Deep Dive: Revisiting CMG ($CMG)

Thoughts on the New M&A Framework, Intensifying Competition & CMG's TAM

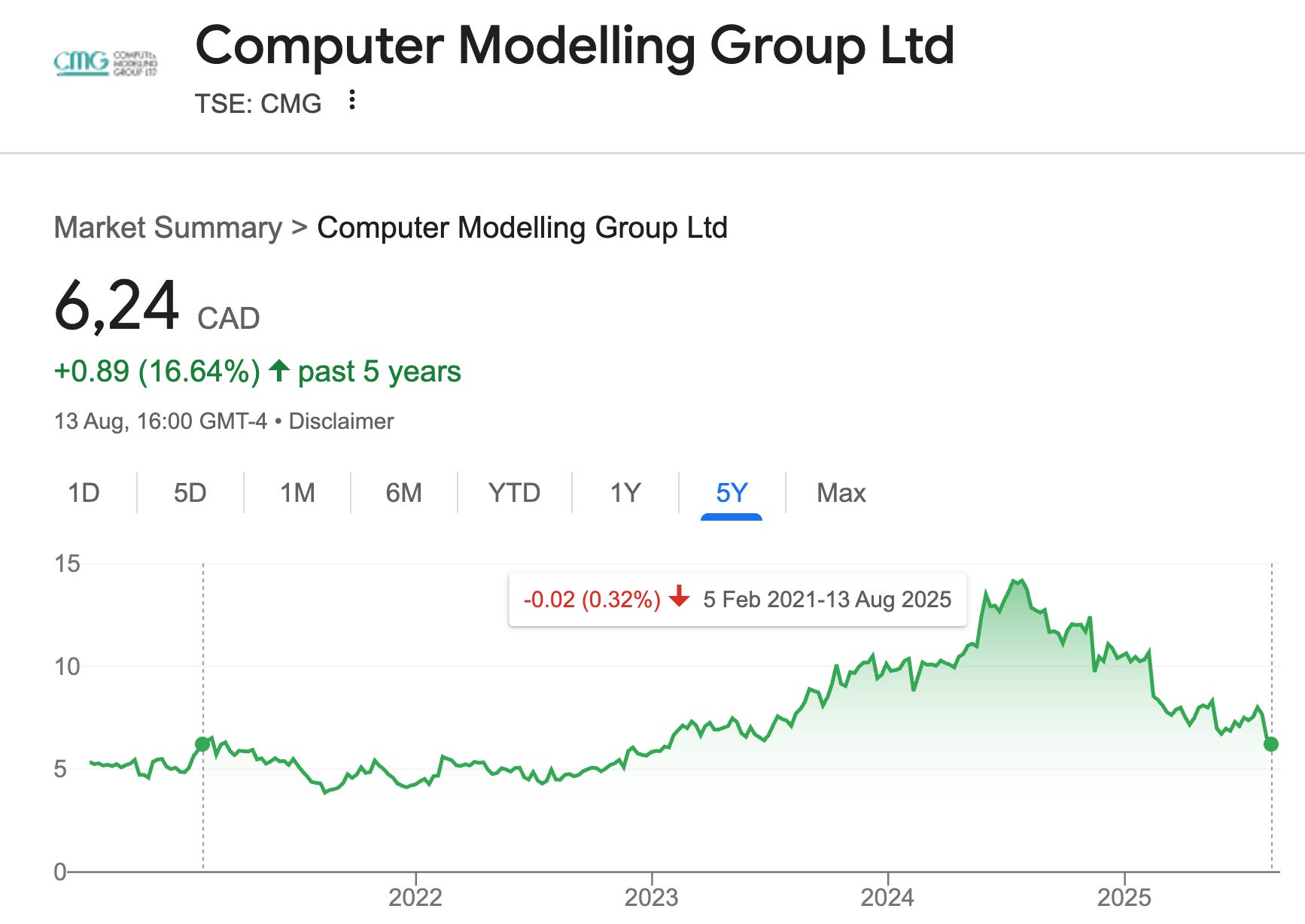

I’ve been following Computer Modelling Group for a while now, ever since Chris Mayer started buying and the stock started declining – now down 56% from its prior peak and now flat over four and a half years.

Clearly, the stock performance has been pretty lackluster. But the past few weeks felt like a line in the sand. Management is no longer sketching a direction – they’re naming it. “Act 2.” A different tempo, a different capital allocation stance, and a clearer blueprint for where the next increments of value will come from.

The two big tells are unmistakable: a now sharply articulated M&A framework (more on this below) and a decisive capital policy reset. Both sit inside a broader story about widening CMG’s playing field, tackling the “TAM constrained” bear case head-on, and doing it while navigating the kind of competitive and cyclical noise that inevitably shows up when you change gears.

In the shareholder letter, Pramod Jain made two moves that reframe the next few years. First, he tied the strategy to a single objective – deploy 100% of our available capital at attractive rates of return – and then backed that up by shrinking the dividend to free up cash for deals. Cutting the payout by 80% to $0.01 per share – with roughly $13 million of annual cash redirected to acquisitions – tells you Act 2 is not a slogan; it’s an operating posture.

“So since the last three years, or especially last twenty four months, we've deployed 73,000,000 of capital and have acquired $50,000,000 of revenue.“ Jain at the CG 45th Annual Growth Conference

Jain also laid out a taxonomy for the kind of businesses CMG will buy and how they’ll be made better under CMG’s roof.

But there is a lot of near-term turbulence. The letter was blunt about losing a long-standing reservoir customer due to “unusually aggressive discounting and competitive bundling by a global peer.” That stings, and it showed up the quarter and in the guidance (a mid-single-digit sequential dip in recurring revenue and pressure on adjusted EBITDA).

Still, the response was equally specific: more focus on strategic relationships, bundling with the seismic portfolio, acceleration with channel partners in the Eastern Hemisphere, and a newly created Energy Advisory Board to pull senior operators closer to the product roadmap.

This piece is my attempt to map CMG’s Act 2 – what’s changing, what isn’t, how the acquisition framework widens the runway, and where the execution risk truly sits. I’ll challenge the “TAM constrained” narrative, parse what the customer loss might mean, and outline what I’m watching over the next 12–24 months as proof points. You don’t need to buy every premise to learn something here. But if you care about how compounders are built – or broken –, CMG’s playbook is a live, teachable case.

Here’s what I’ll cover:

Why the “Act 1 vs Act 2” framing matters now – and why the dividend cut is more than optics, including how the payout reset and upcoming credit facility rebalance CMG’s capital stack toward high-IRR deployment.

Inside the new M&A framework – how Core, Platform, and Standalone expand the aperture.

Is CMG really TAM constrained? – a fresh look at the opportunity set given CMG’s size, the white space across the upstream workflow, and the credibility of expansion outside the core.

Operating system, not slogans – how CMG intends to create value post-deal.

The near-term noise we can’t ignore – what to make of the lost customer, organic recurring pressure, and the “unheard of” pricing dynamic from a global competitor, plus what management says they learned and how they plan to respond.

Private equity as a new counter-bidder – how increased PE activity changes price discipline, why CMG’s “trusted home” pitch to founders matters, and how recent founder retention supports that story.

The scoreboard I’ll track in the next 12–24 months

✅ Want the full experience?

Become a paying subscriber to read the rest of this post and get access to all of my other research, including valuation spreadsheets, deep dives (e.g. LVMH, Edenred, Digital Ocean, or Ashtead Technologies), and powerful investing frameworks.

Annual members also get access to my private WhatsApp groups – daily discussions with like-minded investors, analysis feedback, and direct access to me.

Choose your level of commitment and unlock your next edge.

PS: Using the app on iOS? Apple doesn’t allow in-app subscriptions without a big fee. To keep things fair and pay a lower subscription price, I recommend just heading to the site in your browser (desktop or mobile) to subscribe.