You likely think of global ubiquity in terms of the technology in your pocket or the way we travel across borders. But there is a silent sovereign in the American economy that moves more volume than the tech icons we obsess over, and it does so without a single retail storefront.

Every year, Fair Isaac Corporation – better known as FICO – sells over 10 billion scores (which translates to approximately 27 million scores purchased daily).. To put that in perspective, that is roughly 40 times the number of iPhones Apple ships to the entire world in a year and nearly double the total number of passengers who board a commercial flight globally.

It is the de facto passport for financial mobility, used in 90% of all top U.S. lending decisions and serving as the primary measure of risk for over 12 trillion dollars in U.S. mortgage debt.

If you want a mortgage, an auto loan, or even to rent an apartment, you aren’t just a person – you are a three-digit number owned by a company that started in a studio apartment in 1956 with 400 dollars and a radical dream of replacing “handshake-and-vibes” lending with objective algorithms.

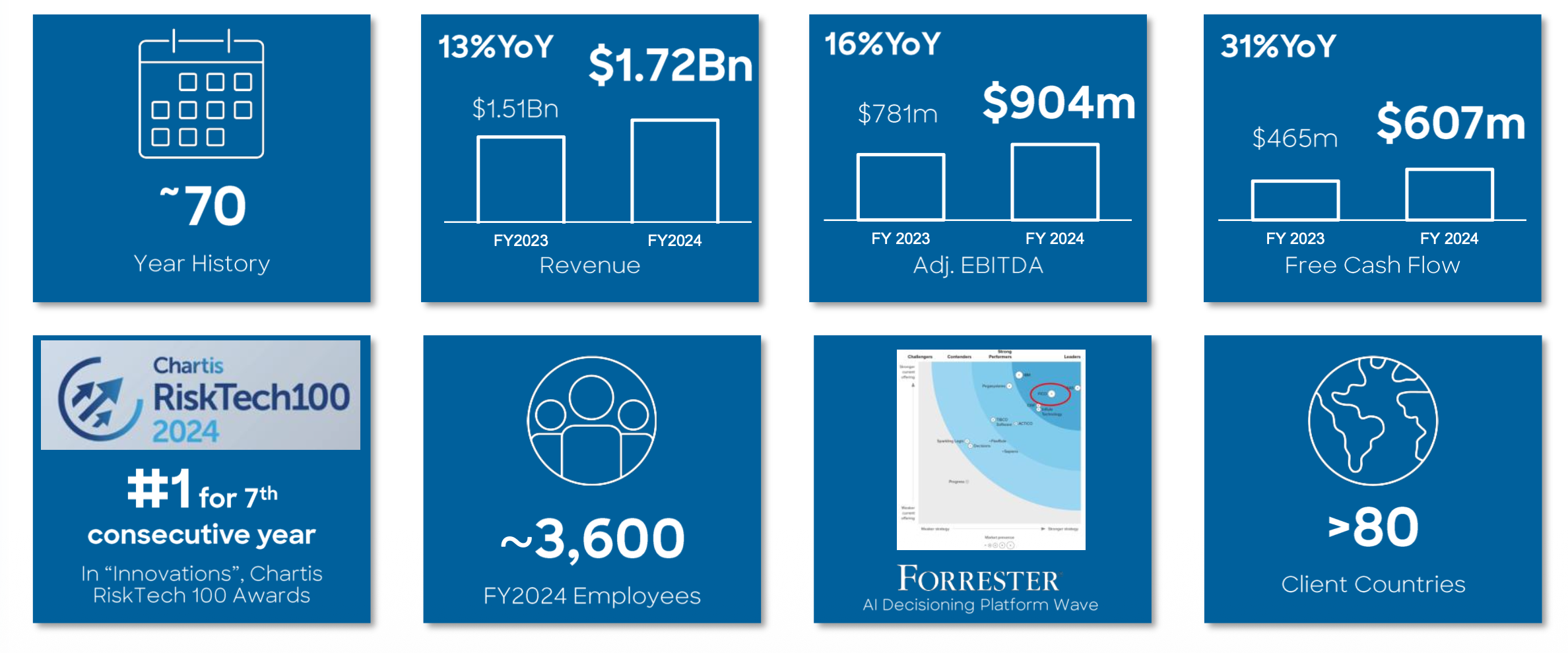

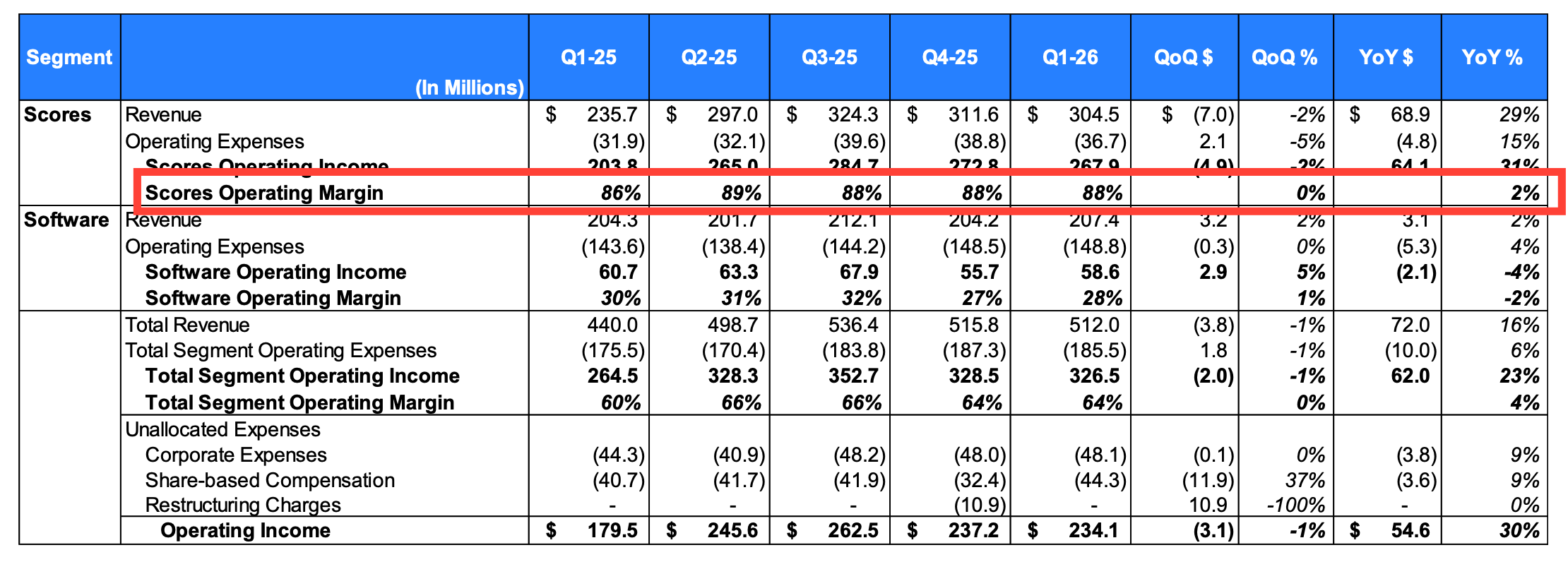

In this multi-part deep dive, I want to pull back the curtain on the most efficient toll-bridge in global finance (88% EBIT margins in the Scores segment), and why its supposedly certain downfall was just derailed by a massive regulatory reversal.

I find it fascinating how few people realize the sheer, unchecked pricing power FICO wields. Between 2022 and 2025, the company did something that would be a death sentence for almost any other business – and it brought its fair set of challenges to FICO too, to be fair. It raised the price of its mortgage scores from roughly 0.60 to 4.95 dollars by 2025. That is an 800% increase in just three years. And then again to $10.00 (or $4.95 + $33 Success Fee) for 2026 – another 2x increase.

Imagine your internet provider or utility company jacking up rates by eight times; there would be a congressional inquiry by sunset.

Yet, because FICO is the “universal language” of the mortgage market – cited in 98.8% of all securitizations – lenders simply paid the toll. The financials are the stuff of legend. The company’s core Scores segment operates with 88% operating margins. Even more staggering is the “95% Rule” – for every new dollar of revenue FICO generates through these price hikes, nearly 95 cents drop straight to the bottom line.

As of FY2024, the company turned 1.72 billion dollars in revenue into more 600 million dollars of free cash flow. It is a capital-light compounding machine that requires no factories. It is pure risk math.

For the last 1-2 years, the primary “bear case” for FICO was built on the threat of “Lender Choice” – a regulatory push to break the monopoly by allowing competitors like VantageScore into the ecosystem. The plan was to move from a “tri-merge” (where lenders pull scores from all three bureaus) to a “bi-merge” (where they only pull two). This would have effectively stripped FICO of its guaranteed seat at the table. But everything changed in July 2025. In what some have dubbed the “Pulte Pivot,” FHFA Director Bill Pulte unexpectedly maintained the tri-merge requirement, effectively pulling all three bureaus and slamming the door on the bi-merge transition. This move preserved the existing plumbing of the mortgage market and cemented FICO’s dominance just as the market thought the “invisible engine” was about to be dismantled.

Given the excessive price hikes, this doesn’t mean the regulatory risk is “done” though.

Is the Largest Drawdown Since 2008 an Opportunity?

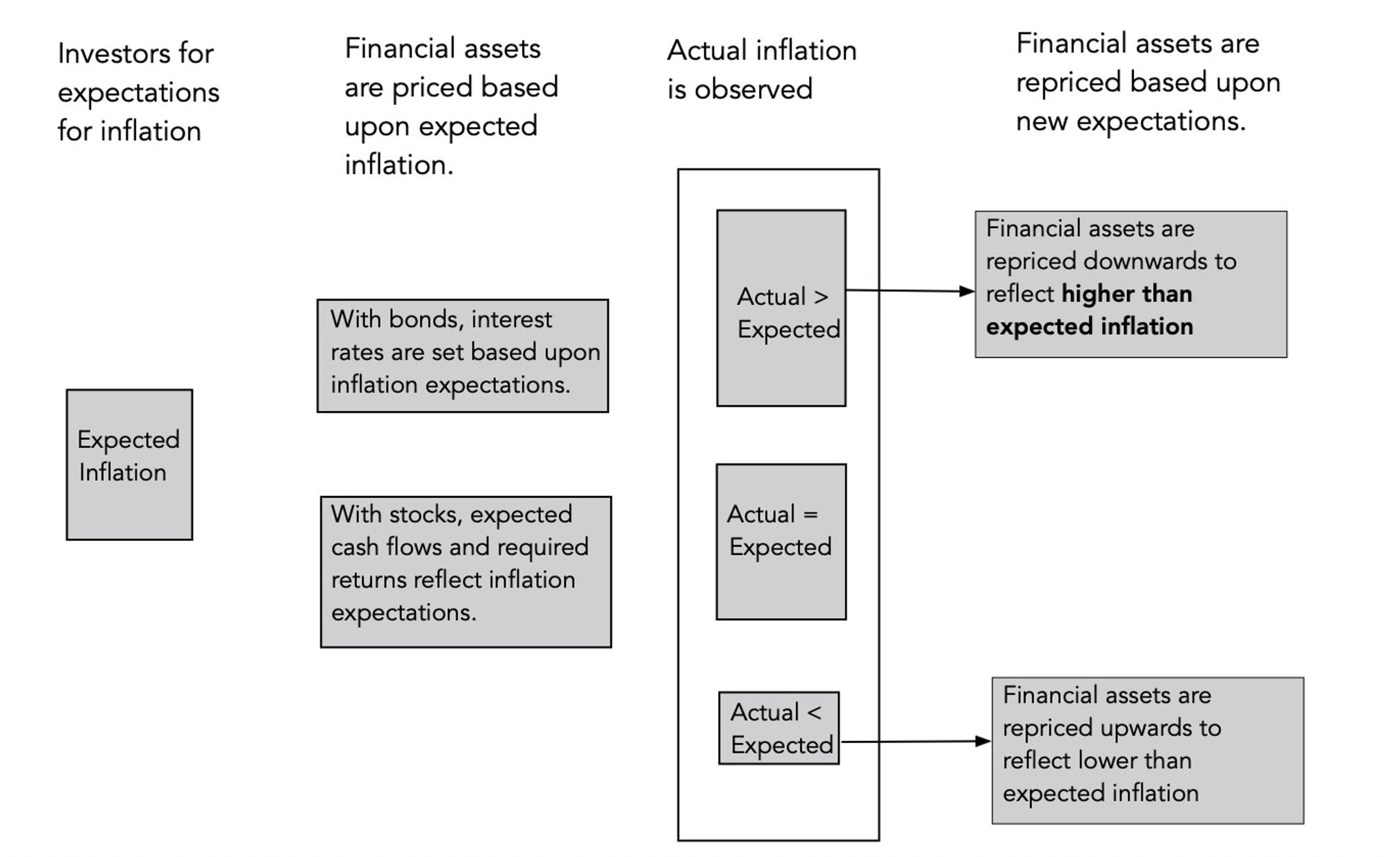

The world looks significantly more volatile than it did even a few months ago. The ongoing war with Iran has sent geopolitical shockwaves through every asset class, and we are now staring down a macro environment where inflation is expected to skyrocket.

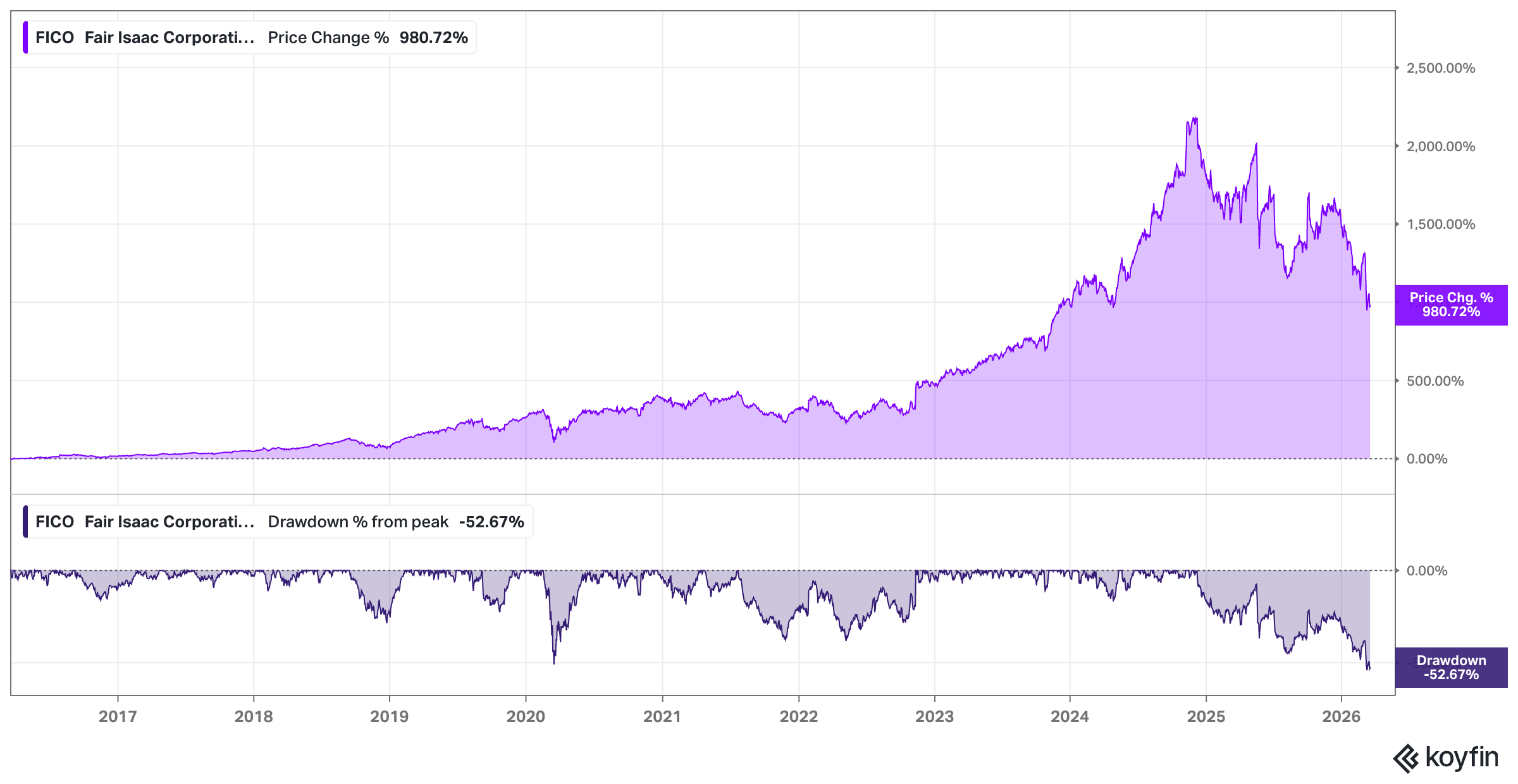

Market sentiment has turned decidedly cold. FICO is currently experiencing its largest drawdown since the Great Financial Crisis, with the stock falling 52.67% from its peak.

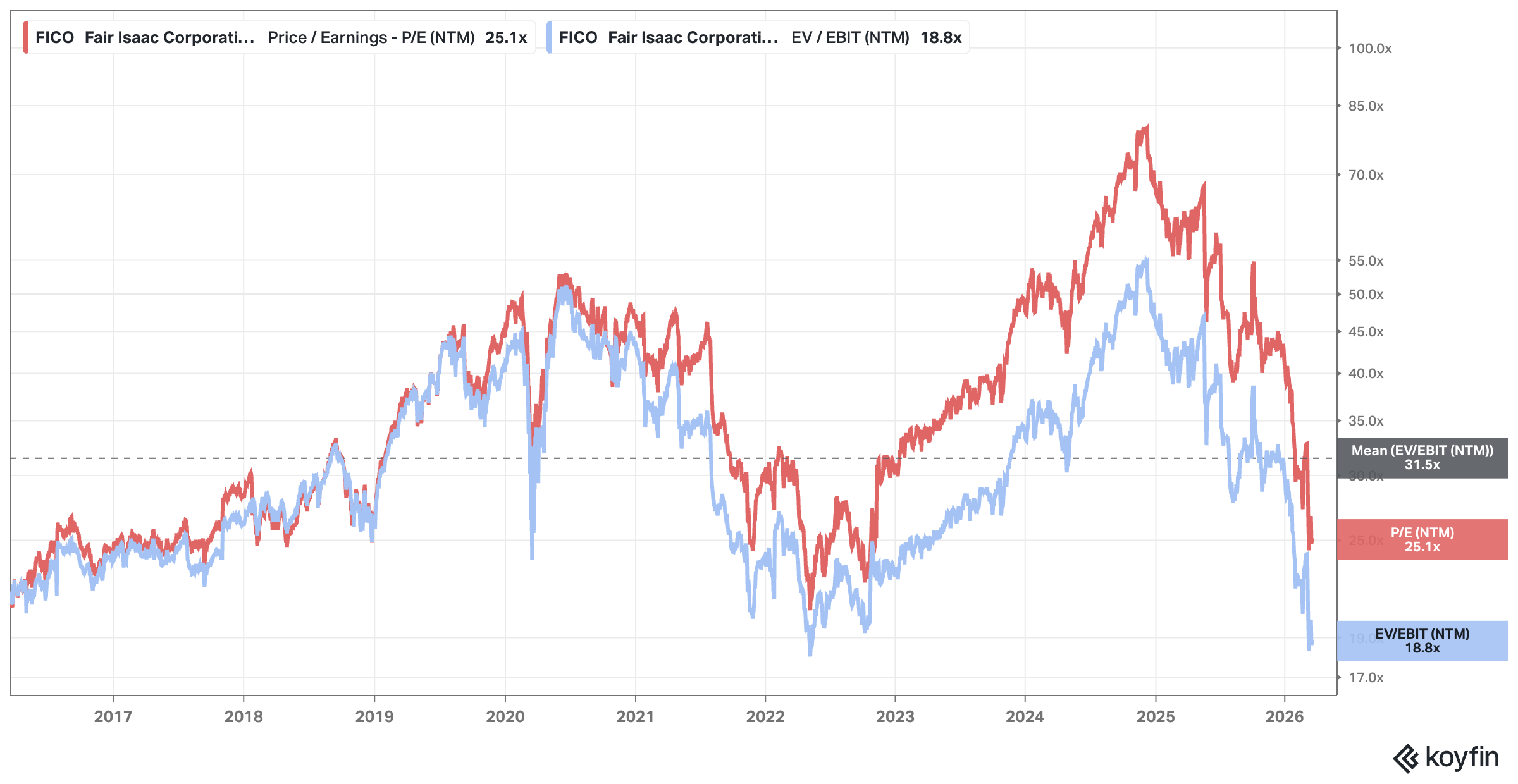

I see a market growing increasingly cautious around credit risk, fueled by concerns over debt exposure at firms like Blue Owl ($OWL) and Oracle ($ORCL). This anxiety may have contributed to the drag on FICO’s valuation, down to 25.1x NTM P/E and 18.8x EV/EBIT – well below its five-year mean of 31.5x.

You have to ask yourself: is this a warning of a broader credit event, or a generational buying opportunity for a monopoly?

So in this deep dive series, I’ll explore how FICO is positioned to navigate this era of stagflation and war, and whether the “high beams” of federal regulators are still a threat after the Pulte Pivot.

In this first part, we cover the business’s history, the business model, its products, and competitive environment (11,000 words in total).

Here’s what I will cover in this deep dive series:

“BAM BAM BAM BAM BAM” 90-Second Pitch – Why Fair Isaac and Why Now?

1) Understanding the Business

1.1. Business History

1.2. Product

1.3. Business Operations

1.4. Customers

1.5. Industry & Competitive Landscape

2) Business Quality

2.1. Competitive Advantages Analysis

2.2. Other Thoughts on Business Quality

3) Management and Governance

3.1. Management Background

3.2. Integrity, Incentives, and Compensation

3.3. Capital Allocation

3.4. Management Roasting

4) Financial Health

4.1. Balance Sheet Health

4.2. Operating Perspective

4.3. Off-Balance Sheet Items & Hidden Risks

5) Risks

5.1. Inversion

5.2. VantageScore vs. FICO: Is the Credit Scoring Giant Losing Its Grip?

6) Other Items

7) Valuation

7.1. Past Growth

7.2. Future Growth (including a TAM analysis and identifying key growth drivers)

7.3. Valuation Work

Fun Fact

Appendix

Disclaimer: The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

High-Level Thesis: “Bam Bam Bam Bam Bam”-90 Second-Hypothesis

When you think of the stock market, one of the biggest challenges is quickly determining whether a business truly has potential. As my regular readers know, Bill Miller, legendary investor, is known for his “Bam Bam Bam Bam Bam” approach to pitching stocks – which I’ve shamelessly copied.

In essence, it’s a quick pitch that gets straight to the point: Why is this a great business? Miller’s style demands clarity and precision, with just five reasons why an investment could make sense. So, let’s apply this framework to Fair Isaac Corporation (FICO), a company that may not be on everyone’s radar, but absolutely should be.

Here we go …

BAM #1 – Indispensable Industry Standard: FICO’s scores are the industry standard. In fact, 90% of top U.S. lending decisions use FICO scores. Beyond that, FICO scores dominate the secondary market for securitizations, with 98.8% of U.S. securitizations – a financial process that pools income-generating assets (such as mortgages, auto loans, or credit card debt) and converts them into marketable securities – using FICO to communicate credit risk to investors. This is a business that has become synonymous with credit risk, and replacing FICO would be like changing the engine of a plane mid-flight – a daunting task.

BAM #2 – Unmatched Pricing Power & Value Gap: FICO is in the midst of a remarkable pricing transformation. After decades of keeping prices flat, FICO raised its wholesale mortgage score price from about $0.60 to $4.95 by 2025 – an eye-popping 800% increase –, and $10 by 2026. Despite this hike, FICO’s fee still represents a negligible 0.2% of average mortgage closing costs. This leaves ample room for further price hikes – at least if you have a long-term view (less so in the near term) – without significantly impacting volume.

BAM #3 – Elite Margin Profile: FICO’s Scores segment boasts near-monopoly margins, with 88% – yes, you read that right! – operating margins in Q1 2026. The key here is the low incremental cost structure: the core algorithms, developed decades ago (but frequently updated), require minimal investment to scale. That means when FICO raises prices or increases volume, almost every new dollar drops straight to the bottom line.

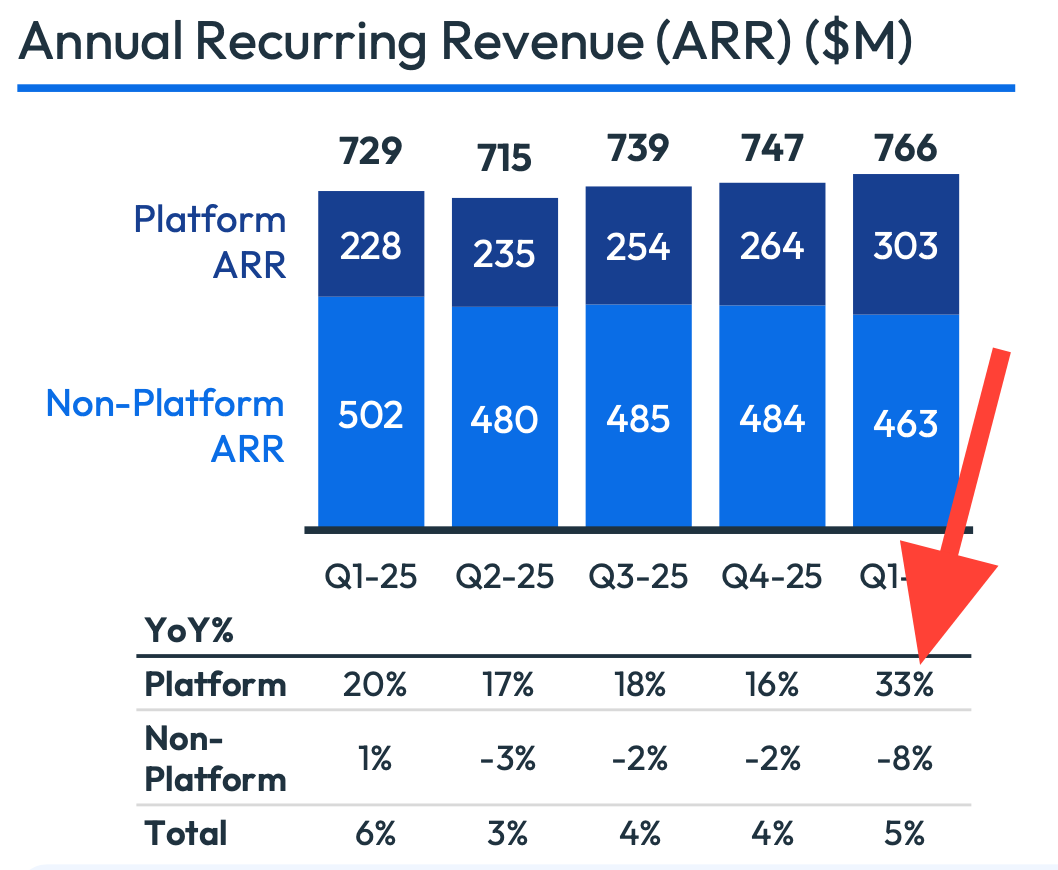

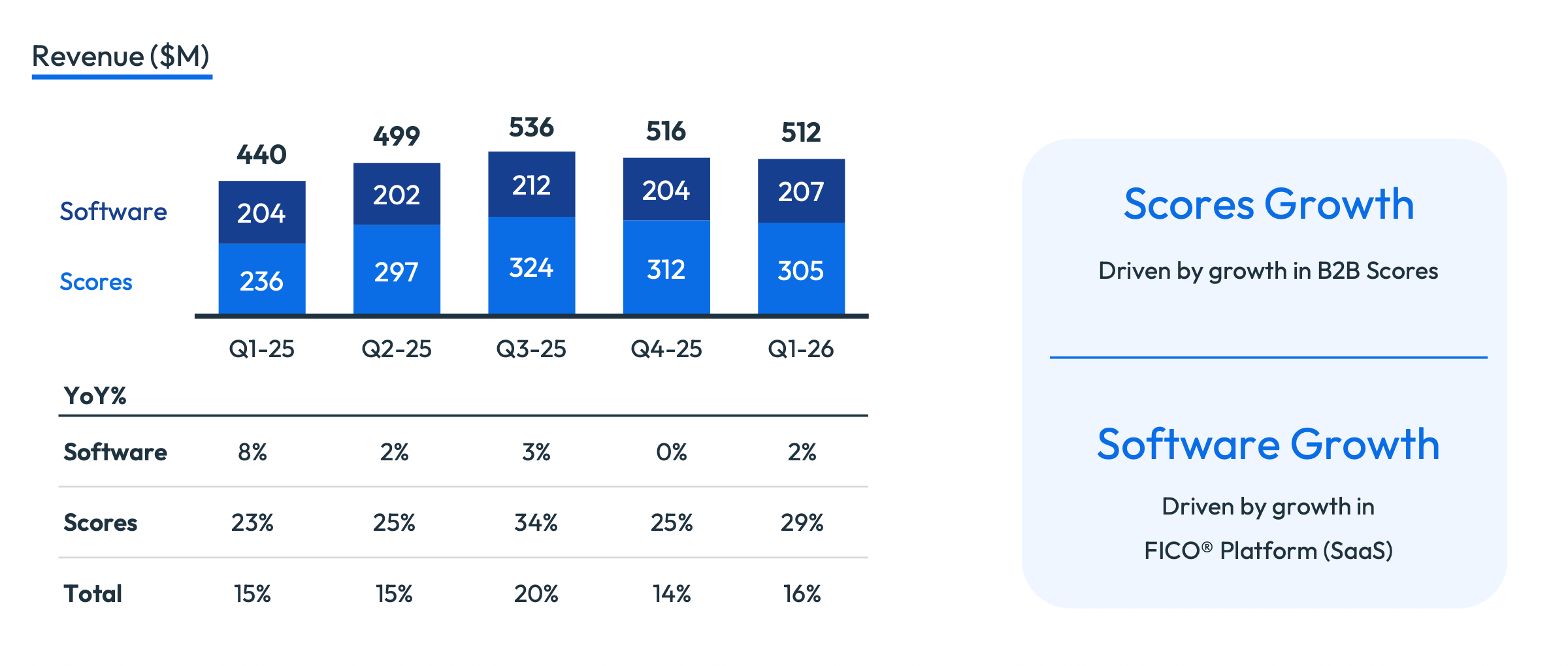

BAM #4 – Strategic SaaS Transformation: FICO is transitioning its Software business from legacy on-premises applications to a cloud-native platform. This transformation is paying off, with platform-specific Annual Recurring Revenue (ARR) growing at over 30% in Q1. The company’s “land and expand” strategy is also working well, with existing customers spending significantly more as they adopt new decision-making use cases. This positions FICO for long-term growth in the SaaS space.

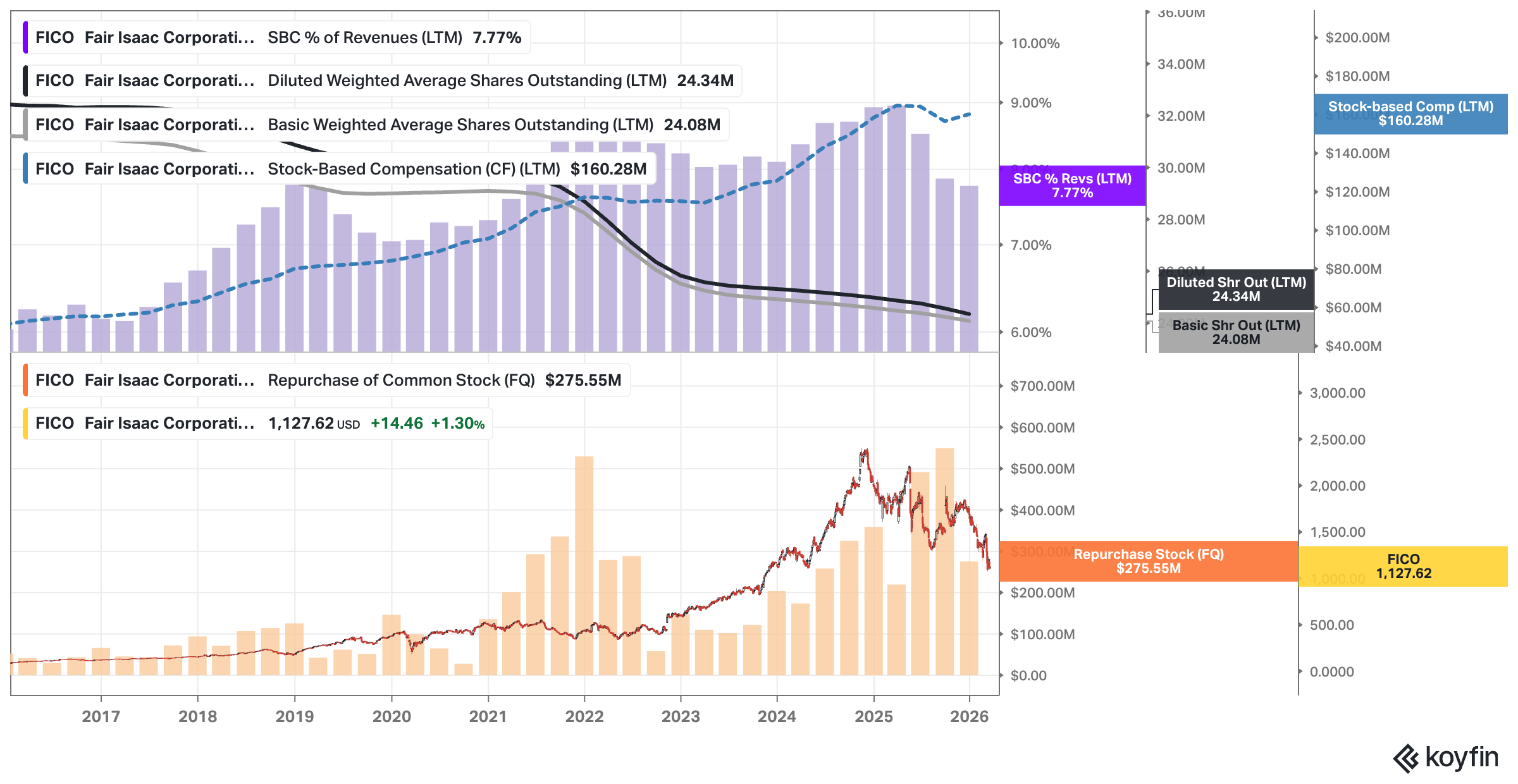

BAM #5 – Aggressive, Shareholder-Aligned Capital Return: FICO has used its cash flows to buy back stock aggressively, reducing its share count by 30% over the past decade, leading to incredibly fast profit per share growth. In fiscal 2025 alone, the company returned $1.4 billion to shareholders via buybacks.

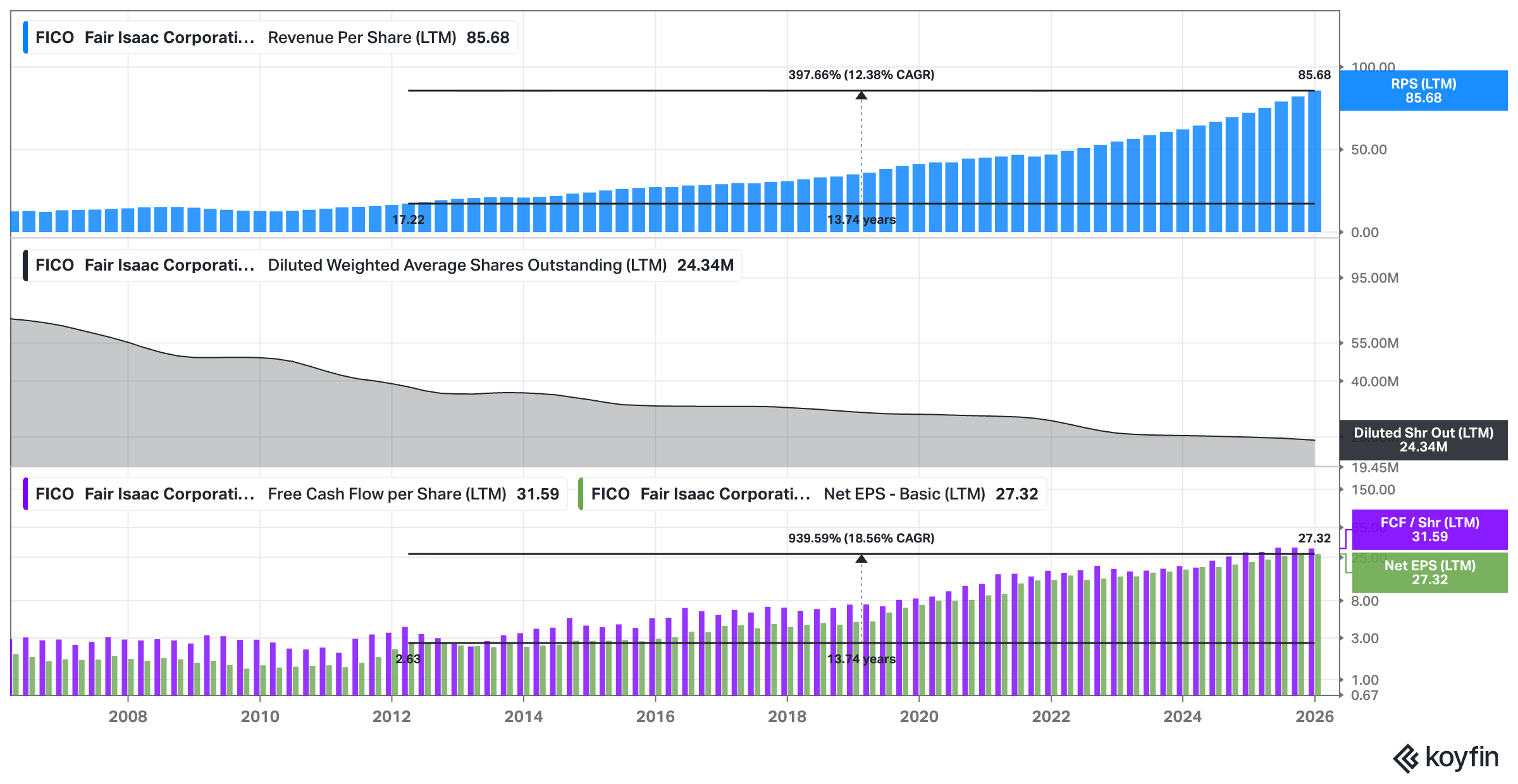

This strategy has led to a stellar 18% EPS CAGR over the last 13 years, far outpacing its 8-9% revenue growth (not per share revenue growth as displayed in the chart below). Simply put, FICO is showing its commitment to delivering value to shareholders.

As we enter 2026, FICO finds itself at a rare entry point. The stock has experienced a 52% price drop from its highs, making it a possibly attractive buy for long-term investors.

So why the drop?

What Went Wrong?

Despite FICO’s strong business fundamentals, the company hasn’t been immune to challenges. The key issues that have weighed on the stock recently are:

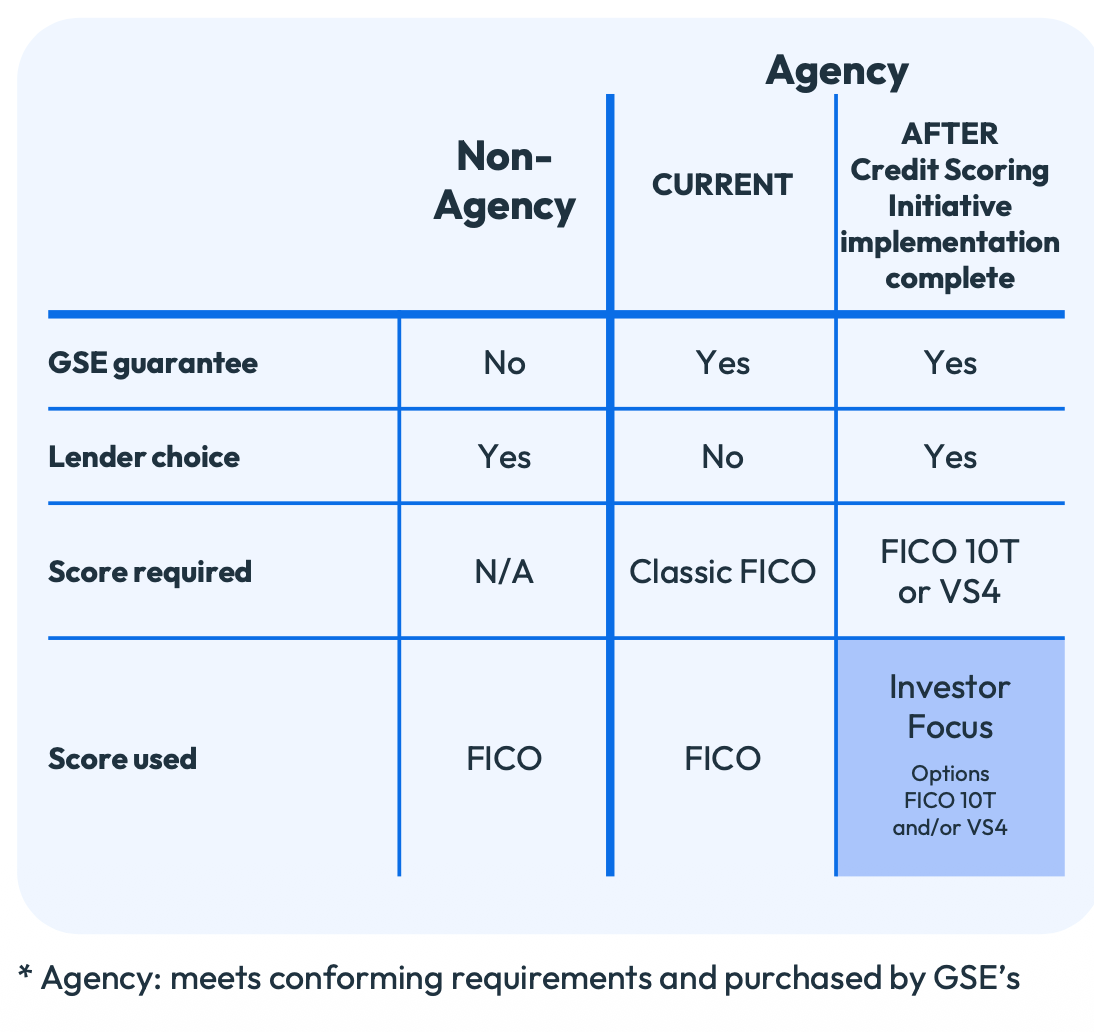

Regulatory Breach of the Monopoly: The FHFA’s formal transition to a “Lender Choice” model has opened the door for VantageScore 4.0 to compete directly with FICO in the market for Fannie Mae and Freddie Mac loans. While this introduces competition and substitution risk, it’s not an existential threat to FICO’s dominance – yet.

Volume and Revenue Contraction Risks: The potential shift from a “tri-merge” model, requiring three credit scores, to a “bi-merge” model, requiring only two, has the potential to reduce FICO’s score volume by as much as one-third per application. This could directly impact revenue growth in the short term.

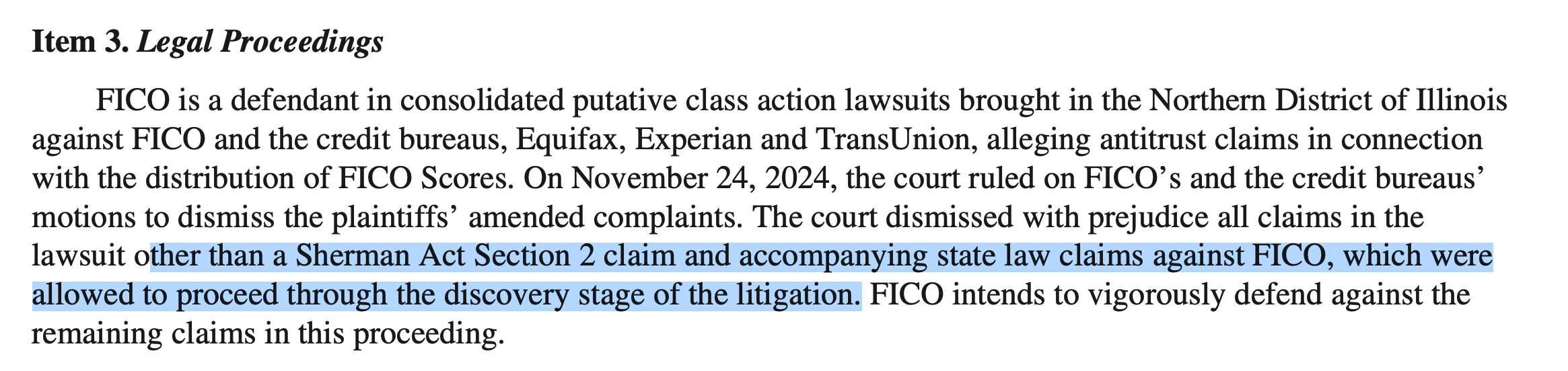

Intensifying Antitrust Scrutiny: FICO is currently defending itself in the “In re FICO Antitrust Litigation” case, which addresses its distribution practices and “transmission fees.” While it’s early in the legal process, the outcome could have implications for FICO’s cost structure.

“On November 24, 2024, the court ruled on FICO’s and the credit bureaus’ motions to dismiss the plaintiffs’ amended complaints. The court dismissed with prejudice all claims in the lawsuit other than a Sherman Act Section 2 claim and accompanying state law claims against FICO, which were allowed to proceed through the discovery stage of the litigation. FICO intends to vigorously defend against the remaining claims in this proceeding.“ - FY25 Annual Report

Software Segment Growing Pains: FICO’s transition to a SaaS model has not been entirely smooth. Despite strong growth in its Scores business, its Software segment grew a mere 2% in Q1 2026, possibly raising concerns among investors about the potential monetization lag this segment.

Part 1 – Understanding the Business

1.1. History: The Evolution of a Global Risk Standard

The story of Fair Isaac Corporation (FICO) is one of innovation, adaptation, and an unwavering commitment to shaping how credit risk is understood and quantified. From its humble beginnings in a small apartment to becoming a critical part of the global financial ecosystem, FICO has grown into the architect of the pervasive credit risk standard in the United States, serving thousands of businesses across over 100 countries. Let’s take a look at how this company evolved over the years to become a cornerstone of modern financial systems.

Founding and Early Innovations (1956–1980s)

Before we start with FICO itself, it’s worth highlighting how lending decisions were made historically – way back in the day! For most of the twentieth century, the world of credit was remarkably small, intimate, and – by today’s quantitative standards – frustratingly arbitrary. If you needed a loan to buy a home or expand a storefront, you didn’t appeal to an abstract score. You appealed to a person. Usually, this meant sitting across from a local bank manager who, at best, knew your family, your reputation, and perhaps even where you went to church. Decisions were built on a foundation of trust and familiarity that simply doesn’t scale in a modern economy. I find it fascinating how much weight was placed on a simple handshake.

If the manager liked your story, you were in. If he didn’t? You were out.

It was a gatekeeper’s paradise. There was no recourse and no objective data to prove him wrong.

This extreme subjectivity created a massive efficiency problem for the financial system. And because there was no standardized way to measure risk, lending was essentially a binary outcome. You either qualified for the prevailing interest rate or you were rejected entirely.

The concept of risk-based pricing – where you might pay a slightly higher rate because your profile is a bit thinner – simply didn’t exist yet. Everyone who was approved essentially paid the same price for capital. Think about that for a second. A doctor with twenty years of practice and a young baker starting her first shop would receive the same terms, provided they both cleared the manager’s subjective “trust” hurdle. This lack of nuance meant that banks were constantly leaving money on the table. They couldn’t comfortably lend to anyone outside their immediate social or geographic circle because they had no way to price that uncertainty. You were either a known quantity or a total mystery. There was no middle ground. It was an incredibly rigid way to run a national economy.

This brings us to Fair Isaac.

FICO’s journey began in 1956 when engineer Bill Fair and mathematician Earl Isaac – do you see where today’s name is coming from? –, both visionary thinkers, founded the company with a simple but powerful idea: to apply mathematical algorithms to make lending decisions more objective and standardized. The duo met at the Stanford Research Institute, and based on just $400 in personal investments (equivalent to approximately $5,000 today), they set up shop in a studio apartment in San Rafael, California.

In 1958, FICO achieved its first major milestone by selling its first credit scoring system to the American Investment Company (AIC). This was the beginning of a long journey toward mainstream adoption. Early on, these scoring systems were tailored to individual needs and were labor-intensive, often relying on physical paperwork and borrowed computers to process the data. Despite these challenges, it marked the birth of a product that would eventually reshape the credit industry.

The Equal Credit Opportunity Act of 1974 proved to be a pivotal moment in FICO’s growth. The legislation made it illegal to discriminate against applicants based on factors like gender or marital status, creating a powerful incentive for lenders to adopt more objective, data-driven methods of credit evaluation. FICO’s algorithmic scoring models provided a solution, helping lenders demonstrate that their decisions were merit-based and unbiased, thus propelling the company’s growth.

In the 1970s and 1980s, FICO expanded its reach as credit bureaus (nowadays officially known as Consumer Reporting Agencies or CRAs) – essentially, private companies that collect and manage data about your financial behavior – began consolidating. For context, by 1965, at the peak, the trade association for these companies (now known as the Consumer Data Industry Association) had over 2,200 members.

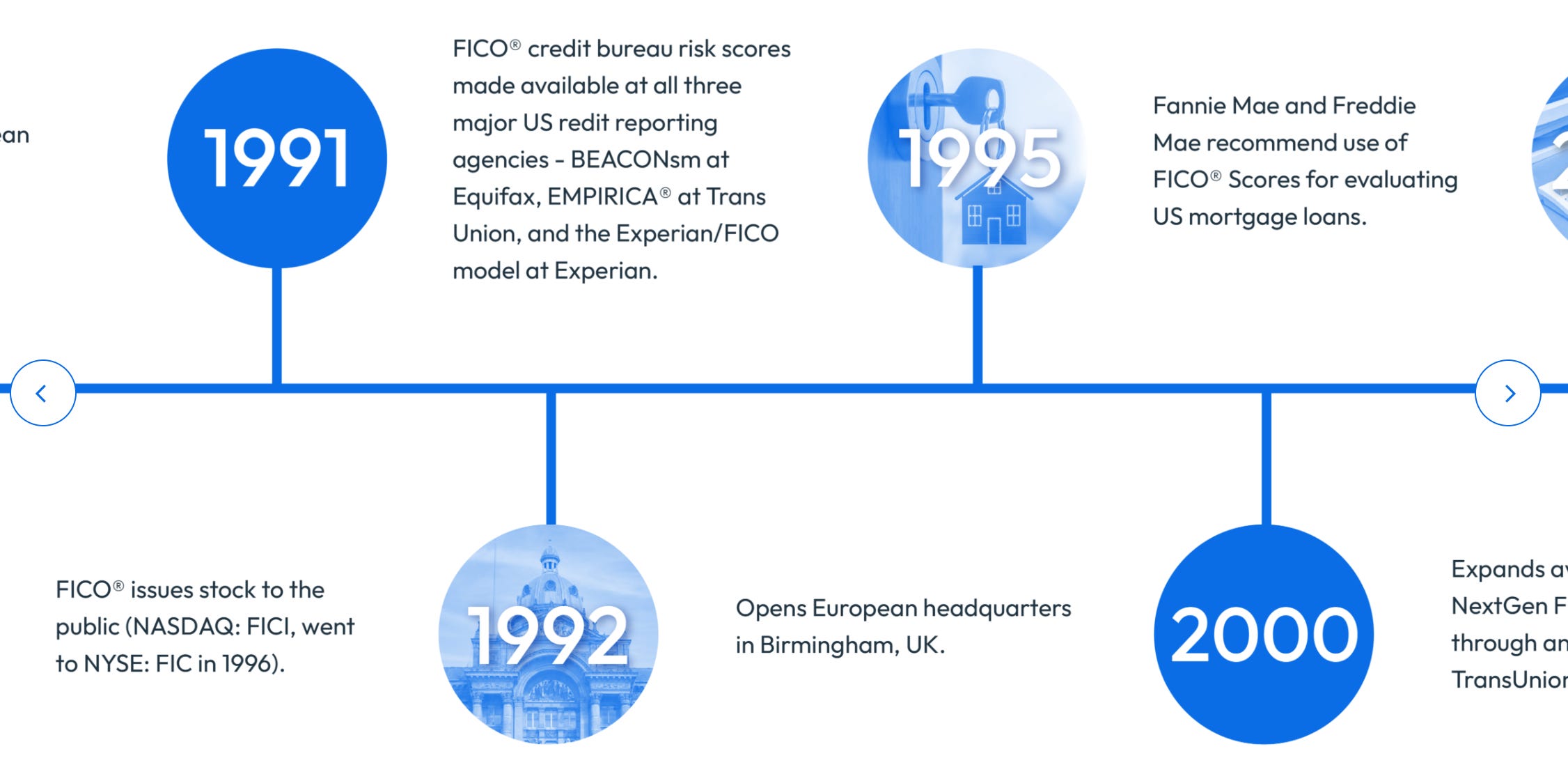

FICO recognized an opportunity to develop models that could be applied universally across different datasets. In 1981, they introduced “PreScore,” the first standardized credit bureau risk score, which laid the groundwork for the universally recognized FICO Score.

The company also went public in 1987 on the NYSE, marking a new chapter in its evolution.

Establishing the “Industry Standard” (1989–2011)

FICO’s true breakthrough came in 1989 with the introduction of the now-famous FICO Score, ranging from 300 to 850.

When researching FICO, I was asking myself why the score doesn't start at zero. So I’ve looked into the origins of the FICO scale and realized that starting at zero would be a mathematical nightmare for lenders because it implies an absolute certainty of default. Bill Fair and Earl Isaac chose the 300–850 range to provide enough "ticks" on the scale for high–resolution risk assessment. This spread allows for a concept called log–odds, where small point increases represent a doubling of your creditworthiness.

As we’ve learned, before 1989, determining creditworthiness was essentially a Wild West of subjective judgment calls. When FICO finally introduced its standardized 300 – 850 range, it fundamentally rewired the plumbing of the American financial system. FICO’s algorithm effectively turned personal behavior into a quantifiable asset class. It relies on five distinct variables, but the heavy lifting comes from your payment history and total debt levels – accounting for 65% of the total weight. You see, the model prioritizes consistency over sheer net worth. It functions as a track record. One slip-up on a mortgage payment carries more weight than a decade of on-time utility bills.

The remaining fragments of the score – length of history, credit mix, and new inquiries – serve as the fine-tuning for risk assessment. I find it fascinating that the algorithm rewards complexity. If you only hold a single credit card, the system views you as an unproven entity. It wants to see you juggle different types of debt, like an installment loan alongside revolving credit, to prove you can handle diverse financial obligations. Applying for a flurry of new accounts usually triggers a red flag because it signals a sudden, desperate thirst for liquidity. Keep it steady. This balance between the age of your oldest accounts and the freshness of your new ones creates a profile that lenders can actually trade against. It changed everything.

FICO’s standardized score quickly became the go-to method for assessing credit risk. Lenders embraced the simplicity and reliability of this scoring system, and it became a key part of their decision-making process.

Then, FICO reached a watershed moment in 1995 when Fannie Mae and Freddie Mac, the U.S. government-sponsored entities (GSEs), required the use of the FICO Score for all conforming mortgage originations. This move solidified FICO’s position as the industry standard, as it became the “lingua franca” of credit risk, enabling the mass securitization of debt. Investors demanded a consistent and reliable benchmark to assess loan pools, and FICO’s scoring system met that need.

Throughout the 1990s and 2000s, FICO diversified its offerings beyond credit scoring. The company expanded into decision software with the launch of products like Falcon Fraud Manager, a tool that now protects around two-thirds of all credit card transactions worldwide. This diversification helped FICO cement its reputation as not just a score provider, but as a comprehensive risk management partner for businesses.

Leadership Change and Strategic Pivot (2012–Present)

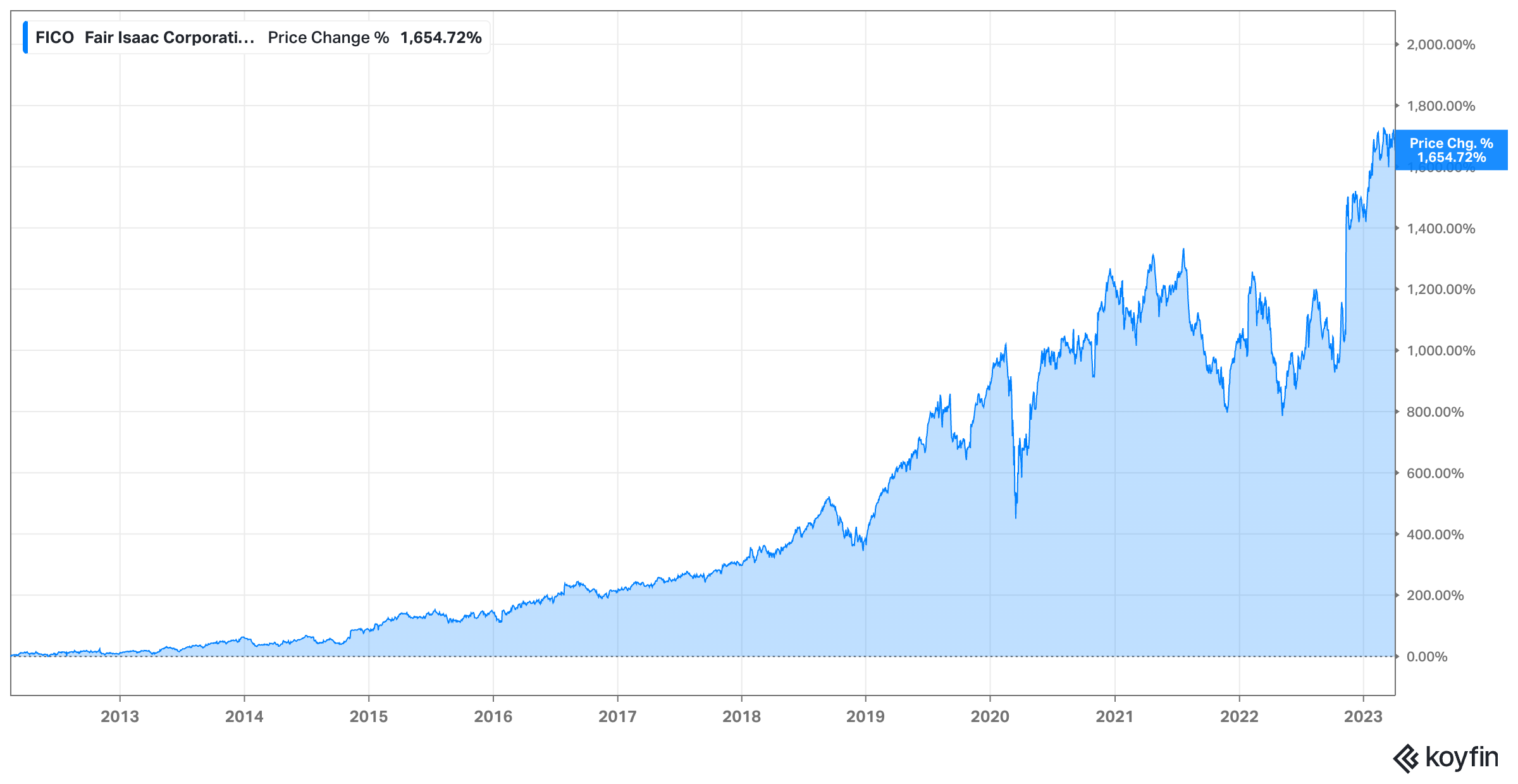

A significant shift occurred in 2012 when William J. Lansing was appointed CEO. Under Lansing’s leadership, FICO embarked on a path of modernization and aggressive monetization. This shift paid off in a big way: by 2023, the company’s stock price had increased approximately sixteen-fold. Lansing’s strategic vision positioned FICO to capitalize on both its legacy business and new growth opportunities in cloud-based software.

Importantly, for nearly three decades, FICO kept its prices largely unchanged, prioritizing widespread adoption. However, in 2018, the company began a strategic pricing shift, particularly in the mortgage sector. The price of wholesale mortgage scores jumped from around $0.60 to nearly $5.00 by 2025 – an 800% increase! This dramatic pricing move, although controversial, is a reflection of FICO’s growing recognition of the immense value it provides in the financial ecosystem.

FICO’s leadership recognized the growing importance of cloud-based technologies and embarked on a massive, multi-year investment to transition from legacy on-premises solutions to the cloud-native FICO Platform. As part of this transformation, FICO also divested non-strategic businesses such as its Cyber Risk Score (2020), Collections and Recovery (2021), and Siron compliance (2023).

This focus on cloud-based software has set the stage for FICO’s future growth, with Annual Recurring Revenue (ARR) from platform-specific offerings growing at over 30% annually.

To align its operations with the new platform-first strategy, FICO merged its Applications and Decision Management Software segments into a unified Software segment in 2021.

This consolidation aimed to streamline operations and improve the company’s focus on its evolving cloud-based platform. In 2022, Stephanie Covert was appointed as the first leader of the newly unified software group, bringing fresh leadership to an increasingly complex and global business.

Challenges and Strategic Controversies

The 2008–2009 financial crisis was a difficult period for FICO, as lenders pulled back on extending credit in the wake of the housing crash. This resulted in a nearly 27% drop in Scores revenue, highlighting the company’s sensitivity to economic downturns. However, FICO’s adaptability and position in the credit risk ecosystem allowed it to rebound in the years following the crisis.

In 2022, the Federal Housing Finance Agency (FHFA) approved the use of VantageScore 4.0 for GSE mortgages, ending FICO’s long-standing monopoly on GSE-originated loans.

This regulatory change, which introduced a “Lender Choice” model, has posed a significant challenge to FICO’s traditional business model. The company has responded by promoting its more predictive FICO 10T model and introducing the Mortgage Direct License Program in 2025 to circumvent traditional credit bureau distribution channels.

FICO’s pricing model has come under increasing scrutiny in recent years. The company’s aggressive price hikes and “transmission fees” – charges imposed on credit bureaus for delivering FICO scores – have led to legal battles, including the ongoing “In re FICO Antitrust Litigation.” Additionally, U.S. lawmakers have raised concerns about potential price gouging in the mortgage market. These legal and regulatory challenges could pose risks to FICO’s growth and profitability.

There’s, of course, more to all of this, and we will discuss the FHFA’s shift and the risk it presents to FICO in depth in part 5 (risks).

Finally, FICO has faced criticism for its models, which some argue may disadvantage groups with limited credit histories. In response, the company has focused on broadening financial inclusion by investing more than 50% of its Scores R&D into products designed to include individuals with limited credit history, such as UltraFICO and FICO Score XD.

1.2. Product

FICO, a leader in credit risk management, operates through two primary reportable segments:

Scores and

Software

Both of which can be further subdivided.

These segments, though distinct, are deeply interconnected, with each contributing significantly to the company’s overall growth and profitability.

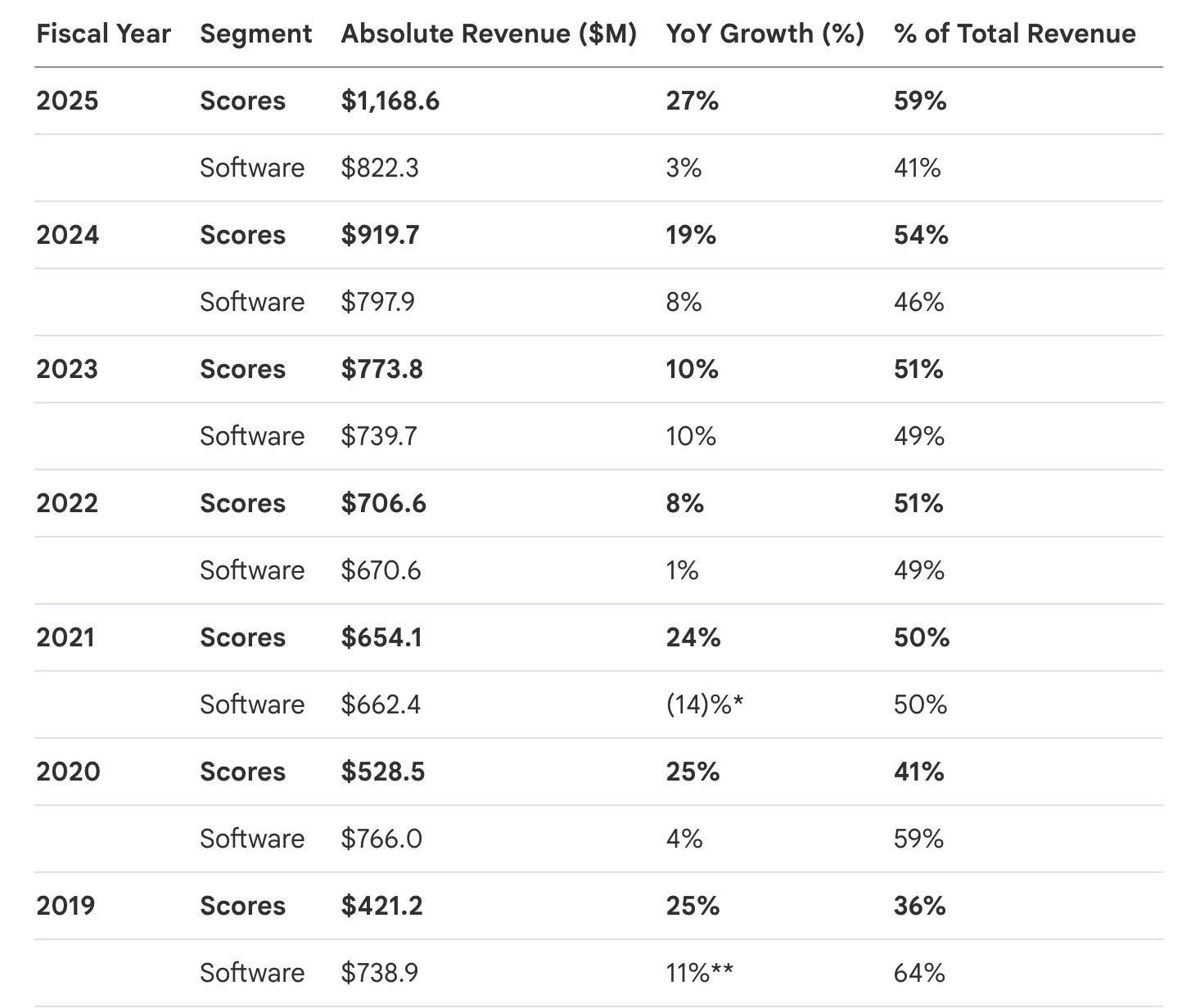

Below you find the overall revenue contribution of each segment for the last seven fiscal years and the respective YoY growth rates.

Let’s explore the products and services FICO offers, and how they stand out in a competitive market.

The full analysis starts here:

The rest of this post and the follow-up parts of this deep dive series will cover the topics outlined in the table of contents displayed in the introduction. If you’re serious about sharpening your investing edge, the full post (and all my previous premium content, including valuation spreadsheets, deep dives (e.g. well-known mid- and large caps such as LVMH, Duolingo, Meta, Edenred as well as more hidden gems such as Tiger Brokers, Digital Ocean, Ashtead Technologies, InPost, Timee, and MANY more) and powerful investing frameworks. is just a click away. Upgrade your subscription, support my work, and keep learning.

Annual members also get access to my private WhatsApp groups – daily discussions with like-minded investors, analysis feedback, and direct access to me.

PS: Using the app on iOS? Apple doesn’t allow in-app subscriptions without a big fee. To keep things fair and pay a lower subscription price, I recommend just heading to the site in your browser (desktop or mobile) to subscribe.