Earnings Review: Brockhaus Technologies ($BKHT)

Big Update, Zero Headlines & Shareholder Pressure Mounts: Why Brockhaus Might Be at a Turning Point

Right now, the Tour de France is airing, and with it, road cycling is having one of its few annual moments in the mainstream spotlight. Jerseys, breakaways, mountain stages, and time trials are back in people’s feeds, conversations, and living rooms (I’ve somehow managed to train my X feed to display more bike racing content and less MAGA-related nonsense). Even casual observers can’t help but notice the spectacle – and for those of us following the bike leasing space, one name pops up more than once: Visma Lease a Bike, one of the race’s most prominent and well-funded teams. It’s a subtle reminder that leasing has entered the cultural and commercial foreground.

That visibility stands in sharp contrast to what’s happening at Brockhaus Technologies, the listed holding company that owns a large stake in Bikeleasing – the firm at the heart of this update. While the bikes are out racing and the logos are flashing across screens, Brockhaus itself has been... quiet. Too quiet. No press release. No public celebration of the most significant business model change in years. Just silence – and a lot of potential waiting to be unlocked.

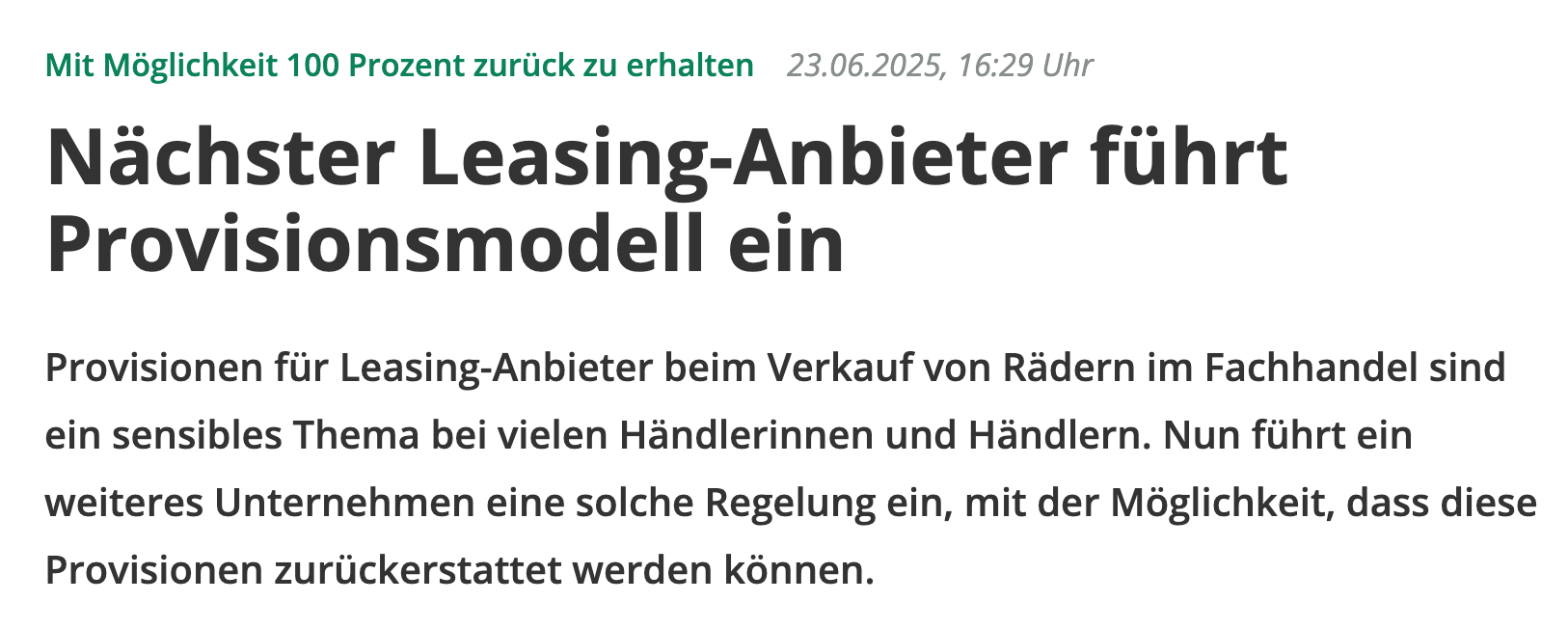

For those not following closely, the most significant update isn’t even something Brockhaus itself announced. No press release. No investor update. Just a quiet change that first surfaced in a German niche magazine, hinting at a new fee model that could alter the unit economics of Bikeleasing going forward. It’s the kind of thing that, while small on paper, can have ripple effects throughout a thesis – especially when the holding company is this concentrated.

But the fee change is just one part of the story. Over the past few weeks, I’ve been reflecting on the entire Brockhaus investment case again – it’s, of course, a continuous process) –, the moat dynamics, the market backdrop, the management strategy, and the valuation trap that has frustrated investors for far too long. Along the way, I’ve also been tracking what other shareholders like Paladin Asset Management have been saying in their most recent update from this week; their most recent letter brought up some provocative options to unlock value that are well worth unpacking.

This post is my attempt to bring it all together – not just as a surface-level update, but as a deep dive for investors who want to understand what’s really going on with Brockhaus Technologies beneath the hood.

Here’s what I’ll cover:

What the new bike retailer fee model actually is, how it works, and what it could mean for Bikeleasing’s economics

Why this change shifts the narrative around differentiation – and why I don’t think it’s a big deal

How online partnerships and “digital shelf space” could be forming a new type of moat in the industry

What the broader industry data says about demand, pricing, inventory levels, and macro tailwinds

A close look at Paladin’s proposed strategies to close the valuation gap – and my take on each one

Why Brockhaus’s lack of acquisitions is both understandable and frustrating, and how it compares to “real” serial acquirers

The role of communication and complexity in suppressing the stock’s valuation, and what might change that

Smaller updates and signals: executive departures, branding visibility, and why I think something might be brewing behind the scenes

Ultimately, why I’m still holding, what I’m watching next, and where I think this story could go

The full update starts here:

The rest of this post covers the content outlined above. If you’re serious about sharpening your investing edge, the full post (and all my previous premium content) is just a click away. Upgrade your subscription, support my work, and keep learning.

Disclaimer: I do own Brockhaus shares. The analysis presented in this blog may be flawed and/or critical information may have been overlooked. The content provided should be considered an educational resource and should not be construed as individualized investment advice, nor as a recommendation to buy or sell specific securities. I may own some of the securities discussed. The stocks, funds, and assets discussed are examples only and may not be appropriate for your individual circumstances. It is the responsibility of the reader to do their own due diligence before investing in any index fund, ETF, asset, or stock mentioned or before making any sell decisions. Also double-check if the comments made are accurate. You should always consult with a financial advisor before purchasing a specific stock and making decisions regarding your portfolio.