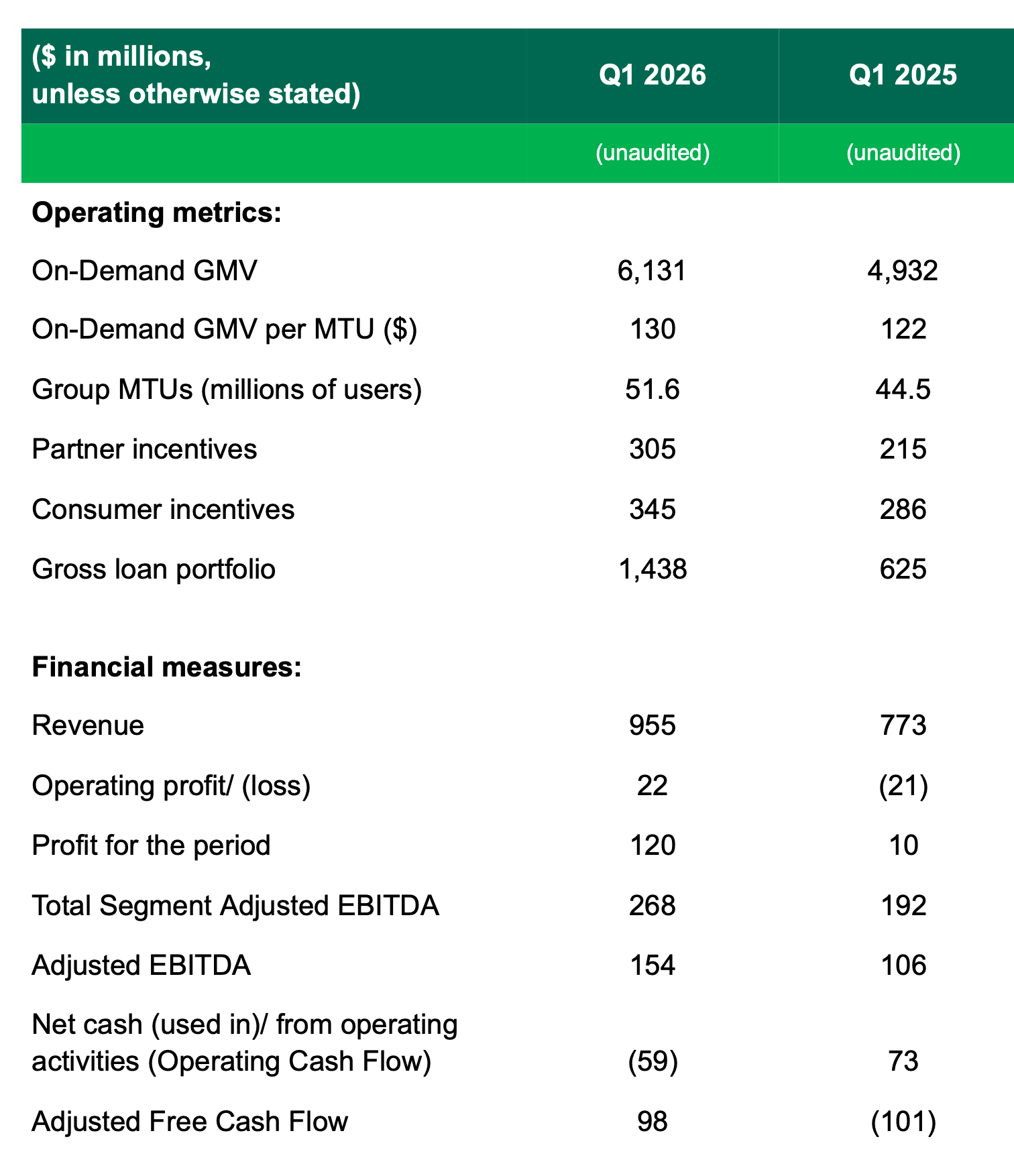

In Q1, Grab reached an all-time revenue high of $955 million, a 24% leap year-on-year (19% YoY on a constant currency basis) that suggests the platform is still finding new pockets of demand.

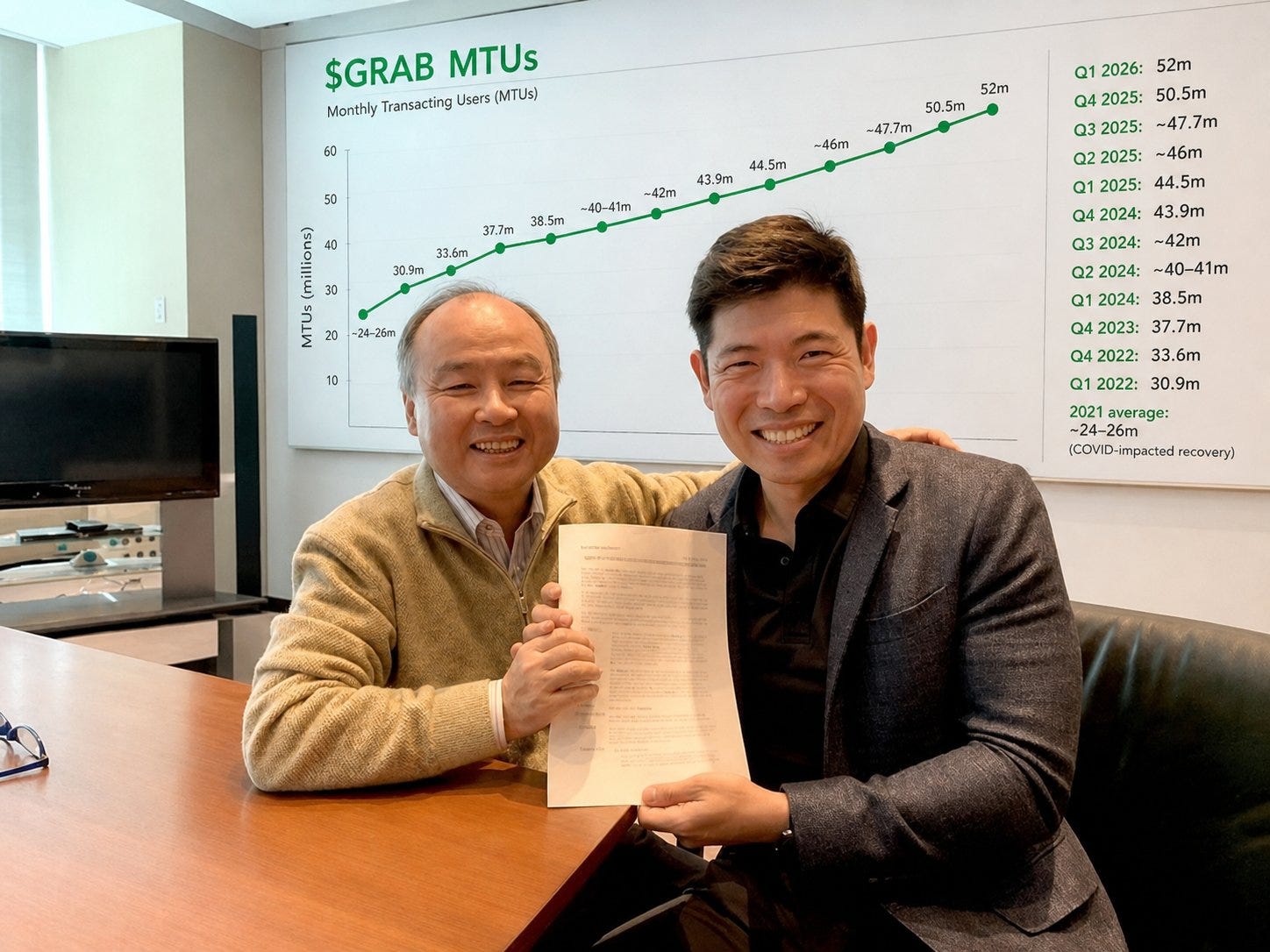

Group MTUs increased both YoY (16%) and QoQ to 52 million.

In addition, we are looking at the seventeenth consecutive quarter of Adjusted EBITDA growth. This is a testament to a compounding machine that has finally learned how to generate profits.

“As we look ahead to the rest of the year, we remain committed to delivering durable, profitable growth while standing shoulder-to-shoulder with our communities — leaning deeply into AI to outserve our users with hyper-personalized experiences, while simultaneously unlocking more sustainable earnings opportunities for our ecosystem partners.“ - Anthony Tan

Grab posted $120 million in profit for the period. The business is now self-sustaining. It generated $98 million in Adjusted Free Cash Flow this quarter alone, pushing its trailing twelve–month total to a very healthy $489 million (remember that management aims for $1.2 billion in FCF by 2028, so we’re very well on track).

For those of us who remember the days of billion–dollar annual burn rates, this feels like a historical pivot point.

This profitability is not a result of “starving” the ecosystem. On the contrary, user engagement is at record levels. As mentioned, Monthly Transacting Users (MTUs) grew 16% to 51.6 million, and the On-Demand GMV accelerated to $6.1 billion.

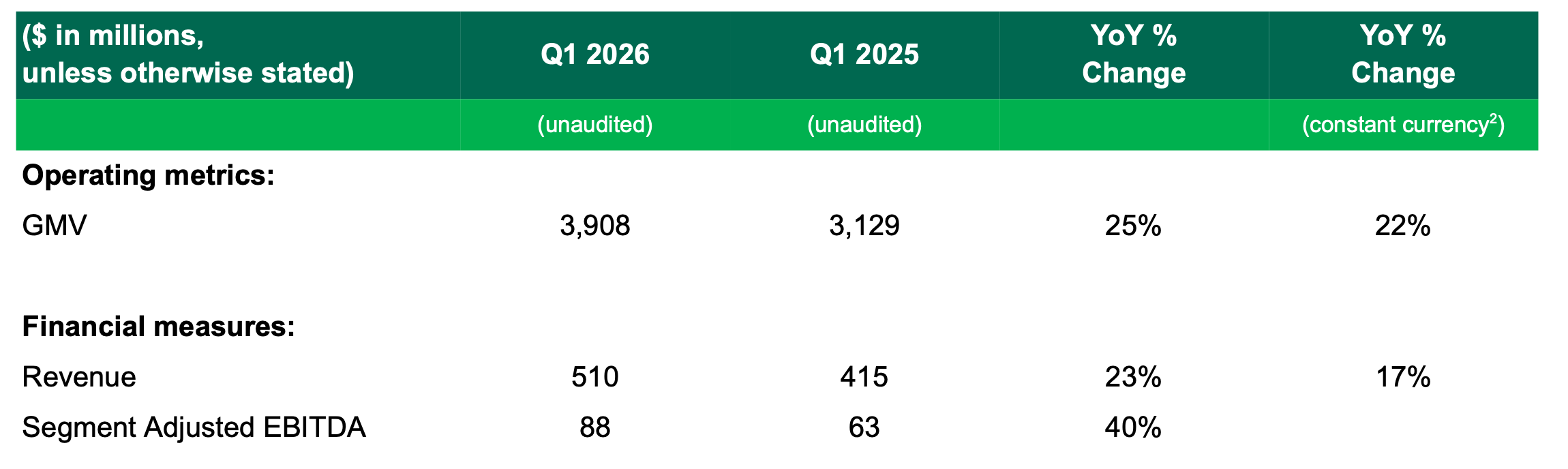

I find the segment–level efficiency particularly revealing. In the Deliveries division, GMV reached $3.9 billion despite the festive season. This was driven by a clever “barbell” strategy. On one end, affordability initiatives like Saver Deliveries and Group Orders brought in the volume. On the other hand, the segment’s Adjusted EBITDA margin improved to 2.3% of GMV (from 2%). It seems like they are capturing the budget–conscious user without sacrificing the overall margin profile.

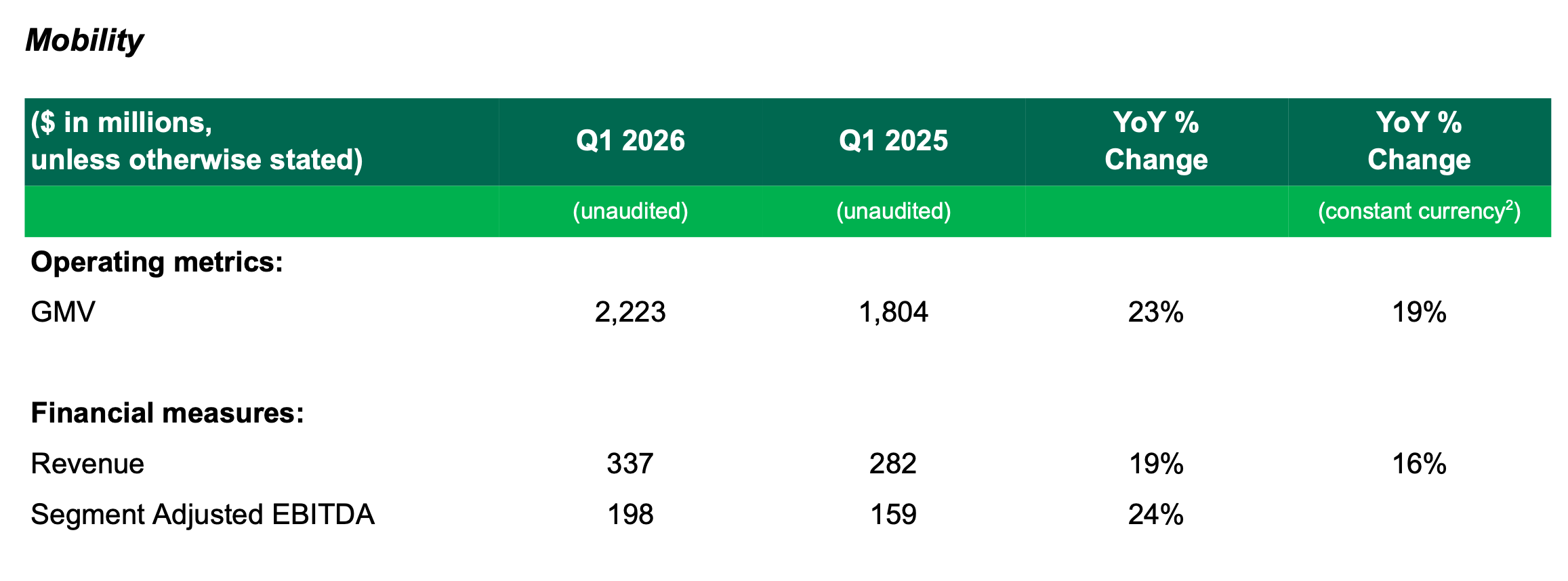

Mobility followed a similar path, with GMV reaching $2.2 billion. Interestingly, transactions grew faster than GMV at 28%, indicating that the service is becoming more accessible and high–frequency rather than just more expensive.

They are maintaining a steady 8.9% Adjusted EBITDA margin here, even while navigating the sharp regional fuel crisis that could have easily derailed a less efficient operator.

On the autonomous vehicle side of things, Grab is clocking 40,000 autonomous kilometers in a controlled Singapore residential estate, learning how to integrate hybrid fleets of human and AI drivers. They want to be the most experienced operator in Southeast Asia, ready to plug in any AV software player when the technology and the regulators are finally ready. However, as noted on the earnings call,

“… the adoption of AVs in Southeast Asia remains nascent. We see governments and regulators taking a measured approach in implementing AVs, which we believe is the right approach for our region. We will continue to incorporate AVs in our platform at a pace that reflects the trust communities place in us and our emphasis on customer safety. To be clear, we do not expect anyone to be able to deploy impactful disruption to our human driver network in the near future.“

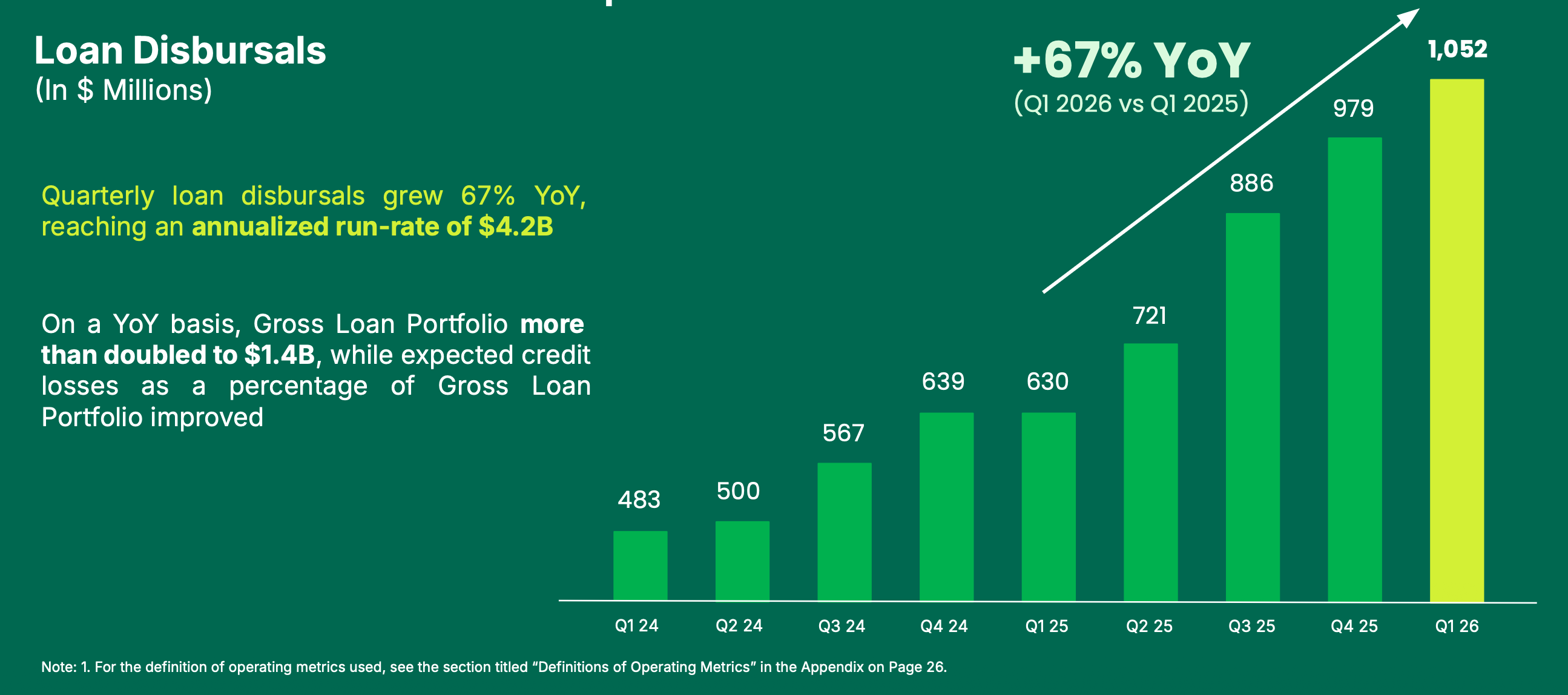

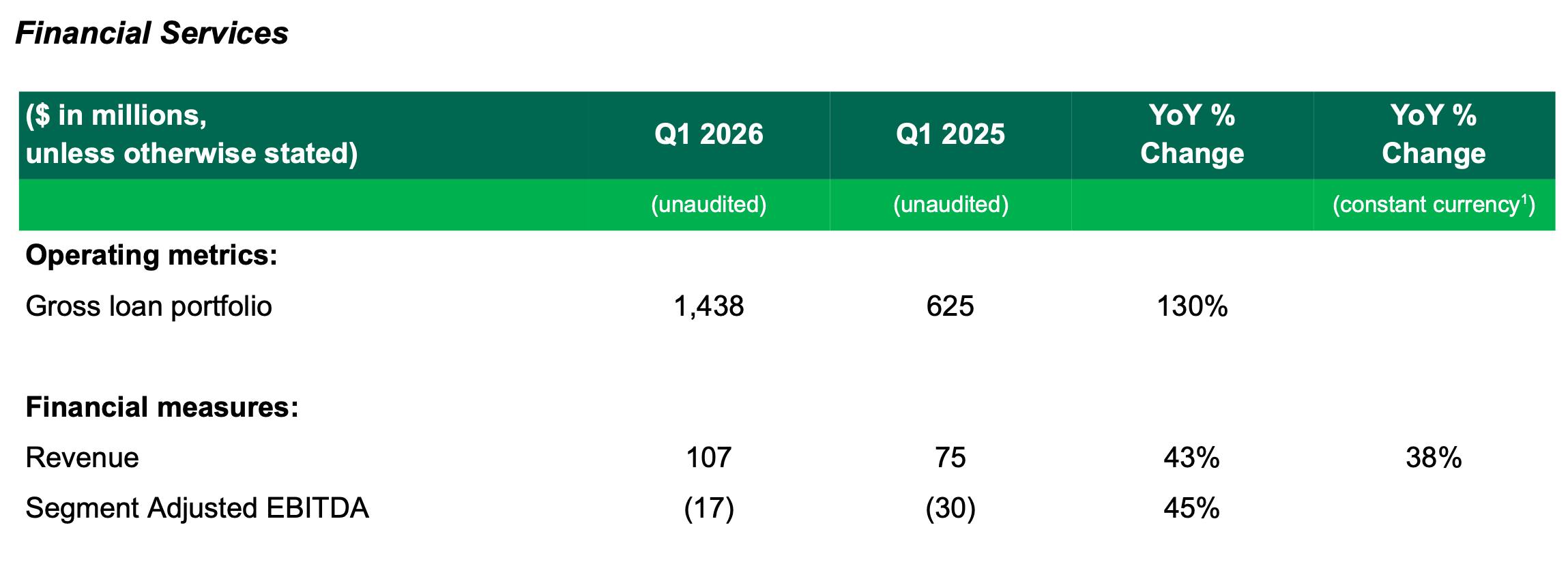

If there was a “shock” this quarter beyond the Indonesian regulation, it was the explosive growth of Financial Services. The $1 billion milestone in quarterly loan disbursals is hard to ignore.

That is a 67% year-on-year increase.

More importantly, the Gross Loan Portfolio has swelled to $1.4 billion – even though QoQ growth was more modest – while credit discipline and credit quality actually improved. They are lending into their own ecosystem – to drivers and merchants, and consumers (app users), all of which they already know – which creates a massive information advantage for their underwriting AI.

According to Grab’s management team, “more than 1/3 of that incremental revenue dropped straight to the bottom line for Financial Services, demonstrating that operating leverage that we've been speaking about.“

So this segment is on a clear trajectory to break even in the second half of 2026.

“We also reiterate our expectations to exit 2026 with a Gross Loan Portfolio of over $2 billion and achieve Segment Adjusted EBITDA breakeven in the second half of 2026 for the overall Financial Services segment.“ - Earnings Call

It is becoming a legitimate third pillar for the group, not just a loss–leading side project.

Furthermore, management is increasingly talking about the “Grab Intelligence Layer” as their ultimate competitive moat – 20 billion transactions of historical data built over 14 years are hard to replicate.

“We capture highly localized real-time data on how over 50 million users and partners interact across 8 markets […] We feed these multimodal signals, from hyperlocal mapping to in-store payment terminals, into our AI Intelligence Layer to optimize our marketplace efficiency, from dynamic pricing to last-mile routing. Crucially, we paired this data advantage with our massive through physical fulfillment network. That closed loop system or ecosystem is our biggest competitive moat, which is why our AI investments translate directly into measurable financial outcomes.“ - Earnings Call

For instance, consider the “Turbo” mode for drivers. Those who opted into this AI–powered optimization saw a 23% uplift in earnings per hour. It is a simple equation: more efficient routing means more jobs per hour, which protects driver livelihoods even when fuel prices are at record highs (here Grab tried to cushion the impact by deploying targeted fuel rebates and proactively engaging with regulators across their markets).

“This has contributed to Mobility transactions growth outpacing Mobility GMV growth, with transactions up 28% YoY.“

On the fuel crisis subject, to provide some more context, management also said the following on the call:

“In the medium term, we are committed to accelerate the EV transition to reduce our driver partners exposure to fuel price volatility. So for example, in Thailand and Philippines, we have a drive-to-own program that connects our drivers with OEMs like BYD and GAC, where we have deals of up to 70,000 vehicles available across 6 markets with accessing to financing so they can own those more easily.

In Vietnam, we have secured preferential charging rates also through our charging network partners, EBOOST and Charge+, which helps our drivers in the transition also. And finally, in Thailand, I am pleased to say that our total fleet supply has crossed 30,000 EVs on the platform and demand for those from consumers is also strong, where they can select that EV option, and that demand has grown by over 35% year-on-year. So this fuel crisis has become an opportunity in the sense that it helps us to accelerate that EV transition.“

For merchants, the AI Assistant is driving a 15% GMV uplift for those who engage with it.

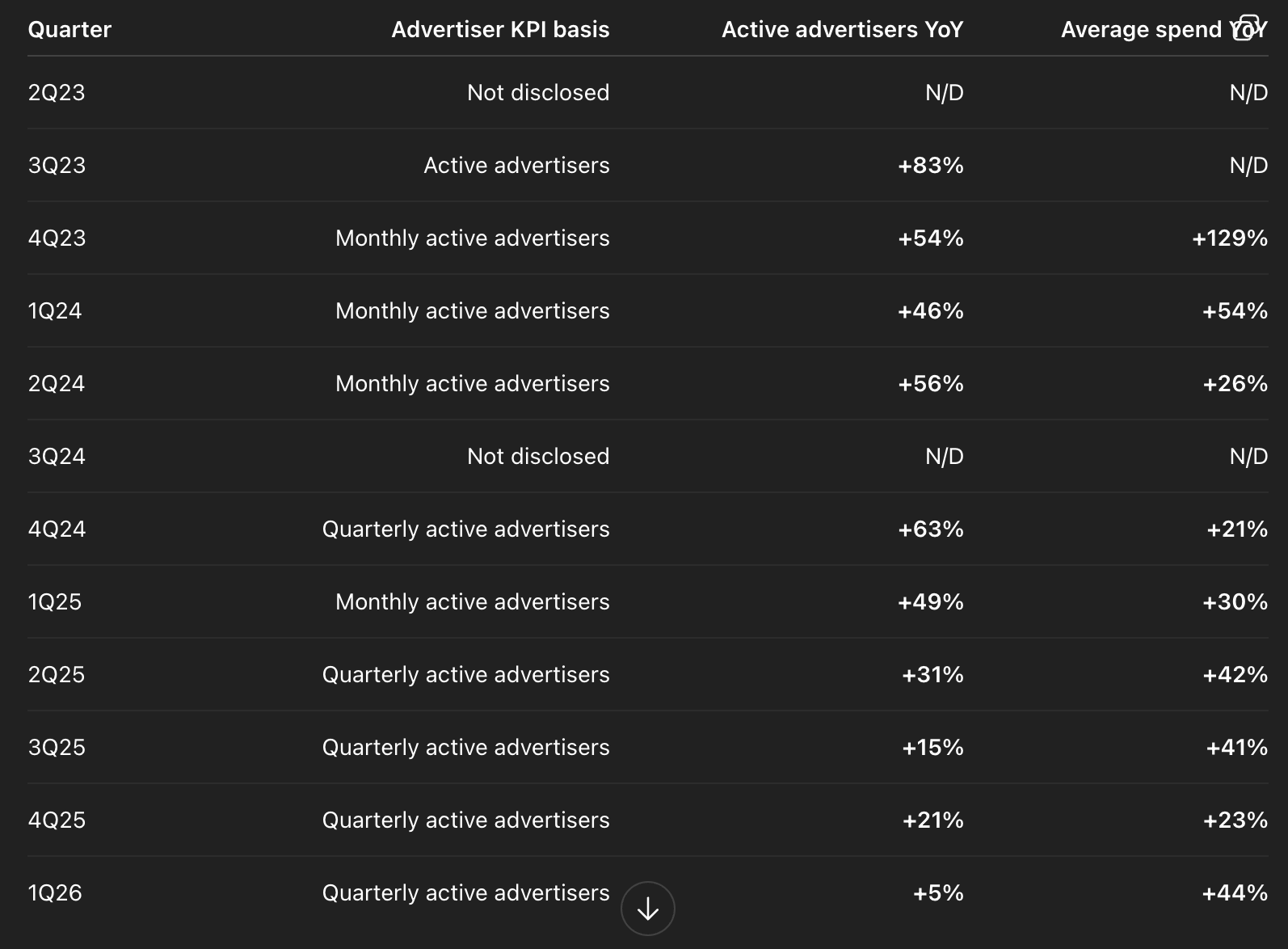

The high-margin ad business is also developing favorably: average advertiser spend grew 44% YoY as merchants see increasing measurable returns. However, as @the_zack_zhu shared on X (see overview below), the number of active advertisers only grew 5%, and it remains to be seen whether Grab has already hit a structural ceiling or whether this is just a temporary slowdown (I’m leaning towards the latter).

Overall, Grab is “winning” because they are out-serving the competition by making the platform more profitable for the people who actually do the work.

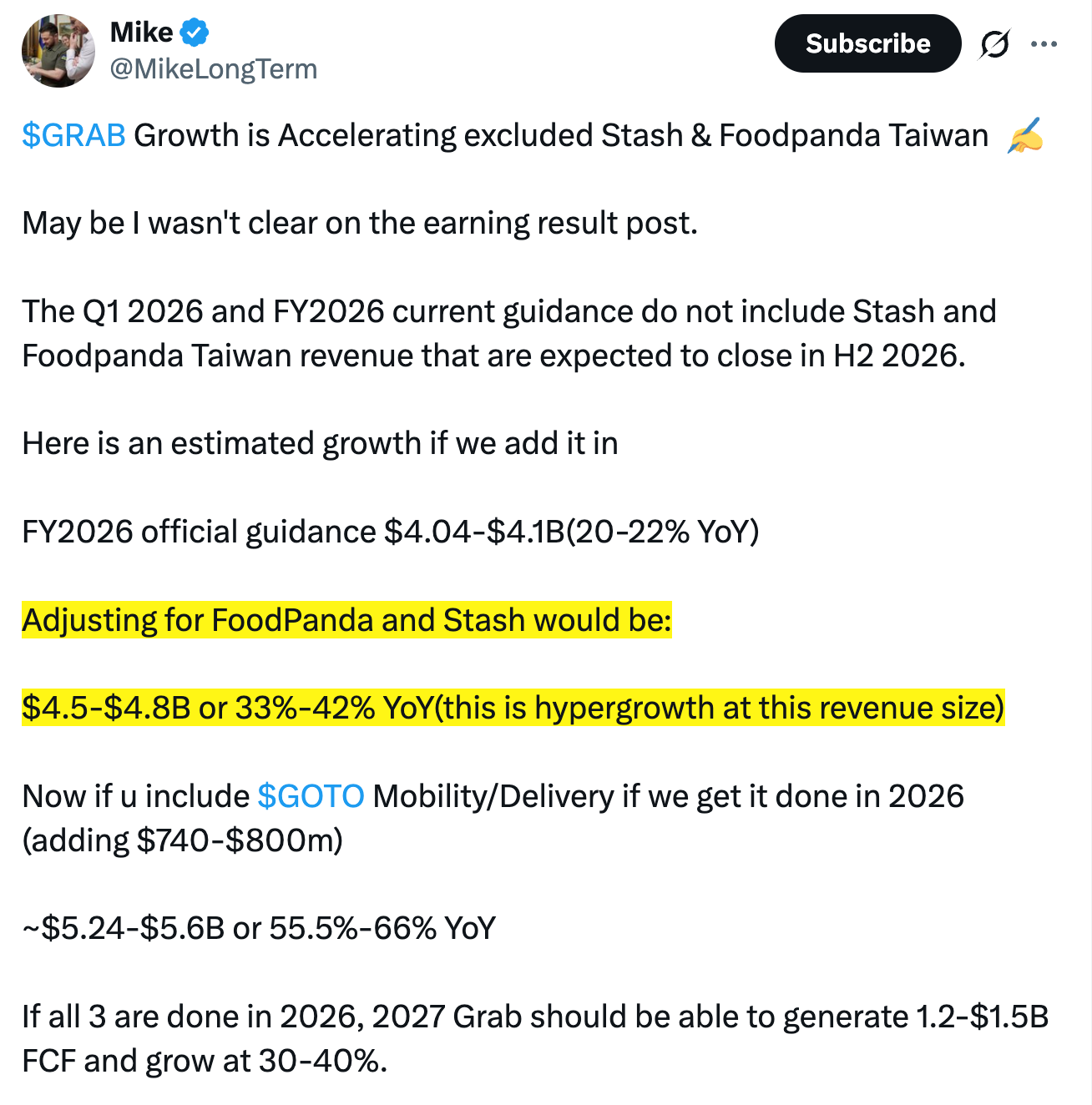

The strategic horizon is also expanding. The acquisition of foodpanda’s business in Taiwan is a bold move into a high–ARPU market outside their traditional Southeast Asian stronghold. And importantly, the Q1 figures and the outlook do not include revenue from both the Stash and Foodpanda Taiwan acquisitions.

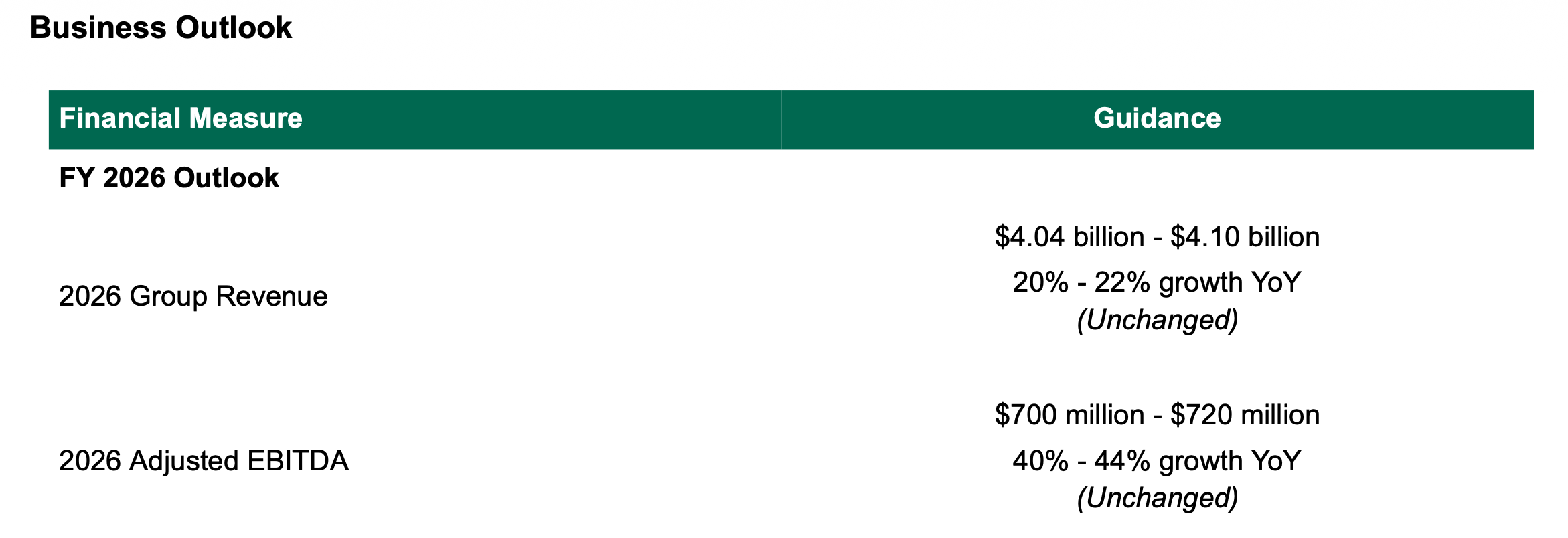

The outlook remains remarkably steady despite the near-term noise. Grab reiterated its full–year 2026 guidance, targeting revenue up to $4.10 billion and Adjusted EBITDA as high as $720 million.

As readers of my initial deep dive know, they are also putting their money where their mouth is with a $500 million share repurchase agreement.

“In March 2026, we entered into an accelerated share repurchase agreement and a contingent forward purchase agreement to repurchase $250 million and up to $150 million, respectively, worth of Class A ordinary shares, as part of our previously announced $500 million share repurchase programme approved by the Board of Directors in February 2026.“

At the same time, it’s important to note that nonetheless, the basic and diluted shares have increased both year-over-year and quarter-on-quarter.

However, management added some more nuance on this subject during the call:

“So a total of $400 million has been accelerated, which means only in the market for 5 to 5 trading days in Q1 itself. So you can’t look at it in isolation. Now both these programs are expected to be executed over the next 4 months. So I’ll share a lot more in the next quarterly earnings when we look at the Q2 results. Now in terms of share count, it would have amount to roughly around 2% of our total share count, which will more than offset for the dilution from stock-based compensation. So that’s how we’re viewing it. As a reminder, there’s still another $100 million left to go in the share buyback program, and we’ll continue to have discussions around capital allocations with our Board.“

The Indonesia Shock: Regulatory Caps and Its Implications – Is the Grab Thesis Now Broken?

Indonesia, one of Grab’s largest and most important markets, just threw a curveball at investors. In early May, the government introduced price caps on ride-hailing fares through Presidential Decree No. 27/2026, aiming to protect drivers and curb rising ride costs for consumers.

On the earnings call, management clarified that the regulations will specifically target the “ojol” (short for ojek online) motorcycle sector.