Deep Dive: Grab Holdings Ltd ($GRAB) – Part 4

Unlocking Grab’s Future: Valuation, TAM Analysis, and Long-Term Opportunities

Welcome back to the latest installment of the Grab Deep Dive Series! In this fourth part, we turn our attention to valuation, focusing on Grab’s historical performance, growth trajectory going forward, and the future potential of its market (a thorough total addressable market analysis). As a company that began as a simple ride-hailing service and has since expanded into an all-encompassing “superapp,” Grab’s journey is anything but ordinary.

In this part, we will:

Explore Grab’s historical growth

Dissect the trends that will fuel Grab’s future growth, which collectively create a fertile ground for Grab’s sustained success.

Provide insights into Grab’s market valuation using different approaches, offering a clearer picture of its true attractiveness at the current share price.

What really sets Grab apart is its strategic vision for the future. The company isn’t just looking at incremental growth; it’s investing in next-gen innovations like autonomous vehicles and AI-driven solutions, making bold moves that signal Grab’s ambition to become the backbone of Southeast Asia’s digital economy. As you’ll see, the runway for growth is vast – and Grab is showing signs of a “spawner DNA” – making this valuation assessment not only relevant but a pivotal guide for anyone looking to understand Grab’s position in the evolving tech landscape.

Part 4 – Valuation

4.1. Past Growth

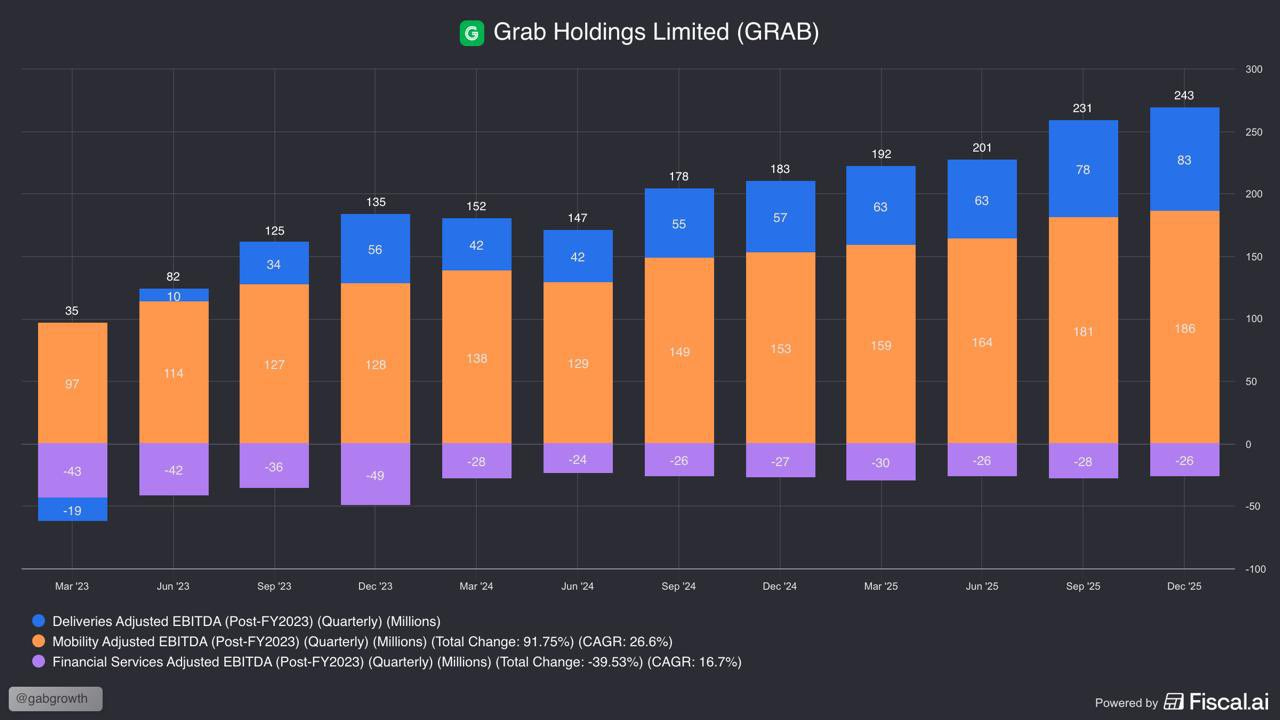

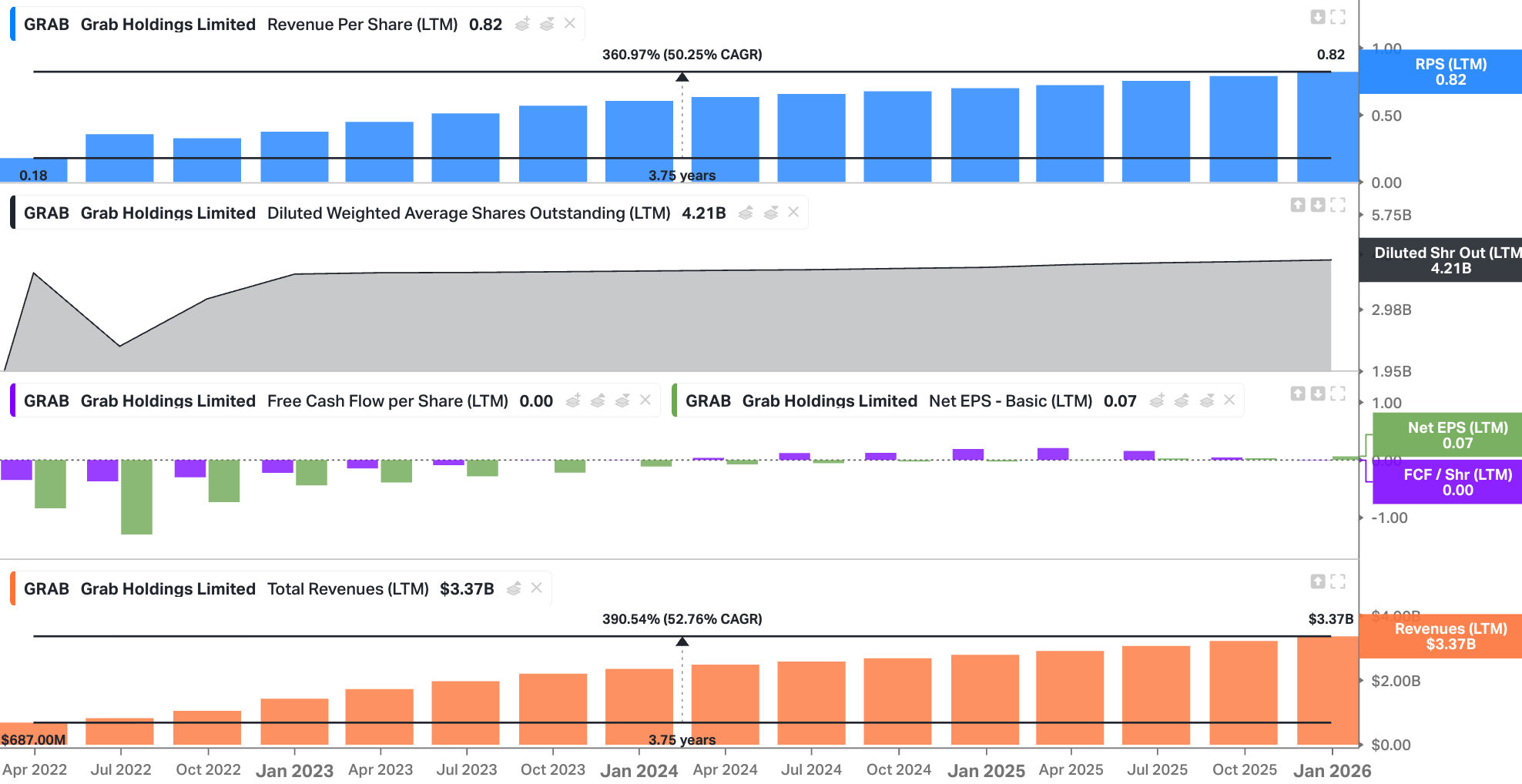

Grab has managed to scale its revenue significantly in recent years. As discussed in the previous parts, from its humble beginnings as a ride-hailing service, the company evolved into a multi-service “Superapp” offering mobility, delivery services, and financial services. The historical data indicates strong revenue growth fueled by increasing demand across these segments.

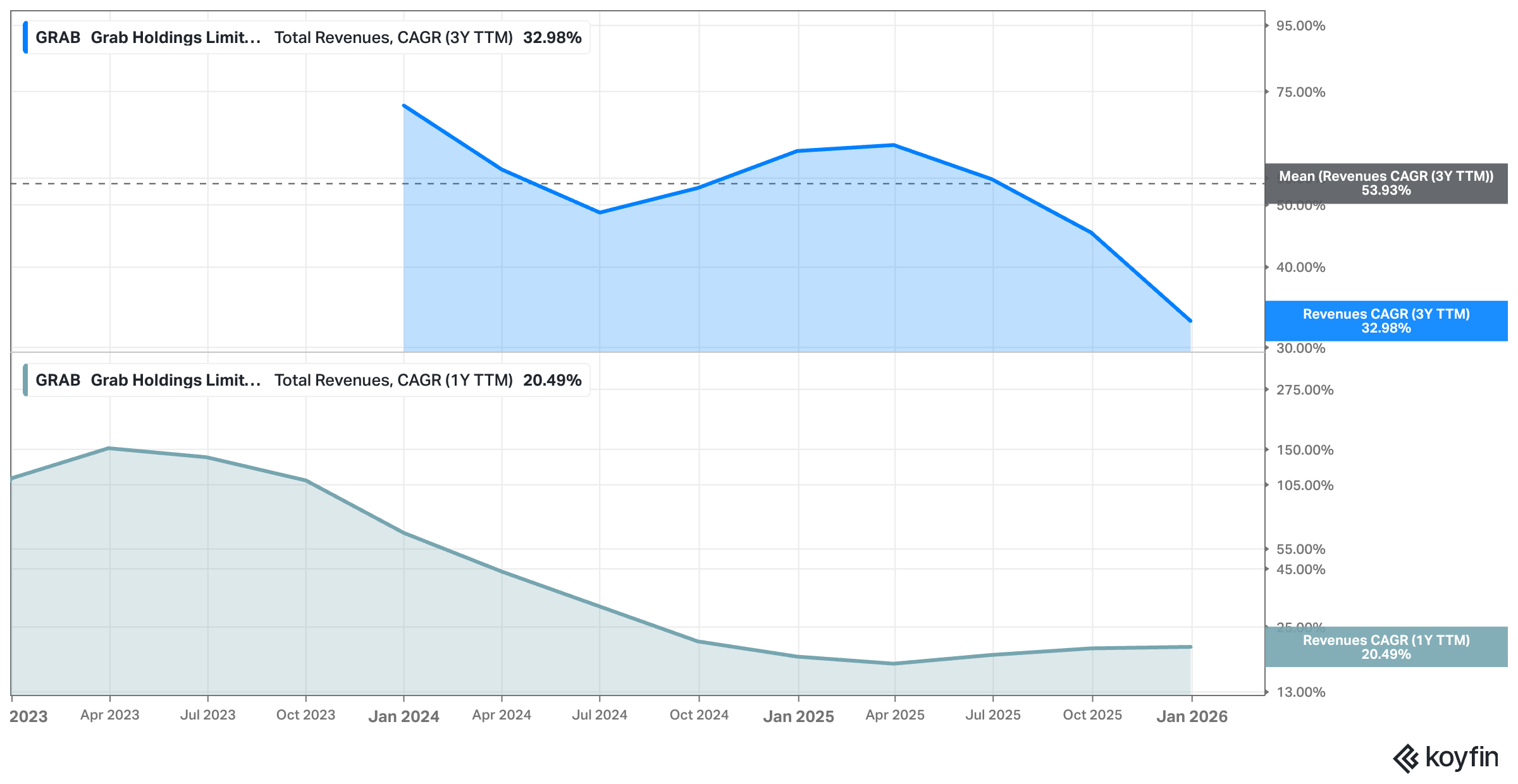

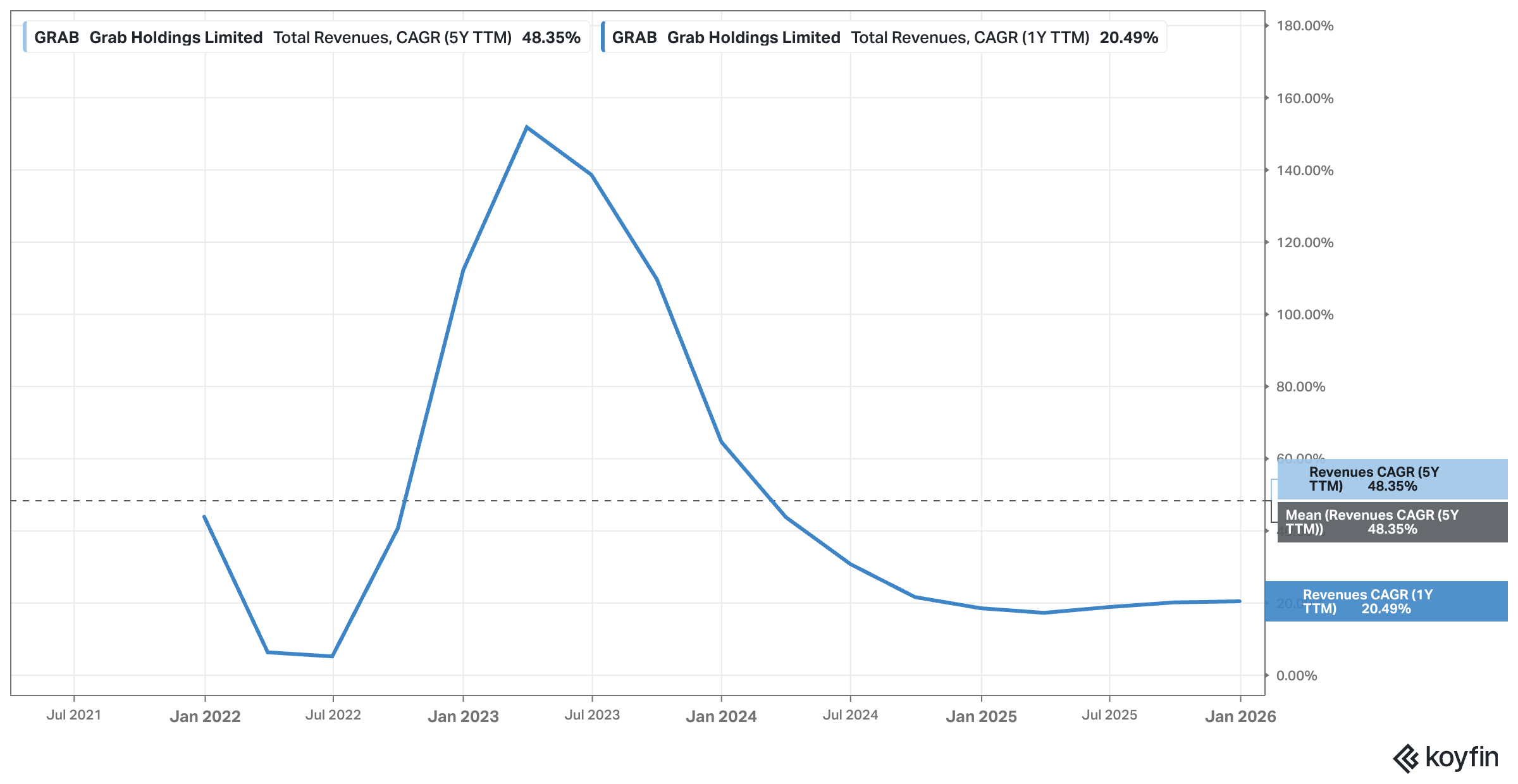

Looking at the revenue CAGRs, it’s clear that Grab achieved substantial revenue growth in recent years, with a 3.75-year revenue/share CAGR exceeding >50%.

More recently, topline growth rates have naturally slowed – as Grab matures – to more sustainable levels, but if Grab can continue compounding in the mid- to high-teens, investors are looking at an interesting setup at current price levels (to be discussed further below).

As suggested, I don’t think the slowing growth rates should be of concern – especially as Grab’s management team has deliberately moved into a phase more focused on profitability and self-funded growth, where growth is naturally more measured, but as I said, more sustainable, compared to a high-flying growth-at-all-costs model.

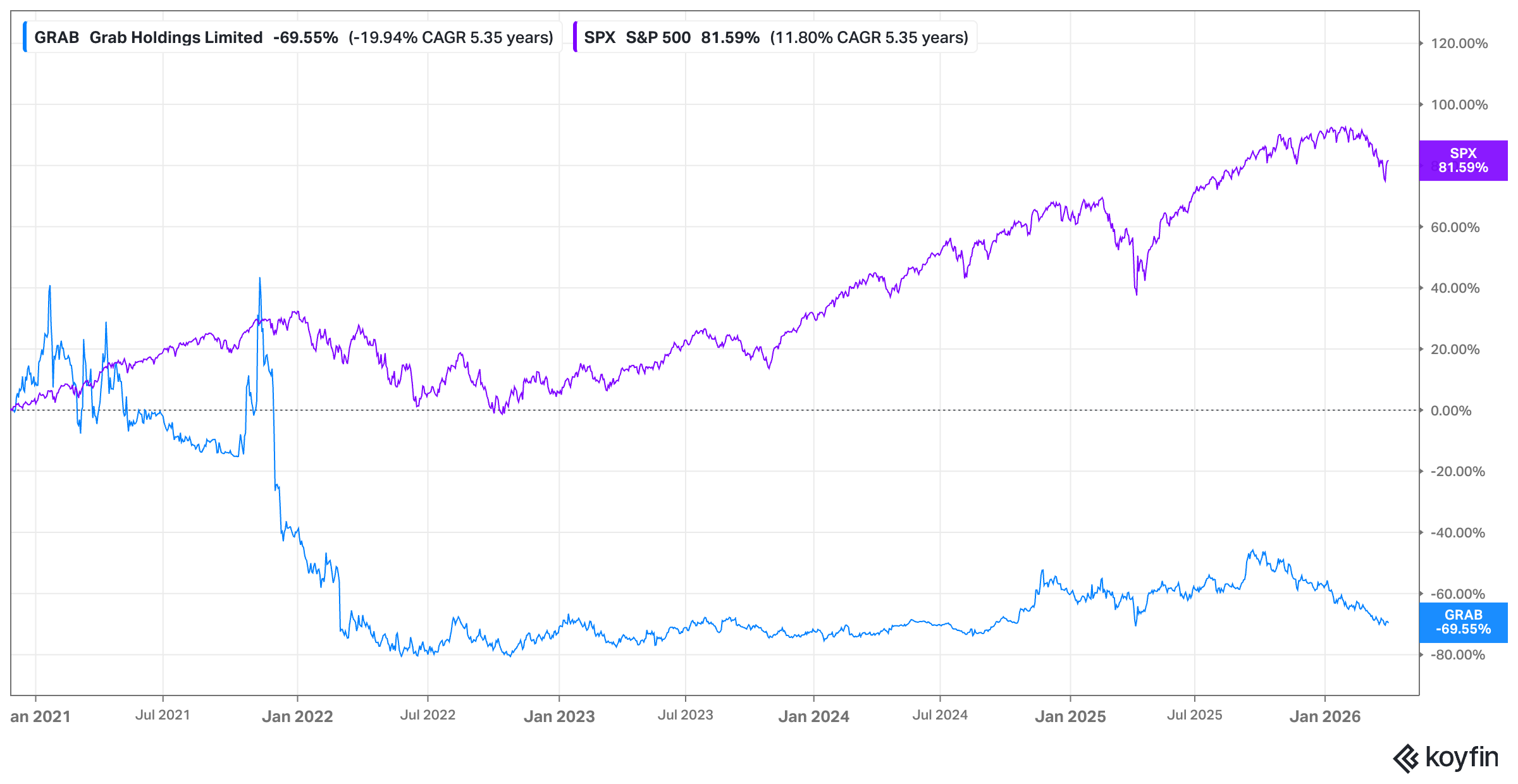

When comparing Grab’s performance against the S&P 500 over the past few years, Grab has underperformed significantly. Since its public listing in 2021, the stock has seen a sharp decline, down about 69.55% as of 2026. Over the past 5 years, Grab’s stock performance translates into a CAGR of -19.94%.

This stark contrast to the S&P 500, which has increased by 81.59% over the same period, highlights how poorly Grab’s stock has performed relative to the broader market, which can largely be attributed to the timing of the IPO (during the Covid and SPAC craze) – as a reminder Grab went public on the Nasdaq on December 2, 2021, via a SPAC merger with Altimeter Growth Corp at a valuation of nearly $40 billion… I’d argue Grab’s case study serves as a stark reminder that IPO actually stands for “it’s probably overpriced” – you can’t really blame management for the listing price (quite the opposite as they did a good job timing the IPO as the IPO raised gross proceeds of $4.5 billion in the largest-ever U.S. public market debut by a Southeast Asian company).

Disclaimer:

I own Grab shares. The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

4.2. Future Growth

Total Addressable Market Analysis

To understand the future growth potential of Grab, we need to first examine its Total Addressable Market (TAM).

“Scale wins. And large TAMs increase the opportunities for companies to tap into these scale benefits.” – Mark Mahaney

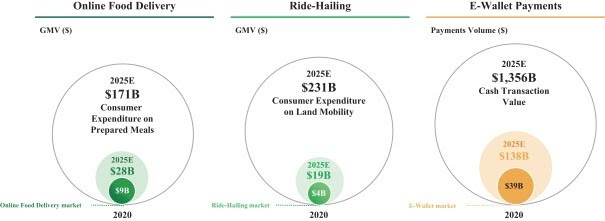

Grab is operating in rapidly expanding sectors, including online food delivery, ride-hailing, and digital banking, which collectively form a massive opportunity. Before its IPO, management estimated in the F1 filing that its core TAM – encompassing these services – will exceed $180 billion by 2025.

“There is a tremendous amount of headroom to grow, and Euromonitor estimates our addressable market to be over $180 billion by 2025, consisting of online food delivery, ride-hailing, and e-wallet markets. We are able to address these different market opportunities through our superapp and our Grab ecosystem.“ - F-1

This already represents a significant market, but if we broaden our scope, the numbers become even more impressive. The overall personal consumption expenditure (GMV) for land mobility back then was projected to reach $231.3 billion by 2025, while expenditure on prepared meals is expected to hit $170.5 billion (again GMV).

“Our Addressable Market and Growth Potential: We started out by providing a platform addressing the mobility opportunity in Southeast Asia, with the ride-hailing market estimated to be at $4.5 billion in 2020 according to Euromonitor. We have since expanded our platform to address food and other deliveries and e-wallet opportunities, estimated at $9.4 billion and $38.9 billion in 2020, for the online food delivery and e-wallet markets respectively.

According to Euromonitor, total personal consumption expenditure for prepared meals and land mobility, which includes operation of personal transport equipment, personal consumption expenditure on buses, coaches and taxis, are expected to reach $170.5 billion and $231.3 billion, respectively, by 2025. Cash payments transaction values are expected by Euromonitor to reach $1,356.1 billion by 2025. We expect that digital penetration rates will increase over time as digital alternatives become more popular.“ - F-1

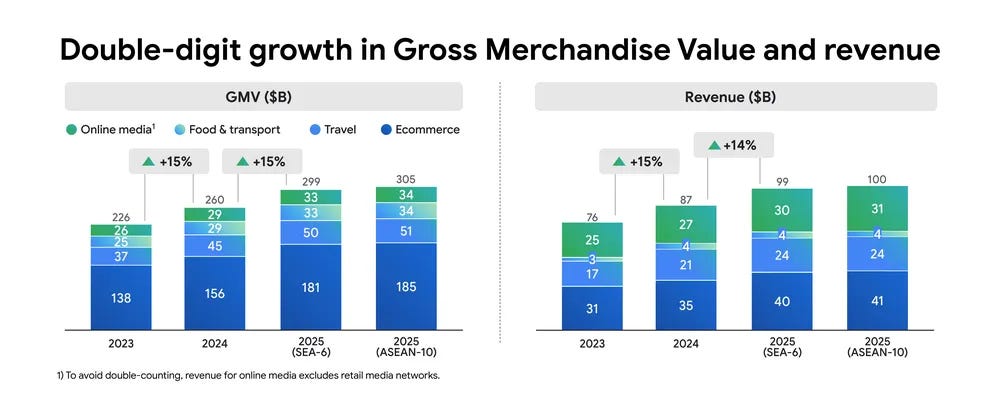

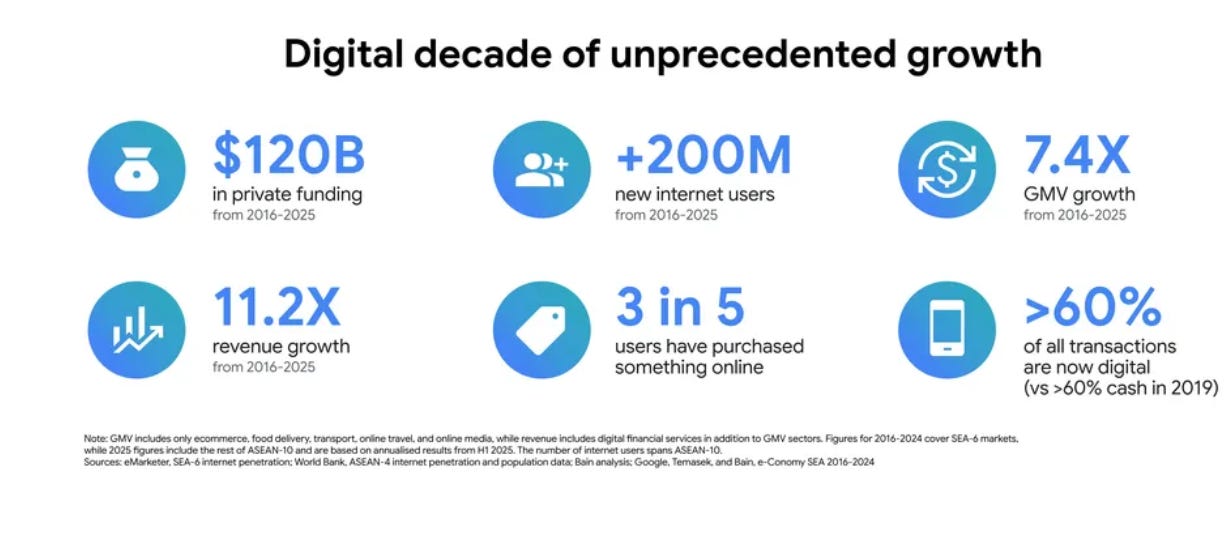

Let me stress that those were the historical, pre-IPO projections. According to the e-Conomy SEA 2025 report by Google, Temasek, and Bain & Company, the region’s total digital economy Gross Merchandise Value (GMV) surpassed $300 billion in 2025.

This expansion was driven by a decisive shift toward deep digital participation, with over 60% of all transactions in the region now occurring digitally.

Here is a breakdown of what drove that expansion and the characteristics of it:

Video Commerce: One of the biggest drivers has been the rise of “shoppertainment.” Video commerce (buying through live streams and social video apps) now accounts for roughly 25% of the region’s total e-commerce Gross Merchandise Value (GMV).

Infrastructure & QR Codes: The expansion was largely fueled by national unified QR systems (like QRIS in Indonesia or PromptPay in Thailand) and cross-border QR interoperability between ASEAN nations.

Depth of Adoption: It’s not just about more users; it’s about deeper usage. Roughly three out of five Southeast Asians now shop online, and the focus has shifted from acquiring new users to increasing the frequency and value of transactions from existing ones.

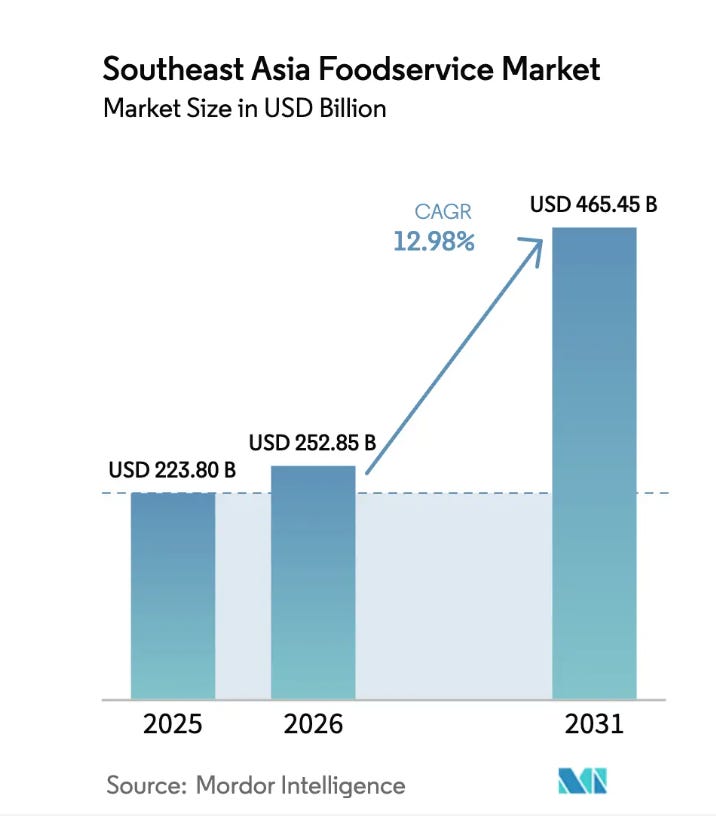

Similarly, within Grab’s core segments, the 2026 Mordor Intelligence Foodservice Market Analysis estimated the total Southeast Asian foodservice market reached $223.8 billion in 2025, well ahead of the $170.5 billion initially expected. The Analysis is projecting a market growth CAGR of 13% throughout 2031.

In the slide deck below, which Grab shared recently after the foodpanda acquisition, Grab itself estimates the current size of the foodservice serviceable market in SEA to be $200 billion+.

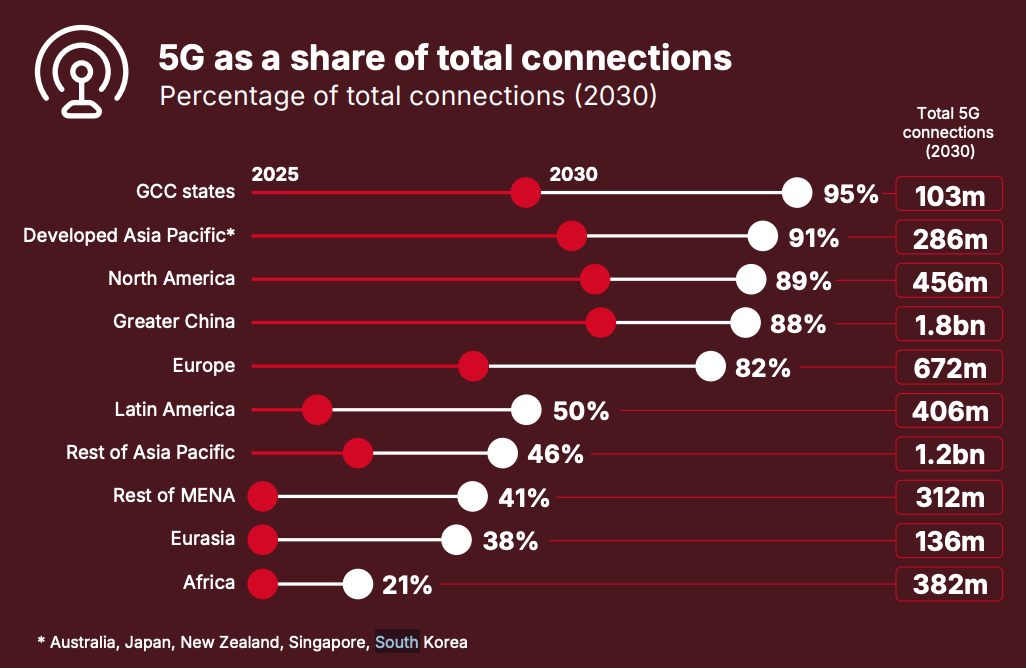

Looking ahead, the addressable opportunity is shifting from a “digital decade” of user acquisition to a $1 trillion “intelligent economy.” Analysts from HSBC’s Digital Frontiers 2030 and the e-Conomy SEA 2025 report now project the ASEAN digital economy GMV could reach $1 trillion by 2030, fueled by the integration of AI-driven logistics and the maturation of digital financial services.

“By 2030, Southeast Asia’s digital economy will reach $1 trillion, with the potential to hit $2 trillion as ASEAN implements its Digital Economy Framework Agreement. Growing at double the global rate, GDP in Southeast Asia hit $4.25 trillion in 2025, making it the world’s fourth-largest economy after the US, China, and Germany. With a young, digitally engaged population and pro-innovation policies, Southeast Asia is quickly becoming a global economic powerhouse, leaving its former identity as a modest, developing region decidedly in the past.“ - HSBC

Grab is well-positioned for this next phase. As you should know by now, the company announced its first full year of net profit recently and record Monthly Transacting Users (MTUs) today exceed 50 million.

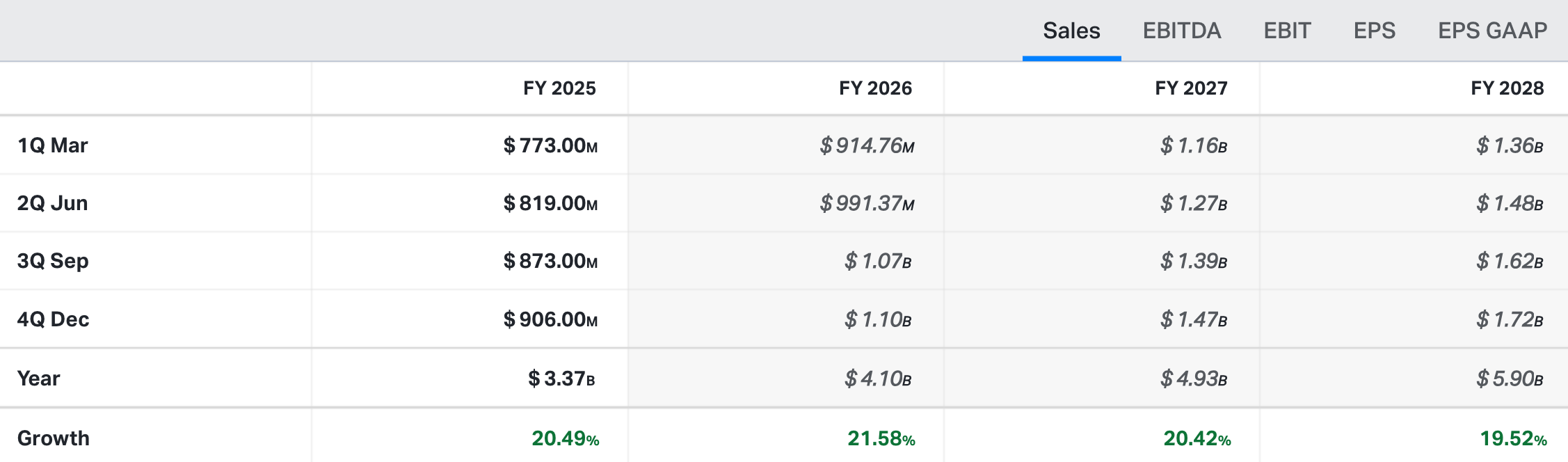

Moving into 2026, S&P Global Ratings and internal guidance forecast continued momentum, with Grab’s total revenue expected to grow by approximately 20% to $4.1 billion in 2026, supported by a projected 15.8% CAGR in the broader Asia-Pacific fintech market through 2031.

Koyfin’s consensus estimates (consensus earnings estimates compile individual projections from various analysts into an averaged figure) project similar topline growth rates for the next three years.

Looking Ahead!

Over the years, Grab has consistently expanded its TAM, demonstrating its ability to adapt and evolve. What started as a taxi-booking app in 2012 has transformed into a multi-modal platform, adding food delivery and, more recently, digital banking. The company has expanded geographically, with the acquisition of Foodpanda Taiwan marking its first major step out of Southeast Asia. Similarly, its acquisition of Stash signals Grab’s entry into the digital investing space, which could tap into the $5 billion+ AUM market.

The key takeaway here so far shouldn’t really be an exact number of the TAM’s size – most TAM estimates turn out to be wildly off and while I’m referencing some numbers to provide context, there’s really no way to have an informed opinion on the accuracy of any of them – but rather that the runway is significant. But just using common sense suggests that Grab, and the entire SEA region, are early in their respective growth stories.

Grab, for instance, stands to benefit from several secular tailwinds in Southeast Asia that will continue to fuel the expansion of its TAM. These trends include:

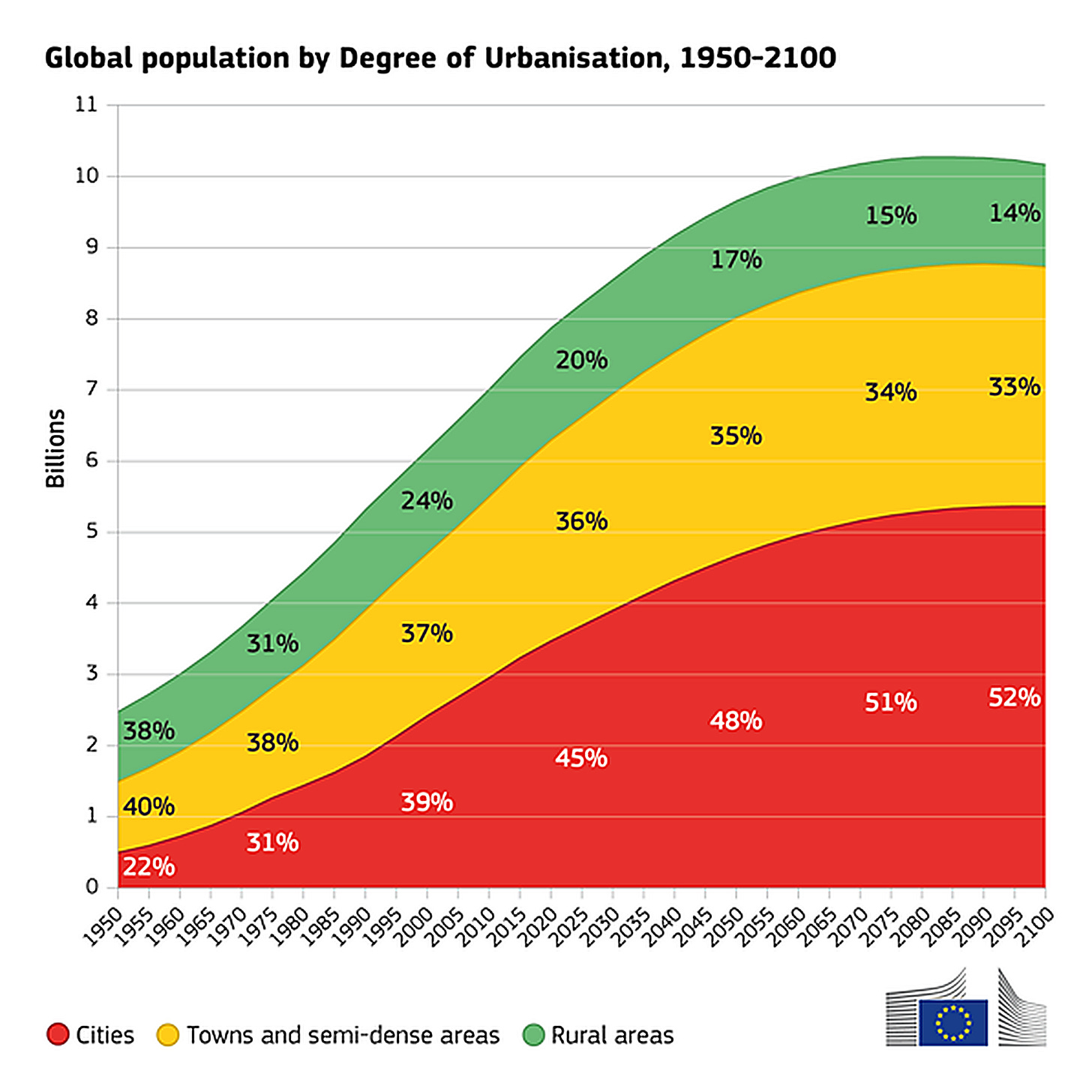

Accelerated Urbanization: According to the United Nations’ World Urbanization Prospects 2025, the majority of the world’s population now resides in urban areas, with Southeast Asia remaining a primary engine of this growth. Jakarta has emerged as the world’s most populous city-region with nearly 42 million inhabitants, and the broader Asian urban population is projected to exceed 55% by 2030. This densification directly scales the demand for Grab’s localized mobility and delivery infrastructure.

https://www.copernicus.eu/en/news/news/observer-seven-things-we-learned-un-world-urbanization-prospects#:~:text=The%20United%20Nation’s%20World%20Urbanization,cities%20and%2036%25%20in%20towns. Near-Universal Mobile Connectivity: The GSMA Intelligence Mobile Economy 2026 report indicates that smartphone penetration in the region has successfully reached the previously forecast 84% benchmark. With a growing number of connections operating on high-speed 3G/4G/5G broadband, the “mobile-first” population has matured into a “mobile-only” consumer base that relies on superapps for daily survival.

The Persistent “Underbanked” Gap: While the 2024/2025 ASEAN Monitoring Progress Report by the UNCDF highlights that pure financial exclusion (unbanked) has dropped significantly to approximately 20.8%, a massive opportunity remains in the “underbanked” segment. The World Bank’s Global Findex 2025 and the e-Conomy SEA 2025 report note that nearly 70% of adults in Southeast Asia still lack access to credit, insurance, or wealth management tools. This provides Grab’s digital banking and lending arms with a vast, underserved market as the region transitions toward a $1 trillion digital economy.

These trends will provide long-term secular support for Grab’s services, ensuring that the market it operates in continues to expand rapidly.

Historical TAM Expansion

Also, the ability of management to “manufacture” new TAM is often a more reliable predictor of long-term value than the initial size of the market they enter.

Over the years, Grab has consistently expanded its TAM, demonstrating its ability to adapt and evolve. What started as a taxi-booking app in 2012 has transformed into a multi-modal platform, adding food delivery and, more recently, digital banking. The company has expanded geographically, with the acquisition of Foodpanda Taiwan marking its first major step out of Southeast Asia. Similarly, its acquisition of Stash signals Grab’s entry into the digital investing space, which could tap into the $5 billion+ AUM market.

“Companies can expand their TAMs through business category evolution, hence placing their products or services at the heart of an ecosystem. Done successfully, this allows the company to take advantage of network effects, encourages customers to remain within the ecosystem, and extends a company’s period of competitive advantage.” – Michael Mauboussin

(Almost) Just as Steve Jobs transformed the $91 billion cell phone industry into a multitrillion-dollar mobile economy by redefining the device as a software platform, Grab’s leadership has consistently demonstrated an operational reflex for market creation rather than just market capture.

This “optionality” was embedded in their DNA as far back as the F-1 filing, where they identified the “informal economy” not as a static segment, but as a massive, underserved opportunity for digital infrastructure.

“As we continue to expand our platform and increase the breadth of our offerings over time, our platform is able to address additional consumer and business needs, and grow our addressable market. For example, given the importance of small businesses and the informal economy, we believe there is a large and important opportunity to help such businesses and participants in the informal economy to navigate an increasingly digital world. We leverage our existing reach with our driver- and merchant-partners to provide digital tools and training that are critical to thriving in the increasingly digital economy, helping to lay the foundations for more inclusive growth across the region. With our scale, ecosystem and platform advantages, we believe that we are well-positioned to navigate the complexity of Southeast Asia and address certain key challenges in the region.“ – F-1

The full story starts here:

The rest of this post covers TAM penetration and market share dynamics, the identification of seven key growth drivers going forward, and two valuation approaches. If you’re serious about sharpening your investing edge, the full post (and all my previous premium content, including valuation spreadsheets, deep dives (e.g. well-known mid- and large caps such as LVMH, Duolingo, Meta, Edenred as well as more hidden gems such as Tiger Brokers, Digital Ocean, Ashtead Technologies, InPost, Timee, and MANY more) and powerful investing frameworks are just a click away. Upgrade your subscription, support my work, and keep learning.

Annual members also get access to my private WhatsApp groups – daily discussions with like-minded investors, analysis feedback, and direct access to me.

PS: Using the app on iOS? Apple doesn’t allow in-app subscriptions without a big fee. To keep things fair and pay a lower subscription price, I recommend just heading to the site in your browser (desktop or mobile) to subscribe.