Imagine possessing a business that effectively acts as a digital checkpoint for every major live event across Central Europe.

Think about an ecosystem so technologically hardened that its core architecture – EVENTIM.Net – can effortlessly handle over 1 million concurrent users during a high-stakes stadium tour on sale for elite artists like Taylor Swift or Ed Sheeran without breaking a sweat, a technological feat very few regional competitors can dream of replicating.

Picture a company so dominant that it has secured the prestigious Arthur Award, widely recognized as the “Oscar” of the global live entertainment industry, in the Best Ticketing Provider category.

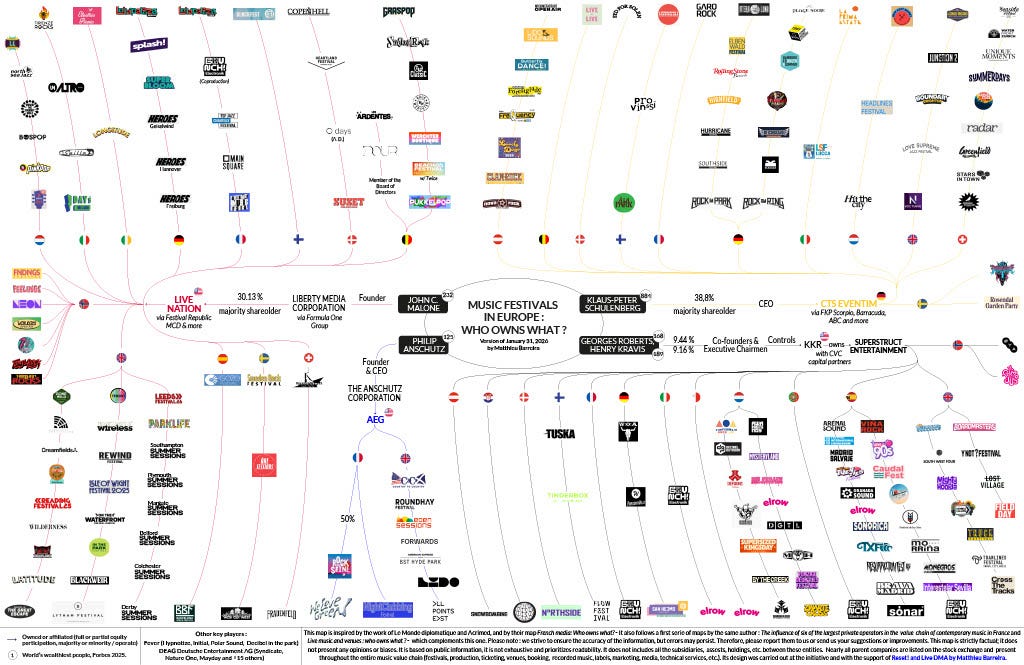

And did you know that the 200 major European festivals are owned by just four companies? (the company we cover today being one of them; the other three being Live Nation, Superstruct, and AEG)

Reset! and Live DMA recently published the map above to make the ownership of various music festivals (which historically has been rather obscure to the average consumer) more transparent and accessible to the public.

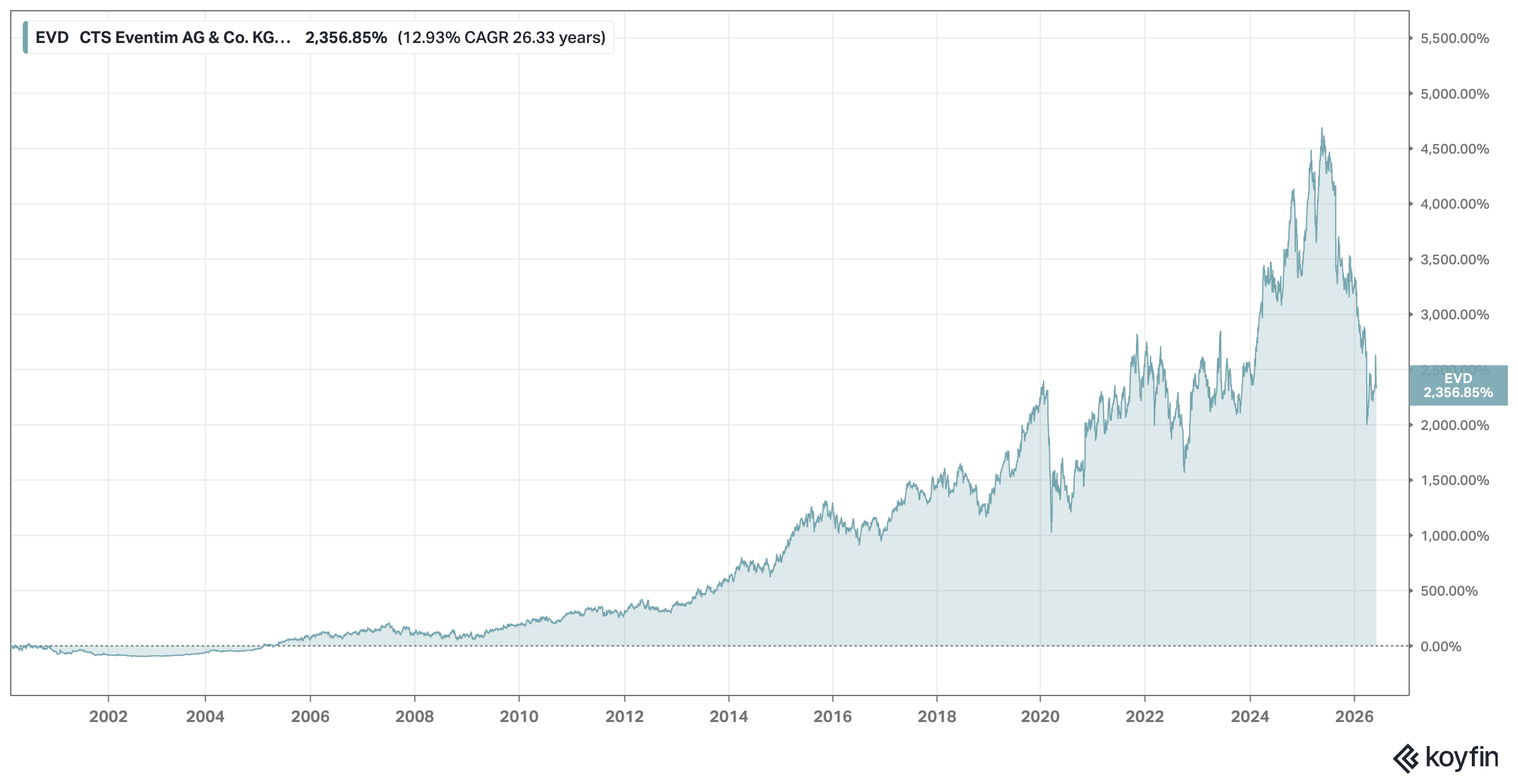

The company we will cover in this deep dive is CTS Eventim, a business that billionaire founder Klaus-Peter Schulenberg took over as a small Munich-based software firm with just 83 employees back in 1996. Since its initial public offering in February 2000, it has compounded capital to deliver a staggering 2,350% total shareholder return – amounting to a 13% annually over more than two decades (17% before the recent drop).

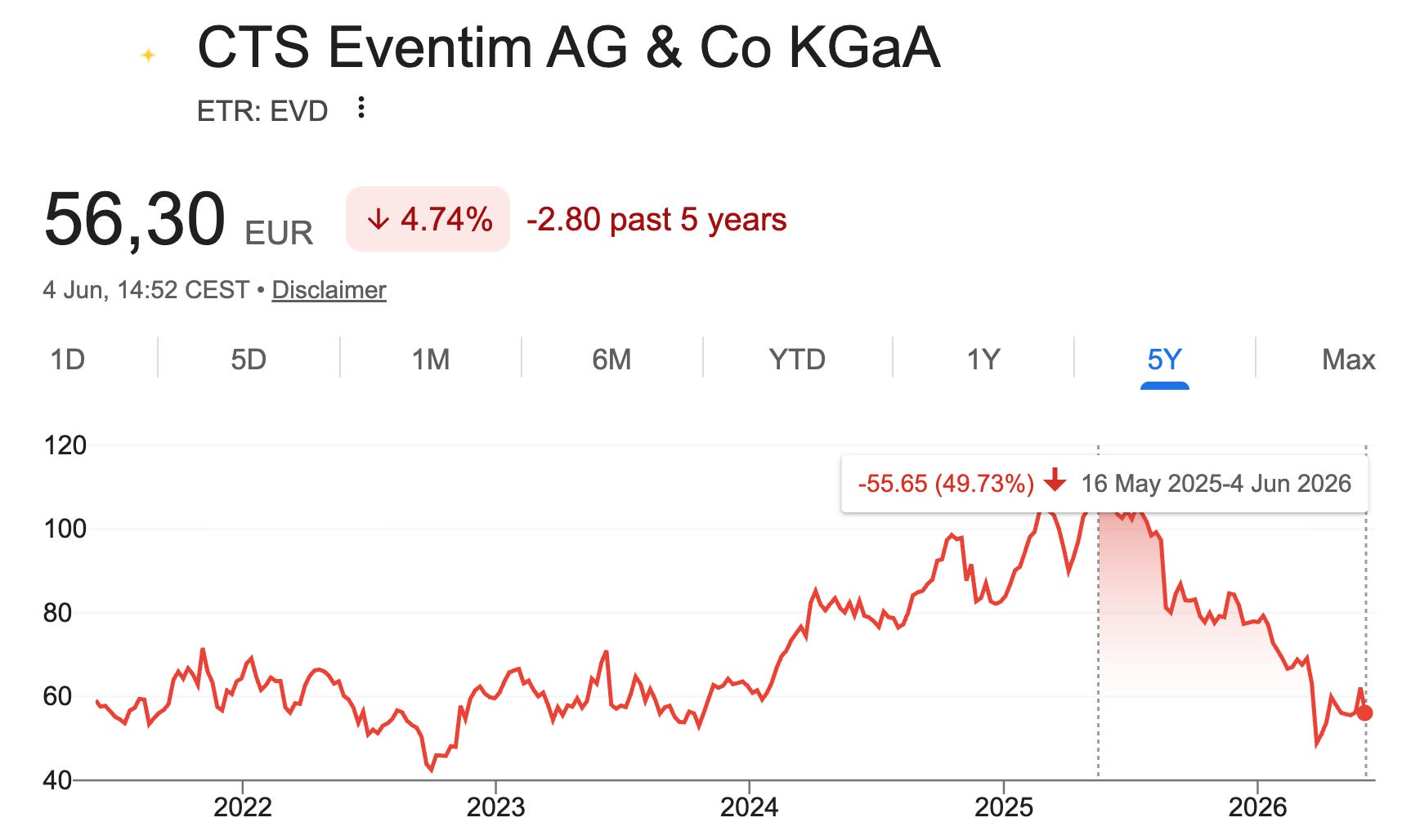

Yet, if you pull up a stock chart today (the chart above gives a clue), you will confront an entirely different emotional landscape. The equity has been practically dead money, trading completely flat to slightly down over a trailing five-year period. More shockingly, the stock has plunged roughly 50% from its absolute peak achieved only in May last year. This steep correction has caused valuation multiples to heavily compress across the board – be careful just glancing at research terminal multiples though! (for reasons we will discuss below) –, drawing immense skepticism from short-term public market analysts.

So what caused this premier long-term compounder to lose its tune?

The answer lies in a highly visible shift in corporate strategy and near-term execution headwinds, coupled with investors favoring clear “AI winners.”

The company is currently navigating a major physical infrastructure revolution, aggressively transitioning from a pure, asset-light digital software play into a heavy-capital venue powerhouse. It operates iconic spaces like the LANXESS Arena in Cologne – which Pollstar officially ranked as the third most successful entertainment arena on the planet, trailing only Madison Square Garden in New York and the SSE Hydro in Glasgow –, which Eventim has managed since 2012, alongside a rapidly growing international portfolio.

The company here follows PropCo/OpCo philosophy, which is a corporate arrangement that splits a business's real estate assets from its daily operations; PropCo owns the land and buildings, while OpCo leases the property and manages the core business.

“As you rightly mentioned, we follow a propco/opco strategy. We follow the idea and we confirm the idea of an asset-light model for the entire company. Having said this, this is work in progress, but we are in accordance with our planning. I sincerely hope more details can be shared later this year. As I mentioned in the last call and in our bilateral discussions, these are very structured or highly structured discussions and negotiations with a variety of different partners. So please rest assured we are working on this and working on this very hard. Nothing has changed that we want to keep only a minority share in propco. And in other words, we will preserve the asset-light model, but we don’t have a result yet, which can be announced at this state.“ - Q1 Call

Furthermore, it recently celebrated the opening of the Unipol Dome in Milan (the former Milan arena), which stands as Italy’s most modern arena, and secured a major contract to build a brand new 20,000-seat arena in Vienna.

“… after hosting the Olympic Ice Hockey Tournament in February with about 400,000 visitors, the Unipol Dome in Milan opened for music concerts in May this year. The Milan arena contributes, therefore, already to the operational results and is a meaningful addition to our high-margin venue portfolio.“ - Q1 FY26 Call

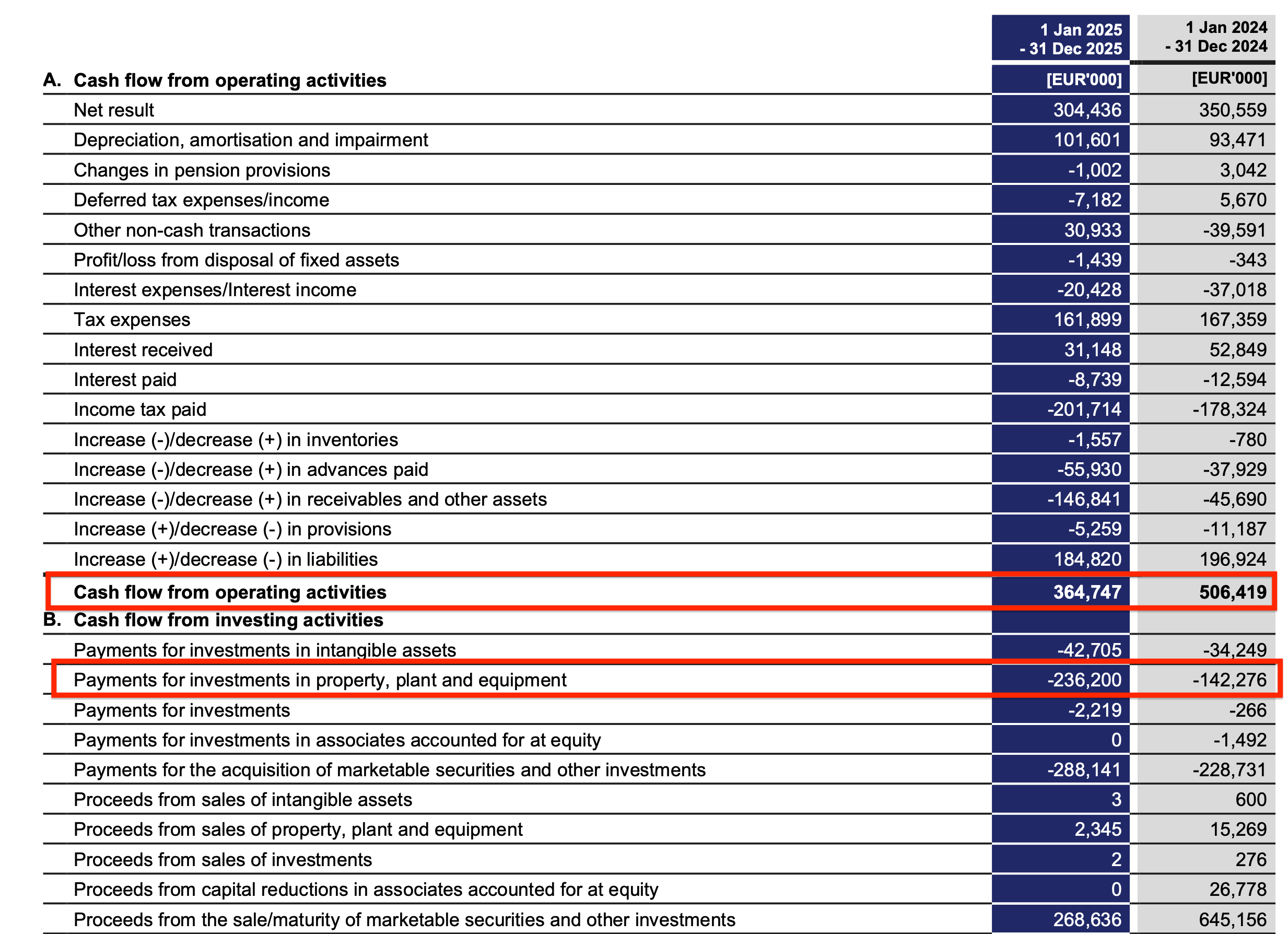

But this real estate pivot has come at a steep near-term price, hit by unexpected construction cost overruns in Milan that temporarily decimated free cash flow and induced sudden structural panic throughout the market. When CTS Eventim originally took on the project to plan, build, and operate the 16,000-capacity arena for the Milan-Cortina Winter Olympics, the total construction budget was estimated at €180 million. However, a combination of severe global inflation, skyrocketing energy prices, supply chain disruptions, and tight design modifications turned it into a financial nightmare, and the actual cost ballooned to roughly €400 million.

This tension sits at the absolute center of my core investment hypothesis. Is the market right to re-value Eventim as a lower-return, capital-heavy infrastructure play, or is it handing long-term investors a classic mispricing in a structurally competitively advantaged, recession-proof business model? Let’s not forget how this engine behaves during a broader economic crisis. During the 2008–2009 Global Financial Crisis, while traditional industrial sectors faced absolute ruin, Eventim’s ticketing revenues surged by 29%, proving that modern consumers stubbornly prioritize experiences over material goods.

In this comprehensive deep dive, I will break down the underlying mechanics of Eventim’s vertically integrated flywheel, evaluate the hidden risks of its venue expansion, audit its balance sheet strength, and dissect the valuation disconnect to determine whether this live entertainment monopoly represents a compelling asymmetric opportunity for patient, long-term capital.

Disclaimer: I bought shares of CTS Eventim for my parent’s portfolio. The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.

High-Level Thesis: “Bam Bam Bam Bam Bam”-90 Second-Hypothesis

As my regular readers know, if you spend any time presenting investment ideas to portfolio managers, you quickly realize they have ultra-short attention spans. Bill Miller always used to emphasize that no successful fund manager wants to hear a story longer than 90 seconds. Miller’s advice was simple: give them the ticker, the current price, the valuation anchor, and then hit them with five immediate, hard-hitting reasons. Bam. Bam. Bam. Bam. Bam.

That is exactly how I want to look at CTS Eventim. Well, I ended up putting together eight BAMs. Close enough.

Let’s look at the baseline. The stock is currently trading around €56. It has carved out a 52-week range between roughly €49 and €111, pulled down heavily after management issued a cautious outlook in late March that spooked short-term traders.

CTS Eventim’s stock plummeted by up to 21% following its March 26, 2026, annual report because unexpected future headwinds completely overshadowed record-breaking 2025 revenues. The primary shock to investors was a stagnant outlook for 2026, with management guiding for flat-to-minor profit growth that fell drastically short of the increase analysts expected.

“With this in mind, we guide for 2026. In ticketing, we expect all KPIs on previous year level, respectively, slightly higher. In Live Entertainment, we expect moderate growth in adjusted EBITDA and EBIT, whereas the revenues are expected to reach prior year level. Finally, we expect Eventim Group level KPIs on or slightly higher level than previous year. CTS Eventim has a consistent track record of returning value to its shareholders.“ - Q4 Call

This growth slowdown was further compounded by the disclosure of a major structural ticketing contract expiration with Stage Entertainment, leaving a revenue gap the company must now work to fill.

“Finally, let's have a look at our 2026 guidance and our new capital market communication approach. […] Eventim will stay a growth asset for the years to come, even though our 2026 budget needs to compensate for a onetime effect in form of a structural income change from a long-term contract. We have set ourselves ambitious midterm targets in both our segments and on group level.” - Q4 Call

However, treating this as a total loss of the Stage Entertainment relationship misses a critical nuance. On April 20, 2026, CTS Eventim, in fact, announced an extension of their retail ticketing partnership across Germany, France, Spain, and the Netherlands.

So the “structural income change” management warned about in March likely stems from Stage Entertainment insourcing its core, backend white-label software infrastructure. However, Stage Entertainment cannot easily replicate Eventim’s massive consumer-facing distribution network. By maintaining the retail relationship, Eventim protects its high-margin transaction fee volumes on the actual point of sale, mitigating a portion of the feared revenue cliff.

Furthermore, investors were deeply rattled by a massive drain on the company’s liquidity. The final construction costs for the newly opened Unipol Dome in Milan more than doubled from an initial €180 million budget to nearly €400 million, according to a Barclays research note. This aggressive capital expenditure caused full-year free cash flow to drop significantly, and “Cash and cash equivalents decreased by EUR 162,889 thousand compared to 31 December 2024. Cash and cash equivalents decreased, inter alia, due to the higher investments in property, plant and equipment […].“

But if you look past the temporary headwinds and noise, the core compounding machine seems completely intact.

Before listing the core pillars, I want to clarify how I approach this setup. I am intentionally calling this an investment hypothesis rather than a thesis. To me, a thesis implies a static statement of belief, which naturally tempts an investor to search for confirmatory data. A hypothesis is something you actively try to falsify. You test the edges, look for structural cracks, and remain objective. My core hypothesis here is that the market is currently over-indexing on temporary venue cost overruns and a conservative near-term corporate outlook, entirely missing a structural, vertically integrated monopoly that is exporting its elite unit economics globally.

The full story starts here:

The rest of this post covers the full analysis. If you’re serious about sharpening your investing edge, the full post (and all my previous premium content, including valuation spreadsheets, deep dives (e.g. well-known mid- and large caps such as LVMH, Duolingo, Meta, Edenred as well as more hidden gems such as Tiger Brokers, Digital Ocean, Ashtead Technologies, InPost, Timee, and MANY more) and powerful investing frameworks are just a click away. Upgrade your subscription, support my work, and keep learning.

As a member, you get:

Complete Access: Every deep dive in our library (65+ and counting).

The WhatsApp Community: Real-time discussion and networking with like-minded investors.

Digital Investing Conferences: 3-4 times a year, we also hold digital conferences where members present and share stock ideas, and discuss broader themes, and we’d love for you to join in!

Incredible Value: Full access to all of this for less than $1/day.

PS: Using the app on iOS? Apple doesn’t allow in-app subscriptions without a big fee. To keep things fair and pay a lower subscription price, I recommend just heading to the site in your browser (desktop or mobile) to subscribe.