In the first part of this FICO deep dive series, I laid out the structural foundations of Fair Isaac Corporation. That piece provided a comprehensive 11,000-word overview of the business history, the business model, the two major segments (and sub-segments), and the products (as well as a concise 90-second-pitch). If you haven’t read that comprehensive overview yet, you can find it here:

Deep Dive: Fair Isaac ($FICO) – Part 1

You likely think of global ubiquity in terms of the technology in your pocket or the way we travel across borders. But there is a silent sovereign in the American economy that moves more volume than the tech icons we obsess over, and it does so without a single retail storefront.

I’m focusing this second part of our analysis (6,500 words) on everything you need to know about the quality of the business itself, specifically its competitive advantages and the people calling the shots from the C-suite. So without further ado, let’s get into it:

As a reminder, here’s what I will cover in this deep dive series:

“BAM BAM BAM BAM BAM” 90-Second Pitch – Why Fair Isaac and Why Now?

1) Understanding the Business

1.1. Business History

1.2. Product

1.3. Business Operations

1.4. Customers

1.5. Industry & Competitive Landscape

2) Business Quality

2.1. Competitive Advantages Analysis

2.2. Other Thoughts on Business Quality

3) Management and Governance

3.1. Management Background

3.2. Integrity, Incentives, and Compensation

3.3. Capital Allocation

3.4. Management Roasting

4) Financial Health

4.1. Balance Sheet Health

4.2. Operating Perspective

4.3. Off-Balance Sheet Items & Hidden Risks

5) Risks

5.1. Inversion

5.2. VantageScore vs. FICO: Is the Credit Scoring Giant Losing Its Grip?

6) Other Items

7) Valuation

7.1. Past Growth

7.2. Future Growth (including a TAM analysis and identifying key growth drivers)

7.3. Valuation Work

Fun Fact

Appendix

Disclaimer: The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

Part 2 – Business Quality

2.1. Competitive Advantage Analysis

The Tollbooth Model

Based on the understanding of FICO’s business model that we developed in part 1, I want to start this “competitive advantage discussion” with a more general observation:

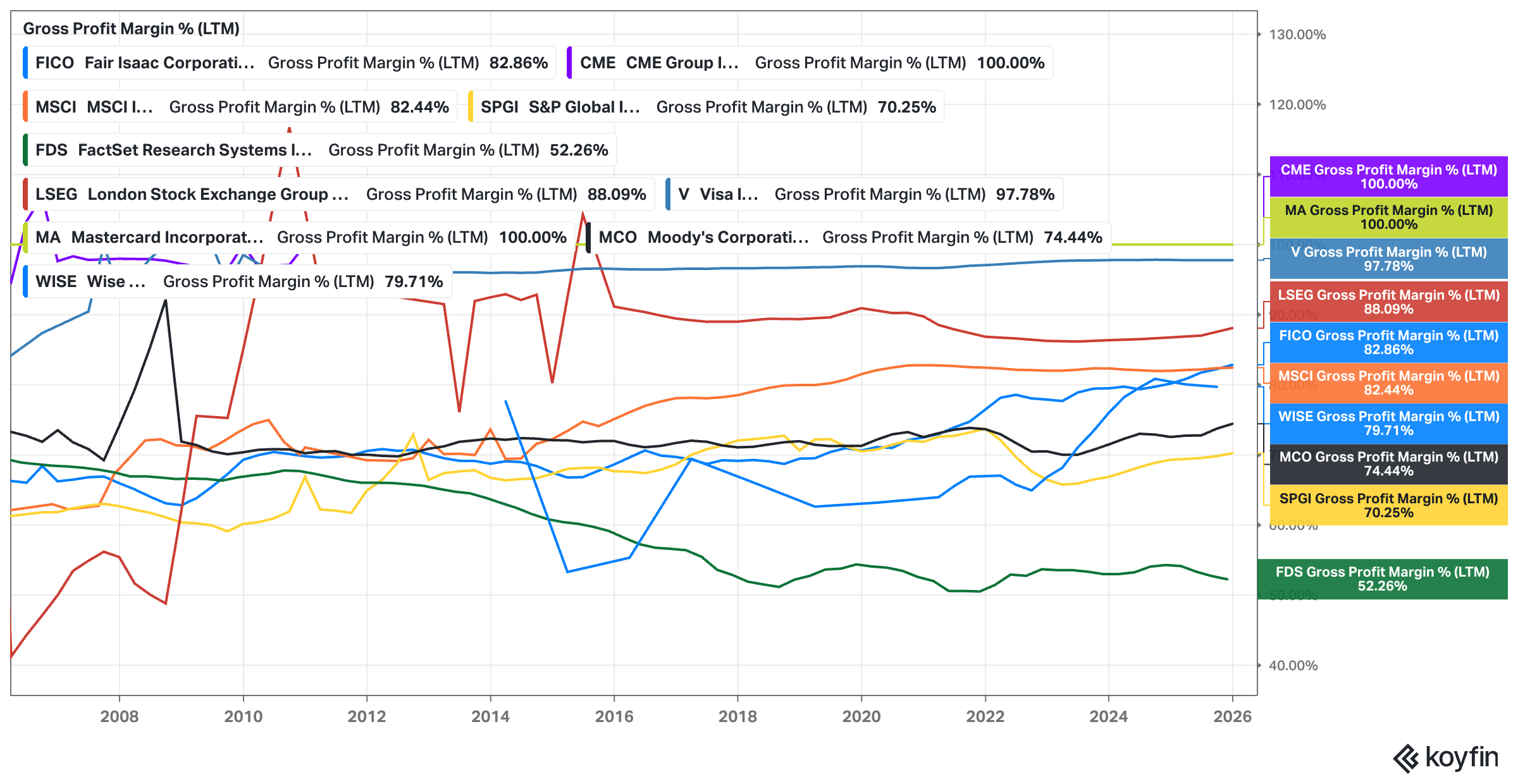

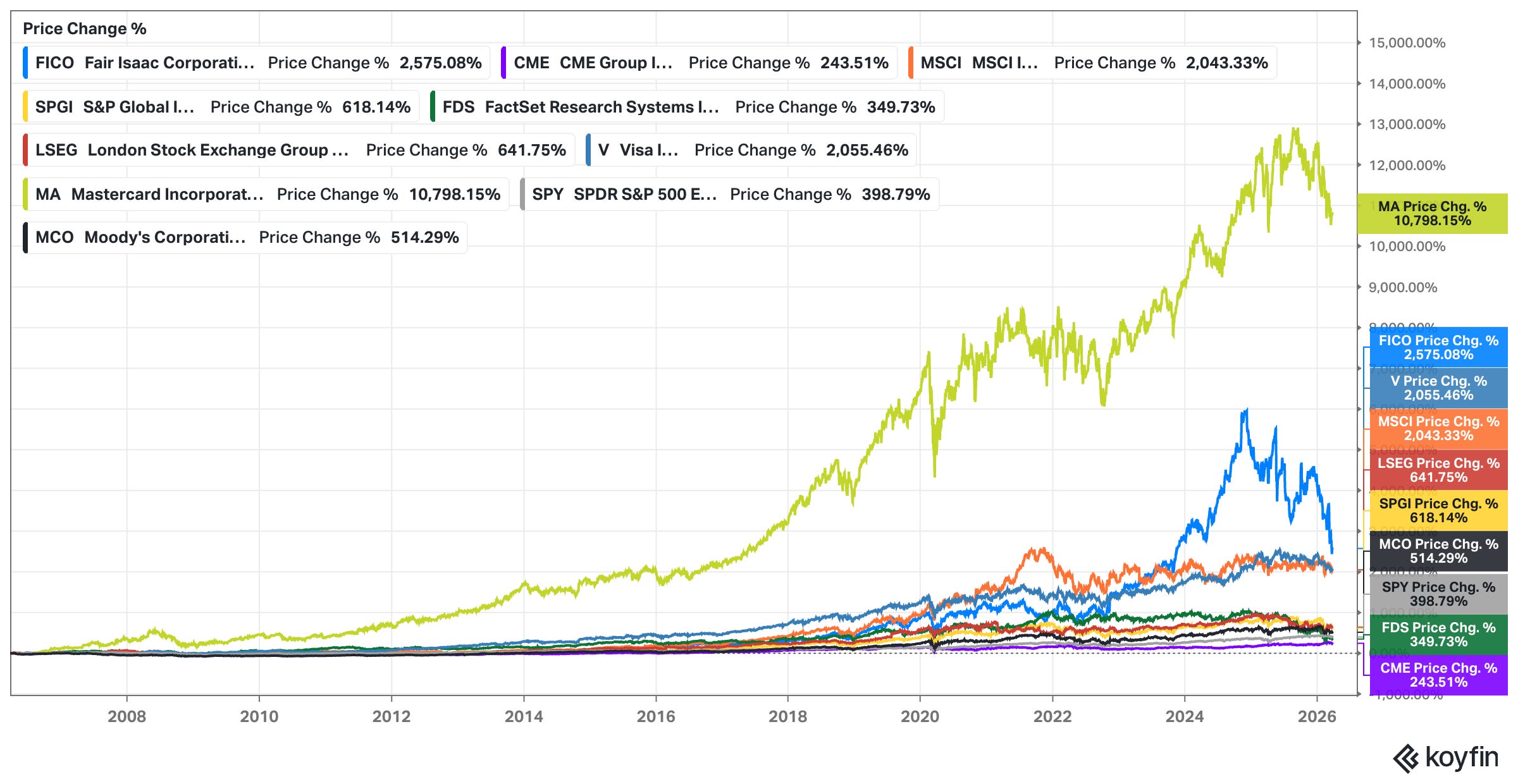

The “financial tollbooth” model is a powerful and enduring business model that continues to create clear winner-takes-all or winner-takes-most dynamics in many industries. Companies like S&P Global, Wise, LSEG’s clearing business, Moody’s, MSCI, CME Group, and Mastercard/Visa are all prime examples of businesses that sit at the heart of the financial system, taking a small fee every time money moves or decisions are made. These tollbooths thrive because they are embedded into the system itself – they don’t manufacture physical goods or take on significant capital expenditures, yet they continue to enjoy exceptional margins and stable, recurring revenue streams.

Their fees, often a tiny percentage of a much larger transaction, are largely invisible to end-users, making them highly efficient revenue generators. And the best part? Once these tollbooths are in place, they benefit from tremendous scalability with minimal ongoing investment.

For FICO, its tollbooth model is equally powerful. It’s embedded at the very heart of the U.S. credit and mortgage markets. In 2025, FICO scores were used in over 90% of top U.S. lending decisions. Each time a consumer applies for a loan, buys a car, or even rents an apartment, a FICO score is used to assess their creditworthiness. Just like Visa and Mastercard, FICO charges a small fee (typically only about 0.2% of the average mortgage closing cost) every time a transaction occurs. With its status as the de facto standard in U.S. credit risk assessment, FICO remains indispensable.

Similar to MSCI, FICO’s pricing power and dominance in the industry are underpinned by its cultural and regulatory embeddedness. FICO scores are so deeply woven into the financial fabric that they are the primary measure of risk in the U.S. mortgage industry, where 98.8% of all U.S. mortgage-backed securities rely on FICO scores for risk assessment.

Despite these advantages, FICO’s position in the financial tollbooth space is not without its risks. While VantageScore, a joint venture of the three major U.S. credit bureaus (Experian, TransUnion, and Equifax), has been working to challenge FICO’s dominance, the competitive dynamics in the industry – at least so far – are still structured in a way that benefits FICO. The credit scoring market, much like other financial tollbooths, exhibits clear winner-takes-all or winner-takes-most characteristics.

We embedded this FICO management comment from 2025 in part one, explaining the nature of this industry structure:

“As for lender choice, the FHFA has long rejected the practice because it undermines the safety and soundness of the enterprises and their counterparties, damaging liquidity in the $12 trillion mortgage industry. Lender choice encourages mortgage participants to shop for the most [ lax score, which drives unavoidable gaming and adverse selection for all risk holders“

And today I stumbled across this comment by Akre Capital (especially known to be a long-term Moody’s shareholder), who made a similar point:

“Allowing lenders to cherry-pick a single score creates “rating shopping,” selecting the highest score rather than the most accurate or most accepted. This leads to an adverse-selection problem for consumer-credit investors. FICO’s dominance is a market-driven outcome because it is the score demanded by investors."

In short, once a standard is established, it is extremely difficult to get a competing standard off the ground.

The industry structure is worth noting, as FICO’s tollbooth model shares characteristics with other leading firms like S&P Global and Moody’s in debt markets or CME Group in futures and commodities trading. These companies, much like FICO, charge fees each time a decision is made, whether it’s through credit ratings, securitization, or trade execution. Their economic model is brilliant in its simplicity – asset-light, with virtually all revenue flowing to the bottom line. Unsuprisingly, their stocks crushed it over the last 20 years.

CME Group, for instance, benefits when market volatility increases, as more trading activity translates into higher revenues. MSCI, meanwhile, has a different spin on the tollbooth model. By charging a small fee on trillions of dollars tied to financial benchmarks, MSCI’s pricing power remains largely invisible to individual users, making it extremely durable and less sensitive to regulatory pushback.

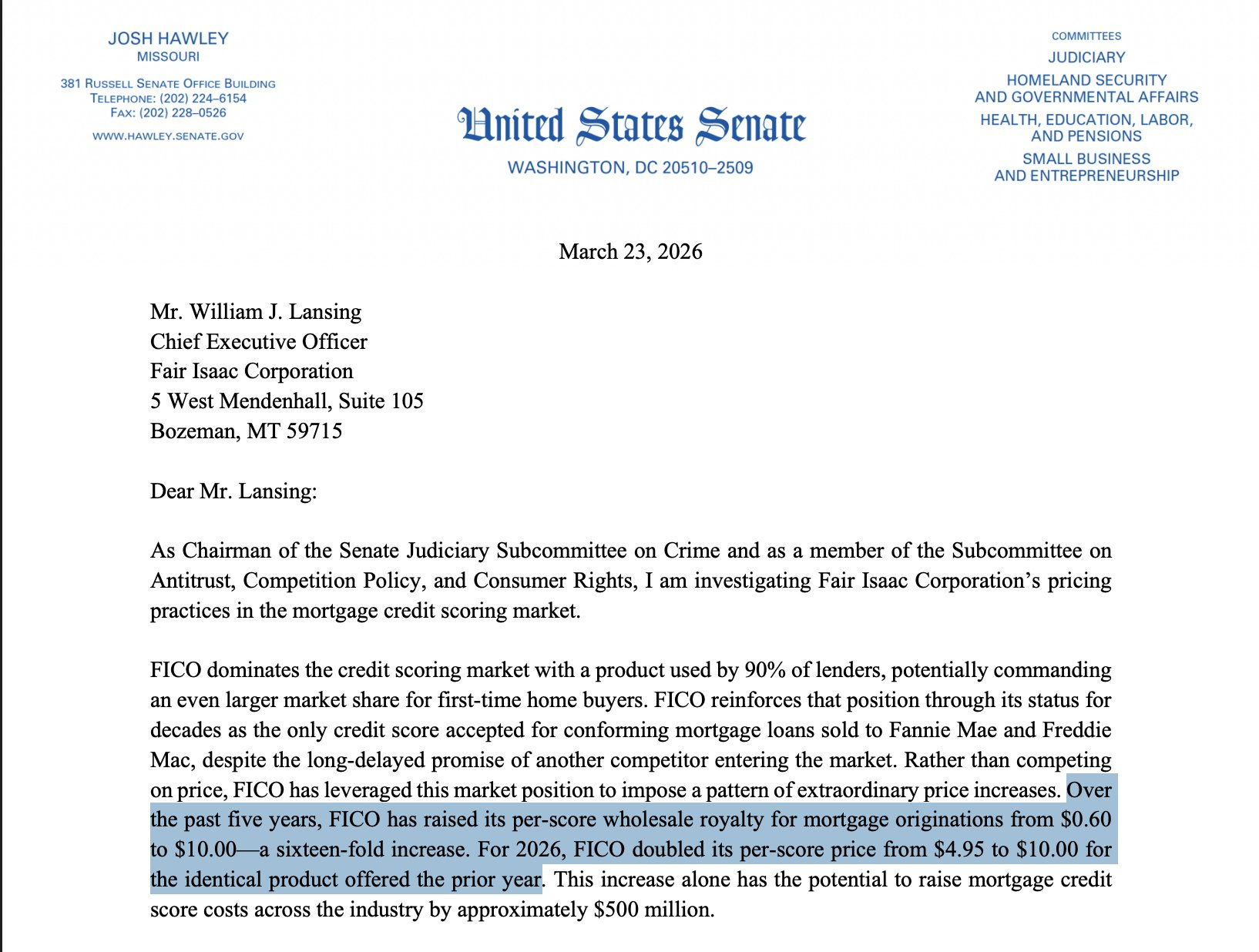

In FICO’s case, the risk to its tollbooth model stems from growing competition within the Scores segment and its increasing vulnerability to pricing scrutiny. While it has successfully raised prices for mortgage scores by 1,600% between 2022 and 2026, the pressure from the credit bureaus, which now act as both partners and competitors in the space, is intensifying. The recent approval of VantageScore 4.0 for use in government-backed mortgages by the FHFA in July 2025 is a pivotal development, undermining FICO’s monopolistic pricing power. This move is significant as it potentially opens the door for lenders to diversify their score sources, potentially squeezing FICO’s ability to maintain its past pricing leverage.

Despite these threats, FICO’s business model remains incredibly resilient. Its “tollbridge” strategy, similar to that of companies like Verisk Analytics (which serves the insurance industry) continues to generate exceptional margins. These businesses all share a common trait: they operate as essential intermediaries in systems that are difficult to disrupt.

A Powerful Industry Standard

This is where it gets interesting

Become a paying subscriber to read the rest of this post and get access to all of my other research, including valuation spreadsheets, deep dives (e.g. well-known mid- and large caps such as LVMH, Duolingo, Meta, Edenred as well as more hidden gems such as Tiger Brokers, Digital Ocean, Ashtead Technologies, InPost, Timee, and MANY more), and powerful investing frameworks.

Annual members also get access to my private WhatsApp groups – daily discussions with like-minded investors, analysis feedback, and direct access to me.