Deep Dive: Grab Holdings Ltd ($GRAB) – Part 2

The Super-App Flywheel: A Multi-Layered Moat!

We continue our deep dive into Grab Holdings. In this second part, we will explicitly focus on Grab’s “moat stack” and assess the width and depth of Grab’s competitive advantages.

Before we dive in, let me share the 2026 product day, Grab X, below, which introduced a couple of very fascinating products and features, including …

GrabMaps for Consumers: Enhanced maps featuring indoor mall navigation, real-time parking, EV charger locations, and AI voice cloning for navigation.

Grab More: Enables users to order from two different nearby merchants in a single delivery order without extra fees.

Grab Shopping Agent: Allows users to build checkout carts across multiple merchants using photos, voice notes, or text.

Cash Loan: In-app AI-powered lending for all Grab users with instant approval and customized repayment for users with limited credit history.

Discover by Grab: An AI-curated feed for local dining recommendations and community-driven content.

Group Ride: Allows up to four passengers to share a single vehicle with multiple pickups/drop-offs and split fares (up to 40% cheaper).

Personalised Travel Experience: A centralized travel portal with airport guides, check-in reminders, and baggage belt navigation.

GrabStays: An in-app hotel booking service offering same-day rates and GrabCoin rewards.

GrabPay for Travel: Seamless cross-border QR payments using existing saved cards without needing local wallet top-ups.

Driver AI Assistant: A hands-free voice chatbot to assist drivers with navigation, messaging, and policy queries.

Tap to Pay: Converts any smartphone into a contactless payment terminal via the GrabMerchant app.

Carri: A prototype AI robot designed to assist delivery partners by navigating “the last mile” inside malls and office towers.

And this is just my personal selection of highlights. There’s more.

Disclaimer: I own Grab shares. The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

Part 2 – Business Quality

Competitive Advantages Analysis

Grab’s competitive advantages are built on a multi-layered moat that combines digital network effects, physical infrastructure, and regulatory barriers. These advantages make it difficult for competitors to replicate Grab’s success in Southeast Asia.

Brand Moat: Trusted and Embedded in Daily Life

Grab’s brand is one of its most powerful advantages. It has become a household name and trusted brand in Southeast Asia, so much so that in some countries, “Grab” is used as a verb for hailing rides or ordering food. Its strength lies in being the category leader across multiple sectors, from mobility to deliveries to e-wallets. This brand dominance is not about prestige (the type of brand moat companies like Hermés, Ferari, or LVMH lean into) – it’s about trust and reducing search costs.

Grab has positioned itself as a utility-based brand, essential for everyday tasks like commuting and eating.

The company’s brand is also highly habit-driven. For millions, Grab is deeply integrated into the daily rhythm of middle-class life, making it a go-to solution for transportation and food delivery. Customers associate Grab with quality, reliability, safety, and convenience, which, as mentioned, reduces search costs – customers don’t need to look elsewhere for alternative services; it becomes habitual.

Over time, this deep brand loyalty is expected to endure for decades as Grab continues to evolve from a startup into a key part of regional digital infrastructure.

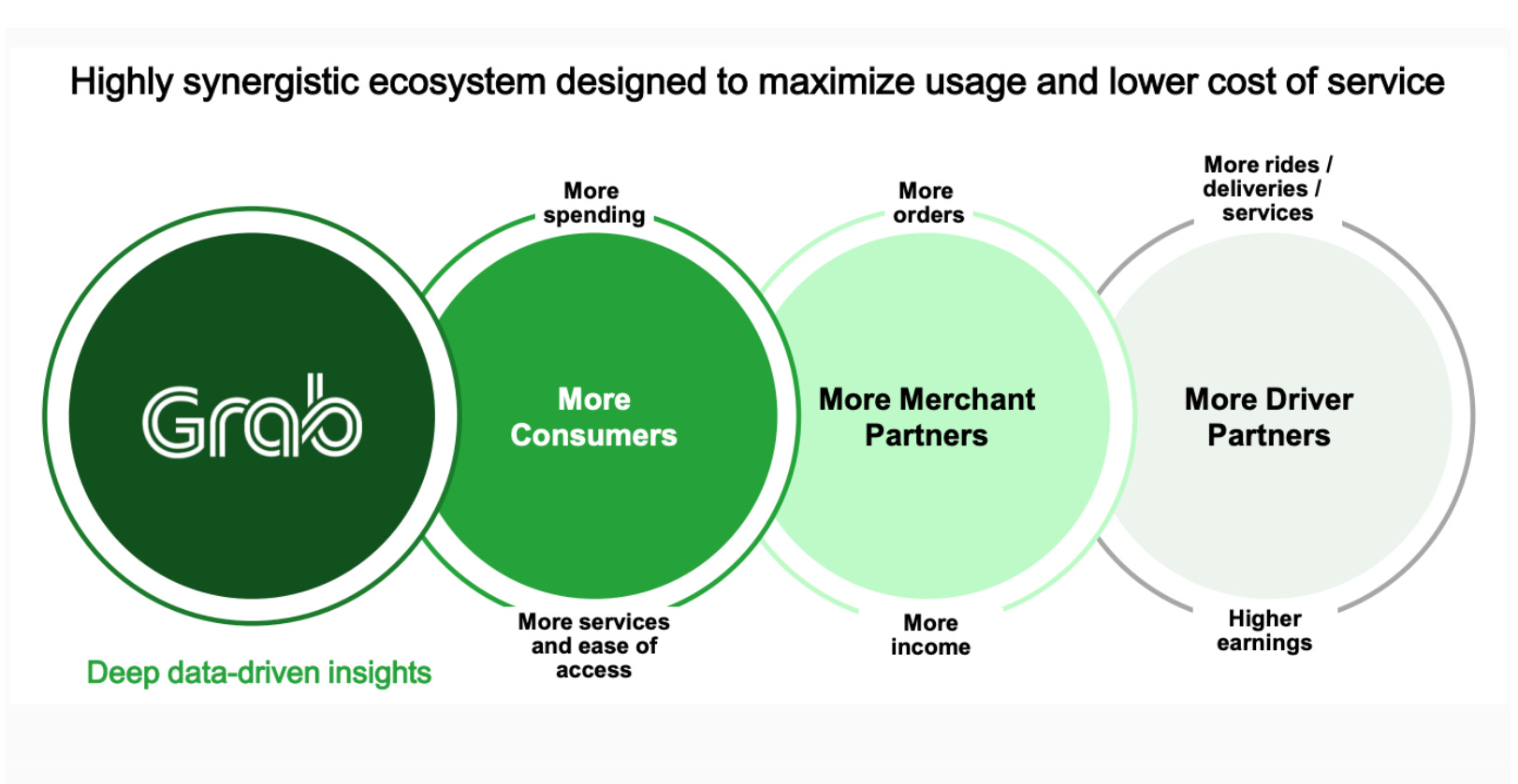

Network Effects: The Grab Ecosystem Flywheel

Arguably, the most powerful competitive advantage Grab possesses is its network effects. As the company expands, its platform becomes increasingly valuable. This is known as the “Grab ecosystem flywheel”.

Here’s how it works: as more drivers join, wait times drop, attracting more consumers. As more merchants join, a wider selection of products and services becomes available. And the more consumers there are, the more orders are placed, which attracts even more drivers and merchants. This virtuous cycle makes the platform increasingly difficult for competitors to disrupt.

The power of Grab’s network is also fueled by data loops. With billions of transactions occurring on the platform, Grab is able to continuously improve its services through AI, driving better routing for drivers and more efficient credit scoring for financial services.

What’s more, because Grab serves daily needs – transportation, food delivery, payments – the frequency of interaction strengthens the network far more than platforms offering less frequent services. There are 50 million MTUs. As of early 2025, Grab recorded 7.8 million DTUs. These daily users represented approximately 16% to 17% of the total Monthly Transacting User (MTU) base at that time. Customers who utilize both GrabFood and GrabMart (groceries) have order frequencies 1.8x higher than those who only use food delivery. And members of the GrabUnlimited paid loyalty program interact far more often, showing 3x to 4x higher order frequency in the food segment compared to non-subscribers

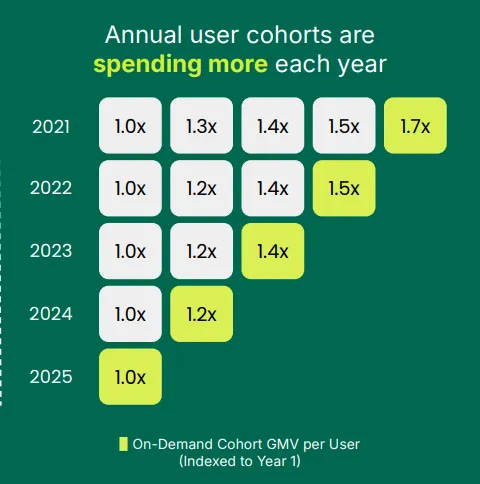

So it seems like once onboarded, users remain on the platform, and over time, increase their purchase frequency and spend more, continuing to contribute to the growth of the flywheel.

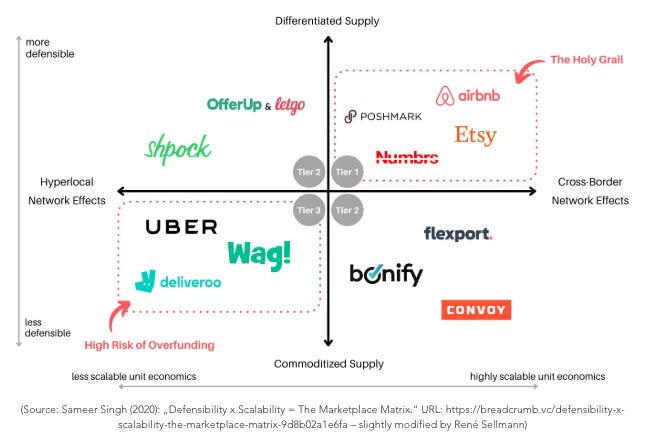

The Hyperlocal Nature of the Network

When studying Grab, most investors probably see a regional giant spanning eight (soon nine) countries, but the reality is much more granular. A driver in Bangkok provides zero utility to a commuter in Ho Chi Minh City. This places Grab firmly in the hyperlocal quadrant of the marketplace matrix I always come back to when studying network effect marketplaces and platforms.

Every time Grab enters a new city or even a new neighborhood, they essentially have to restart the flywheel from scratch. They must spend heavily on driver incentives and passenger promos just to reach that critical mass where the wait time drops enough to make the service viable. It can be a grueling, capital–intensive process – especially early on – and it was for Grab, battling for market share with behemoth Uber and local peers. You can see this reflected in their historical burn rates.

Unlike a global network like Airbnb where one listing can attract a traveler from anywhere on Earth, Grab is forced to win thousands of tiny, isolated battles against regional competitors. The network effects don’t cross borders easily. Success in Singapore does not guarantee a win in Jakarta. It never has.

If the geographic limitations weren’t enough of a hurdle, we have to talk about the supply side of the equation. In the ride–hailing and food delivery segments, Grab deals almost exclusively in commoditized supply. A car is a car. A delivery rider is a delivery rider. From your perspective as a user, you likely don’t care who is behind the wheel as long as they arrive in five minutes and don’t overcharge you. This lack of differentiation is a nightmare for defensibility. It leads to the “multi–tenanting” problem where consumers may use multiple apps, opting for the best offer available at any given point in time – price comparison. This may create a permanent ceiling on margins.

The real question for any Grab shareholder is whether the “super–app” strategy can actually move the company up the matrix into a more defensible tier. Grab isn’t just trying to be a taxi service. They want to be your digital wallet, your insurer, and your bank. Your everything app. This is an attempt to create a differentiated supply combined with a strong lock-in effect (as to be discussed below). Financial services and loyalty programs like GrabRewards are designed to create this exact “lock–in” that transcends the commoditized nature of a car ride. If you have all your wealth and points stored in one ecosystem, you are far less likely to switch to a competitor for a fifty–cent discount on a laksa delivery. It’s similar to ordering on Amazon: you may know that there may be a cheaper offer available on another ecommerce website, bit Amazon just works, you know the return policy is incredibly consumer oriented, and that the parcel may be at your doorstep in 24 hours.

By layering multiple services, Grab is attempting to build a “horizontal” network effect where the frequency of ride–hailing feeds the data for credit scoring, which in turn fuels the fintech arm. It is an ambitious goals. I believe the success of this determines whether Grab remains a lower-tier utility or becomes a tier–1 powerhouse. They are trying to build a moat where none naturally exists. It’s a bold bet. The jury is still out.

The full story starts here:

The rest of this post covers the remaining pillars of Grab’s moat stack and the trajectory the business is on. If you’re serious about sharpening your investing edge, the full post (and all my previous premium content, including valuation spreadsheets, deep dives (e.g. well-known mid- and large caps such as LVMH, Duolingo, Meta, Edenred as well as more hidden gems such as Tiger Brokers, Digital Ocean, Ashtead Technologies, InPost, Timee, and MANY more) and powerful investing frameworks. is just a click away. Upgrade your subscription, support my work, and keep learning.

Annual members also get access to my private WhatsApp groups – daily discussions with like-minded investors, analysis feedback, and direct access to me.

PS: Using the app on iOS? Apple doesn’t allow in-app subscriptions without a big fee. To keep things fair and pay a lower subscription price, I recommend just heading to the site in your browser (desktop or mobile) to subscribe.