There was a period, not so long ago, when you couldn’t scroll through Fintwit without tripping over the stock of Dino Polska.

Somewhere between 2020 and 2024, this obscure Polish grocer chain became something of a cult stock among a certain type of quality-compounder investor, the kind who quotes Nick Sleep (“the Costco of Poland”) and gets genuinely excited about high return on invested capital coupled with high reinvestment rates.

And for good reason!

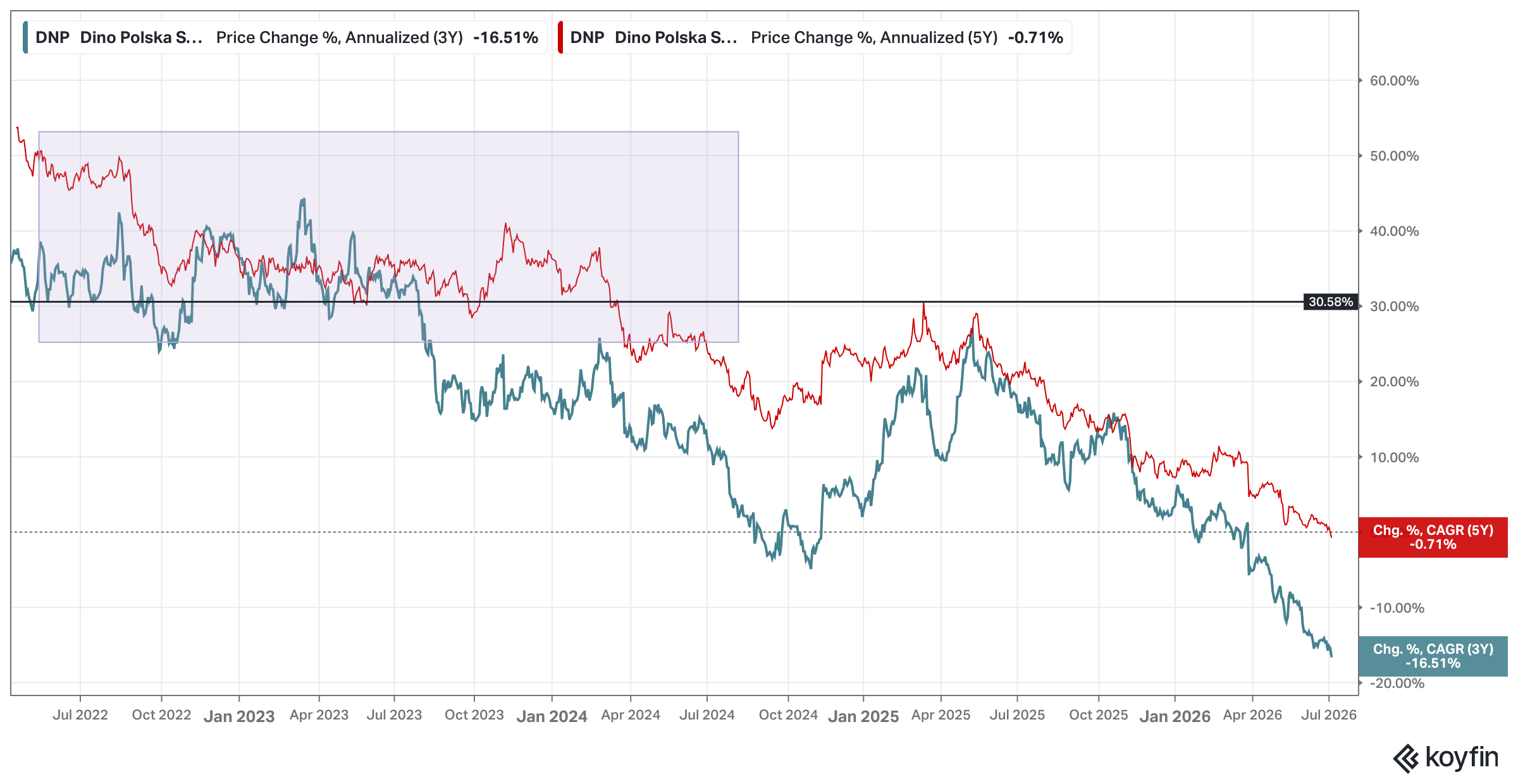

The stock had compounded at a pace that made most European retailers look like they were standing still (Dino posted a 5-year CAGR of 30%+ in the market area in the chart below; and a >50% 5Y CAGR in 2022).

Moreover, the “compounder investor” himself, Chris Mayer, owned it too. What could go wrong?

Well, then, quietly, the conversation moved on. New themes came along, the stock stopped performing, AI ate the discourse, and Dino slipped out of the group chats it once dominated.

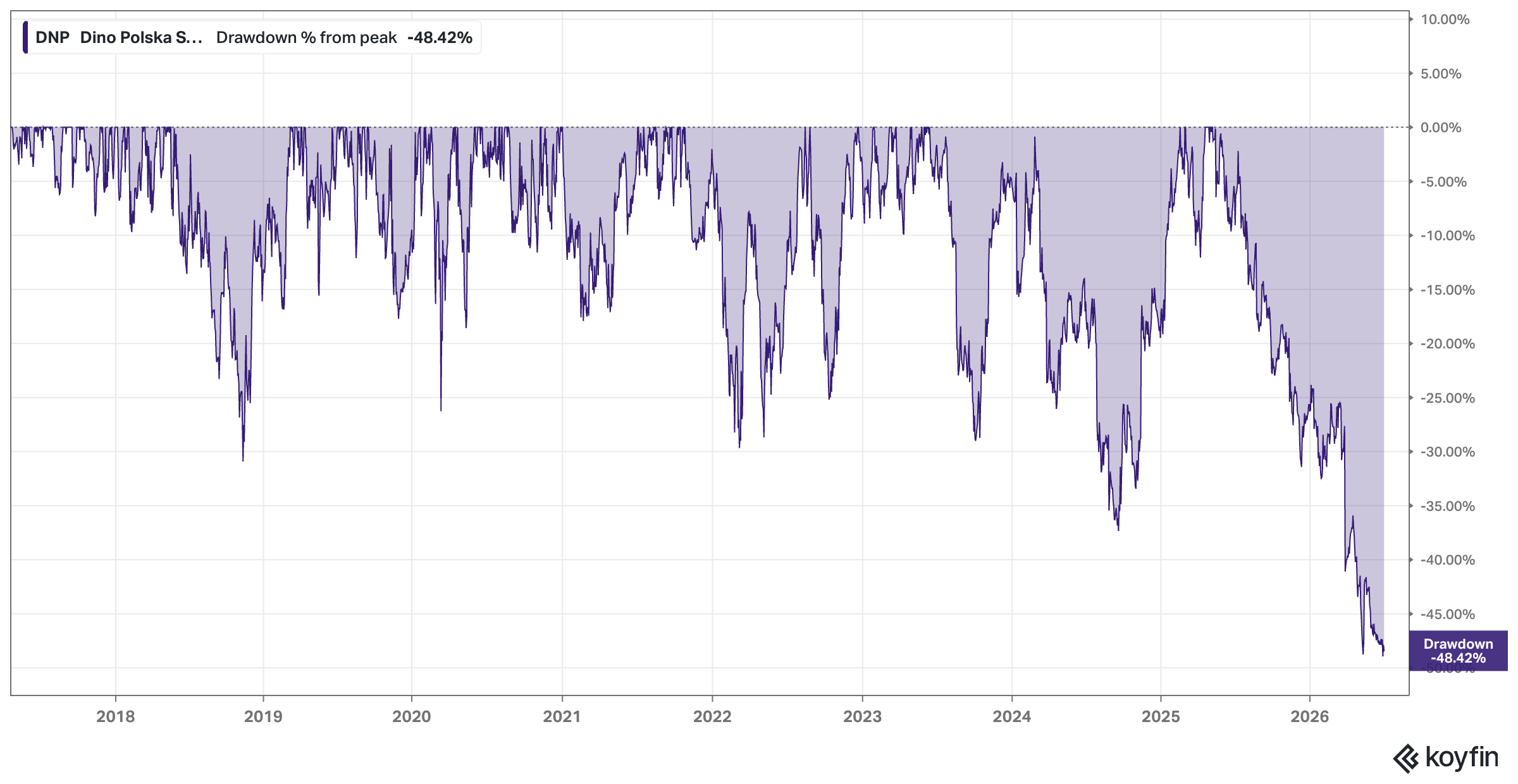

Fast forward to today, and I haven’t seen the ticker of DNP 0.00%↑ in months! Unsurprisingly, we have now reached NEGATIVE 5-year CAGR territory.

Who would’ve guessed? And that’s arguably exactly the time when you should start looking!

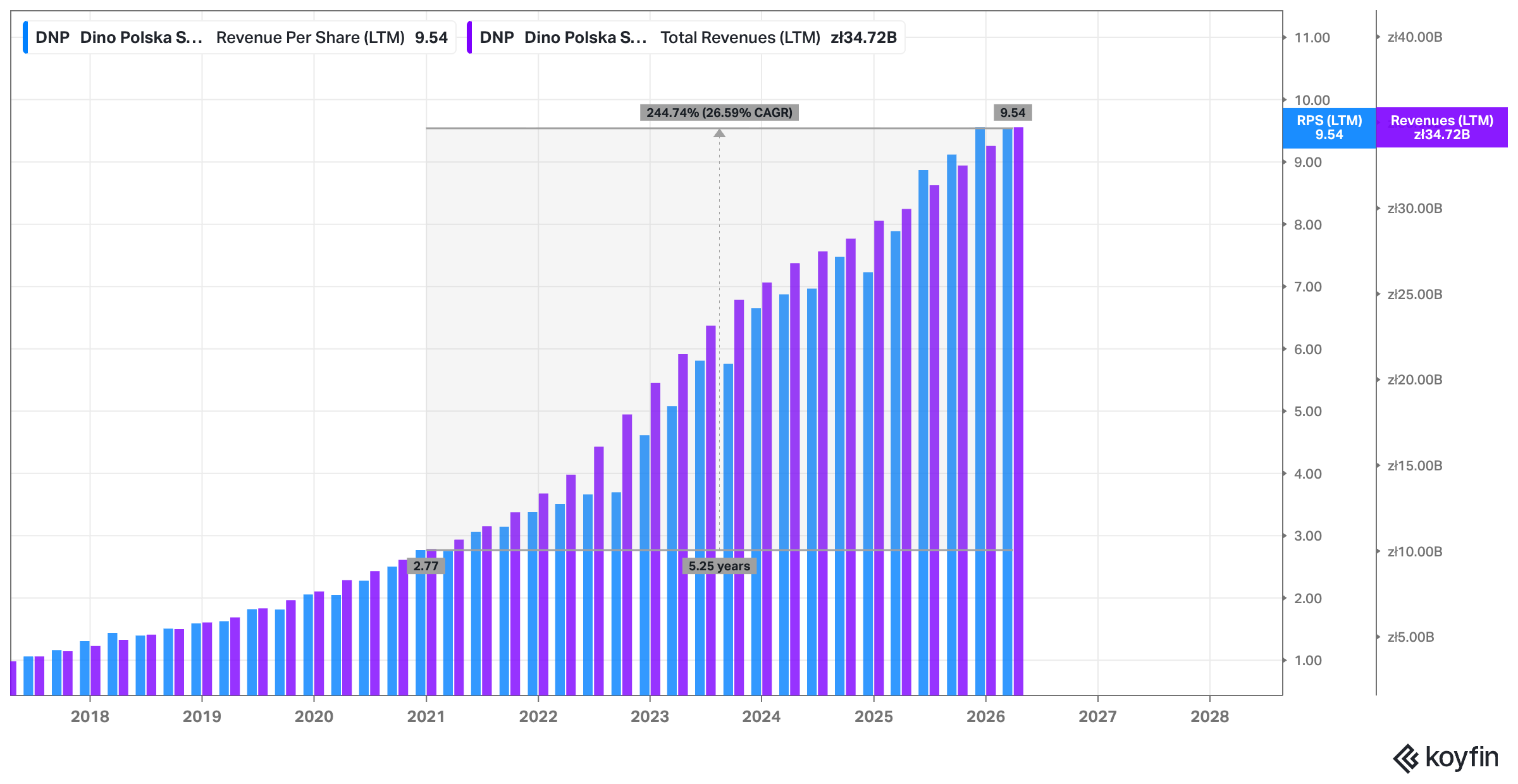

Look at the five-year chart above, and Dino Polska is sitting below where it traded half a decade ago, despite revenue more than doubling over that same stretch and the company opening more than a thousand new stores.

That’s not a typo, and it’s not a broken business either, as I’ll get into.

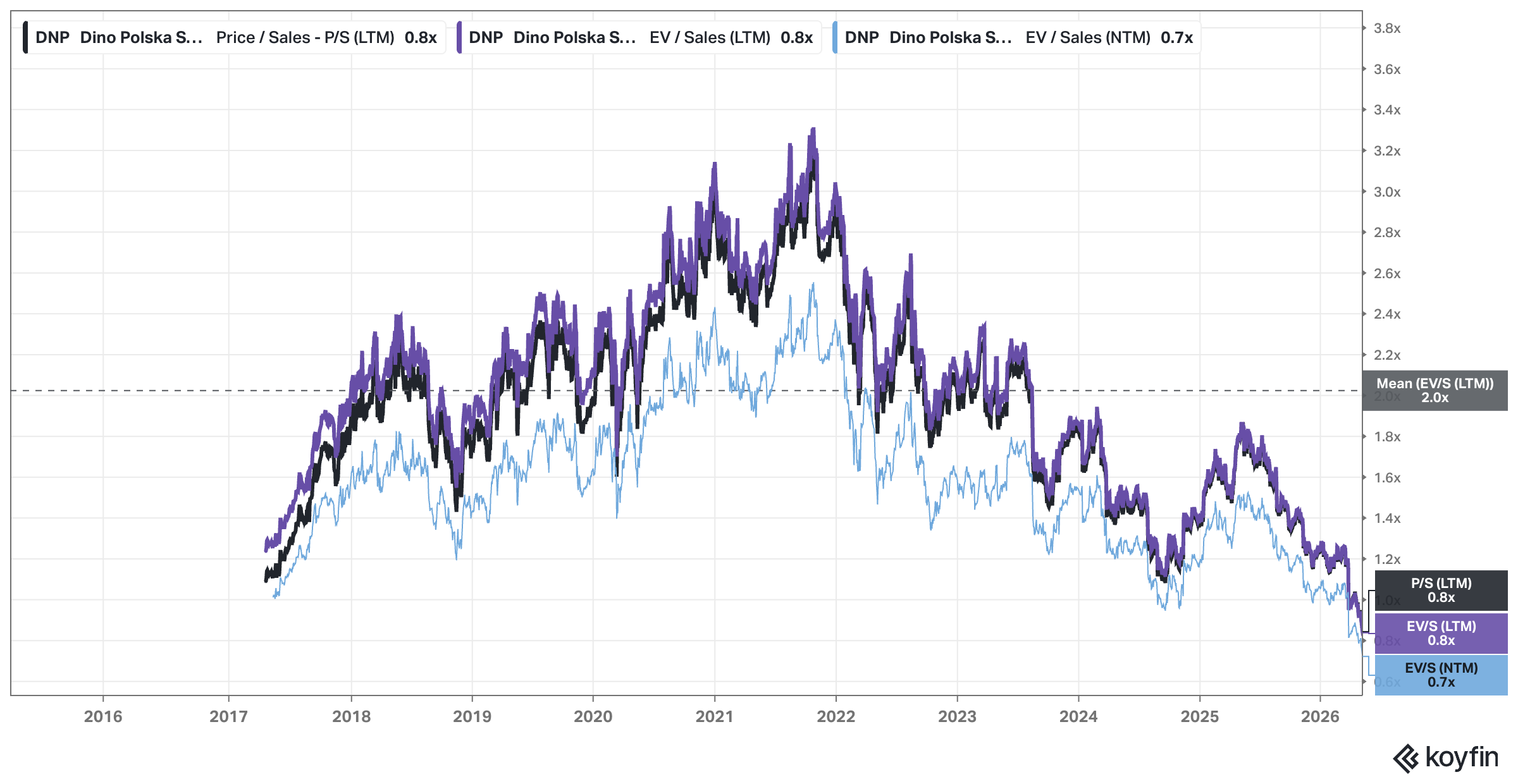

It’s a business that kept executing while its valuation multiple quietly got more than cut in half, and its stock price got dragged along with it. The chart of Dino’s forward sales multiple, sliding from a growth-stock premium down to something that now looks, frankly, cheap for a company still opening a store almost every single day.

So what happened? The short version, which I’ll unpack properly in this piece, is a genuinely nasty collision of a Polish price war, an unexpected swing into food deflation, and a minimum wage hike shock that together squeezed margins hard enough to spook a market that had gotten used to Dino only ever surprising to the upside and has shifted its focus to more exciting sectors anyhow.

The stock is down roughly 50% from recent highs, and value investors love nothing more than a good business having a bad quarter. Or in this case, a bad year and a half.

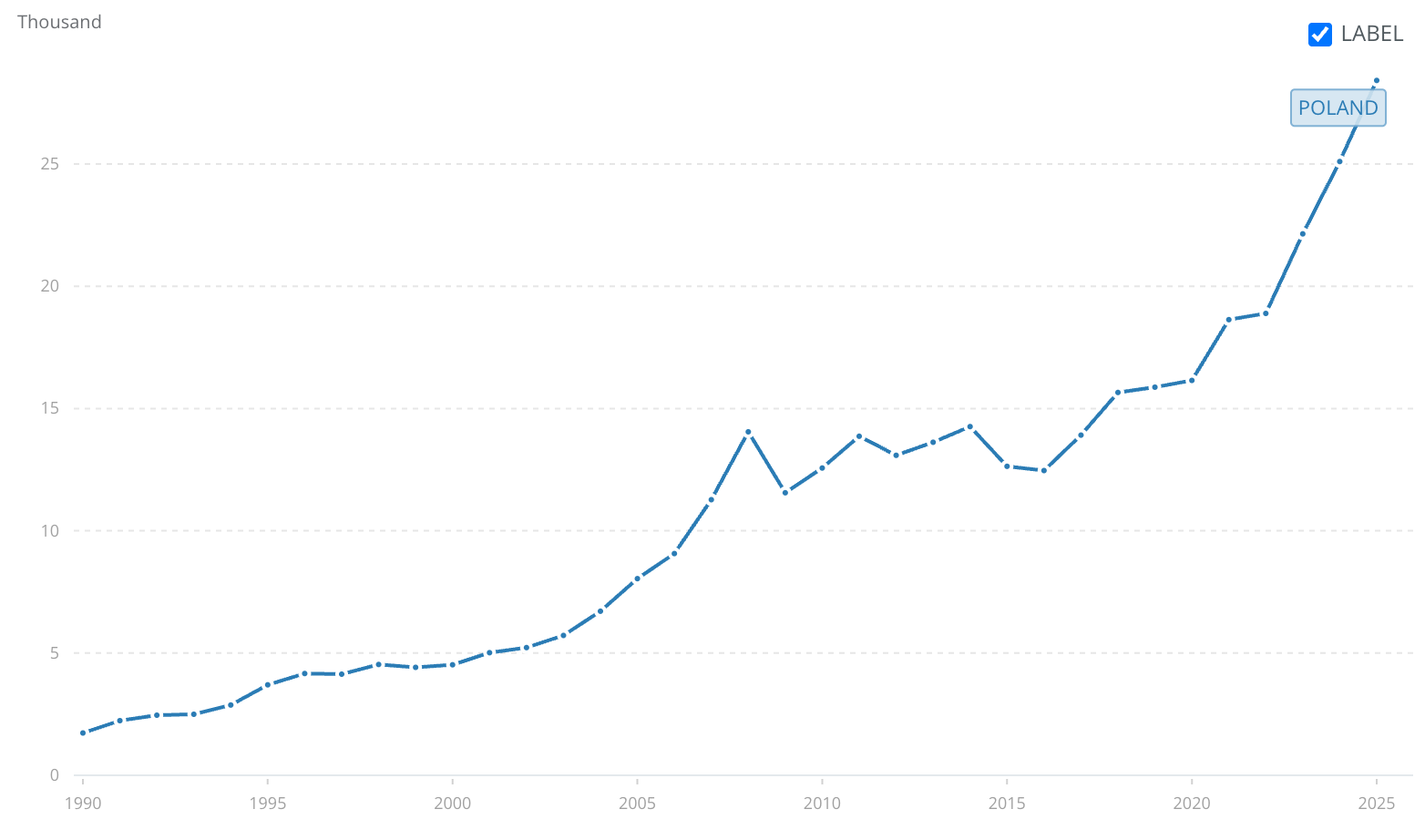

But here’s where it gets genuinely interesting, and it’s worth zooming out from the income statement for a second. This selloff is happening at the exact moment Poland itself is having something of a coming-out party on the global economic stage. Poland has now closed to within roughly 87 percent of UK per-capita income on a purchasing power basis, having already overtaken Spain, and government projections suggest full parity with the UK within five or six years.

“The entire world is looking at Poland, Polish companies, and Polish entrepreneurs. In five years, we will catch up with Great Britain.” - Prime Minister Donald Tusk

Some individual Polish regions, Warsaw’s metro area among them, already post GDP per capita figures that rival parts of Western Europe outright.

This is not the Poland of two decades ago, viewed as a cheap, catch-up economy on Europe’s periphery. It’s becoming one of the more legitimately dynamic consumer markets on the continent, and Dino has built its entire empire serving the 80 percent of that population most economists and journalists never bother writing about.

And then there’s Tomasz Biernacki, who might be the strangest, most quietly compelling founder story I’ve come across in a while. A man who controls 51% of a multi-billion-euro public company (about 7 billion € to be more precise), has never sold a single share, draws a salary of exactly zero, and reportedly didn’t even bother showing up to his own company’s IPO in 2017.

There are essentially no public photos of him. No interviews. He’s said to shop anonymously in his own stores just to see what the customer experience actually feels like, which is either an eccentric habit or the single best piece of due diligence a controlling shareholder can do, depending on how you want to look at it.

I’ll dig into what this level of founder alignment, or perhaps founder strangeness, actually means for minority shareholders later in this piece, because it cuts both ways and deserves an honest look rather than blind hero worship.

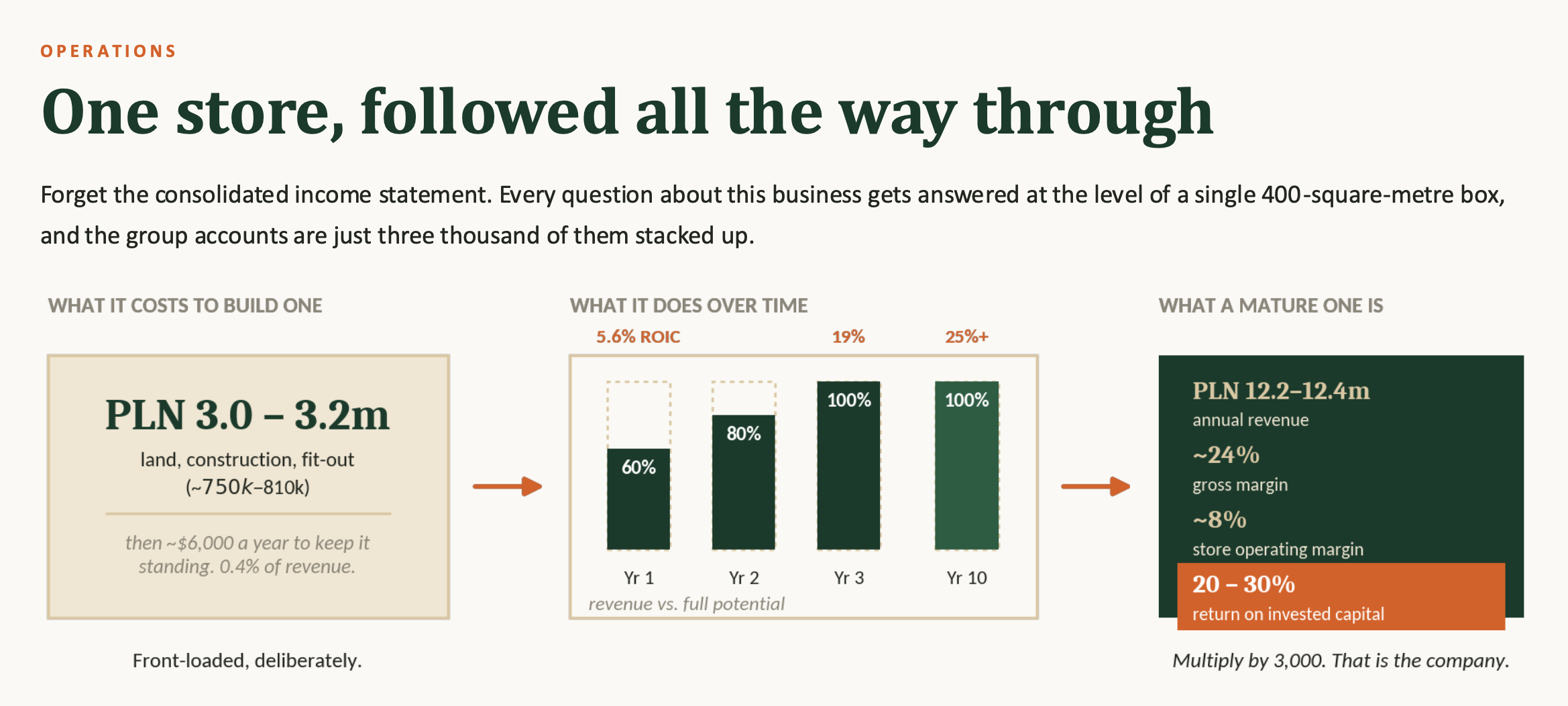

What I want to do in this deep dive is pull apart exactly what makes this business tick, and then stress-test whether the recent stock price weakness represents a genuine opportunity or a warning the market is right to heed. Because underneath the price war headlines sits a company that opened 345 new stores in 2025 alone – nearly one a day – using an internal construction arm to build identical 400-square-meter stores it also owns outright, eliminating rent as a cost line entirely across 95 percent of its footprint. It’s a company that’s turned its own rooftops into one of the largest private solar networks in Poland, that still runs a staffed butcher counter in every single location because Polish shoppers actually care about that, and that has, by some counts, a theoretical runway to more than triple its current store count before it even approaches saturation.

Whether all of that is enough to justify getting excited about a stock the market seems to have quietly forgotten is exactly what the rest of this piece sets out to answer.

What we cover in this deep dive:

The five-part bull case (”Bam Bam Bam Bam Bam”)

What went wrong?

Investment Slide Deck – the deep dive in a highly compressed + visualized form

Something NEW! Starting with this piece: every deep dive now comes with a companion slide deck. It’s the whole argument in compressed form – the hypothesis, the business, the competitive position, the valuation, and the case against – for the days when you don’t have an hour to spare but still want the shape of the thing. Paid subscribers get both, the long piece and the deck, on every deep dive from here on.

The origin story – from a single Krotoszyn supermarket to a national “execution machine”

The business itself – what Dino actually sells, and to whom

How the money actually gets made – segments, revenue model, and the negative working capital flywheel

Unit economics analysis – what a single 400-square-meter store actually earns

The moat – ownership, standardization, and the geographic monopoly effect

The customer – who they are, why they keep coming back, and whether this business can become a cult

Legal structure, cyclicality, and operating leverage

Is it a good business in a good industry – base rates, competitive landscape, and long-term survivability

Growth drivers and forecasting – breaking five-year revenue growth into its component parts

Margin outlook – where operating and net income margins likely settle over the next decade

Management and governance – the reclusive founder, zero-salary alignment, and the related-party question

A replacement value perspective – what it would actually cost to rebuild this network from scratch

Valuation (including a downloadable model)

Disclaimer:

As of the date of publication the author owns no shares in the company; but that may change. The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

High-Level Thesis: “Bam Bam Bam Bam Bam”-90 Second-Hypothesis

As always, I start by referring to Bill Miller, who had a theory about pitching stocks. The way pitch them. And it was about attention. Portfolio managers, he observed, have almost none of it. Ninety seconds, and you’ve either made your case or you haven’t. Miller’s fix was brutally simple: state the price, state what you think it’s worth, give five reasons why, done. No preamble. No hedging. Just the case.

I want to try that here, applied to Dino Polska (WSE: DNP), although admittedly, in my latest format, I’ve certainly extended the 90 seconds by quite a bit. But I try to stick to his “Bam Bam Bam Bam Bam” framework.

Why This Stock Now?

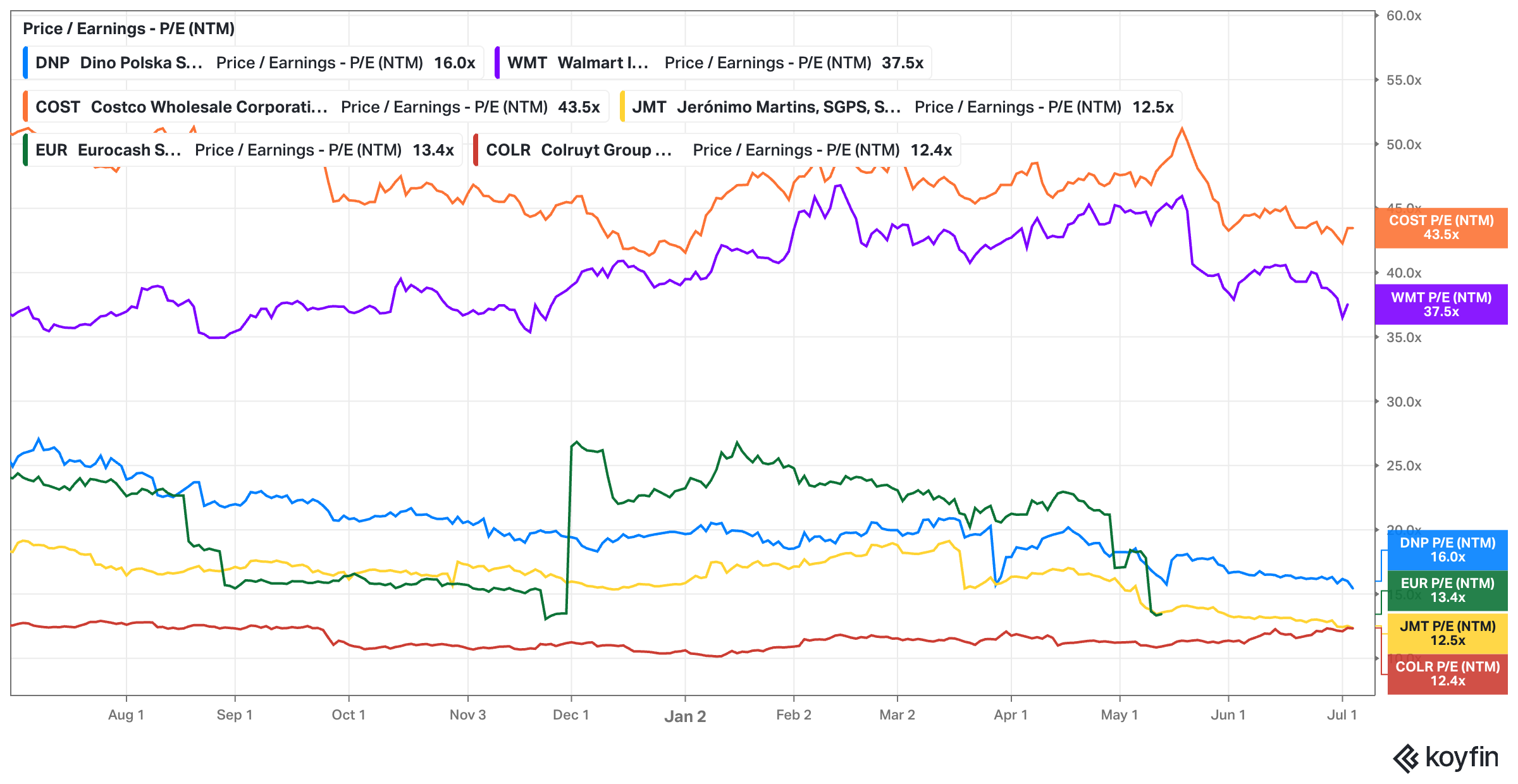

The stock of Dino Polska trades at roughly 16x forward earnings right now. Compare that to Costco at 43x, or Walmart at 38x. Poland-focused peers trade at similar multiples, though.

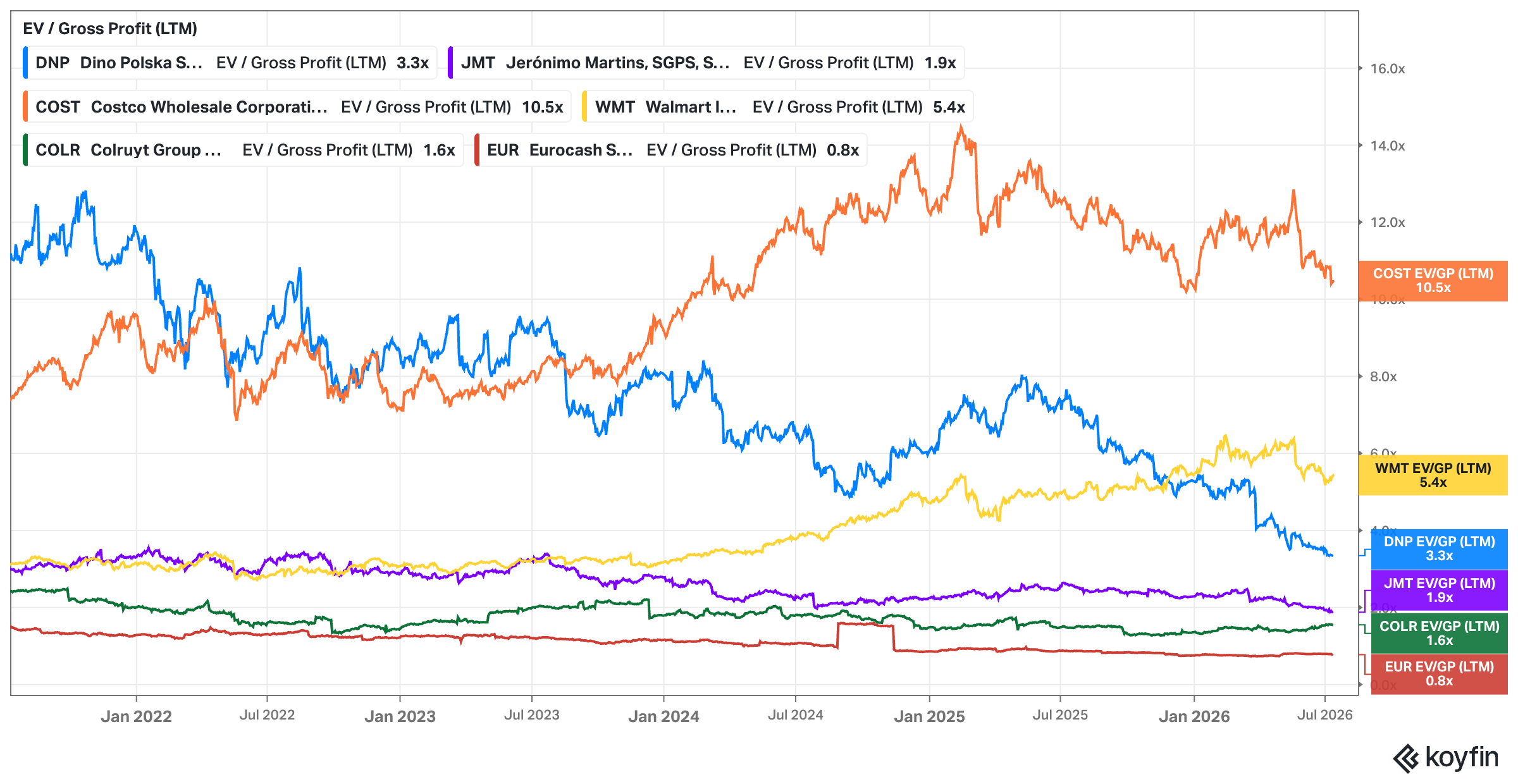

The gross profit multiples currently look like this:

That gap alone should make you pause. A Polish grocer growing faster than either of those two, priced at less than half their multiple. The pitch, stripped down to its essence, is that simple. And that’s exactly the kind of gap that either means the market knows something you don’t, or the market has temporarily stopped paying attention to something important. Figuring out which one it is – that’s the whole game.

Now, going into this research, my first hunch right now as I type this, before I did any real digging, is a mix of skepticism and fascination.

On the one hand, it’s a proximity supermarket chain. Nothing exotic about groceries, nothing defensible on the surface, and the conventional wisdom on retail is that returns are generally mediocre unless you can carve out real protection at one end of the spectrum or the other. Luxury works, because scarcity and brand equity let you charge good prices. Discount works, if you can achieve genuine scale. Everything sitting in the middle tends to get squeezed from both directions and produces the kind of forgettable, low-return businesses that litter most retail indices. Think about how brutal the base rates have been in fashion retail, in toys, in sporting goods, in department stores generally. Graveyards, most of them, littered with once-dominant names that either got outcompeted on price and never had a real moat to begin with.

But here’s my second hunch going in, and it’s the thing I actually wanted to test through this deep dive rather than assume. Not all retail is created equal, and I suspect the base rate for relatively immature grocery businesses specifically, when it’s built around a genuine scale-economies-shared model, is meaningfully better than the base rate for retail more broadly. Whether that’s actually true for Dino specifically, and to what extent the scale advantages genuinely get shared with the customer rather than just captured by the company, is exactly what the rest of this piece needs to establish rather than assume. But the pattern shows up often enough elsewhere that it’s worth taking seriously. Lowe’s and Floor & Decor built genuinely excellent businesses out of what looks like unglamorous, low-margin retail categories. Costco and Walmart, back when they were still young and small rather than the behemoths they are today, were extraordinary compounders built on exactly this kind of model. And Aldi and Lidl, even though neither is available to public shareholders, which tends to be the case with a lot of the best German business stories given the country’s thin public ownership culture, are arguably two of the most successful retail operators in the world over the past several decades.

If that pattern holds, and if Dino has actually built something structurally similar in a Polish context, then this stops looking like just another mediocre retailer and starts looking like something considerably more interesting.

That’s the question I want to actually answer here, not assume my way into.

The Investment Hypothesis, Not Thesis

One word choice matters as always. I’m deliberately calling this a hypothesis, not a thesis. A thesis is a statement of belief – something you defend, something you go looking for evidence to confirm. That’s not what I want to do here, and honestly, it’s not what good investing looks like at all. A hypothesis is different. It’s a claim built to be tested, and ideally, broken. My job through the rest of this piece isn’t to convince you I’m right. It’s to actively hunt for the data that would prove me wrong, and see whether it turns up.

So here’s the hypothesis, stated plainly:

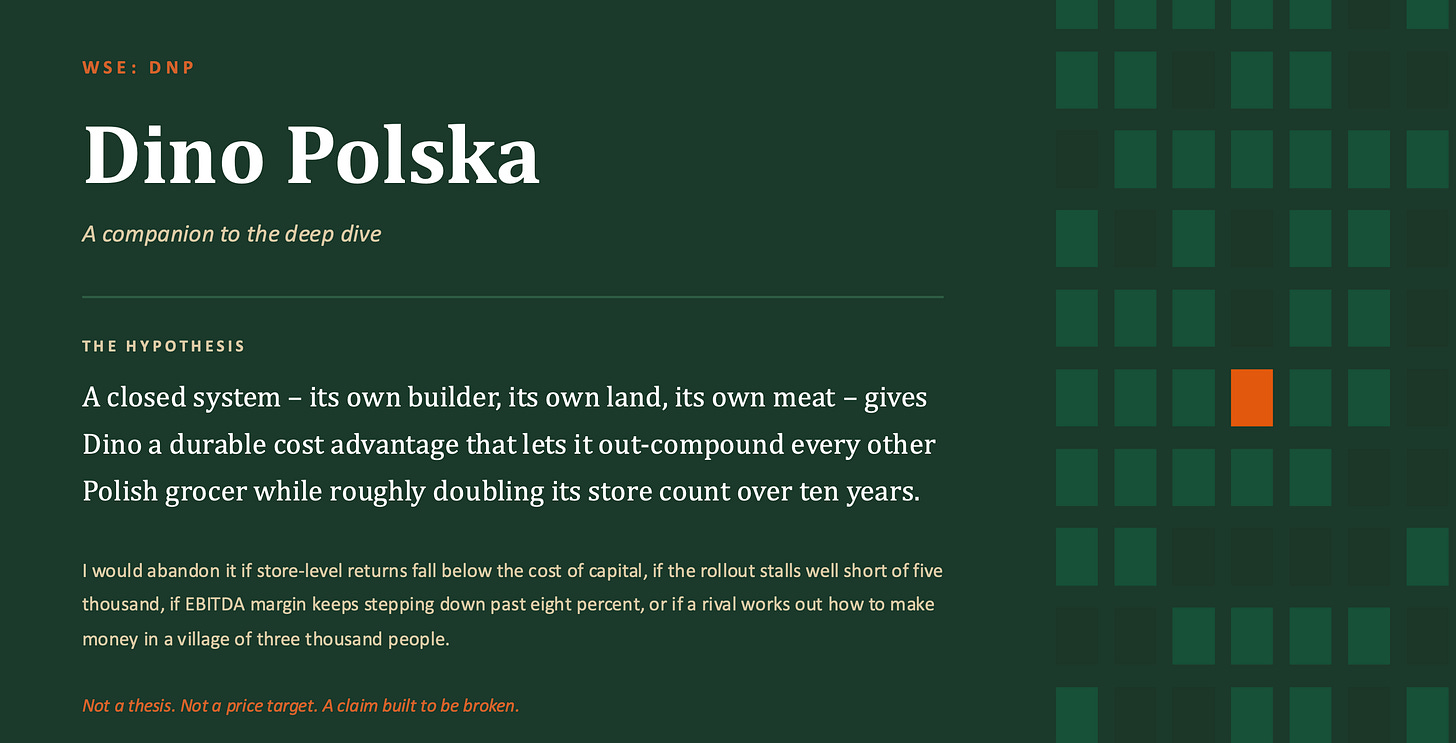

Dino Polska’s closed-system integration – internal construction, owned land, internal meat processing – gives it a durable cost advantage that will let it out-compound every other Polish grocer, while roughly doubling its store count over the next ten years.

That’s the claim. Everything that follows in this piece – the business model, the competitive moat, management quality, the balance sheet, the risks, the valuation – is really just an extended stress test of that one sentence.

Let’s start with the BAMs.

The full analysis starts here:

The rest of this post covers TAM penetration and market share dynamics, the identification of key growth drivers going forward, and two valuation approaches. If you’re serious about sharpening your investing edge, the full post (and all my previous premium content, including valuation spreadsheets, deep dives (e.g. well-known mid- and large caps such as LVMH, Duolingo, Meta, Edenred as well as more hidden gems such as Tiger Brokers, Digital Ocean, Ashtead Technologies, InPost, Timee, and MANY more) and powerful investing frameworks are just a click away. Upgrade your subscription, support my work, and keep learning.

As a member, you get:

Complete Access: Every deep dive in our library (65+ and counting).

The WhatsApp Community: Real-time discussion and networking with like-minded investors.

Digital Investing Conferences: 3-4 times a year, we also hold digital conferences where members present and share stock ideas, and discuss broader themes, and we’d love for you to join in!

Incredible Value: Full access to all of this for less than $1/day.

Reminder: Something new, starting with this piece: every deep dive now comes with a companion slide deck. It's the whole argument in compressed form – the hypothesis, the business, the competitive position, the valuation, and the case against – for the days when you don't have an hour to spare but still want the shape of the thing. Paid subscribers get both, the long piece and the deck, on every deep dive from here on.